CCJ - URNM : Waiting For Price Consolidation

2023-12-30 01:51:14 ET

Summary

- The Ukraine invasion and energy scramble in Europe has increased the need for clean and reliable electricity, leading to a resurgence in nuclear energy.

- Asia and China are leading a massive build-out of nuclear power plants, requiring a significant increase in uranium.

- The Sprott Uranium Miners ETF (URNM) is well-positioned to benefit from this trend with its holdings in uranium companies and physical uranium.

- However, the 55% gain in uranium prices may need time to consolidate.

Summary

The Ukraine invasion and subsequent scramble for energy in Europe substantially increased awareness and the need for clean, reliable, cost-effective electricity. Nuclear energy began to shake off its negative image and rapidly became the answer to the energy transition. Asia and China are leading a massive build-out with over 270 new power plants planned or proposed, i.e. China is going electric. This will require a considerable increase in Uranium, the substance that makes the nuclear reactor boil water that becomes steam that turns turbines that generate electricity. The Sprott Uranium Miners ETF ( URNM ) could be in the right place at the right time with the right asset mix.

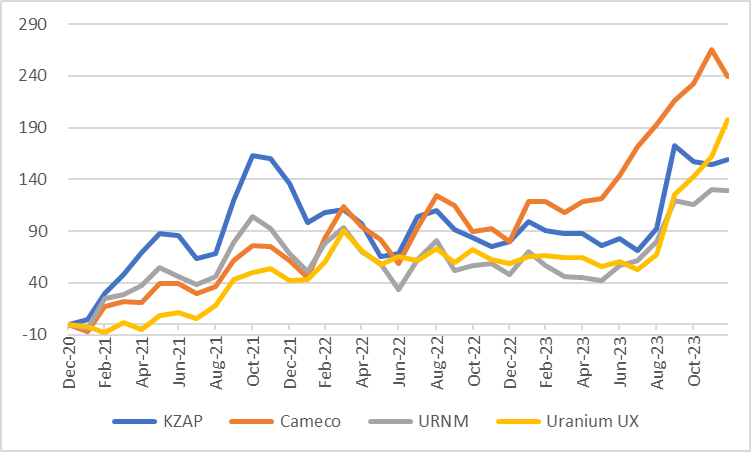

Performance

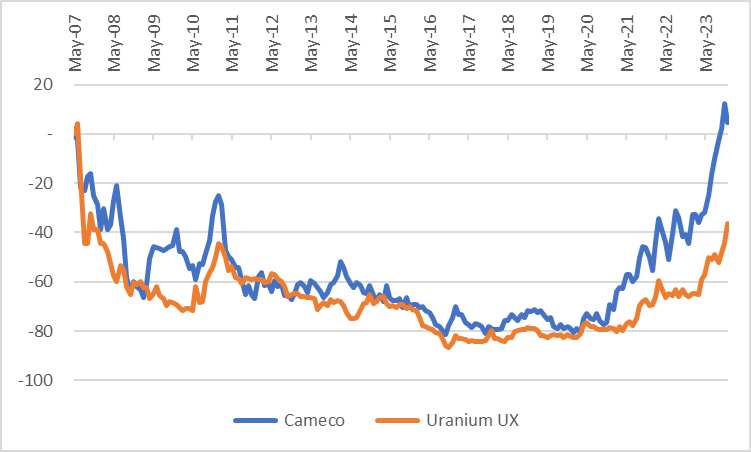

The ETF has moved in line with uranium prices via large holdings in Cameco ( CCJ ) and Kazatomprom and physical uranium via Sprott Physical Uranium Trust ( OTCPK:SRUUF ). The portfolio should continue to capture uranium demand and prices up or down.

{kind=link}

URNM Performance vs Key Holdings (Created by author with data from Capital IQ)

{kind=link}

Cameco and Uranium Prices (Created by author with data from Capital IQ)

