VLD - Velo3D: Takeover Target

2023-12-19 20:23:14 ET

Summary

- Management attributed third quarter weakness to delays, but executive turnover and a shift in strategy suggest larger underlying problems.

- Declining revenue, low gross profit margins, and elevated operating expenses raise doubts about Velo3D's viability as a standalone company.

- Velo3D now appears to be positioning itself for a sale. While this may boost the share price from current levels, investors are unlikely to be pleased with any offers received.

Velo3D’s ( VLD ) third quarter results were soft, which the company attributed to shipment delays. A strategic realignment, the exit of the CEO and pursuit of a potential sale could hint at larger issues though. This doesn’t appear to be a macro problem either, as most of Velo3D’s sales are to customers that are less sensitive to the economic environment. Velo3D still has a sizeable cash balance with which to work, but stalled growth and a shift in strategy are unlikely to be a source of comfort for shareholders.

I highlighted the risk of paying a high multiple for Velo3D earlier in the year, and this risk has since come to fruition, with the stock down approximately 77% since then.

Third Quarter Results

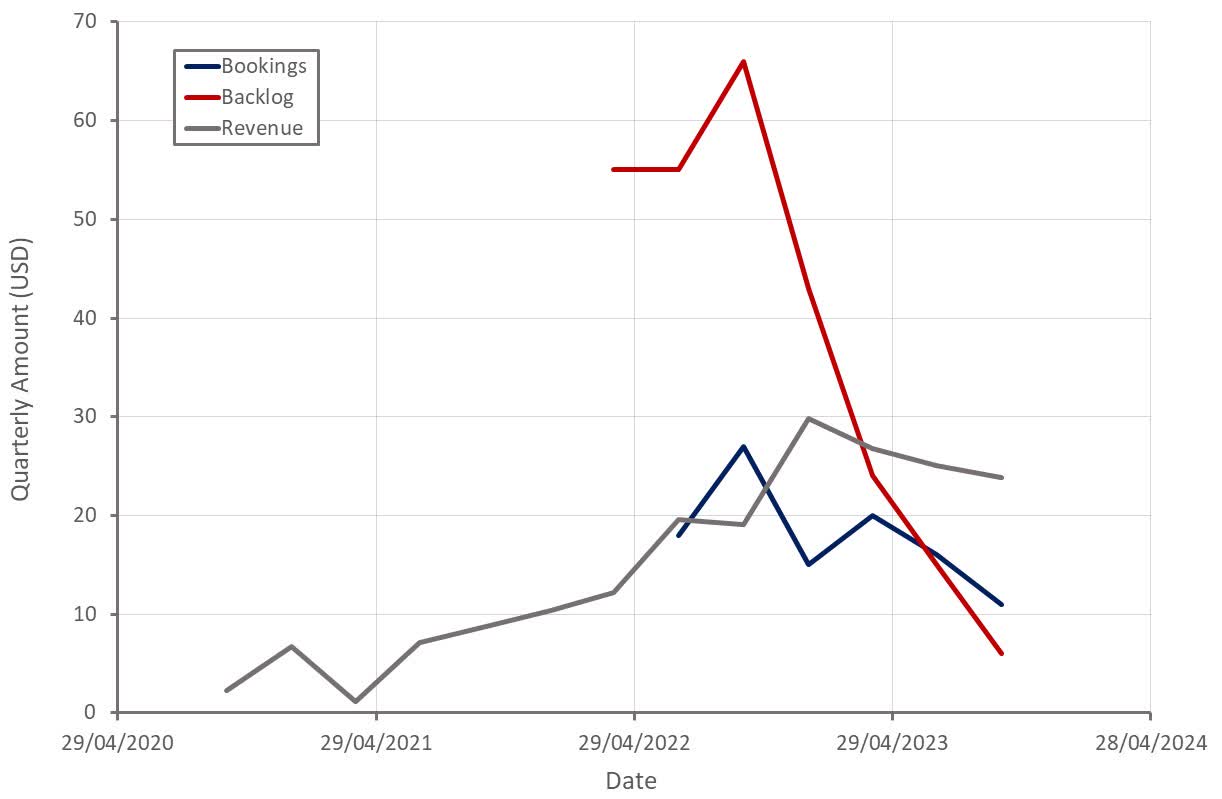

Velo3D’s third quarter bookings and revenue both came in below plan, which was attributed to customer order and shipment delays . Revenue increased 26% YoY in the third quarter but has now been fairly flat over the past three quarters. In addition, Velo3D's bookings and backlog continue to decline.

Bookings growth has been negatively impacted by soft existing customer sales, although new customer acquisitions have also been weak. Velo3D is not attributing this to the macro environment though, stating that most of its customers are well financed and in non-cyclical industries. Most of Velo3D's sales come from North America, with turbo machinery and rocket engines for space and launch programs and engine components for hypersonic aircraft particularly important use cases.

A lack of customer support has also reportedly increased system installation times, and uptime and yield on some machines have been below Velo3D's expectations, leading to customer dissatisfaction. Velo3D has suggested that this drop in satisfaction has contributed to the decline in orders. In response, Velo3D is adding headcount to the customer support organization, forming a dedicated issue resolution team, and improving employee training.

To help drive revenue growth, Velo3D is also focusing sales on markets where it has already demonstrated traction (space / defense / aerospace). It is also developing partnerships to expand non-US markets / applications.

Velo3D is guiding to 15-27 million USD revenue in the fourth quarter, implying a substantial YoY revenue decline at the midpoint. In addition, the size of the revenue guidance range suggests the company has little visibility into performance going forward. Based on the rapid decline in backlog, a pause on the procurement of new inventory and a shift in focus towards profitability, I would expect fourth quarter revenue to come in at the low end of the guided range.

Figure 1: Velo3D Revenue (source: Created by author using data from Velo3D)

