VLD - Velo3D: Speculative Dip-Buying Opportunity

2023-07-05 17:38:14 ET

Summary

- I consider VLD a speculative buy due to its share price bottoming out.

- Risk remains high. VLD has been unprofitable and facing gradual decline in cash position since its SPAC merger.

- Despite these challenges, VLD has a proven track record with key clients such as SpaceX. Growth opportunities remain solid, and cash burn may slow down in FY 2023.

Velo3D (VLD) is a leading manufacturer of metal 3D printers / 3DP for additive manufacturing / AM, specializing in advanced laser powder bed fusion technology. Their solutions enable the production of complex metal parts with high precision, quality, and reliability.

VLD went public through SPAC in 2021 and raised ~$274 million. VLD later reached an all-time high of ~$13 per share, though since then, shares price continued trending downwards. Today, it trades in the $2 range.

I rate VLD a speculative buy for now. The share price seems to have bottomed, creating a dip-buying opportunity. As it stands, VLD is a high-risk high-reward opportunity. While VLD seems unlikely to reach cash flow positive this year, growth continues to be attractive, demonstrating solid demand for its 3DP solution. Slowdown in cash burn and improving gross margin are also possible.

Risk

Despite strong bookings growth that has reflected strong demand, VLD continued to see challenges across profitability and cash flow generations in Q1.

