CA - Vermilion Energy: Once I Had Love And It Was A Gas

2023-12-20 09:29:10 ET

Summary

- Vermilion Energy experienced a disastrous 2023 due to windfall taxes and poor capital return to shareholders.

- But the pain of 2023 is the opportunity for 2024.

- Despite operational challenges, VET has the potential for double-digit returns from here.

Sometimes the best setups fail. Everything can be aligned and you can get in at what appears to be a bargain, only to have the unpredictability of the markets remind you that you do not control the outcome. Vermilion Energy (VET) ( VET:CA ), was one such case where valuation looked so compelling in 2022, that it was hard to not mortgage your house and go levered long on the stock. We go over why the bulls suffered in 2023 and why things are looking up for 2024. We also tell you why you should not get too optimistic for returns here.

The Company

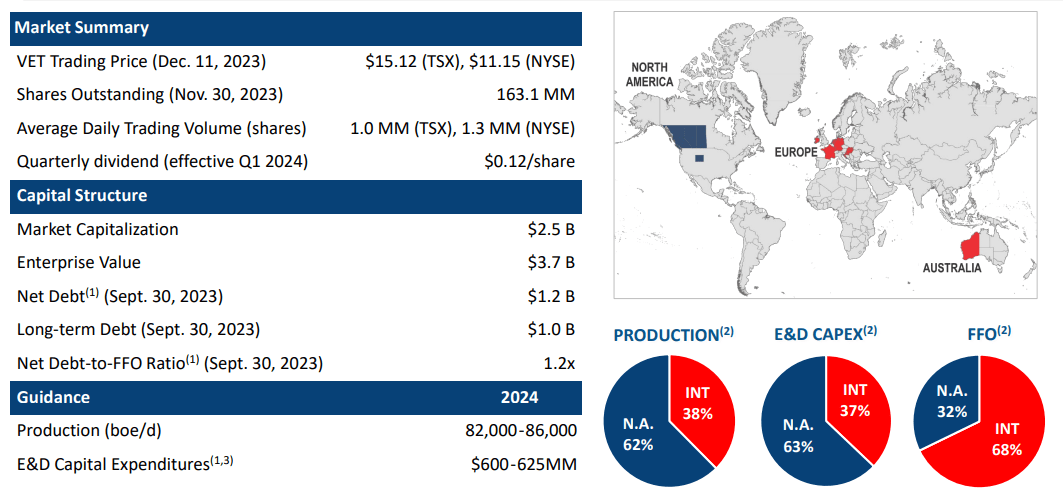

If you buy the super majors like Exxon Mobil Corporation (XOM), or Chevron Corporation (CVX), you automatically get exposure to global oil and gas assets. But that exposure rarely leverages you to any one area. VET on the other hand gave you that leverage and gave you that leverage to one area of extreme imbalance. European Gas.

{kind=link}

The Setup

Once I had a love and it was a gas

Soon turned out had to pay windfall tax.

