XLU - UTG Has A Great Track Record But Utilities Aren't Exactly Cheap

2023-08-15 04:14:19 ET

Summary

- Reaves Utility Income Trust is a closed-end fund that focuses on utility stocks for income generation.

- Utility stocks are facing high valuations collectively, which may limit UTG's performance in the future as UTG relies heavily on capital gains for its dividend distributions.

- Investors with long-term horizon should still hold this as the fund is likely to continue to deliver good results in the long term.

Reaves Utility Income Trust (UTG) is a closed-end fund that specifically focuses on utility stocks for the purpose of income generation. The fund has been around for almost 2 decades and it has a strong track record which almost matches the performance of S&P 500 index ( SPY ) which not many actively managed funds can brag about. Still, utility stocks might be reaching high valuations collectively which might limit this fund's performance moving forward.

Utilities are typically considered a unique class of stocks which come with its own set of pros and cons. On pro side, utilities are almost recession resistant because people have to pay their utility bills no matter what and many of them enjoy a near monopoly status. Also, utilities can generally raise their prices to match the inflation rate so the income portion is somewhat protected from the effects of inflation. On a negative side utilities are highly regulated, their employment force is typically unionized and there is very little room for them to grow with the exception of price hikes and population gains where they operate. People typically invest in utility stocks for predictable, stable dividends that also tend to be on the higher side of the yield but lately yields haven't been that high either. Not long ago one could expect close to 5% dividend yields from utilities sector ( XLU ) but these days 3% is considered high yield for most utility stocks due to their stretched valuations.

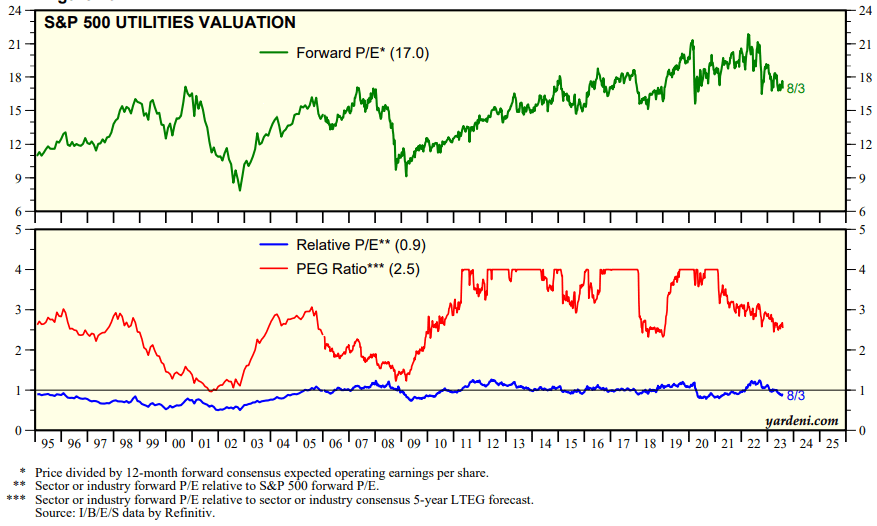

According to Yardeni, utilities sector as a whole currently trades at a forward P/E of 17 and PEG ratio of 2.5 which doesn't necessarily put it at an extreme valuation but still puts it closer to the higher end of its historical average than the lower end. To be fair, the current forward P/E is much lower than what it was in the beginning of 2022 which was 21 at the time and PEG ratio is much lower than 2021's almost 4 though it is higher than the sector's historical average of 2.

Utility sector's valuations (Yardeni)

{kind=link}

The fund has a total of 46 holdings and top 10 holdings account for 44% of its total weight. The fund's biggest holding is BCE ( BCE ) which is down -16% year-over-year and supports a dividend yield of 6.6% which is rich even for a utility stock. Duke Energy ( DUK ) is another notable holding of UTG and it is down -13% year over year which allowed the stock's dividend yield to rise to 4.4%. NextEra Energy ( NEE ) which focuses more on clean energy solutions recently got punished heavily by investors but it remains a rare play among utilities with its growth story. The stock has a dividend yield of 2.7%.

UTG's top 10 holdings (Seeking Alpha)

