VLD - Velo3D: End-Market Strength

2023-10-24 10:00:00 ET

Summary

- Velo3D's business is holding up well relative to most additive manufacturing peers, which is probably a result of the company's large exposure to the defense industry.

- Despite this, weaker-than-expected demand and executive turnover have weighed on Velo3D's stock in recent months.

- Velo3D's stock could face further declines, as the stock is still relatively expensive and demand headwinds are likely to be ongoing.

Velo3D ( VLD ) has had a difficult 3 months, on the back of weaker than expected growth and executive turnover. The stock is down roughly 42% since I last wrote about the company, and could decline further if economic conditions weaken, interest rates rise further, or growth continues to disappoint.

Longer-term, Velo3D is well positioned due to the rising use of additive manufacturing in the production of high-value metal parts, and the fact that Velo3D's technology enables the production of parts with complex internal geometries. This is unlikely to matter in the near-term though, as demand headwinds are likely to be ongoing and investors have little appetite for unprofitable, small cap companies.

Market

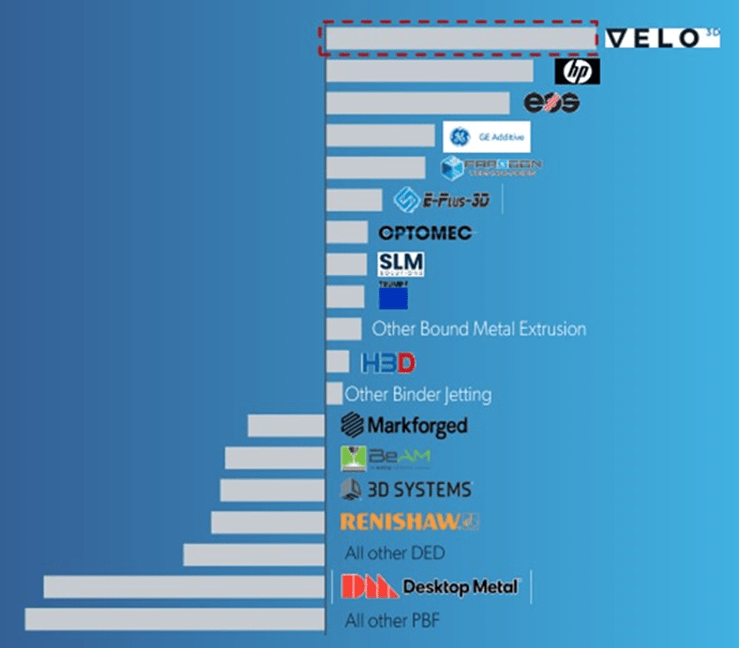

Velo3D’s business is holding up reasonably well in a difficult operating environment, as exhibited by its leading growth amongst additive manufacturing companies, albeit off a small base. Velo3D was the number two supplier of metal additive manufacturing systems at the end of the first quarter of 2023.

Figure 1: YoY Change in Metal AM Hardware Market Share (source: Velo3D)

{kind=link}

Some of this relative strength is due to the appeal of Velo3D’s differentiated products, but it should also be noted that Velo3D has different end market exposure compared to many metal additive manufacturing companies. In particular, Velo3D's reliance on sales to defense companies is currently supporting growth.

Velo3D believes its technology offers a number advantage in key verticals:

- Space – improved performance / ability to rapidly implement design changes

- Defense – reduced lead times / increased readiness / weapon development

- Aerospace – supply chain efficiency / cost reduction

- Contract Manufacturing – improved performance / shorter part lead times

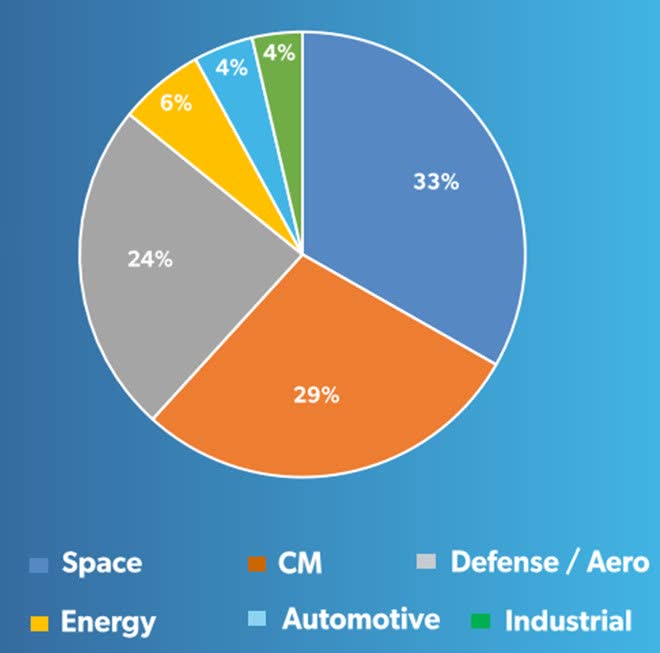

Figure 2: Velo3D LTM System Revenue by End Market (source: Velo3D)