Source: Blondie in collaboration with VET shareholders

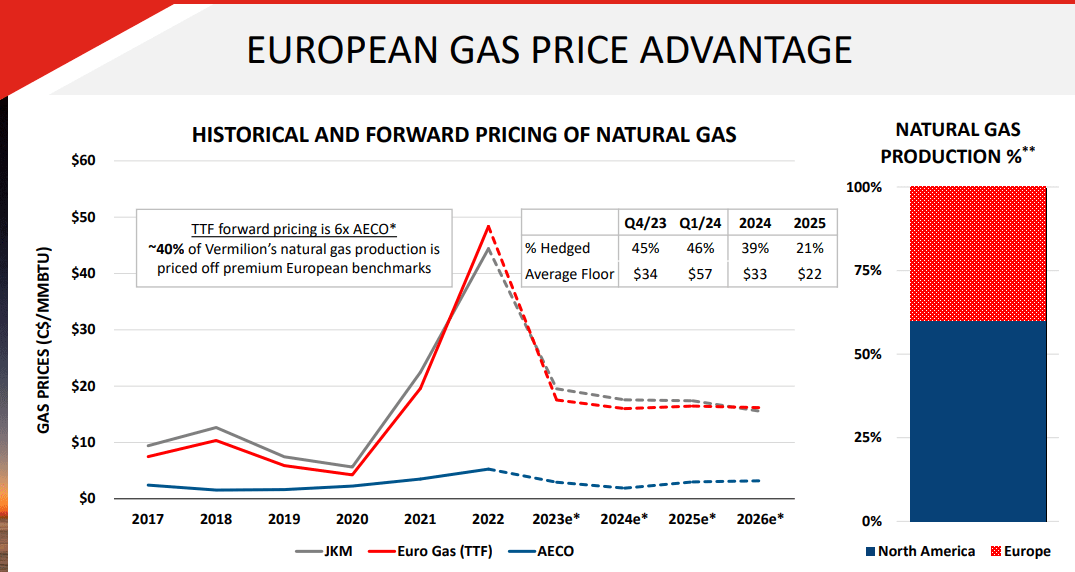

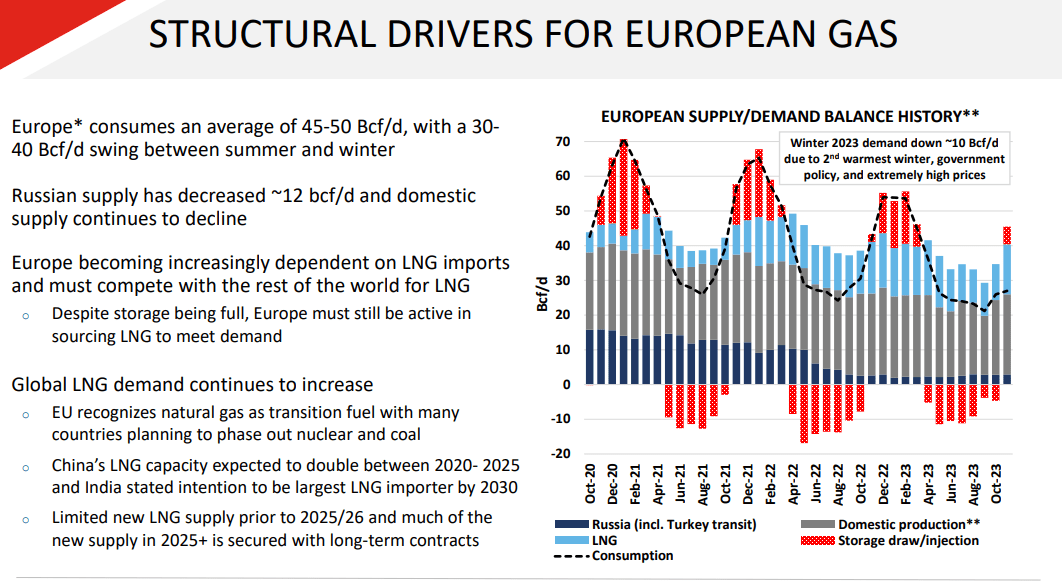

The bull case in 2022 was all about European Gas.

