CEI - Vertex Energy: Still Attractive Despite Headwinds

2023-05-10 21:28:42 ET

Summary

- Vertex Energy reported a decent quarter, benefiting from elevated crack spreads.

- The renewable diesel project start-up is delayed due to technical issues.

- Crack-spreads are deteriorating into Q2 2023, indicating lower results going forward.

- Interest expense is becoming burdensome, and management should focus on deleveraging.

Vertex Energy (VTNR) reported its Q1’23 results. The release revealed that the start-up of the renewable diesel conversion project will be delayed, due to technical problems. To make matters worse, crack-spreads are falling into Q2’23 and interest expense has nearly tripled YoY, presenting additional headwinds. In light of this, I updated my valuation of the company from my previous article. I remain bullish on the company, although my target price is now lower at around US$11/share. The most important short-term event to look for should be a timely solution of the technical problems in the renewable diesel project and the subsequent successful beginning of production. This could calm the market and possibly reverse some of the post-earnings drop in price. In addition, management should really look into deleveraging, as interest expense is becoming burdensome. Any success on that front could also act as a catalyst.

Operational overview

{kind=link}

Q1'23 highlights (Vertex Energy)

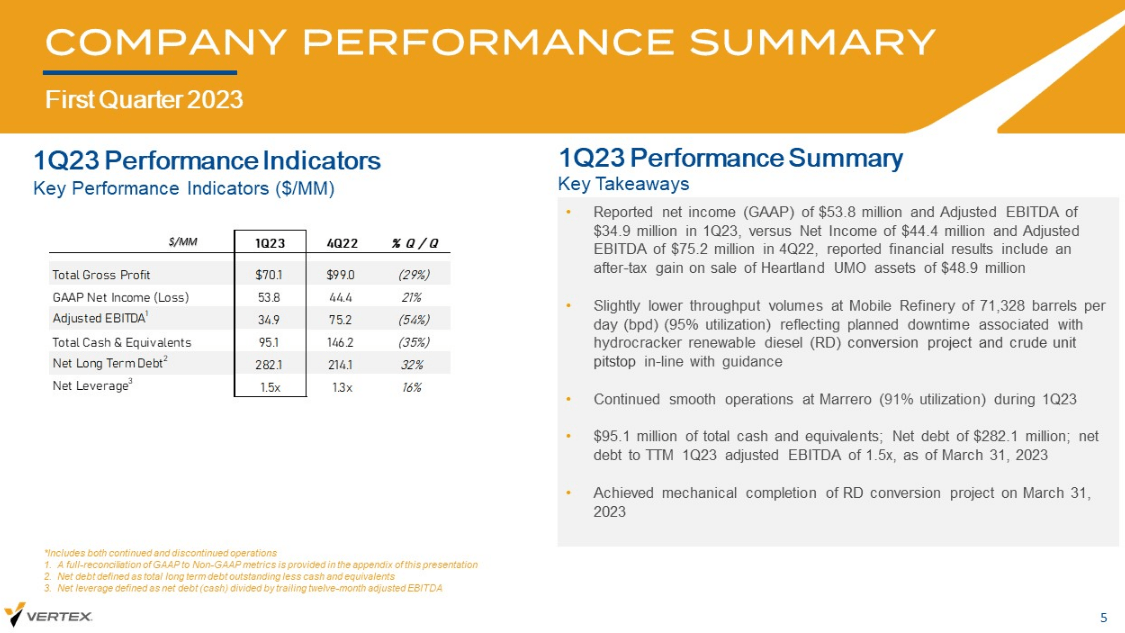

In Q1’23, the Mobile refinery operated at a slightly lower than maximum capacity, due to downtime, related to the hydrocracker conversion to renewable diesel production. As a result, the throughput averaged around 71.3k barrels/day (-8.5% QoQ), slightly above midpoint guidance. The benchmark 2-1-1 crack spread remained historically elevated and averaged at US$31.59/barrel (-6.6% QoQ) and the company achieved 51% capture rate, in line with guidance. This resulted in gross profit of US$65.5M (-27.1% QoQ). During the quarter, Vertex Energy finalized the sale of its Heartland used motor oil refinery, which resulted in booking US$48.9M net gain on the sale. This was the primary driver behind the US$53.8M of net income for the quarter, which translates into EPS of US$0.71. However, net income from continued operations was only US$3.5M or EPS of US$0.05.

Renewable diesel update

Vertex Energy managed to complete its renewable diesel conversion project, pretty much on time and on budget. However, during start-up there was a technical failure, related to the feedstock pumping system:

In the process of unit startup sequencing, we experienced a failure in the feed pumping system. These pumps are responsible for supplying feedstock to the renewable diesel hydrocracker. Upon failure, our safety systems worked as designed and our team responded appropriately to bring the unit down in a safe and controlled manner, preventing further impacts, including preserving the catalyst and our hydrocracker.