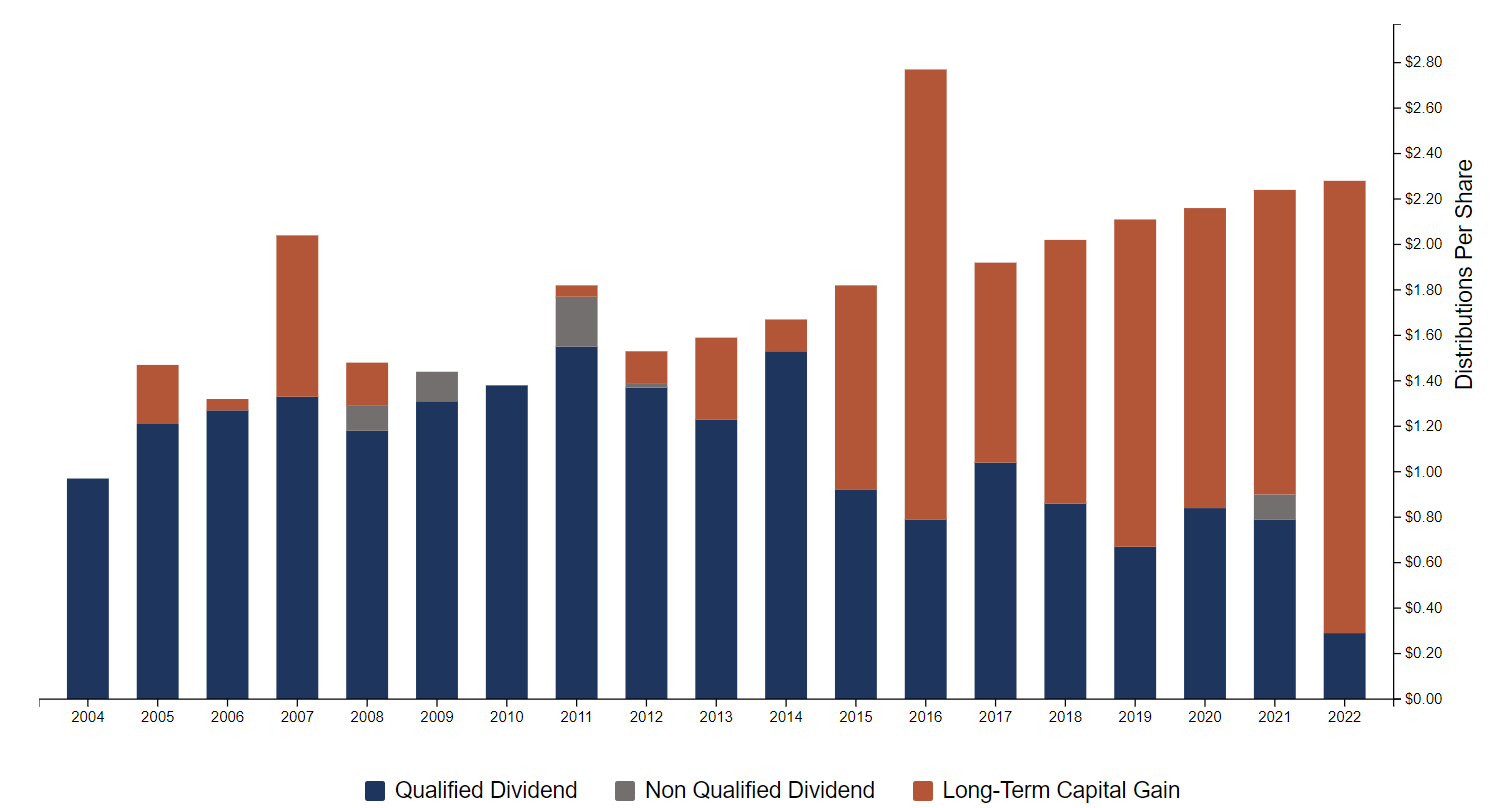

So how does UTG pay a dividend yield of 8.4% not to mention hiking this dividend on yearly basis when most of the fund's holdings pay much less than that? In addition to passing on the dividends it receives from its holdings, the fund also uses a mix of capital gains. For tax purposes, the fund tries to make most of its distributions from long-term gains and rarely resorts to short term gains but this is also expected since the fund's holdings don't change much from year to year (after all there are only so many large utility stocks to pick from) and most of the fund's holdings have been held for many years which means it can easily create long term capital gain distributions by simply offloading some of its stock that it's been holding for a long time.

UTG's capital distribution history (Reaves)

{kind=link}

Still, the fund has been and will be relying heavily on capital gains for much of its distributions moving forward. As you can see in the chart above, between 2004 and 2014, much of the fund's distributions came from qualified dividends it received from its holdings but since then, the role of capital gains in total distributions kept growing and growing to a point where the fund's actual dividend income was negligible in the last couple years. This means investors buying this fund will buy with an understanding that future dividend distributions will rely on capital gains. Utility stocks had a great rally up until the end of 2019 but their stock performance has been choppy since then. If utility stocks don't start rallying soon, this could put pressure on UTG's future dividends but we can also expect limited share price appreciation from utility stocks given their current valuation.

In addition the fund also uses leverage to maximize income for shareholders. In its latest semi-annual report, the fund says that its leverage was 24% of its net assets but this doesn't mean that the fund's leverage rate is only 24%. Think of it like this, for each $100 million the fund holds in assets, $24 million was leverage which means $76 million was the principal amount. This gives us a leverage ratio of 32% when we divide $24 million by $76 million. This kind of leverage is very typical for CEFs and not necessarily harmful as long as the fund can keep its interest expenses low, especially for sectors like the utilities sector where volatility is low in general. The fact that the management is keeping its leverage rate relatively low tells me that they don't believe utility stocks are compellingly cheap at the moment.

Since utilities are often seen as an income play, investors have to often look at bond rates to see if they are overpaying or underpaying for these stocks. When bond yields are near zero, utility yields of 3.5% look juicy but when short term bonds (which are considered virtually risk-free) yield 5.5%, they don't look so cheap anymore. Current high bond yields are another factor that might limit upside in utility stocks for the foreseeable future.

All in all, UTG is a good fund with a solid track record of delivering high yield dividends, dividend growth and strong total return that is comparable to that of the overall market. Meanwhile, the fact that there is limited upside in utility stocks and how UTG relies heavily on capital gains for dividends might have a negative impact on future dividends and future total returns of the fund especially for the next year or two. Investors with much longer term horizons shouldn't be bothered by this and continue holding though.

For further details see:

UTG Has A Great Track Record But Utilities Aren't Exactly Cheap