{kind=link}

Velo3D

Velo3D offers differentiated metal additive manufacturing technology aimed at the production of high-value metal parts. This has led to adoption in areas like the space, defense, commercial aviation, and energy industries. The company offers an integrated end-to-end metal AM solution which enables customers produce high-quality and complex parts without support structures. Support free printing is enabled by a combination of software, hardware and printing processes. This appears to be about process knowledge as much as specific hardware or software capabilities.

Defense has unsurprisingly been an area of recent strength for Velo3D, accounting for more than 35% of Velo3D’s first half system revenue. Defense is also Velo3D's fastest growing end market. There were booking delays in the second quarter which are expected to have an impact on the company's second half revenue though.

Velo3D landed 3 new defense contractors in the second quarter and now has 9 in total. Defense represented only 5% of Velo3D’s customer base at the start of 2022 and now constitutes close to 20%. Adoption is being driven by the ability of Velo3D’s technology to reduce replacement part lead times and enable the development of new weapons.

Scramjets for hypersonic weapons is one potential application that is receiving support through the Growing Additive Manufacturing Maturity for Airbreathing Hypersonics (GAMMA-H) initiative. A scramjet is a type of jet engine where combustion occurs in supersonic airflow. Scramjets do not have moving parts and rely on vehicle speed to compress incoming air for combustion. These types of engines are far more efficient than turbofans or ramjets at extremely high speeds. Traditional manufacturing methods are unable to meet the complex specifications that hypersonics require. Additive manufacturing allows scramjet components to be made from high-temperature metals in a way that eliminates the need for welds or brazing joints.

Contract manufacturing is also a core vertical for Velo3D. Velo3D has over 200 parts customers through its contract manufacturing supply chain and expects to add additional parts customers in the second half of the year.

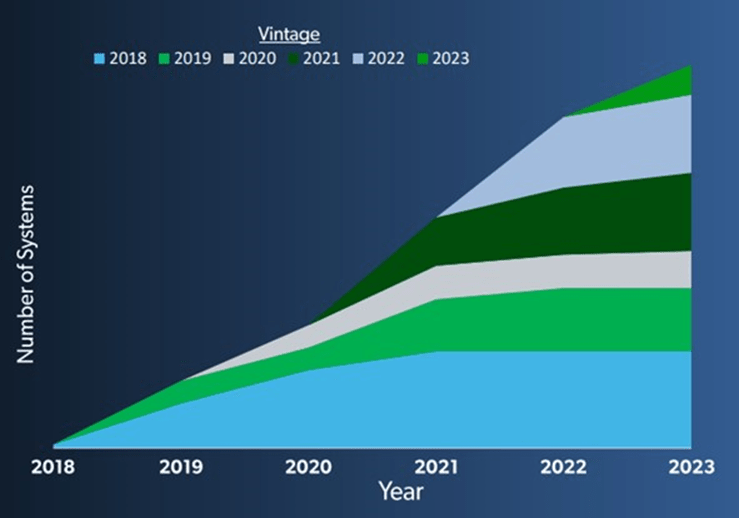

At the end of the second quarter, Velo3D had over 100 systems in the field and around 40 customers. Growth has reportedly been driven primarily by existing customers adding machines to increase capacity and address new use cases. Over 50% of Velo3D’s customer base has more than one system, with 20% owning 4 or more systems. Existing customers are expected to contribute roughly 50% of revenue over the long run.

Figure 3: Number of Systems by Velo3D Customer Vintage (source: Velo3D)

{kind=link}

The failure of demand to meet Velo3D's lofty expectations in recent quarters has been compounded by executive turnover. Velo3D’s CFO resigned in September without a permanent replacement in place, which can hardly be interpreted as a positive. Velo3D’s VP of Finance has been appointed acting CFO with the current CFO staying on in a transition capacity until November 7 th , 2023.

Financial Analysis

Velo3D’s first quarter revenue was 25.1 million USD, a 28% YoY increase. Recurring revenue was down due to a one-time charge related to a customer concession on system lease terms. Printer revenue was up 32% YoY and support services revenue was up 74%.