{kind=link}

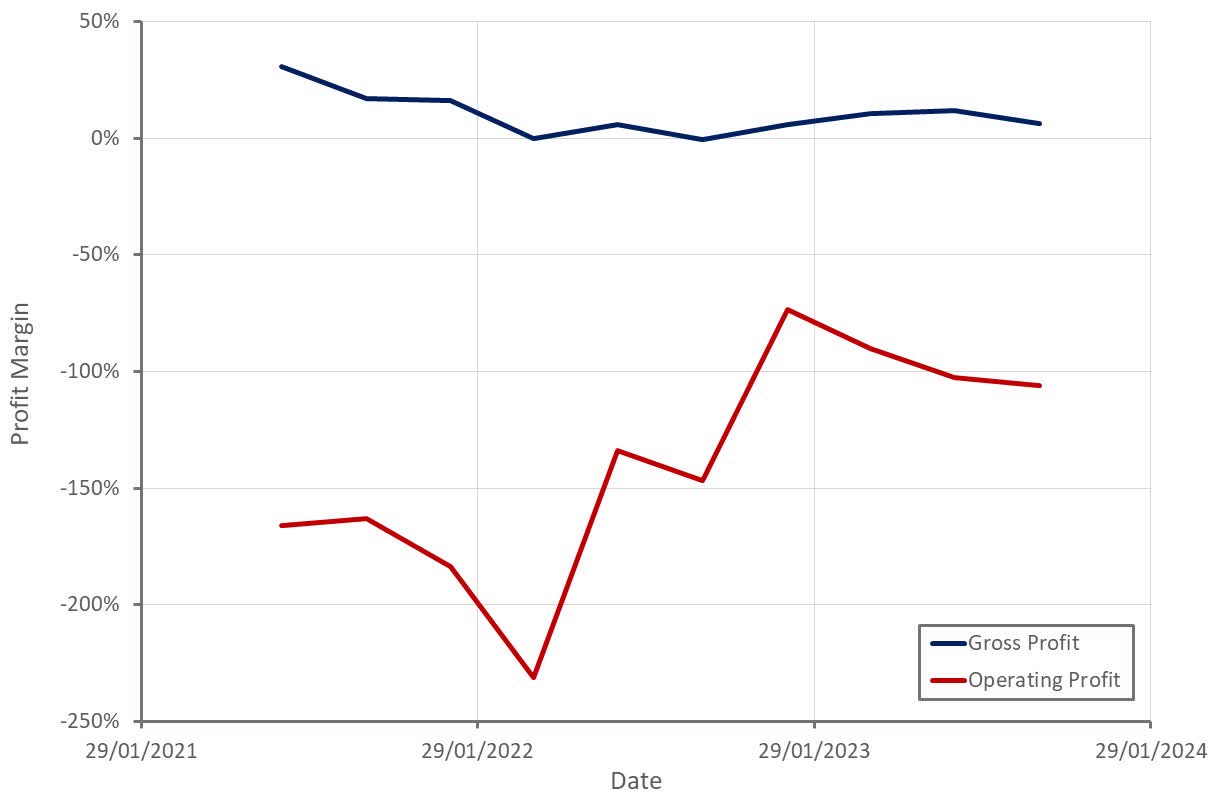

Velo3D's gross profit margin declined in the third quarter on the back of lower system sale volumes , a shift in mix towards lower priced products and higher inventory adjustments. Velo3D expects gross margins to improve in the fourth quarter and throughout 2024, but this will likely be difficult if sales remain weak. Improvements are expected to come from a shift in mix towards higher price products, improved manufacturing efficiency and reduced material costs.

Velo3D's operating profit margin also declined in the third quarter, despite a reduction in operating expenses. The decrease in operating expenses was primarily due to a 2.6 million USD reduction in R&D. General and administrative expenses were up 1 million USD due to Velo3D's realignment initiative and sales and marketing expenses were fairly stable.

Figure 2: Velo3D Profit Margins (source: Created by author using data from Velo3D)

{kind=link}

Declining revenue, low gross profit margins and elevated operating expenses now appear to be raising doubts about Velo3D's viability as a standalone company, despite it still having a sizeable cash balance. Velo3D is trying to reduce cash burn, largely by drawing down its current inventory. The company believes it has sufficient inventory on hand (~ 81 million USD) to meet demand for the next two quarters .

The fourth quarter is also expected to see a one-off cash inflow of 3-6 million USD from a lease termination and 3 million USD from Velo3D redeeming its PhysicsX investment. Fourth quarter cash usage is expected to be 15-18 million USD, including onetime payments for severance and facility consolidations.

Velo3D expects to achieve free cash flow breakeven in the second quarter of 2024 . Based on the company's recent sales trajectory this appears optimistic though.

Strategic Realignment

Velo3D recently stated that its focus on growth has come at the cost of customer service and profitability. This is not a particularly convincing argument given that growth has been modest for most of 2023.

Velo3D is now shifting focus towards optimizing free cash flow and improving customer satisfaction. As a result, it has introduced a cost cutting plan with a goal of achieving profitability in 2024 , which includes:

