VLD - Velo3D: 5 Problems It Must Solve To Succeed

Summary

- While the company remains under duress, if it's able to execute on its strategy, it has the potential, over time, to surprise to the upside.

- It recently announced it'll exceed prior revenue guidance for Q4 of 2022.

- 5 things to watch in order to identify whether or not the company is making progress.

- The company is going to have to turn things around fairly quickly in light of its ongoing cash burn.

The last year and quarter have been challenging for Velo3D, Inc. ( VLD ), a company that produces and sells 3-D printers to companies that produce their own key metal parts, as it burns cash at a quick pace, and its losses continue to mount in face of supply chain constraints, excess inventory, lack of sector diversification, and high input costs.

On the positive side, the company recently announced it'll beat prior revenue guidance for the fourth quarter of 2022, although it remains to be seen if it's only recovering past business that was delayed in the third quarter, or if it's new business it has won; I consider that important because of how it relates to momentum.

After hitting a double-bottom of approximately $1.50 per share on December 28, 2022, the share price of VLD has doubled, but with no real catalysts driving the upward move. That suggests to me the company is primed for a correction, even though it announced on February 6, 2022, that revenue was going to exceed prior guidance.

{kind=link}

In this article, we'll look primarily at the challenges the company faces and what it's attempting to do to solve them, along with some of the recent numbers that reinforce the fact it must start to reduce costs and improve the bottom line if it has a chance at succeeding over the long haul.

Some of the numbers

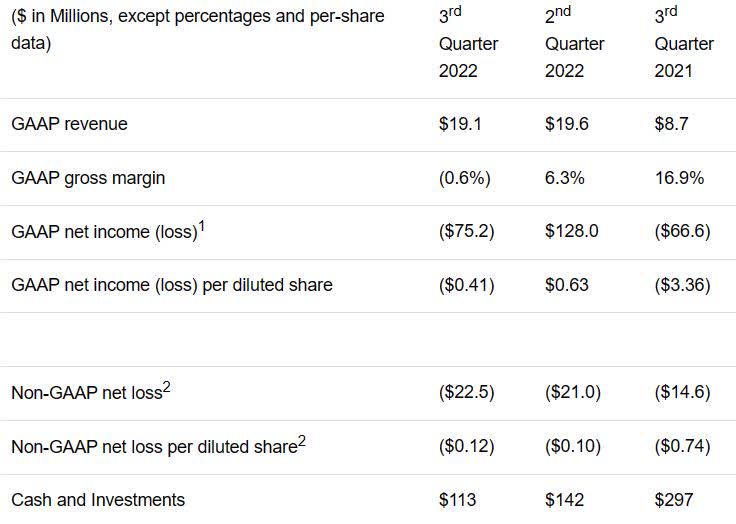

In the third quarter of 2022, the company generated revenue of $19.12 million, missing by $5.12 million, but up 119 percent year-over-year.

Gross margin in the reporting period was -(0.6%), compared to gross margin of 16.9 percent in the third quarter of 2021, and 6.3 percent in the prior quarter.

Net loss in the third quarter of 2022 was -$(75.2) million, or -$(0.41) per share, compared to a net loss of -$(66.6) million, -$(3.36) per share in the third quarter of 2021.

{kind=link}

Management stated that $47.5 million of the loss came from "the fair value of warrants and contingent liabilities."

The company had cash and investments of $113.00 million at the end of the third quarter of 2022.

At the end of the reporting period , the company had approximately $27 million undrawn on its $30 million revolver, and a little over $10 million left on its equipment financing facility.

Cash used in the third quarter of 2022 was $29.00 million, down from the $44.00 million used in the prior quarter.

In the third quarter earnings report, the company lowered guidance for full year 2022 from $89.00 million to a range of $75.00 million to $80.00 million.

Upwardly revised revenue guidance

On its third quarter earnings call, management guided for fourth quarter revenue to come in at a range of $24.00 million to $29.00 million, based upon backlog at the time. For all of 2022, the company guided for revenue to finish in a range of $75.00 million to $80.00 million, citing supply chain uncertainty, shipment delays, and the ongoing initial run of the Sapphire XC 1MZ system.

Gross margin for the fourth quarter was projected to be in the range of 5 percent to 10 percent, not including inventory adjustments and non-recurring items.

On February 6, 2022, the company upwardly revised its revenue guidance for the fourth quarter of 2022, and full year 2022. For the fourth quarter of 2022 revenue was now expected to come in at $29.00 million to $30.00 million, with gross profit guided to be in a range of 5.0 percent to 6.0 percent for the fourth quarter.