Table 1: Velo3D Revenue ('000 USD) (source: Created by author using data from Velo3D)

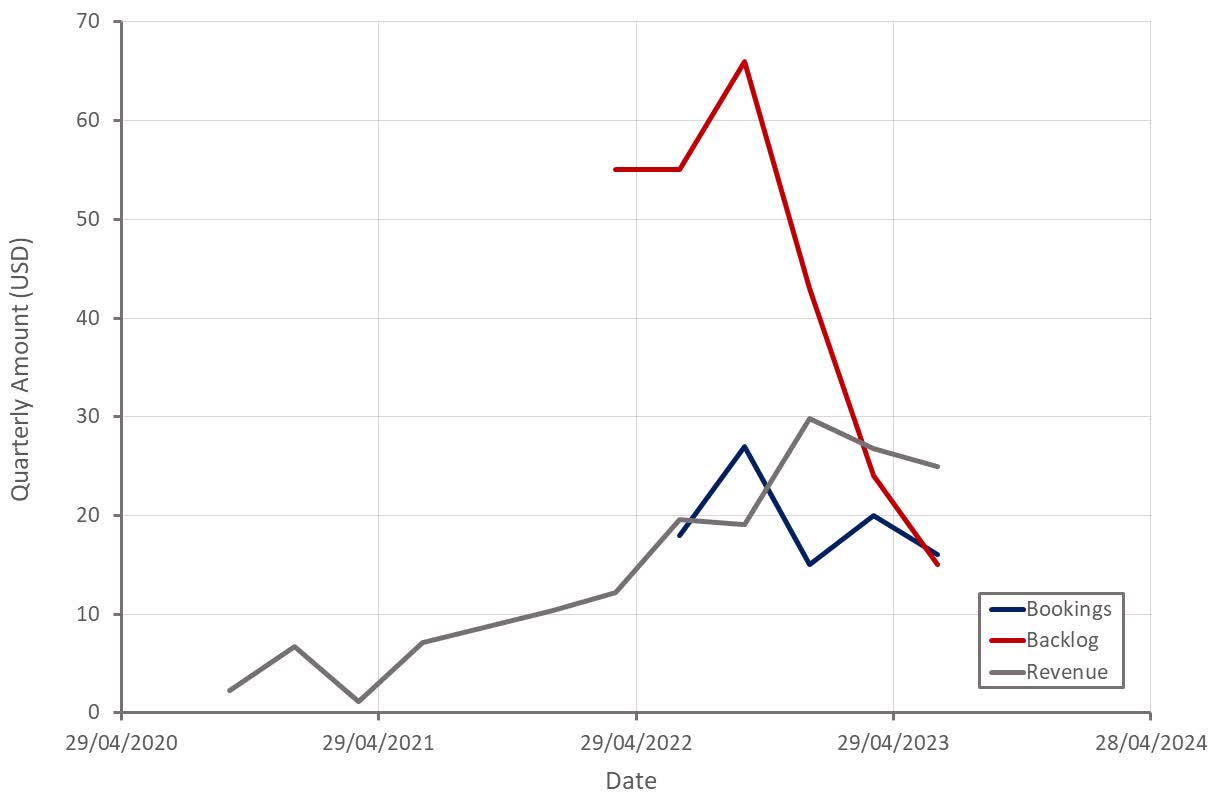

Second quarter bookings were only 16 million USD, with booking weakness driven primarily by delays amongst existing customers. This is demonstrated by the fact that new customer orders accounted for 90% of total bookings in the second quarter. Velo3D remains confident that delayed deals will close in coming quarters though. Velo3D’s backlog also continues to be an area of weakness, declining to 15 million USD at the end of the second quarter.

Second quarter revenue is expected to be the low point, with sequential improvement through the remainder of the year. Velo3D is currently guiding to 25-29 million USD revenue in the third quarter, suggesting roughly 41% YoY revenue growth at the midpoint. Full year revenue guidance is only 105-115 million USD, suggesting fourth quarter revenue growth of 4% YoY at the midpoint.

