CA - Viemed Healthcare: Qualified Growth Company HMP Transaction Accretive To Value

2023-08-15 15:36:56 ET

Summary

- Viemed Healthcare's equity stock has consolidated by ~20% after a strong rally, but the company's economic outlook remains unchanged.

- The acquisition of HMP has added potential value to VMD, expanding its geographical reach and bringing revenue synergies.

- Viemed Healthcare's Q2 earnings showed strong growth, with sales up 31% YoY, and the company expects continued expansion in FY'23 and FY'24.

- Net-net, reiterate buy.

Investment updates

After rallying hard up the page for most of 2022 into Q2 FY'23, the equity stock of Viemed Healthcare, Inc. (VMD) has consolidated by ~20%. Critically, the economic outlook of the company remains unchanged in my view, and completion of its HMP acquisition could add another $28mm to its top line almost immediately. It also continues its growth route via the contributions from its core business units, recycling and redeploying cash flows into additional inventory purchases to fuel demand.

There are multiple growth levers in VMD's arsenal in my opinion. In the last publication , I outlined the case for it to trade at $13—$17/share, and I've retained this target band following the latest investment findings. The recent pullback in market value offers a potentially exciting entry point, offering asymmetrical price returns ahead of the market's expectations (should my estimates come to fruition). Net-net, reiterate VMD as a buy.

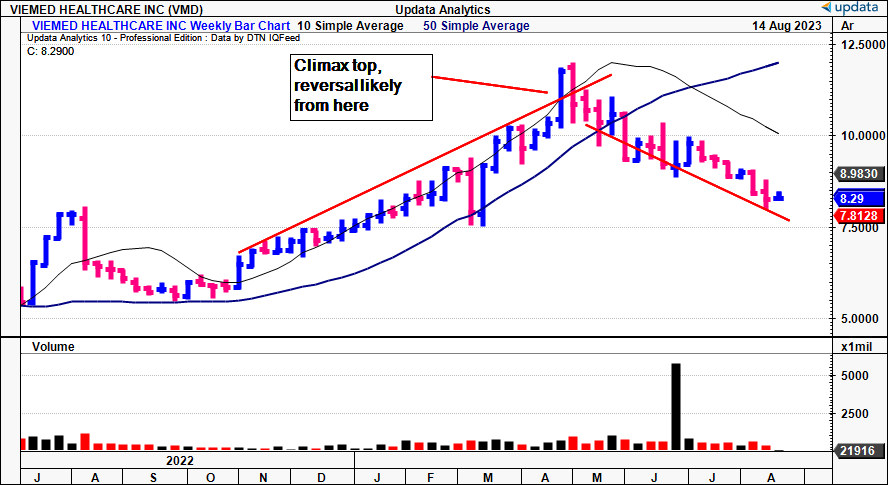

Figure 1. VMD selling into a climax top where it broke the ascending channel shown. Following this technical setup it wasn't surprising to see an exhaustion of the rally.

{kind=link}

Updates to critical investment facts

1. HMP acquisition finalized, ready to add value

The major takeout from the quarter in my opinion, was the successful completion of VMD's acquisition of HMP, finalized on June 1st. In my view, the move has added new torque to the growth engine and widened geographical reach, enhancing VMD's capacity as a larger company.

For instance, the acquisition brings a broader database, strategically distributing patient and payer networks across a broader region. Notably, HMP's business mix is ~45% in sleep and 13% in ventilation, markets where VMD excels. The acquisition is a strategic move that also brings forth revenue synergies as HMP actively expands its sleep franchise, while VMD concentrates on boosting HMP's ventilation segment.

I covered the major benefits in the last publication, but here they are again, updated and summarized:

- "Additional market share" : For one, HMP has a significant presence in Tennessee, Alabama, and Mississippi. In FY'22, HMP reported revenues of c.$28mm, accretive to VMD's top line. At present, it serves over 44,000 activations. The company booked c.$2.5mm revenues in Q2 from the acquisition already—around one month's worth of sales. Management estimates pro forma revenues would be ~$48mm ($1.25/shares) with a full quarter of HMP turnover.

- "Synergies + accretion" : As I pointed out last time, the strategic value of the deal lies in integrating HMP's respiratory team with VMD's respiratory model. This is quite the symbiotic relationship. It opens up plenty of cross-selling opportunities and revenue synergies. Moreover, if you'd have followed the VMD story to date, you'd know its 'tension points' have centered around access to human capital. Buying HMP immediately remedies this. You're looking at 172 new personnel added to the outfit who can accentuate VMD's sales power, bringing the firm's employee base to 974.