Revenue for full year 2022 was upwardly revised to be in a range of $80.00 million to $81.00 million.

At the end of fiscal 2022, the company projected that it would have cash and investments of $81.00 million, $32.00 million less than it than the $113.00 million it had at the end of the third quarter, pointing to significant cash burn in the reporting period.

Even though there was a positive response from the market concerning the upwardly revised guidance, in fact, at least as it relates to full year 2022 revenue, it only brings it back to where it was before the downward revision it gave in the third quarter report, and is still well under original guidance of $89.00 in revenue for all of 2022.

It's also concerning to see how much cash is left after the third quarter.

Another key factor to watch is where gross profit and gross margin stand with the modest increase in revenue. It must show it's executing in a way that is leading toward profitability in order to sustain the general price range the company has been moving within recently. If not, it's going to take a big hit in my opinion as a result of an upward move in its share price with no meaningful catalyst driving it.

Five things to watch in the quarters ahead

There are five things I see as being vital to the performance of the company if it's to sustainably grow in 2023 while improving its bottom line. They include solving its supply chain issues, sector diversification, sales and marketing, revenue growth while cutting expenses, and slowing down on cash burn.

Supply chain

The supply chain remains an issue for VLD, even though it has started improving in the recent past. In the third quarter of 2022, the company was partially held back by a shortage of key components in its system-level electronics in particular. Not only was there a shortage of parts, but when the parts were sent, they were too late in the reporting period.

Among the steps the company is taking to improve the process is, first, to expand its supply chain team in order to meet the challenges of component shortages the company has faced.

Another major step the firm has taken is to work closer with existing and new vendors in order to manage the supply chain better. Part of that improvement is associated with staggering the delivery of parts in order to better match its development schedule while shrinking the size of its inventory levels.

Sector diversification

It has been known that VLD has been at risk because of its heavy exposure to the space sector, but according to management that is starting to change, as it has added customers from the automotive, aviation, defense, energy and hypersonics industries.

Although this will take time to have a strong impact on the performance of the company, it is laying the foundation for future growth while lowering its risk profile.

Sales and marketing

The company stated it believes its sales and marketing unit is now fully staffed and should be positioned to execute on its next growth phase.

If this is an accurate assessment of the situation, it means not only should the company's spending in that segment should be largely over, but that when combined with assumed revenue growth, should result in improvement in the top and bottom lines of the company.

Management believes the improvement in bookings and backlog in the third quarter reflect the investment in sales and marketing, as well as the expansion that brought it beyond the space sector.

Bookings in the third quarter jumped to $27.00 million, up 50 percent from the prior quarter, bringing the backlog to a total of $66.00 million.

Revenue growth while cutting expenses

While revenue growth is an obvious necessity for the company, a major challenge it faces is in being able to do so while lowering expenses, something it has yet to prove it can execute on.

The dismal gross margin in the quarter was attributed to a delay in customer system shipments to the fourth quarter, along with inventory adjustment charges that exceeded expectations in relationship to the production of its Sapphire XC product. Margin in the third quarter was also impacted by an increase in deliveries of lower margin products.

Slowing down cash burn

With cash and cash equivalents dropping to $81.00 million from $113.00 million in the prior quarter, it suggests to me the company is still struggling to slow down cash burn, which is vital for the company to get a handle on.

The issues mentioned directly above are the way to cutting back on expenses, and the company must start to execute in the near term in order to stop the rapid burning of cash.

If it doesn't do so in the next couple of quarters, it could find itself scrambling to find funding for operations if it doesn't start to show significant improvement on the bottom line.

Conclusion

VLD has a lot of problems to solve if it's going to prove it's on a clear path to profitability. Its cash burn is higher than expected, according to its latest press release, when measured against management commentary on its sales and marketing team being in place and steps it's taking to mitigate its supply chain and inventory issues, which should have shown signs of improving as reflected in its cash burn.

It appears to be making progress in regard to sector diversification, but how that will have an impact on margins in the long term has yet to be determined.

The company seems to be solving some of its revenue challenges, but it must be able to boost revenue while lowering expenses if it's going to be successful in the near and long term.

Until it proves it can execute on its strategy, this is a company I would avoid, especially after the recent boost in its share price.

For further details see:

Velo3D: 5 Problems It Must Solve To Succeed