{kind=link}

stockrow

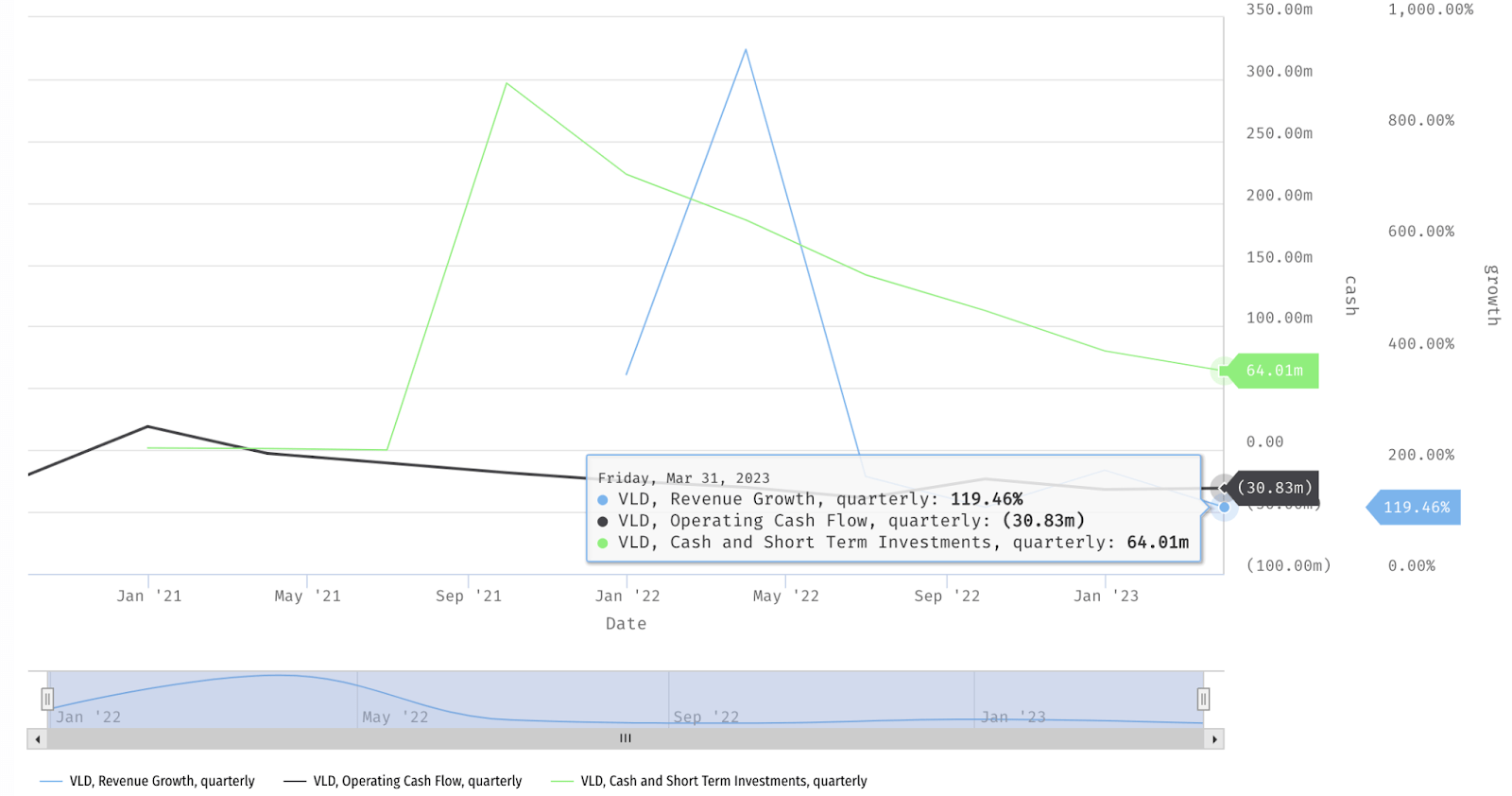

Cash position continued its gradual decline from ~$223 million post-SPAC merger around two years ago to ~$64 million as of Q1 2023, and at the current rate, VLD will need to aggressively deliver on its FY 2023 operational efficiency plan to extend the runway. Since going public, VLD has been relying largely on the capital raised from the SPAC transaction to sustain its business operations.

Over the same period, VLD has not been able to turn cash flow positive. Operating cash flow / OCF has been in the negatives, and while VLD may have done its best in keeping OCF burn rather steady, OCF seems still a bit further from breakeven. In Q1, OCF was -$30.8 million. Given the situation, I would expect VLD to continue to endure a few quarters of tightening and only reach OCF or EBITDA breakeven realistically sometime mid-FY 2024.