The Case for Uranium

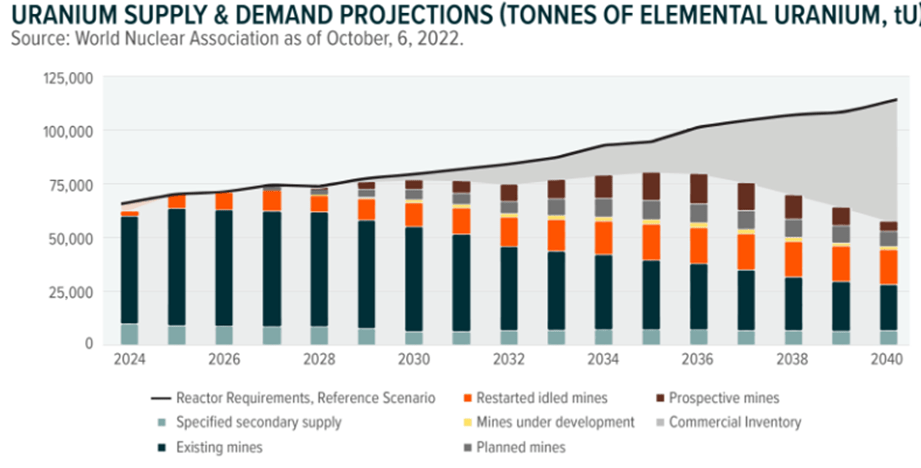

The investment case for uranium requires three key drivers. The first is a nuclear renaissance, despite the demand coming from Asia, both the US and Europe need to begin to build or at least talk about building new nuclear power capacity. The second driver is the uranium mining cost curve that requires over US$100lb for many new mines to be profitable. Uranium is an abundant mineral but is highly deconcentrated and requires massive ore mining and processing to gather a small amount, and this makes it expensive to mine. Finally, discipline at Kazatomprom (40% of global supply) and Cameco (20% supply) i.e. increasing production with demand and not flooding the market to retain share or deter new entrants.

{kind=link}

Estimated Uranium Demand & Supply (globalxetfs.com)

Asia Going Nuclear

Today, about 440 nuclear power reactors operate in 32 countries plus Taiwan, with a combined capacity of about 390 GWe. In 2022 these provided, 2545 TWh, about 10% of the world's electricity. That number may grow 50% in the next 15 to 20 years, driven by Asian capacity increase.

Asian Nuclear Power Plant Growth (Statista and World Nuclear Association)

Cost Curve and Demand/Supply

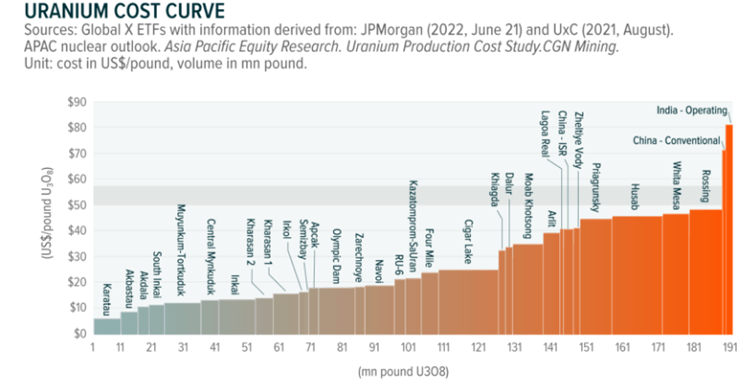

The ETF has 50% of the portfolio in pre-operation mines or prospecting companies, most are years from operations and looking for cost-effective production sources. The estimated breakeven for marginal capacity is around US$80lb, and thus new sources will likely require even higher prices. At the same time, demand from nuclear power plants, which need to replace fuel rods every 3 years, is slated to rise as Asia builds out and perhaps Europe and US expand. This may create a demand/supply imbalance that can only be solved with planned Uranium expansion.

{kind=link}

Uranium Cost Curve (globalxetfs.com)

Portfolio Overview

The ETS holdings are concentrated in three segments, producing uranium mining companies, a physical trust, and pre-operating or exploration companies. Using the consensus price target, I calculated an upside potential of 19% for the ETF. The largest asset, Kazatomprom, has an 11% target price. This company is the world’s largest uranium producer with a 40% share, is listed on the London Stock Exchange, and is controlled by the state of Kazakhstan.

The majority of the mining companies are listed on the Toronto exchange, a haven for pre-operational companies. It's interesting to see sell-side analyst coverage of small and micro caps in this sector. The price targets are based more on resource values on the ground vs revenue, cash flow (EBITDA), or earnings.

This ETF offers broad exposure across the uranium asset classes that should capture further price increases and nuclear plant capacity additions in the future.

URNM Consensus Price Target (Created by author with data from Capital IQ)

