VRRM - Verra Mobility Is Addressing My Problems With Them

2023-09-04 09:00:00 ET

Summary

- Verra Mobility has addressed previous problems with its culture, as seen through improved Glassdoor ratings and changes in leadership.

- The company has taken steps to manage its high debt, including lowering its leverage target and paying down variable rate debt.

- Using an inverse DCF model, Verra Mobility is considered attractively priced and continues to be a buy, with expected growth in owner earnings.

Verra Mobility, a global leader in technology-enabled transportation solutions, has outperformed the market since I first covered it this January. While I rated it a buy, there were several problems that kept me away from owning the stock. The company has addressed some of these problems, so let's review the investment case again.

The problems

Back in January, I addressed two major problems I saw:

- The culture, highly promoted to investors, seemed to be not great according to Glassdoor reviews.

- The high debt could create problems in the future, especially with rising rates against floating rate debt.

Culture

Culture is always a tough topic to judge from outside a company. Over the long-term companies thrive due to a good culture that rewards employees and keeps them with the company for a while, reducing turnover. Verra boasted of its great culture in the 2022 Investor Day, yet after reviewing the company's Glassdoor ratings , it didn't look as rosy.

Since my first article, the total score improved from 3.4 to 3.6, "would recommend to a friend" from 56% to 71% and "approving of the CEO" from 66% to 74%. This is a very good development in a short period of time. Furthermore, an often cited issue was the previous Chief People Officer, who was replaced in July by Katrina Sevier , ex-Chief Human Resources Officer at Teleperformance USA (TLPFF). We can see that the culture seems to be improving, from what we can tell from the outside.

{kind=link}

Debt

While debt is not something bad in general, I am personally not a fan of highly leveraged companies. In its 2022 Investor Day, Verra guided with a 3.5 times average net leverage until 2026. While 3.5 times is not excessive, it is above my comfort level. Since going public, the median leverage was 4.0 times. When I reviewed the stock, $800/$1200 of debt was floating rate at LIBOR + 325bps (should be around 8.7% interest rate right now). On the bright side, maturities were all out until 2028+. In November 2022 the company announced that it would lower its leverage target to 3.0x, due to the unique interest rate environment. Since then improved net leverage from $1.1 billion to $950 million by paying down its variable rate debt by around $75 million and increasing the cash position. We also should keep in mind that the net leverage Verra Reports is based on Adjusted EBITDA and not EBITDA, as I use. This brings leverage from the reported 2.7 times to 2.9 times net debt/EBITDA. Verra intends to bring this down to 2.5 times in 2023.

