VFF - Village Farms: Plenty Of Headwinds Remain

Summary

- Gross margin from Canadian cannabis and produce got crushed in the latest quarter.

- The company faces many headwinds including cannabis oversupply, fresh produce issues gross margin, input costs, and FX.

- VFF has an interesting strategy of competing for Canadian market share as others abandon the market - it could pay off once excess capacity subsides.

- I think it's time the company seriously considers selling off its weak Produce segment.

Village Farms International, Inc. ( VFF ), is a Canadian-based company that primarily competes in the following segments: Produce, Cannabis-Canada, Cannabis-U.S. It started to gain some momentum in revenue growth in the latter part of December 2020.

It appears it will be able to retain that momentum in 2022 and possibly in 2023, but it has a number of headwinds it faces, and even if revenue does continue to grow, it has been doing so with declining gross margins and at a net loss.

Among the headwinds, the company continues to face are cannabis oversupply, lower customer spending in the U.S., fresh produce issues, gross margin, high input costs, and FX.

It's going to take some time for all of these to improve, so while the company aggressively pursues taking cannabis share in Canada, its U.S. produce business remains under stress. On the other hand, its U.S. cannabis business has been growing at a decent pace in the first nine months of 2022, and if it can continue to do so, it should help bolster some of the declining gross margins in produce and Canadian cannabis

The modest amount of U.S. cannabis sales won't have an immediate effect on gross margin, but over time, assuming growth continues that includes favorable gross margin, over time it could be one answer to its margin and overall earning challenges.

In this article, we'll look at some of its recent earnings numbers, the challenges it continues to face, and how 2023 may be shaping up.

{kind=link}

Some of the numbers

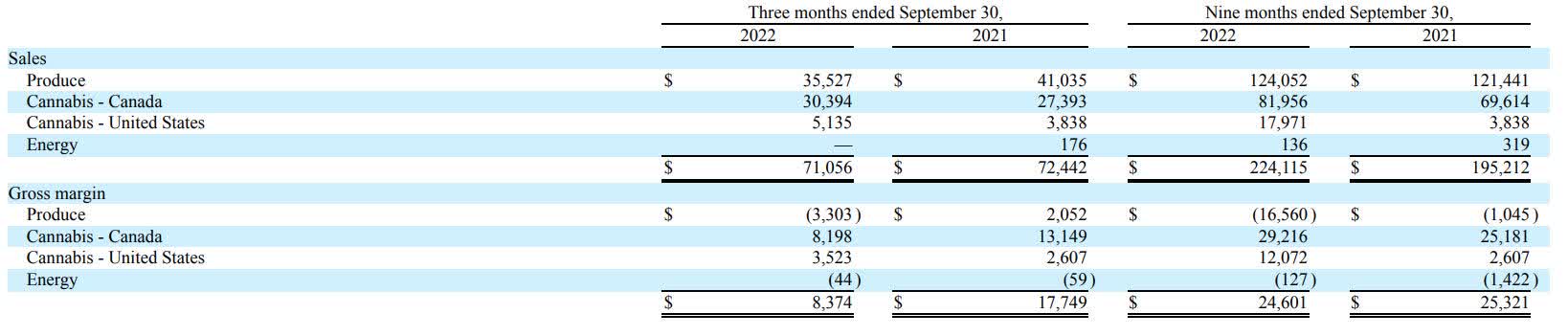

Revenue in the third quarter of 2022 was $71.1 million, down 2 percent from revenue of $72.4 million in the third quarter of 2021. Revenue for the first nine months of 2022 was $224 million, compared to revenue of $195 million in the first nine months of 2021.

Revenue from Produce was $35.5 million, compared to $41 million in revenue from Produce in the third quarter of 2021.

Revenue from Cannabis-Canada was $30.4 million, compared to $27.4 million in revenue in the third quarter of 2021.

{kind=link}

Revenue from Cannabis-United States was $5.1 million, compared to revenue of $3.8 million in the third quarter of 2021.

Gross margin in the third quarter of 2022 was $8.4 million, compared to gross margin of $17.8 million in the third quarter of 2021. Gross margin for the first nine months of 2022 was $24.6 million, compared to gross margin of $25.3 million in the first nine months of 2021.

The weakness in gross margin is likely to continue throughout 2023, based upon the headwinds mentioned above, which should continue on through the first half of 2023, and probably longer. The reason I believe that is because not all the headwinds are connected to macroeconomic challenges.