2. Q2 earnings insights

Turning to the numbers, VMD pulled in $43.3mm in quarterly sales, up 31% YoY, on adj. EBITDA of $9.8mm and operating cash flow of $7.6mm. These are up 52% and 55% from last year, respectively. Management now calls for ~$50mm in sales for Q3 FY'23 at the upper end of range. This gets me to $190mm in sales for the full-year in my modeling, ~35% growth at the top. Consensus also eyes 160% earnings growth this year to $0.42/share and projects 35% in FY'24.

Critically, the firm had 112 sales reps in the headcount as of Q2, averaging a revenue per rep of $0.386mm for the quarter [$1.55mm annualized]. It wants to expand the headcount to 115 by year end, calling each rep to hit $1.65mm to hit my top-line estimates (190mm/115 = ~$1.65mm), or, ~$1.7mm should the headcount stay at 112.

Regarding the breakdown of sales, ~60% fell to ventilator rentals during the quarter, and were up ~$3mm YoY. Other durable medical equipment ("DME") was up 71% YoY whilst equipment sales and services grew 108%.

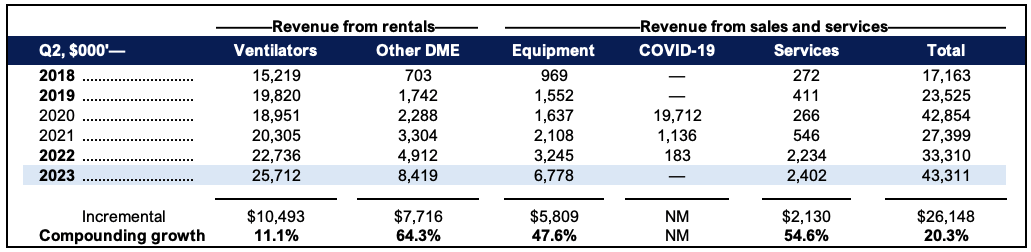

On that note, VMD qualifies as a legitimate growth company based on the following records (Second quarter 2018—'23 in Figure 2, and H1 2018—'23 in Figure 3).

Figure 2.

{kind=link}

As you'll see, it has compounded total sales at 20% YoY each Q2 since 2018, with DME and services contributing 64% and 55% compounding growth, respectively. Ventilator revenues have added 11% each year on the same convention.

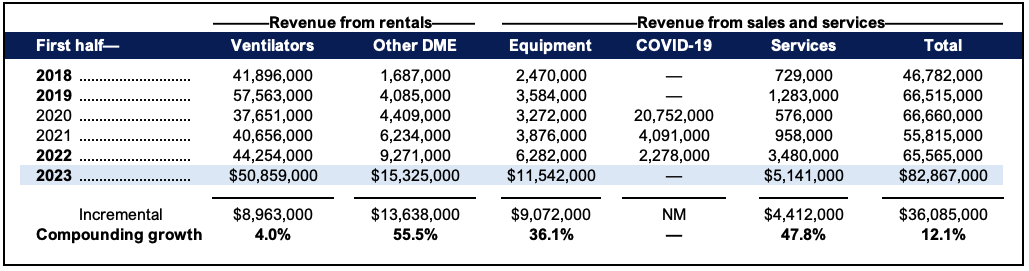

Similarly, in each H1 period from 2018—'23, you've got VMD growing at an average range of 12% with similar growth drivers as above.

Critically, both management's, consensus' and my own estimates have the company to grow at a faster rate than its historical averages with the HMP contributions. At $190mm, this calls for ~35% expansion as mentioned, around 2.9x the historical H1 figures outlined below.

Figure 3.

{kind=link}

3. Capital investments and new commitments

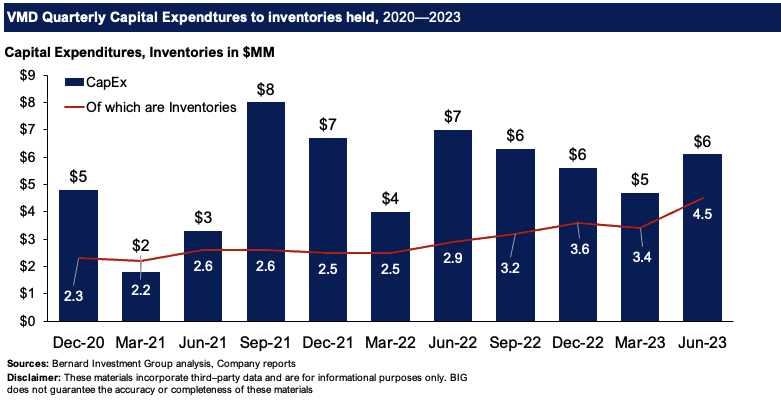

During the quarter, it redeployed $6mm of cash into growth and maintenance CapEx. Most of CapEx was directed towards vent and oxygen products. The use of cash to inventory vs. the remainder of quarterly CapEx is noted below [Figure 4]. Inventories are trending higher along with sales growth, whilst the company looks to be recycling cash flows back into additional inventory sales. That's really the model here for now—get the sales force to sell more units to produce cash flows, recycle these back into additional inventory, get the sales force and existing base to purchase more of these.