- Indefinite pause on procurement of new inventory

- 20% headcount reduction

- Consolidation of office and manufacturing footprint into a single facility

- Prioritizing R&D spend to only high ROI projects

- Optimizing corporate expenses

- New go-to-market strategy to rebuild bookings pipeline

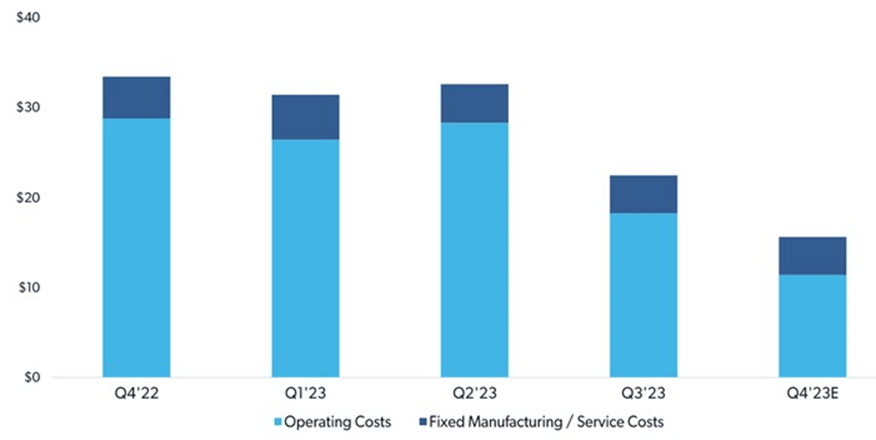

These efforts are expected to result in a 40% reduction in cash expenditures. At the time of reporting third quarter results, Velo3D believed it had sufficient liquidity to achieve its goals in 2024.

Velo3D expects to incur the following costs in the fourth quarter, related to its strategic realignment:

- Severance costs of 1-2 million USD

- Facility consolidation costs of 2-3 million USD

These moves are expected to significantly reduce Velo3D's expenses, but without growth, and a significant improvement in gross profit margins, the company will still be a way off profitability. I estimate that Velo3D needs around a 200 million USD annualized revenue run rate to reach operating profit breakeven on a GAAP basis.

Figure 3: Velo3D Cash Expenses (source: Velo3D)

{kind=link}

Potential Sale

After announcing a strategic pivot and trying to reassure investors at the end of the third quarter, Velo3D changed CEO and hinted at a possible sale in the middle of December. Benny Buller stepped down as CEO at the request of the company's Board of Directors, with Brad Kreger, EVP of Operations, appointed interim CEO while Velo3D searches for a permanent replacement. Kreger has only been with Velo3D for around 12 months and has a life sciences background.

Velo3D's market capitalization is currently around 115 million USD, and the company has approximately 72 million USD cash and 65 million USD debt. While this provides Velo3D meaningful runway within which to resolve issues, the exit of the CEO could suggest that the strategic pivot is not having the desired effect.

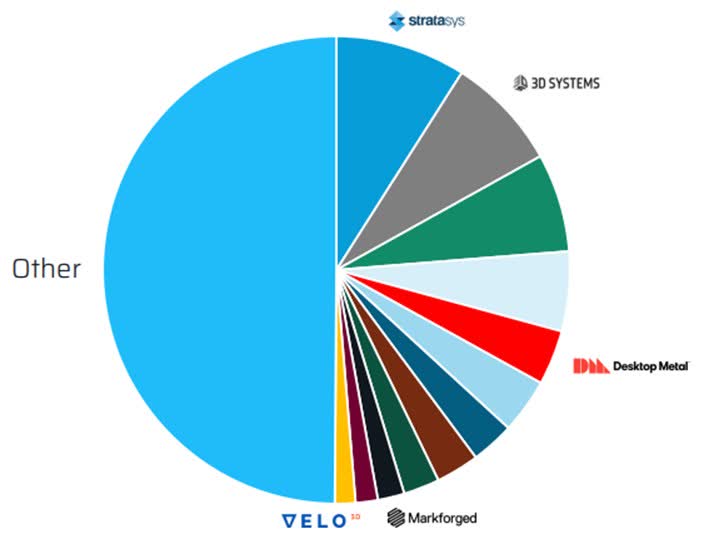

Velo3D is also now exploring alternatives to maximize shareholder value, including a strategic transaction, potential merger, business combination or sale. Many additive manufacturing companies are already financially strained, potentially limiting the pool of viable acquirers. Given Velo3D’s differentiated technology, there isn’t any one company that is an obvious suitor from a technology perspective. Nano Dimension ( NNDM ) is the best positioned financially and has been actively seeking acquisitions, but it has been targeting companies that can provide it with scale or that support its printed circuit board focused product portfolio. Stratasys ( SSYS ) and 3D Systems ( DDD ) are also potential acquirers.