{kind=link}

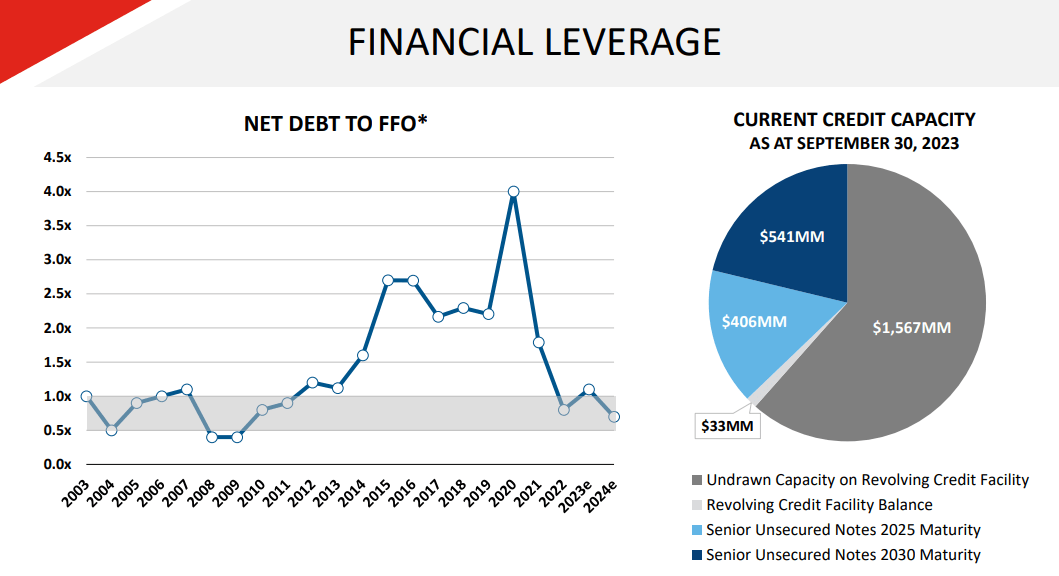

Look at that spike in the middle of the chart. Look where AECO (the Canadian benchmark) traded in comparison. The numbers were just astronomical. Despite VET having already hedged a lot of its Natural Gas production for 2022 at relatively low prices, initial estimates for the cash flow per share were higher than the stock price at the time. The bull story was slowly broken down over time as the EU basically decided to confiscate a lot of that via extra taxation (windfall taxes). The end result was not too bad with cash flow per share close to $9.43 CAD in 2022. But the stock unfortunately had a disastrous 2023 as windfall taxes continued and VET's capital return left a lot to be desired. But this all has actually created a good opportunity. The debt reduction with the stock price drop has really created a value opportunity.

What 2024 Looks Like

VET shareholders heaved a sigh of relief as there is expected to be no extension of EU windfall taxes into 2024. This increases the cash flow by about 10%. VET has also layered in hedges across the curve and almost 40% is hedged for 2024 at mind-boggling prices.

VET Dec 2023 Presentation

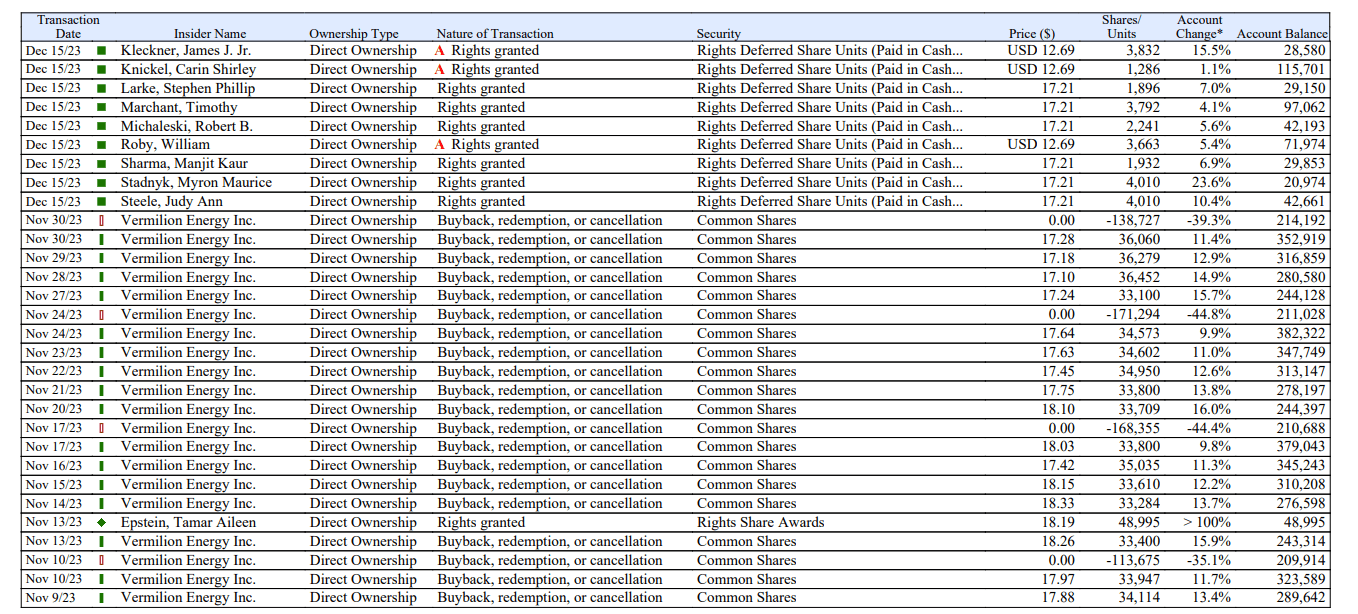

VET has been progressively returning its free cash flow to shareholders in 2023 so far we have seen about 30% in 2023. This is via the small dividend and some buybacks.

