CA - Vermilion: Solid Cash Flows In Q3 Due To Low Operating Costs And Hedging Gains

2023-11-02 07:12:08 ET

Summary

- Vermilion Energy's performance has been poor over the last year due to a retracement in European natural gas prices and windfall profit taxes.

- The company's Q3 results showed an increase in fund flows and free cash flow compared to Q2.

- Shareholder distributions are expected to increase once the net debt target is reached, and the company's valuation for 2024 is attractive.

Investment Thesis

Vermilion Energy ( VET ) is a Canadian oil & natural gas producer, with production in Canada, United States, Europe, and Australia. The company is listed in the U.S. and Canada ( VET:CA ). The reporting currency is Canadian Dollars. I have covered the stock quarterly over the last year and those articles can be found here .

{kind=link}

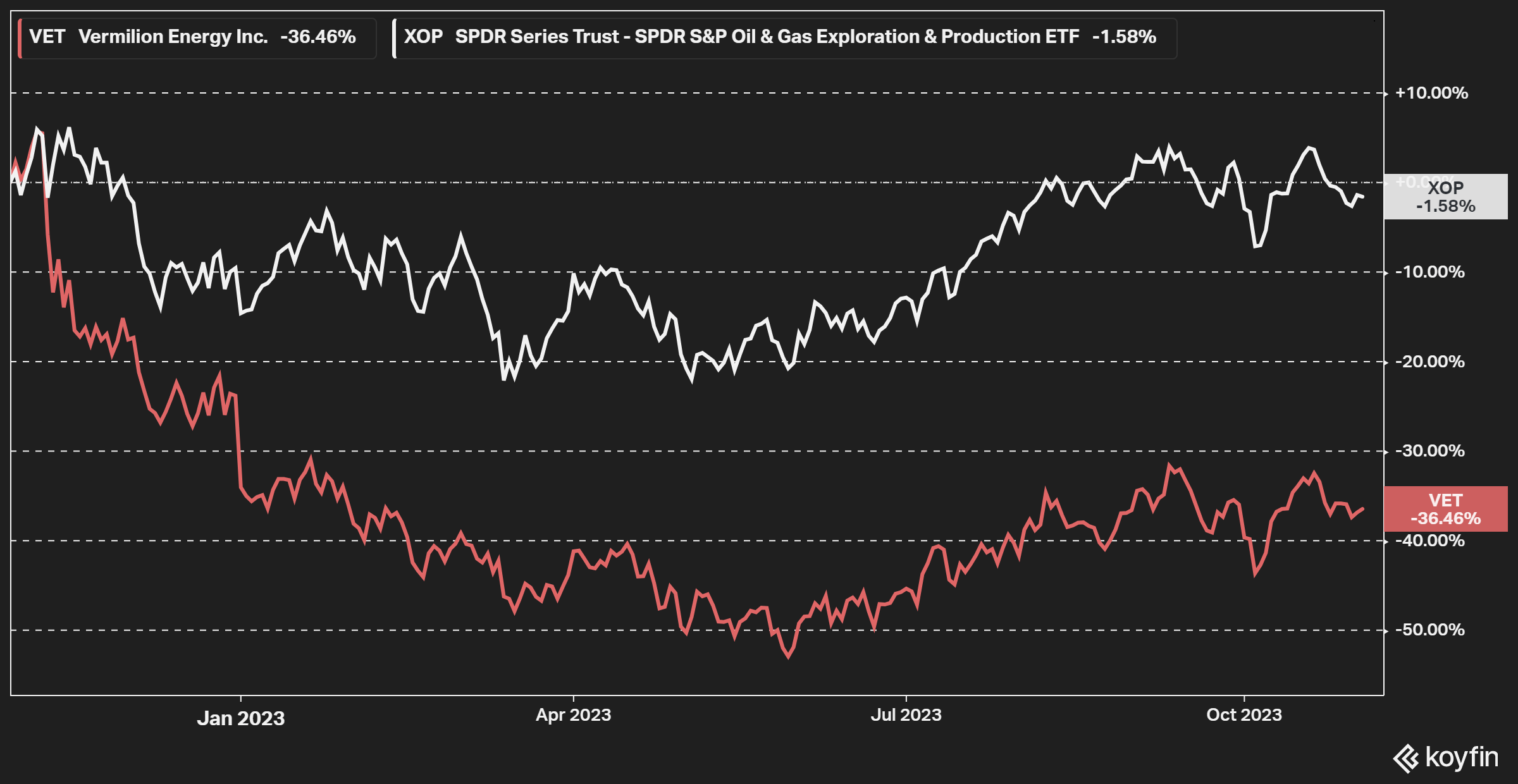

The performance of Vermilion has been very poor over the last year, at least compared to most industry peers, even if it has been much more aligned with peers lately. The large retracement in European natural gas prices compared to 2022, which account for a substantial percentage of total free cash flow, is no doubt the main reason. The European windfall taxes for 2022-2023 have also had an impact, both on the sentiment, and they also delayed an increase in shareholder distributions. Where the low shareholder distributions have likely been a headwind recently as well.

Figure 2 - Source: Vermilion Corporate Presentation

It is looking brighter going forward though, where some or all windfall profit taxes might disappear in 2024, as at least the original windfall profit taxes were only for 2022-2023. If confirmed, that could boost free cash flow by as much as C$150-200M in 2024, somewhat dependent on energy prices. Shareholder distributions are also likely to increase in the coming year as the C$1B net debt target is reached. So, 2024 might be a pivotal year for Vermilion.