Figure 4.

{kind=link}

Investors have provided the company with $116mm in capital value up to Q2, of which the firm has put $108.7mm, or 93% at risk into operations [Figure 5]. Excluding cash and interest-bearing liabilities, it has only placed ~84.5%. Good thing is that it still has ~$10mm in cash on hand and plenty of headroom for new capital commitments (I'm thinking inventories and other tangibles here).

Of the capital provided and deployed into the business, VMD has produced $7.4mm in trailing post-tax earnings, and rotated $17mm of cash into new commitments last quarter. Surprisingly, the company's profits are driven by capital efficiency, with invested capital turnover ranging from 1.4-1.5x over the last 2 years. Consider the following points:

- This is reasonably high for a firm that listed ~6 years ago in my view. This relates to VMD's high tangible intensity via its inventory volumes.

- Relatively high capital turnover implies the firm employs a cost leadership strategy. That means pricing its goods below industry averages.

- The below-average pricing is supported by the efficient use of capital, which allows a lower pricing margin, given the turnover of cash tied up in the firm's investments is also reasonably high.

- As a reminder, firms can arrive at the same capital productivity by many drivers. So it's plausible VMD will move from a cost leadership strategy to a differentiation strategy, aiming to build basis points onto post-tax margin to grow its competitive advantage.

- VMD presents with these economic characteristics and arrives at a 6.8% return on existing capital but has grown its profits incrementally by 29% in Q2 last year and another 11% this year (note, this calculation is done sequentially from Q1—Q2 in both of these years, using TTM values). Net-net, the effect is that ~$19mm of cash flow to owners has been recycled back as inventory (note the change in NWC density as $19mm as well).

Figure 5.

Sources: BIG Insights, Company reports

Valuation and conclusion

VMD sells at ~ 20x forward earnings and 11x forward EBITDA, both discounts to the sector of 2% and 26%, respectively. Its net assets are valued at $3 for every $1 of market value, and you're getting a 10.7% cash flow yield from trailing OCF.

In the last VMD profile, I outlined the case for VMD to grow its intrinsic value to $13—$17/share. I called for $60—$77mm in earnings after tax from an additional $400mm in CapEx by FY'25, otherwise 13.2%—17.4% return on incremental capital deployed (($60, $77–$7.4 = 52.6)/400 = 13.15%—17.4%).

With the findings shown today, I am reiterating these estimates, getting me to $17/share (60, 77/0.12 = $500—$641 = $13–$17/share). Critically, these are asymmetrical to the market's view. At $316mm in current market cap it looks to $38mm in earnings ($38/0.12 = ~$316), therefore implying a potential mispricing. I'm not sure how far out the market is forecasting, but if it's to 2025—there is where the possible dislocation is between estimates. Mind you, it's still a considerable compounding growth rate of ~72.5% in the next 3 years ((38/7.4)^(1/3)-1). Over the next 5 years, it is 38.7% CAGR.

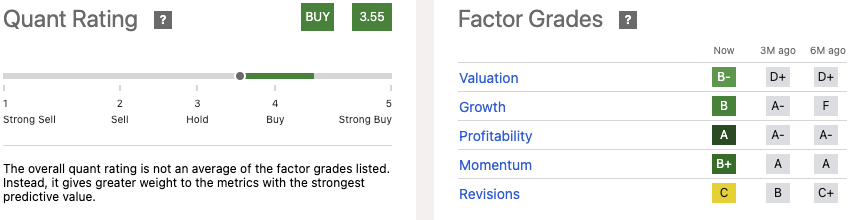

Similarly, the quant system has deviated to a buy as of this week, adding a layer of confidence to the estimates outlined above.

Figure 6.

{kind=link}

In short, the economic data supports VMD as a buy in my opinion. The case outlined here draws on sales data, capital productivity, and, in particular—profitability. The market's expectations have narrowed down from the last publication, but this may be over-extended and I've retained my FY'25 growth estimates on the company, looking to

For further details see:

Viemed Healthcare: Qualified Growth Company, HMP Transaction Accretive To Value