There was a flurry of M&A activity in the additive manufacturing industry earlier in the year, which potentially provides a guide to any interest in Velo3D:

- Nano Dimension made a partial tender offer in cash to Stratasys earlier in the year at an EV/S multiple of roughly 2.40.

- Desktop Metal ( DM ) accepted a proposed merger with Stratasys , which implied an EV/S multiple of approximately 2.90 at the time of the offer. This agreement was subsequently rejected by Stratasys shareholders though.

- 3D Systems made a number of attempts to merge with Stratasys in 2023, but Stratasys showed little interest in 3D Systems' advances. The offers valued Stratasys at an EV/S multiple of up to 2.65 (inclusive of estimated synergies).

Most of this activity was directed at industry consolidation, with the companies involved trying to create sufficient scale to achieve profitability. Velo3D is still a very small player in the industry and cannot offer the scale or consolidation that potential acquirers are likely to desire.

Figure 4: Additive Manufacturing Market Share (source: Nano Dimension)

{kind=link}

Given the low-price tag, one of Velo3D’s customers could also conceivably choose to vertically integrate and acquire Velo3D, assuming the technology is viewed as a strategic advantage. SpaceX is Velo3D's largest customer and an investor, making it the most likely candidate. Based on recent soft sales and customer dissatisfaction, Velo3D's customers don't appear to be clamoring to get their hands on the company's technology though.

Conclusion

Despite the recent price decline, Velo3D's stock isn't particularly cheap given the company's lack of growth and poor margins. Recent issues have likely shifted focus from Velo3D's long-term potential to the company's liquidity and value to any potential acquirers though.