Vermilion did yesterday after the close release its Q3-23 result and will later today host a conference call. This article will be focused on the recent results and my general views on the company.

Q3 Result

The Australian assets have been offline for Vermilion during most of the year but are as of late Q3 back online. That is very encouraging, but they will primarily boost the numbers in Q4 and next year. Where the expectation is for the Australian assets to be producing around 4,000 boe/d in Q4.

Vermilion reported a production of 82,727 boe/d in Q3 , which is at the lower end of the company's annual guidance range of 82,000 - 86,000 boe/d. It is roughly in-line with what the company reported in Q2 (83,152 boe/d) and Q1 (82,455 boe/d). However, production is expected to increase in Q4 where the guidance is set at 86,000 - 89,000 boe/d. So, Q4 should compensate for the slightly lower production during the quarters earlier in the year.

Despite a slightly lower production number in Q3 compared to Q2, Vermilion reported C$270M (C$247M in Q2) in fund flows from operations and C$144M (C$80M in Q2) in free cash flow in the quarter, where the free cash flow is a significant improvement compared to the prior quarter.

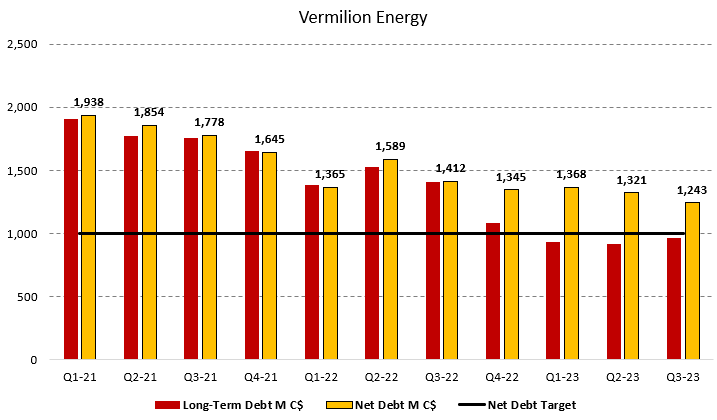

As mentioned earlier in the article, shareholder distributions are relatively low for Vermilion, around 30% in 2023, and the primary capital allocation focus is to deleverage. Vermilion is now only C$243M from its net debt target of C$1B. That net debt target is expected to be reached during the first quarter of 2024, when shareholder distributions will consequently increase. There might be a small dividend increase, but at least my expectation is that the company will primarily increase the buybacks once the net debt target is reached.