- James Rhame – COO

On the positive side, management seemed confident that the issues should be resolved by the end of May and are already working towards phase II of the project, which should increase the capacity of the renewable diesel facility to 14k barrels/day.

Balance sheet health

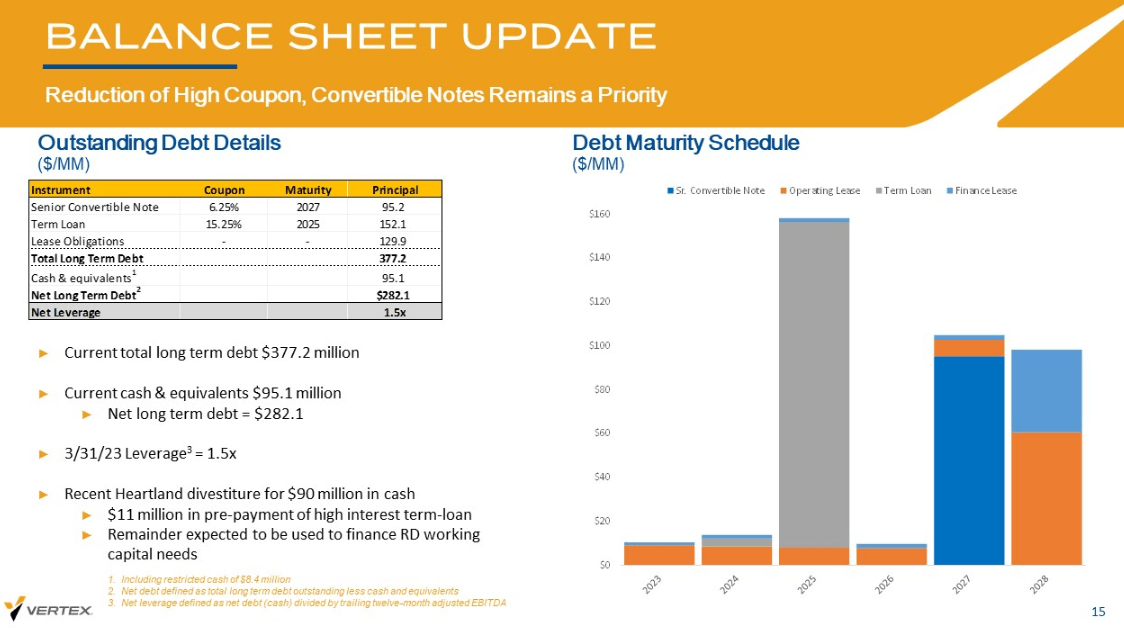

One thing that caught my attention in Vertex’s financials was the skyrocketing interest expense. The company recorded US$12.5M interest expenses, nearly trifold increase YoY. Total IB debt, including leases stood at US$377.2M as of the end of Q1’23. What’s worrying is that some of the debt is very expensive – the term loan is at variable rate, related to Prime and stood at 15.25% as of the end of the quarter.

{kind=link}

Debt profile (Vertex Energy)

Annualizing the Q1’23 interest expense, it appears that the company could be paying around US$50M on its borrowings. This is significant at Vertex’s size and management should really focus on deleveraging. Asset sales, for example, the legacy business at Marrero could help in that regard.