{kind=link}

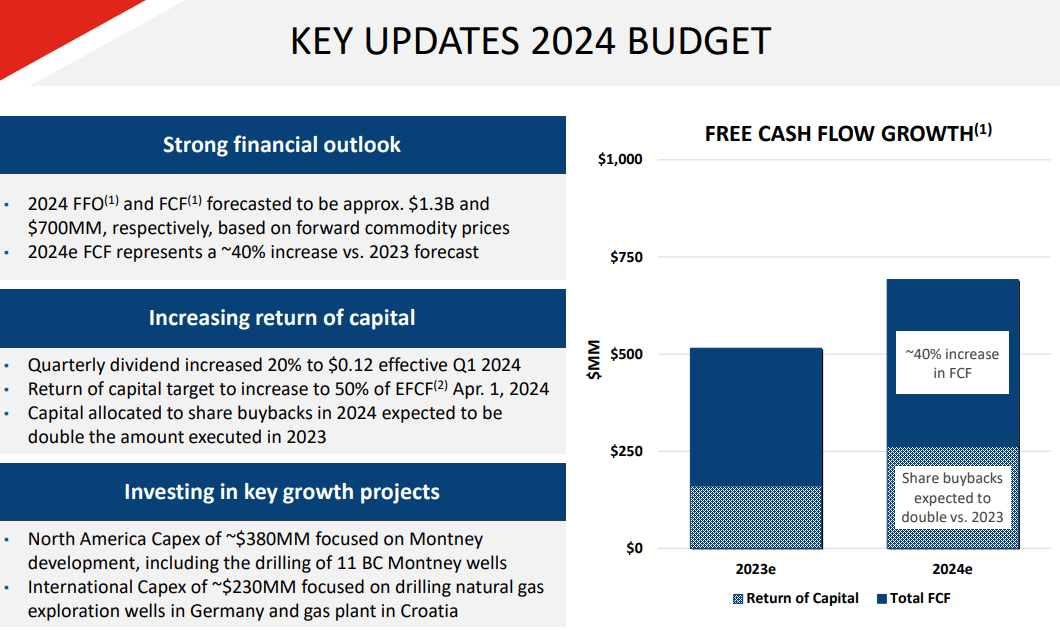

The recently released budget shows that VET expects to double its returns to shareholders (assuming strip prices hold). The official net debt target of $1 billion should be achieved in Q1-2024 and then one can expect the 50% of free cash flow to be redirected towards buybacks.

{kind=link}

Our Outlook

While investors have been a little peeved with the capital return strategy, VET has got the right idea in mind. After the 2020 dividend cut, they have rethought their model and it requires operating with far less leverage.

{kind=link}

We like that and we also like that VET is one of the most responsible hedgers amongst the oil and gas producers. The structural drivers for European Gas are quite strong and we expect at least a high floor price to attract LNG imports.

{kind=link}

How We Played It

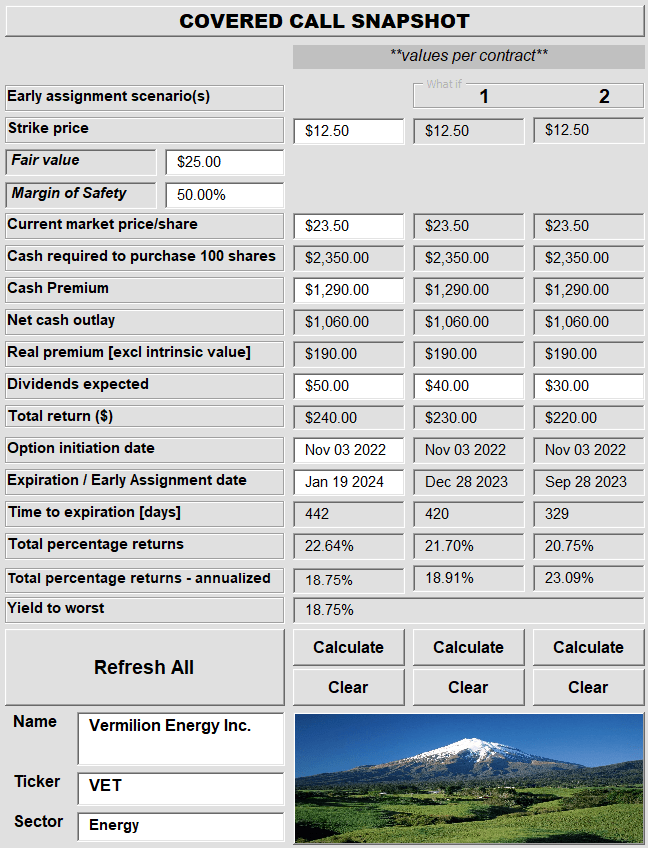

VET was one of the most unusual covered call options we initiated in our Marketplace Service. As anyone who has followed our method knows by now, we throw the standard option-writing book into the garbage can. We focus on very long dated options and value net-price entry over all else. Assessing current volatility versus historical or trying to make high annualized returns with weekly options have no place in our portfolio. Our approach can be summarized in the screenshot below.