{kind=link}

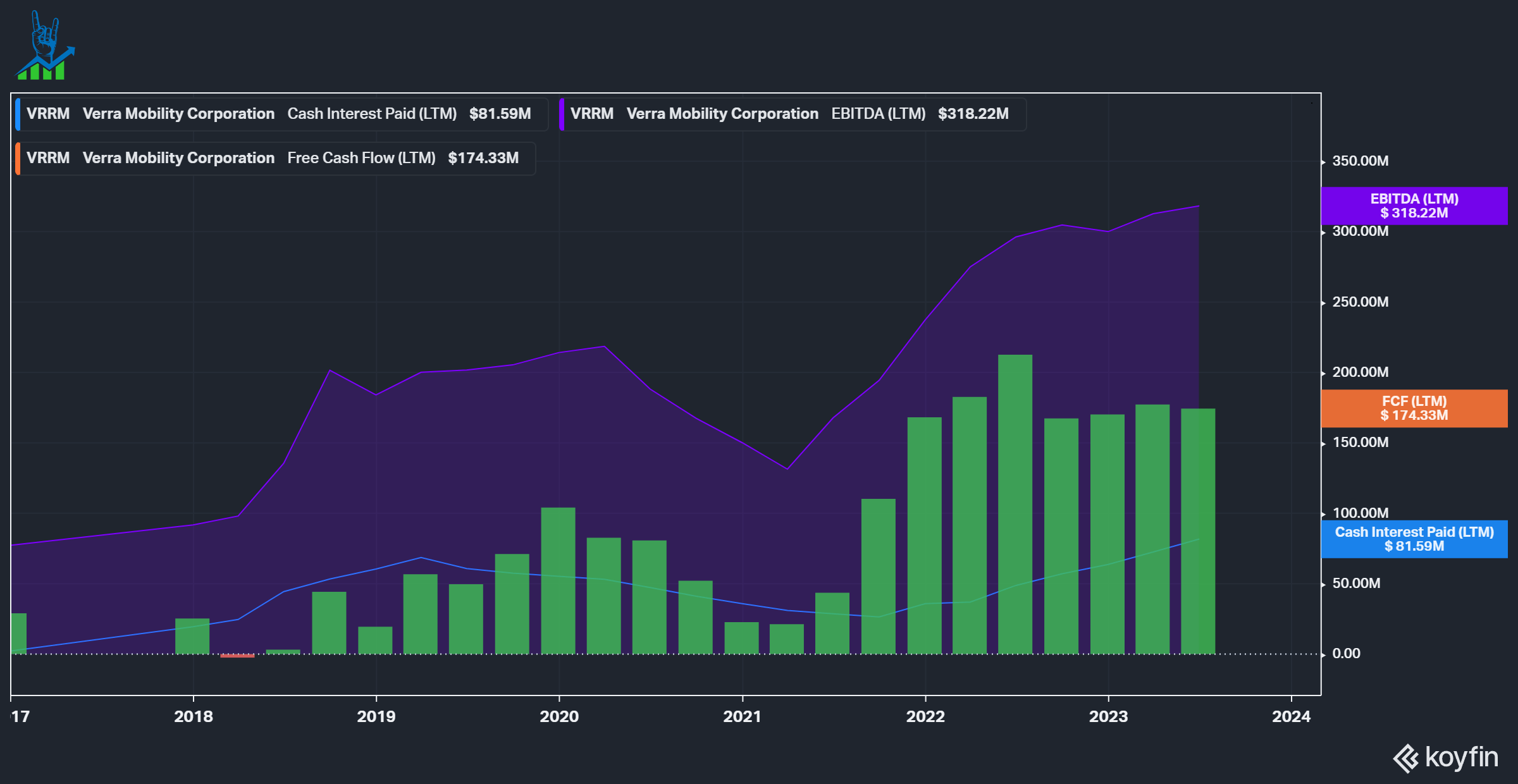

The chart below visualizes the growing concern I have about the leverage Verra has: Interest payments grew from $26 million TTM in 2021 to $81 million TTM in the most recent quarter. This represents almost half of the free cash flow the company generates and is a big headwind to cash generation. In comparison, EBITDA (which excludes interest payments) grew well, while free cash flow declined.

{kind=link}

Earnout shares

Verra did not go through the IPO route but rather went public as a SPAC. As such it still had earnout shares, which are now all issued. This was a headwind to the last quarter and increased the share count by 6 million more than initially expected.

{kind=link}

Verra Mobility looks attractively priced

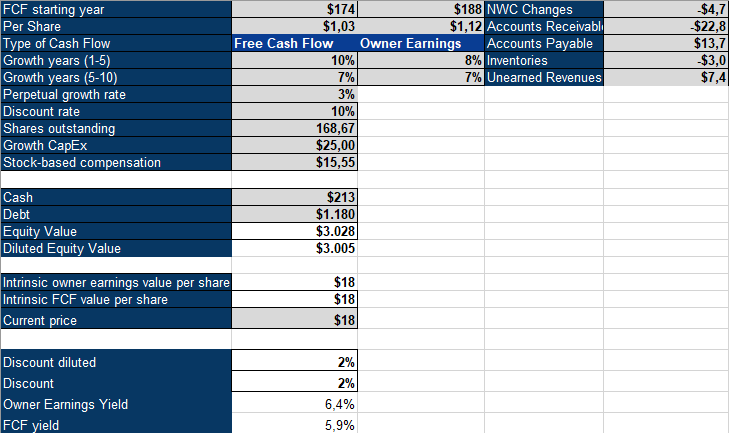

To value Verra Mobility, I'm using an inverse DCF model. I use a 10% discount rate and a 3% perpetual growth rate; I also calculate Owner Earnings besides normal Free cash flows. I believe that Owner Earnings are a better representation of the cash flows to owners than normal free cash flow, which several factors can easily distort:

- Stock-based compensation is paid out in shares and replaces cash expenses, but it is a cost to shareholders.

- Often not all the CapEx spend is going towards maintaining the business, but rather to grow it. These investments could be cut, returned to owners, and thus added back to Owner Earnings.

- Changes in Net working capital can distort cash flows, so I adjust them out.

Owner Earnings = FCF - SBC + Growth Capex +/- NWC changes.

For growth capex, I assume $25/$55 million. Verra invests primarily in new cameras, which they then operate for several years and generate recurring revenues.

Below you can see the inverse DCF model, which requires 8% owner earnings growth in the next five years, followed by five years of 7% owner earnings growth. In its Investor Day, Verra guided for 6-8% organic revenue CAGR through 2026. This excludes M&A and improvements in margins. I believe that Verra is fairly priced and continues to be a buy. Management has taken steps in the right direction and the company now moved up on my watch list again, due to better debt management.

{kind=link}

For further details see:

Verra Mobility Is Addressing My Problems With Them