Forward outlook

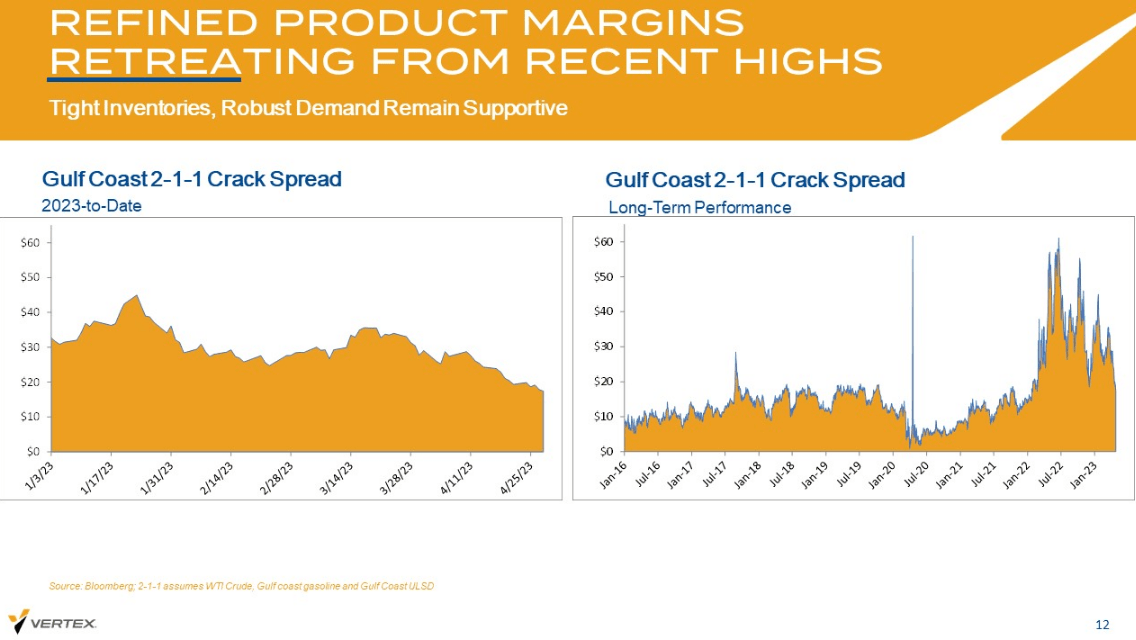

Management also issued Q2’23 guidance, envisioning slightly lower throughput between 68-72k barrels/day, and CAPEX of around US$30M. The worrying thing is that crack spreads are considerably softening into Q2’23, with the benchmark 2-1-1 crack spread dipping below US$20/barrel. This is worrying, as the Mobile refinery is expected to be the cash cow of the company, as the renewable diesel project is yet to start generating revenues and operating at full potential.

{kind=link}

2-1-1 crack spread (Vertex Energy)

Valuation

The market reaction following earnings was quite negative, with the stock price dipping about 14% for the day. So I decided to update my SOTP, reflecting a lower crack spread of US$20/barrel, compared to the previously used US$25/barrel. Also, net debt is updated, according to the latest figures.

| Mobile refinery |

| unit |

| assumption |

| Production capacity |

| kboe/day |

| 75 |

| utilisation rate |

| % |

| 95% |

| effective production |

| kboe/day |

| 71.25 |

| 2-1-1 crack spread |

| US$/barrel |

| 20 |

| capture rate |

| % |

| 52% |

| OPEX/barrel |

| US$/barrel |

| 4 |

| Gross profit |

| US |

| 166 |

| G&A |

| US |

| 40 |

| EBITDA |

| US |

| 126 |

| EBITDA multiple |

| 5 |

| EV |

| US |

| 632 |

* Author's own assumptions

When it comes to the other assets, I kept the value of Marrero at US$170M, as calculated in my previous article , using the Heartland transaction as a reference. The estimated value of the RD project is also kept unchanged from the US$392.5M value, calculated by applying 50% discount to Chevron ( CVX ) acquisition of Renewable Energy Group (REGI) and adjusting for production capacity differences.

I’d like to point out that a recent deal , where Camber Energy ( CEI ) agreed to buy a renewable diesel plant in Nevada for US$750M indicates a much larger value to Vertex’s RD facility. The plant that Camber should acquire has annual capacity of around 43m gallons/year, whereas Vertex’s RD project, assuming the phase I capacity of 9k barrels/day is 3.2x bigger. However, I’m more comfortable to keep a rather conservative estimate for the RD project of Vertex, especially before the facility is up and running and its first actual financial performance numbers are released.

| unit |

| Legacy business (Marrero) |

| US |

| 170 |

| Mobile refinery |

| US |

| 632 |

| renewable diesel |

| US |

| 392.5 |

| implied EV |

| US |

| 1194.7 |

| Net debt, assuming conversion and the cash from Heartland |

| US |

| 186.9 |

| Equity value |

| US |

| 1007.8 |

| share count |

| M |

| 91.9 |

| FV/share |

| US$ |

| 10.97 |

* Author's own estimates

The resulting FV estimate is around US$11/share or about 70% implied upside to current levels.

Risks

While the SOTP valuation indicates considerable upside, the latest market developments are putting extra risks to Vertex.

On one hand, crack-spreads are falling, eroding the refining margin of the company. On that front, the summer driving season in the US could offer some relief, as demand for fuel may pick-up. Also, the recent fall in oil prices is also lowering the cost of materials.

The other significant risk for Vertex is rather company- specific and it relates to its debt situation. The interest costs are very high and are peeling-off the company’s earnings. I think it’s very important for this issue to be addresses, potentially through selling some assets like the legacy business at Marrero or bringing JV partner on board for the RD project. Oil majors are looking into entering the RD space, as evident from the recent agreement between Eni ( E ) and PBF Energy ( PBF ) to partner in a renewable diesel project.

Conclusion

Recent headwinds are putting Vertex Energy under serious pressure. Management should focus on resolving the RD facility technical problems in the short-term and work towards deleveraging in the near-term. Despite the challenges, my SOTP valuation approach indicates FV of around US$11/share, implying 70% upside potential. That being said, the company’s risk profile has deteriorated and it may not be optimal for risk-averse investors.

For further details see:

Vertex Energy: Still Attractive, Despite Headwinds