{kind=link}

VLD's presentation

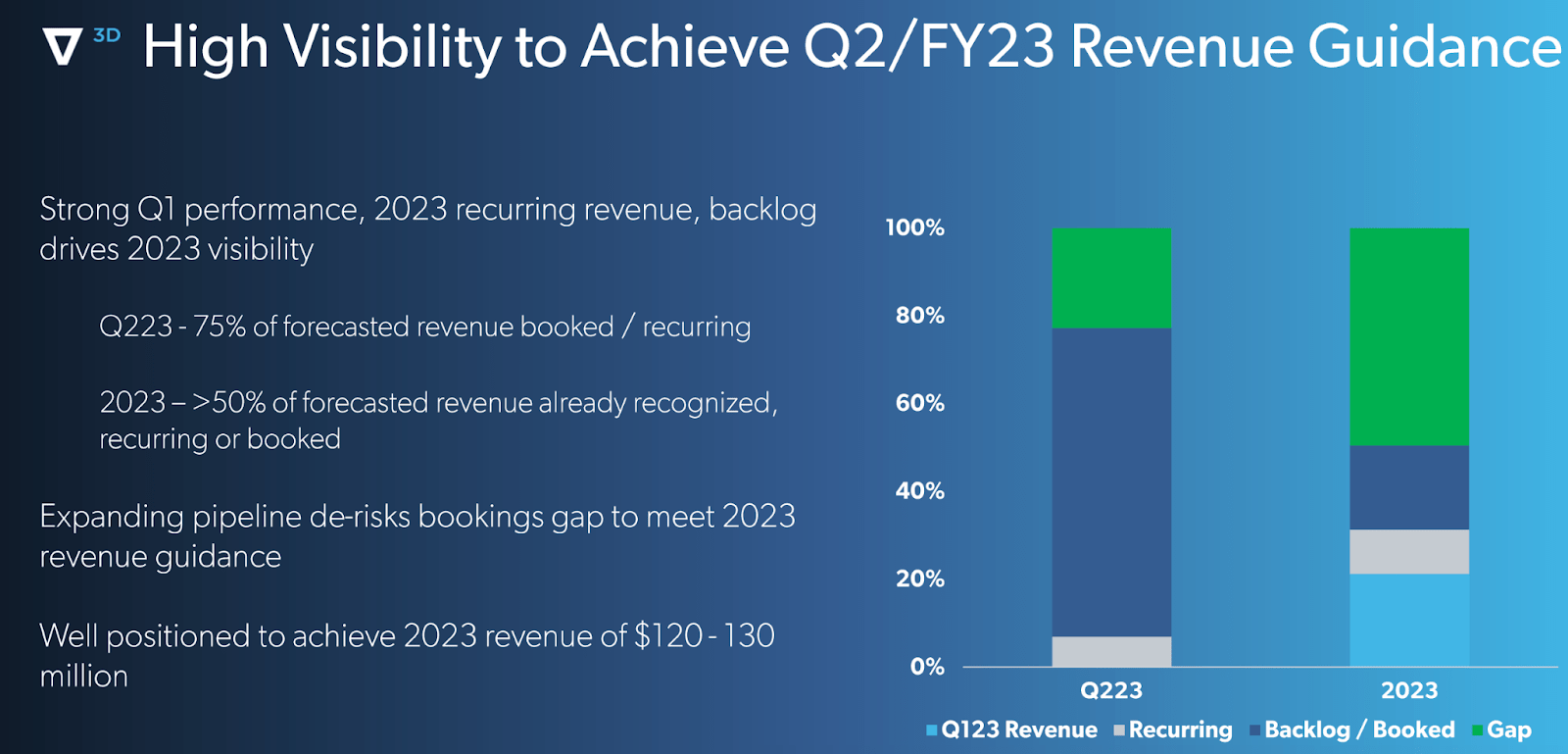

While operational efficiency may help drive costs down, another key part that drives margin expansion is revenue growth. However, there could be two key risk factors that make VLD's booking projection appears rather unreliable. The first one has to do with the high upfront cost of a 3D printer / 3DP ( around $600k as per info from 2018), which may slow down and even cause incomplete bookings on the customers’ end if they fail to secure financing, as we have seen in Q1:

Finally, as Benny mentioned, bookings for the quarter were up 30% to $20 million, and our backlog now stands at $24 million. The decline in backlog is primarily related to adjustment we made to remove an order, which has not been canceled, but where the customer has not demonstrated adequate progress in securing financing to complete the purchase. We therefore believe it's prudent to remove it from backlog at this time.

Source: Q1 earnings call.

The second one is bookings concentration risk. As a company building an emerging technology addressing a highly niche problem in design and manufacturing, it is typical for VLD to have quite a concentrated customer base who understand VLD’s value proposition and can meet VLD’s minimum order requirement for its 3DP, if any. We learned how an incomplete booking from just a single customer could easily result in a $15 million decline in the backlog - almost 80% of the total value - in Q1:

Yes. The order has not been canceled. It's just that – it's been out there for a while and the customer hasn't demonstrated enough progress in getting financing, so we thought that we should remove it in the interest of conservatism. But obviously if the customer gets financing, it could certainly come back. And the – the order is approximately 80% of the decline in backlog were about just a smidge under $15 million.

Source: Q1 earnings call.

While VLD obviously will try its best to expand and diversify its sales pipeline further, I continue to expect higher uncertainties on bookings as VLD seems to have been shifting its product mix towards more expensive variants, Sapphire XC and Sapphire XC 1MZ systems , to increase ASP / average selling price in an effort to improve gross margin.

Catalyst

On the flip side, there appears to be an attractive TAM in Additive Manufacturing / AM. AM is projected to be a $70 billion market by 2030. While it is still a nascent space to date, I continue to see future growth opportunities from AM applications across more industries (e.g. medical or oil and gas) in more geographies.

I believe that VLD is also well-positioned to capture those opportunities. So far, VLD has a proven track record in landing key clients such as SpaceX, Honeywell, and Honda, which has demonstrated the superiority of its 3DP solution. VLD’s breakthrough 3DP is used to print critical parts for one of SpaceX’s rocket engines, for instance, and SpaceX also suggested that VLD is at least five years ahead of its closest competitors in terms of innovation.