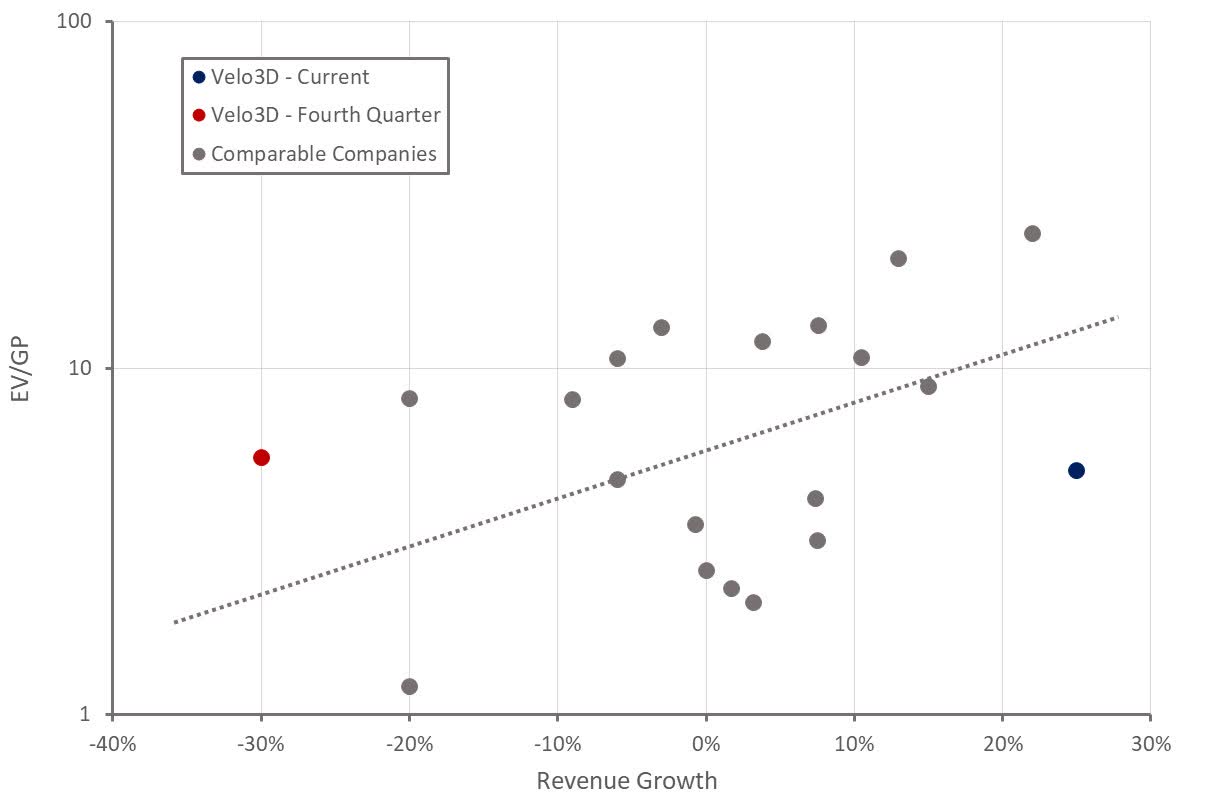

Figure 5: Velo3D Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

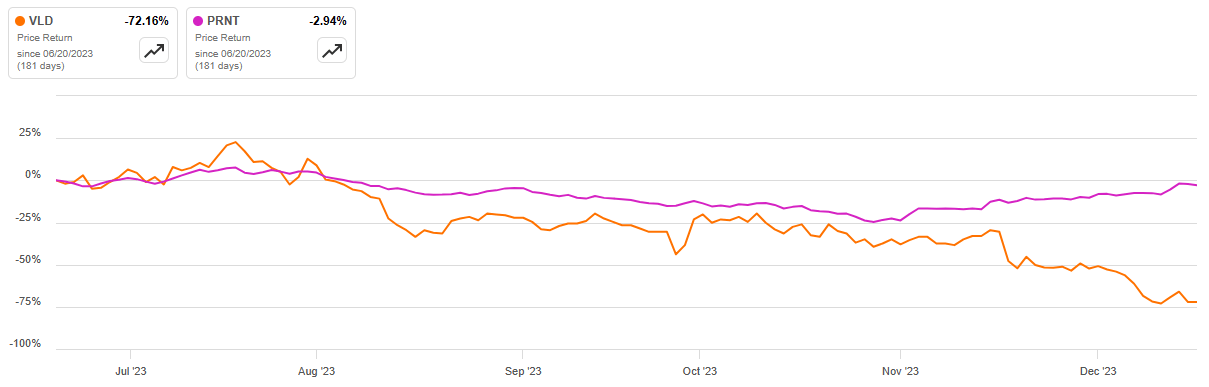

Velo3D's recent share price performance also needs to be considered in light of the dramatic shift in sentiment towards small cap stocks and many unprofitable companies. If investor risk appetite were to sour, Velo3D's stock could come under further pressure. For this reason, it is probably in the company's best interest to provide shareholders with reassurance in the near-term (acquisition offer, capital raise, improved profitability).

Figure 6: Velo3D 6 Month Share Price Performance (source: Seeking Alpha)

{kind=link}

Given Velo3D's differentiated technology, which includes design and simulation software, the company should appeal to acquirers at the right price. Velo3D appears to be negotiating from a position of distinct weakness though, which may limit the amount of upside any offers bring.

Based on M&A activity in the additive manufacturing industry in 2023, Velo3D could expect a valuation of around 1.30 USD per share. Additive manufacturing company valuations have compressed significantly since M&A activity settled down though, meaning any offer that Velo3D is likely to receive will be a lot lower than recent benchmarks. If Velo3D is unable to attract any attractive offers, the company needs to stabilize revenues and demonstrate a viable path to profitability.

For further details see:

Velo3D: Takeover Target