Conservative Income Portfolio

So for VET, we wanted a high annualized yield as well as a huge margin of safety. We were not ready to chase the stock higher despite relatively bullish fundamentals. With the stock at $23.50 USD, we actually sold a covered call for $12.50 USD. Interestingly, those had a very large net premium creating a nice annualized yield, even if the stock held over $12.50 USD.

{kind=link}

In other words, we were aiming for about 23% total returns, as long as the stock fell less than 47%.

Where on the planet can you get that good a return profile for a quality company? The funny aspect here is that VET declined by over 47%! We still made a little dough as we closed out those options and rolled to January 2025.

Conservative Income Portfolio

It was one of the most extreme examples in our trading history where we made money on the long side while the stock was cut in half.

Verdict

We think 2024 should finally reward shareholders and the company likely delivers a 25% total return. The valuation has really gotten compressed. We get that nobody loves VET but look at that EV to EBITDA gap versus Antero Resources (AR).

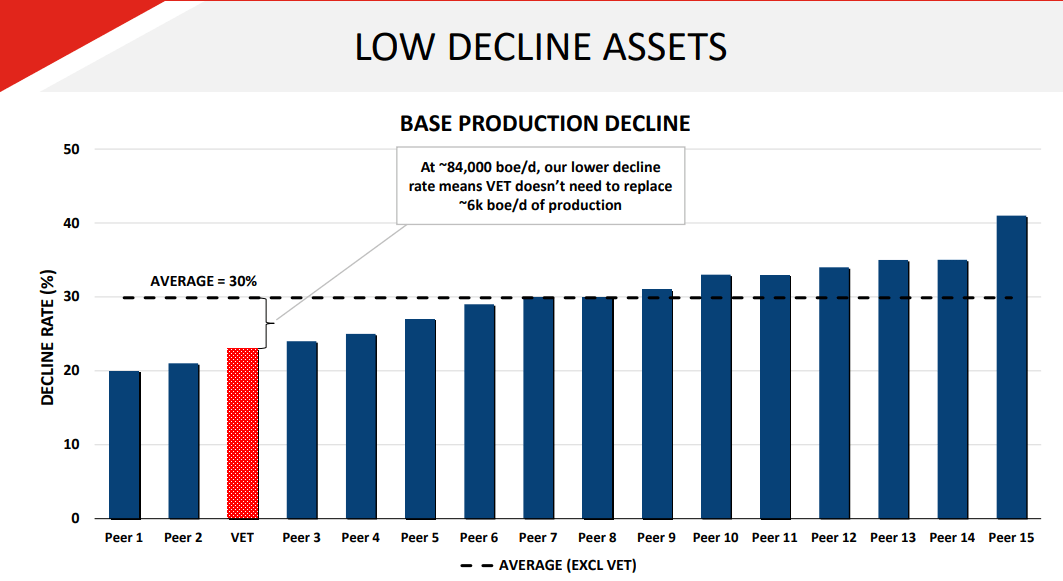

We also own that one, by the way. But you cannot ignore the potential for double-digit returns in almost any scenario for VET and the 20% increase in dividends was a nice gesture by the company. One point of caution before you go all-in here. VET has had one of the poorest operational performances amongst the companies we follow in this space. You won't get that from their slide deck, though. There you will see the "low decline" rates mentioned.

{kind=link}

Low decline or not, just look at where the production was in 2019.

VET Q2-2019 Financials

2024 production estimate, just released, came in at 84,000 BOE.

VET Dec 2023 Presentation

This is also about 2,000 BOE below where estimates stood just before that. So you have to allocate some amount of that cash flow as payment from a depleting royalty asset. We still like it and we are long. We have sold calls at the $12.50 and $15.00 strikes to enhance income and reduce the high volatility associated with this stock.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Vermilion Energy: Once I Had Love And It Was A Gas