Figure 3 - Source: Vermilion Quarterly Report

{kind=link}

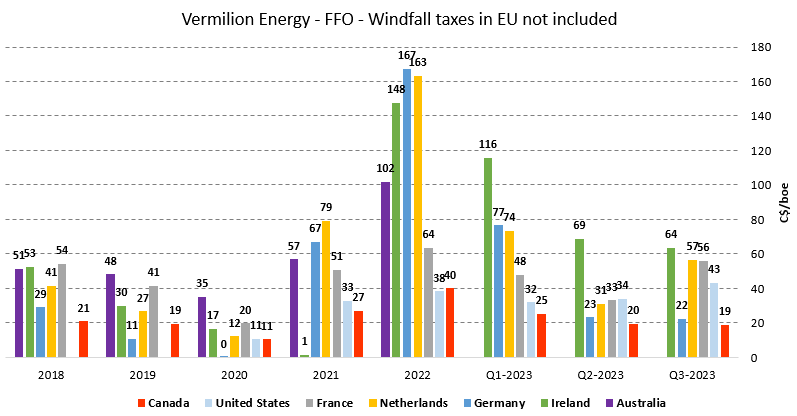

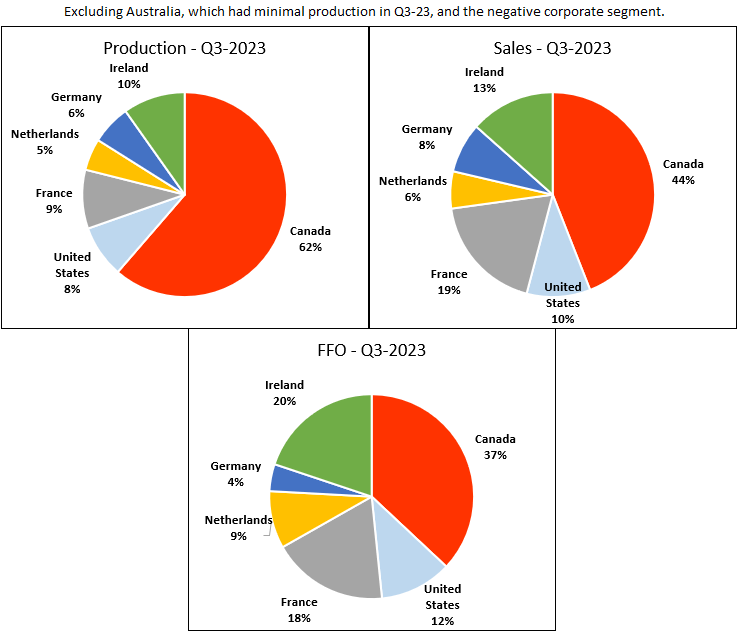

Most of Vermilion's production did in Q3 come from Canada, but a disproportionate percentage of fund flows came from Europe. That is because the margin is much higher in the European markets, in part because 100% of production in France comes from crude oil and due the premium priced European natural gas. The windfall profit taxes are not included in the below figures, as Vermilion books them consolidated in the corporate segment.

Figure 4 - Source: Vermilion Quarterly Report Figure 5 - Source: Vermilion Q3-23 Report

{kind=link}

{kind=link}

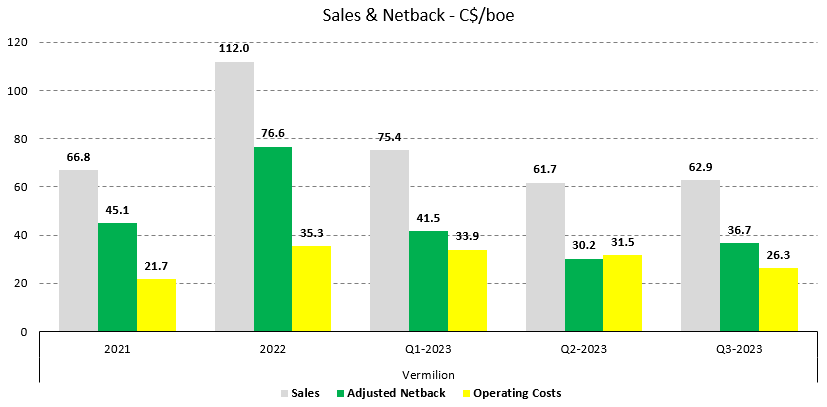

In the chart below, you can see the sales price, total operating costs, and adjusted netback for the Vermilion over the last few years. Please note that the windfall profit tax is included in the total operating cost and deducted from adjusted netback here.