Net loss in the reporting period was $(8.7) million, or $(0.10) per share, compared with net income of $0.8 million, or $0.01 per share in the third quarter of 2021.

Adjusted EBITDA was negative $(2.2) million, compared to positive adjusted EBITDA of $6.9 million year-over-year.

Thoughts on Produce segment

Even though Produce generates the most sales for VFF, I think the company should seriously consider selling off the business in order to focus on its core competency of cannabis.

Some of the reasons include the low margins in that particular sector in general, but also its susceptibility to disruption from factors like disease and high input costs, which the segment has been experiencing recently.

When combined with the low margins associated with the produce industry, in particular, anything that is a negative catalyst can have a disproportionate effect on gross margin and earnings. And since it's the largest generator of revenue for the company, it has a strong impact on its performance from quarter to quarter.

Not only does diseases like the brown rugose virus that is hitting the tomato market around the world, which not only lowers production and revenue but also increases costs. Add to that the current high input costs associated with freight, and it's easy to see produce is more vulnerable to unforeseeable events and economic conditions than cannabis is.

The major problem is costs in agriculture are, for the most part, fixed, so when if conditions emerge which lower production volume, the company has less capital available to cover costs.

Another lesser-known factor in the third quarter was the delay in the crop cycle because of operational changes in the U.S. H-2A worker program.

The point is, in produce, everything has to go just about perfectly in order for the segment to perform at even moderate levels.

This isn't just about one quarter, either. For the first nine months of 2022, the segment had a gross margin of negative $(16.6) million, compared to negative gross margin of $(1.05) million in the first nine months of 2021.

Taking into consideration it being a low-margin business to begin with, I think selling the unit and focusing solely on cannabis in the U.S. and Canada would be a positive step by VFF.

Management said it's doing a review of Produce, and hopefully, the result will be a decision to sell it rather than try to incrementally improve it in some way.

Gross margin in general

Gross margin isn't just a Produce problem, either. Gross margin in Cannabis-Canada dropped almost the same as Produce did, although it was done from a smaller base.

The problem with gross margin, EBITDA and net loss in the quarter, I see as coming from factors such as Canadian cannabis oversupply, fresh produce issues, rising input costs, and FX. These are related to macroeconomic or industry-specific effects that are taking a toll on the performance of VFF, even as they are able to boost revenue.

Canadian cannabis oversupply

Canadian market oversupply of cannabis has been around for a while, and it continues to compress prices, resulting in contracting margins. That said, capacity in the Canadian market is being removed, so over time supply and demand will more accurately align with one another, which will bring prices and margins to levels reflecting actual market conditions.

VFF management pointed out that while there is pressure on cannabis prices in Canada, the market on a volume basis is growing at about twice the rate of sales in the U.S. dollar. The combination of lower capacity and moving volume will help to accelerate the process of lowering supply and ultimately increasing prices. It'll take a little time, but it's already moving in that direction.

The company, while acknowledging the impact on the top and bottom lines, sees this as an opportunity to grab market share, and has been doing so under difficult market conditions.

So while its competitors are cutting back or waiting for more favorable conditions, VFF has been aggressively growing market share. If it is able to maintain and grow its customer base via branded products, when market conditions are more favorable, the company should be positioned for a profitable, long-term run.

That time isn't now, but it could come in the not-too-distant future, as long as prices don't remain lower for longer.

Conclusion

VFF has proven it can take market share and grow under challenging market conditions in the cannabis segment, but it's still doing so at the expense of margin. Its strategy can continue to work as long as market conditions don't fall off the cliff.

In the near term, the company still faces some stiff headwinds that aren't going away anytime soon and will continue to face some revenue and margin compression through much of 2023, and possibly longer, depending on how deep and long the recession goes.

As for immediate steps the company can take, I think selling off its Produce unit would be an excellent step that would be approved of by shareholders and the market in general. I don't see much improvement left in that segment of the company, even if conditions turn more favorable.

On the other hand, for its cannabis business, it would allow for the company to focus on its core competency and not be distracted by issues related to its produce business.

That would of course result in an immediate and significant decline in revenue, but when considering the small impact it has on the bottom line in the best of times, I think it would be a positive once investors get used to what I think would be temporary lower numbers.

Over the long term, VFF is positioned well for sustainable growth once economic conditions improve, and its share price should reward those in it for the long term. In the short term, it's going to remain painful until the headwinds dissipate and the company accelerates its growth momentum; that's going to take some time.

For further details see:

Village Farms: Plenty Of Headwinds Remain