Figure 4: Velo3D Revenue (source: Created by author using data from Velo3D)

{kind=link}

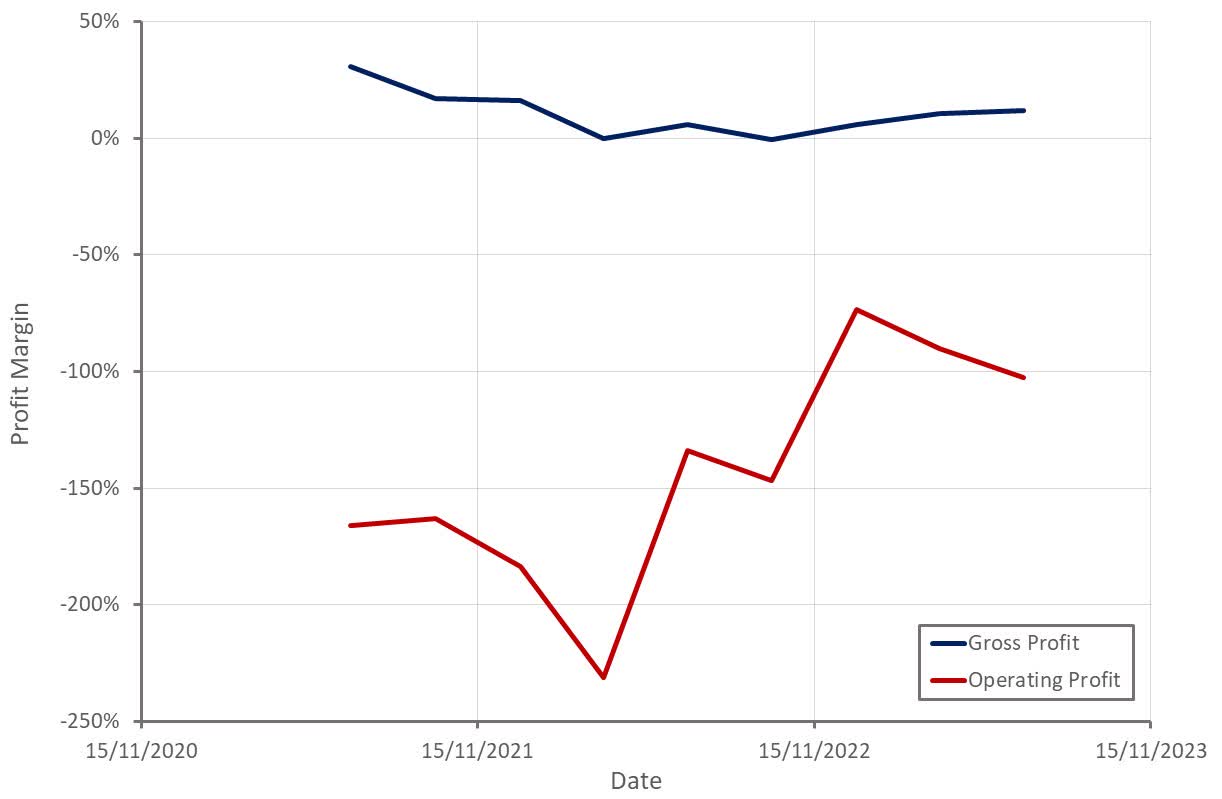

Velo3D’s gross profit margin in the second quarter was 12%, up 1% sequentially. This expansion was driven by lower material costs, increased production efficiency, ASP increases (mix shift) and overhead cost absorption. Gains were somewhat offset by the one-time recurring revenue charge and higher service support costs. Printer margins increased approximately 4% sequentially to 14.9%.

Velo3D is anticipating 14-18% gross profit margins in the third quarter of 2023 and is targeting 21-25% gross profit margins in the fourth quarter.

Second half margin improvements are expected to be driven by:

- Lower material costs as supply transitions to new, long-term contracts

- Reduced material inefficiency and scrap costs

- Normalization of recurring payment and service support revenue margins

- Greater production volumes leading to lower labor overhead and other factory costs as a percentage of revenue

- Labor and production efficiency

- Higher ASPs due to product mix shift

Increased operating expenses were a result of a 1.9 million USD increase in R&D expense, primarily related to material costs for a new product development program. This spend was an outlier that is not expected to be ongoing. This increase was partially offset by a small decline in general and administrative and sales and marketing expenses.

Velo3D is aiming to reduce non-GAAP operating expenses by 20% through Q4 2023, with OpEx expected to decline in each quarter through the rest of the year. Cash flows are also expected to be improve, driven by gross margin expansion and operating expense control.

Even with continued growth, gross profit margin improvements and a moderation in operating expenses, Velo3D is probably still at least 18 months off of reaching breakeven on an operating profit basis.

Figure 5: Velo3D Profit Margins (source: Created by author using data from Velo3D)

{kind=link}

While Velo3D's business has long-term potential, the macro environment has made liquidity a near-term concern. Velo3D raised approximately 16 million USD in the second quarter, comprised of 5 million USD of equity sales and 11 million USD of borrowing.