The quarter-over-quarter rebound in energy prices has had a slight impact on the sales price for Vermilion, which saw a C$1.2/boe increase compared to last quarter. However, the adjusted netback increased to C$36.7/boe, which was more impacted by very low total operating costs in the quarter. Based on current energy prices, sales and possibly also netback will improve further in Q4.

Figure 6 - Source: Vermilion Quarterly Report

{kind=link}

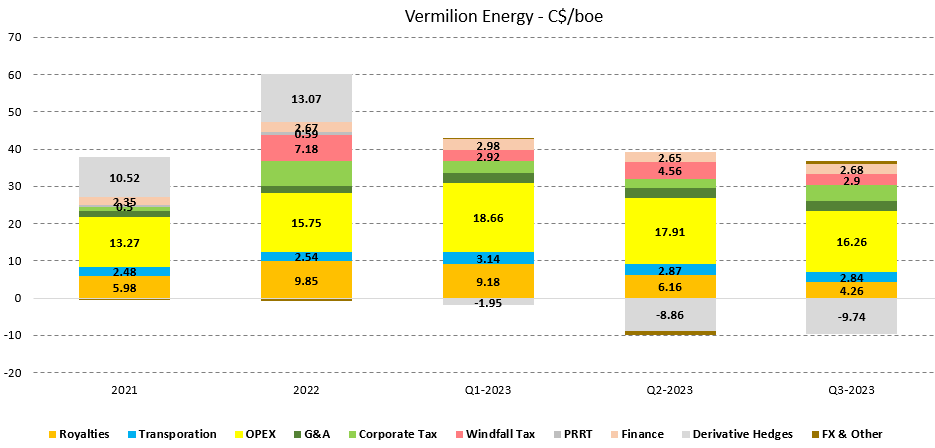

If we zoom in on the cash costs of the company, we can see that the commodity hedges have also been a substantial tailwind in the last couple of quarters. Much of the hedging gains are from European natural gas production. Where the percentage of production that is hedged will decrease in 2024, but the company still has as much as 38% of the European natural gas production hedged in 2024, at an average floor price of C$33/mmbtu.

Figure 7 - Source: Vermilion Quarterly Report

{kind=link}

Valuation & Conclusion

There is still some uncertainty regarding what will happen to the windfall profit taxes next year, where we should hopefully get more clarity over the next few months. At this point, no windfall profit taxes for 2024 have according to Vermilion been announced by the European Union.

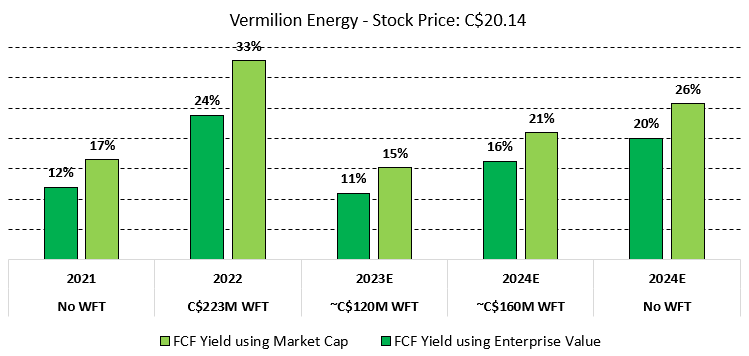

Vermilion's stock price has underperformed to such a degree early 2023, that the projected free cash flow yields are very attractive even if we were to see the windfall profit taxes continuing in 2024. The below 2024 figures are based on the estimates in the latest Vermilion slide deck, where I have roughly estimated a potential 2024 windfall profit tax to C$160M.

Figure 8 - Source: Company's Reported Figures & My Estimates

{kind=link}

Vermilion's stock is currently trading with a 2024 free cash flow yield, using the market cap, around 26% without windfall profit taxes in Europe next year and around a free cash flow yield of 21% with the taxes. This is in my view a very attractive valuation.

Because the company has lower shareholder distributions and less growth prospects than some peers, a slightly lower valuation might be justified, but the discount is too large to ignore in my view. However, I would emphasize that Vermilion is a deep value investment, where you need quite a bit of patience. It is not realistic to buy a company at a significant discount to peers and then expect to be rewarded straight away.

For further details see:

Vermilion: Solid Cash Flows In Q3 Due To Low Operating Costs And Hedging Gains