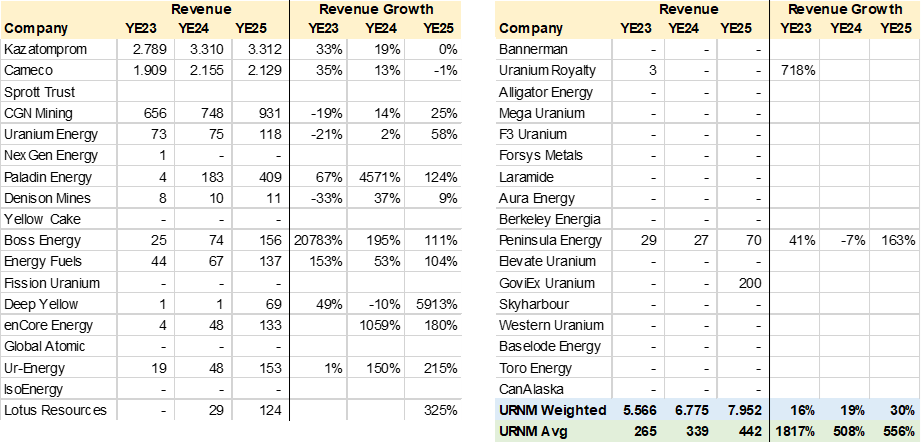

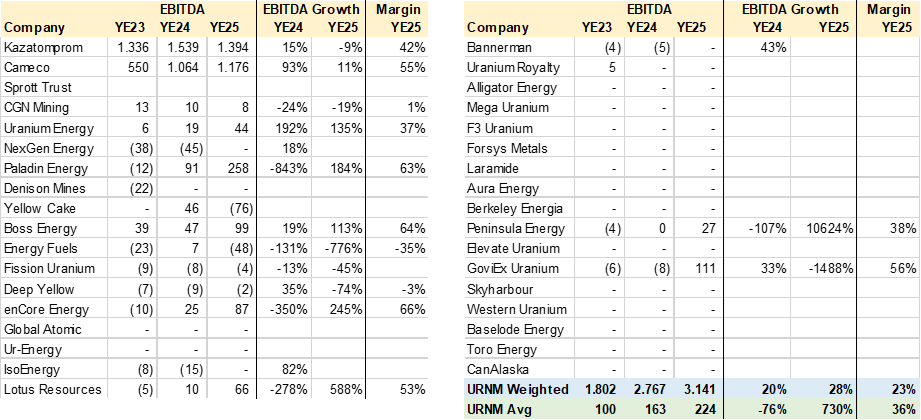

Revenue and EBITDA

The following two tables are consensus forecasts for Revenue and EBITDA of the ETF holdings. As can be seen, only three of 35 companies have relevant operating fundamentals, the remaining are in the start-up phase, conducting exploration or waiting for environmental licenses etc.

In the absence of further uranium price gains, can the mining companies continue to grow revenue and EBITDA. In the medium term yes, since realized prices, lag spot prices and the impact on margins should be fully felt in 2024. This portfolio has an estimated 19% revenue growth rate and 20% increase in EBITDA for 2024, which is consistent with flat price estimates going forward.

{kind=link}

URNM Consensus Revenue (Created by author with data from Capital IQ)

{kind=link}

URNM Consensus EBITDA (Created by author with data from Capital IQ)

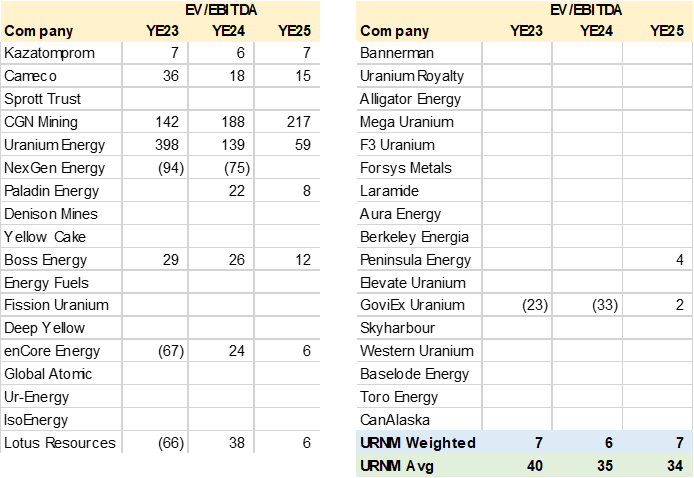

Valuation

Given the run-up in Uranium prices as well as Cameco and Kazatomprom the question of valuation is relevant. On consensus estimates the ETF is trading at 6x EV/EBITDA for year-end 2024 which is consistent with the two key stocks' historic valuations. Cameco has traded above 20x EV/EBITDA for most of the last 5 years, while Kazatomprom is around 7x. The discount is due primarily to country risk, despite the London Stock Exchange listing and good disclosure. The valuation of the ETF seems reasonable, but I would not factor in multiple expansions for continued performance, which will be driven by EBITDA growth and perhaps higher Uranium prices.

{kind=link}

URNM Consensus EV/EBITDA (Created by author with data from Capital IQ)

Consensus Forward EV/EBITDA (Created by author with data from Capital IQ)

Physical Uranium Assets

The ETF holds a 14% stake in Sprott Physical Uranium Trust, which provides investors with direct exposure to the mineral. The trust has acquired over 40m lbs. since July 2021 with a market value of US$5bn. If the Uranium price rises, so will the value of the trust and the ETF.

Sprott Uranium Trust (Sprott Uranium Trust)

Sprott Uranium Trust (Sprott Uranium Trust)

Conclusion

I rate URNM a Hold. The ETF holdings are providing direct and exponential exposure to over 60% of the world's Uranium production, as well as physical stock and future mining expansion and exploration. However, the holding rating is predicated by Uranium’s 55% price increase seen in 2023 which may consolidate in the medium term and perhaps provide a better accumulation level.

For further details see:

URNM : Waiting For Price Consolidation