Velo3D also recently announced 70 million USD registered direct offering of senior secured convertible notes. The investor has also been granted the right to purchase up to an additional 35 million USD in aggregate principal amount of the notes within the next 12 months. The notes only have a 6% annual interest rate, but Velo3D must also pay 115% of the principal amount at the end of the loan term. The initial conversion rate is equivalent to 2.1 USD per share. Net proceeds are expected to be 66 million USD, with Velo3D intending to use roughly 22 million USD of the proceeds to repay outstanding debt. The remaining proceeds will be used for working capital, capital expenditures and general corporate purposes.

Velo3D now believes it has sufficient cash to finance the business through to cash flow breakeven. Based on the company's current growth rate and improvement in margins this expectation seems reasonable, but Velo3D could easily find itself in search of liquidity if growth stalls.

Valuation

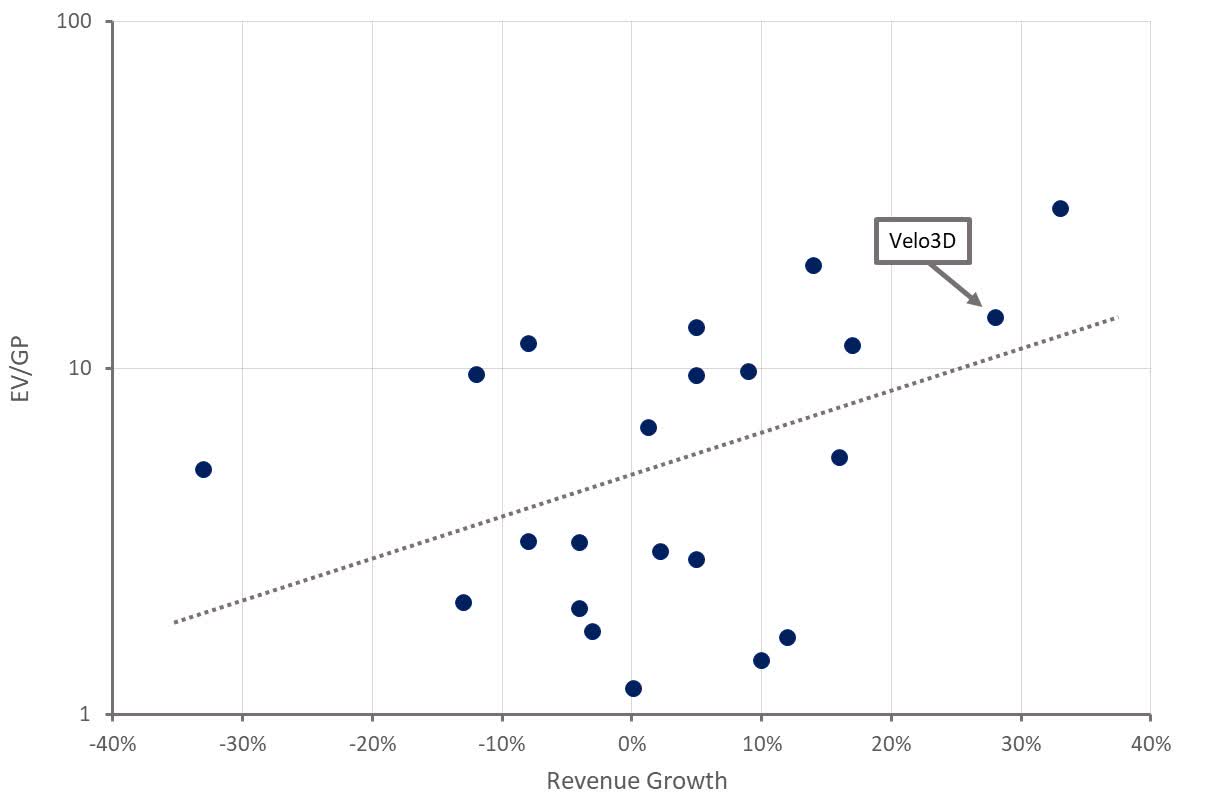

Velo3D trades on one of the highest revenue multiples in the additive manufacturing space. This is somewhat justified by Velo3D's high growth rate relative to peers and the fact the company has differentiated technology with integrated software and hardware. Demand from Velo3D's end markets has also been less impacted by high interest rates and macroeconomic uncertainty.

Enthusiasm should be tempered by the fact that the additive manufacturing market is fragmented, with a range of competing companies and technologies offering advantages / disadvantages across different applications. Hardware suppliers have also shown limited ability to capture value so far.

There is also currently limited investor appetite for unprofitable technology companies, particularly those that are heavily exposed to the manufacturing sector, and Velo3D's high valuation leaves the stock susceptible to further declines.

Figure 6: Velo3D Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Velo3D: End-Market Strength