{kind=link}

VLD's 10Q

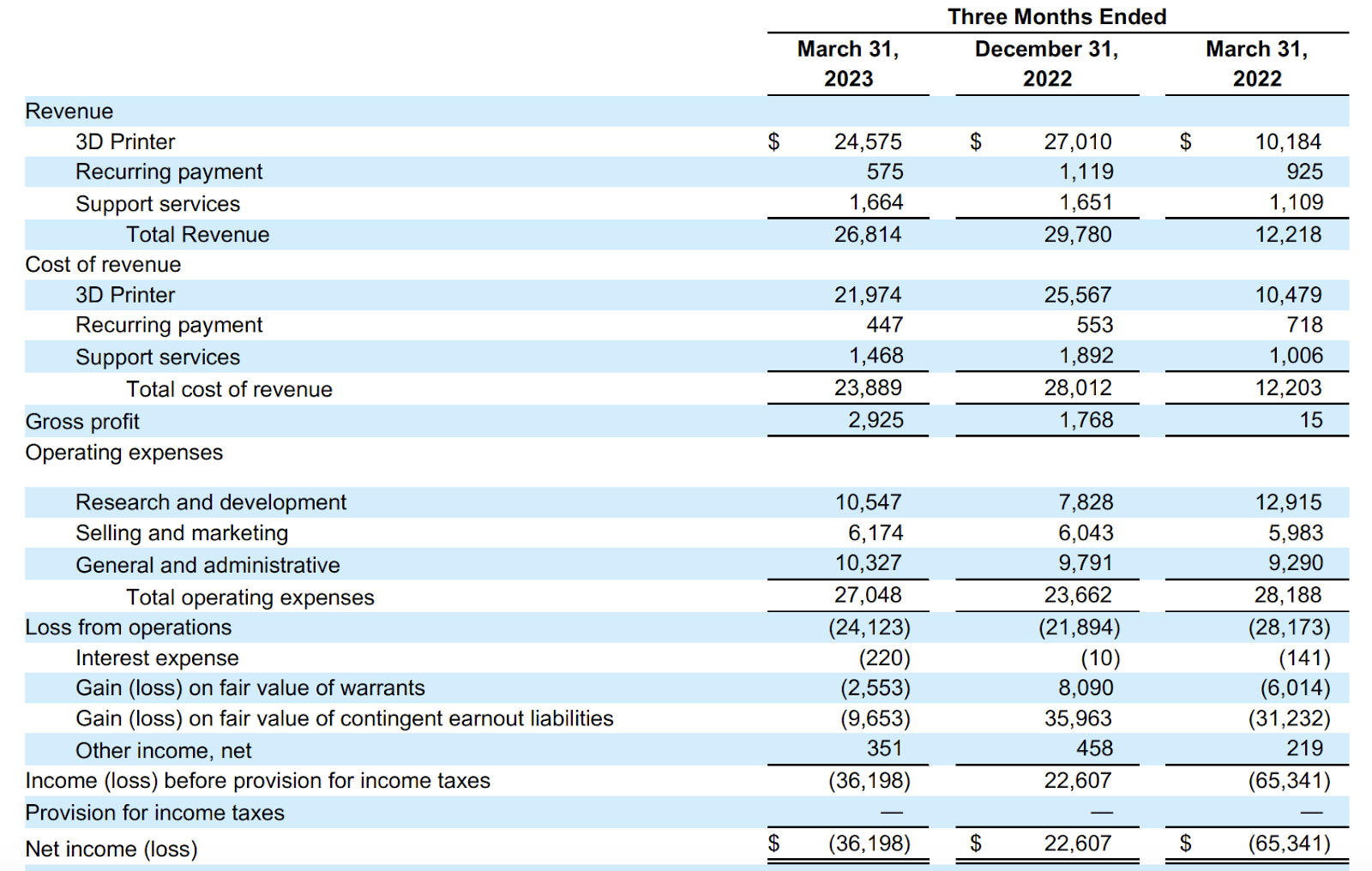

Furthermore, though VLD is unlikely to see cash flow positive this year in my opinion, I would probably expect annual cash burn to ease off due to the improvement in BOM / Bill of Materials, which may help reduce production cost per machine and expand gross margin. VLD also seems to be on the right track for this as highlighted by the gradual improvement in 3DP gross margin since last year. In Q1 last year, VLD barely turned a profit on its 3DP business, where gross margin was -3%. However, gross margin later turned positive and continued to expand to ~5% and ~11% in Q4 2022 and Q1 2023 respectively.

Valuation/Pricing

My target price for VLD is driven by the following assumptions for the bull vs bear scenarios of the FY 2023 target price model:

-

Bull scenario (50% probability) assumptions - VLD to finish FY 2023 with $120 million of revenue, at the low end of its $120 - $130 million guidance, reflecting a 50% YoY growth.

-

Bear scenario (50% probability) assumptions - VLD to finish FY 2023 with $100 million of revenue, implying a merely 25% YoY growth.

author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of ~$2.45 per share. With VLD trading closer to ~$2.05 per share recently, the stock appears undervalued by ~22%.

At the current price, VLD seems a bit oversold. As such, it may present an interesting speculative buy opportunity. Furthermore, it is currently trading below the target price I set for the bear scenario.

If cash burn slows down and margins expand a bit more, I expect P/S to potentially trend upwards. While I rate the stock a buy at this time, I would probably point out that investors may have two options here. Given the speculative opportunity, investors may want to make a small allocation and buy the dip today. Otherwise, investors can also reassess VLD in Q2.

Conclusion

VLD is currently considered a speculative buy due to its share price bottoming, making it a good opportunity for dip-buying. However, investing in VLD comes with high risk. It is unlikely to achieve positive cash flow this year in my opinion, however, its growth potential remains strong, displaying solid demand. Based on my analysis, I have set a target price of approximately $2.45 per share for FY 2023. Considering that VLD has been trading around $2.05 per share recently, it appears undervalued by approximately 22%.

For further details see:

Velo3D: Speculative Dip-Buying Opportunity