VIPS - Vipshop: An Attractively Priced Recovery Play

Summary

- Vipshop outperforms its guidance in Q2 2022, as a demand recovery looks to be taking shape.

- Massive spending cuts also continue to boost earnings growth, and if management can balance cost discipline with a consumption recovery, I see further upside from here.

- With a ~$1bn buyback in place and ample cash on the balance sheet, the stock offers compelling downside protection as well.

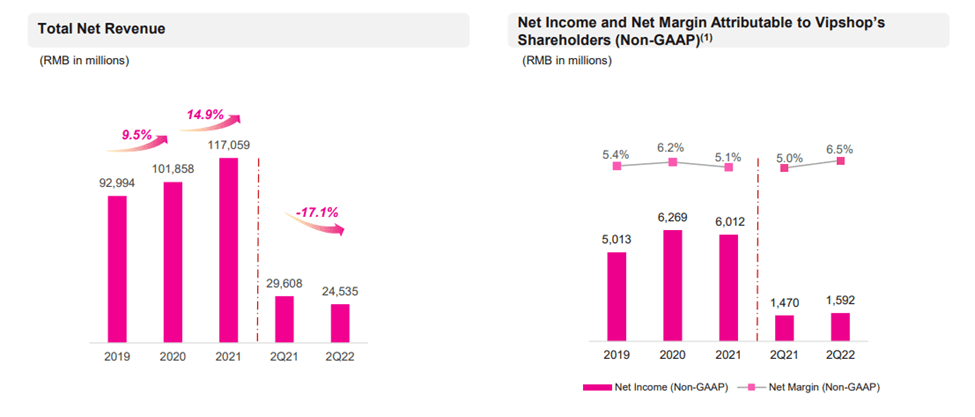

Vipshop ( VIPS ) saw a better than expected Q2 2022 revenue decline of -17% YoY and a non-GAAP net margin of >6%, both of which came in well ahead of management guidance. The key driver was a significant >60% YoY cut in marketing costs as well as a slower -18% YoY quarterly decline in customers. The momentum looks set to continue into Q3 2022 as well, with revenue guidance at -10% to -15% YoY on the back of an expected return to positive user growth. Given management commentary that the revenue recovery is picking up pace in July and early August (relative to the June base) and the narrowing YoY decline, I suspect there is some buffer in the guidance numbers as well. To be clear, there remain risks to the near-term growth path, with consumer sentiment weakness, a COVID-19 resurgence, and weather fluctuations potentially weighing on the outlook. That said, expectations are low at the current ~8x fwd P/E (well below its long-term average), while the ~$4/share of net cash and equivalents (including short-term investments) and ~$1bn buyback program offer investors ample downside protection.

Cost Cuts and Emerging Recovery Signs Drive Quarterly Outperformance

Revenue remains in decline, but the better-than-expected -17% YoY for Q2 2022 (well above the previous -25% to -20% YoY guidance range) will come as a welcome relief to investors. Key revenue drivers include a ~18% YoY decline in active customers to ~42m during the quarter amid COVID lockdowns and weak apparel demand, while orders per customer came in at a surprisingly solid YoY increase. In contrast to a ~16% YoY decline in gross merchandise value (GMV), GMV per order was broadly flat YoY as well. Per management, operating metrics have been consistently improving over the April to June period, with June declines narrowing to the single digits % on an emerging (but still modest) consumer demand recovery and a gradual supply chain/logistics normalization (e.g., express delivery).

{kind=link}

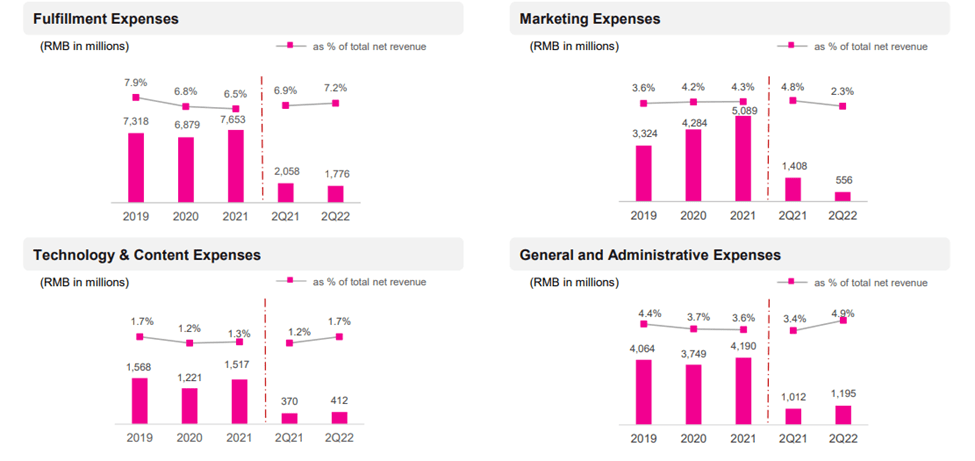

The bottom-line beat was the key highlight, though, with the adjusted net margin reaching 6.5% (vs. the previous guidance of 5%). Driving the profitability improvement was a significant ~60% YoY cut in marketing spending to RMB556m, as well as disciplined promotions over the quarter. In addition, a one-off FX gain of ~RMB217m also contributed to the positive delta, partially offset by higher tech/G&A expenses. Some of the margin gains should stick, given management commentary that it had cut back on subsidizing promotions and suspended low ROI marketing spending to sustain a stable YoY gross margin trend going forward. In the meantime, live streaming appears to have had a limited impact on VIPS, validating its decision to focus on the apparel category (vs. the more standardized product focus of live streaming platforms).

{kind=link}

Hints of Conservatism in the Near-Term Guidance as Management Tone Turns Positive

Building off the strong results, management pegged soft Q3 2022 revenue guidance at -15% to -10% YoY to RMB21.2-22.4bn and a stable adjusted net margin of >5% for H2 2022 on more stringent product selection and disciplined marketing spending. Of note, management is also accounting for potential negative impacts from COVID lockdowns, consumer confidence, and weather conditions in its guidance - despite noting a sequential improvement to high-single-digit YoY declines in July/August (vs. June). That said, VIPS will need to balance planned spending cuts with new customer acquisitions and registered reactivations (e.g., pre-installation, channel spending, and coupons) as the consumption recovery gains traction following the exit from full lockdown.

Still, the strong beat in Q2 2022 shows the guided 10-15% YoY decline for the upcoming quarter could prove conservative, in my view. On earnings, bears might point to management's aim to push active customer growth back into positive territory in Q3 2022 as cause for concern, but given the low base (active customers stood at 41.7m in Q2 2022 vs. 43.9m in Q3 2021), the marketing spending requirement will likely remain relatively low. Still, discipline will be key as management indicated few low-hanging fruits on the gross margin side following the significant measures implemented over the past few quarters.

Beyond the next quarter, VIPS also sees a better growth outlook in Q4 2022 (a typical peak season for the company), with revenue potentially even turning positive if it can secure active customer growth in Q3 2022. Meanwhile, higher margins are also well within reach if management can keep sales & marketing expenses lower YoY via efficiency gains and spending discipline. For context, VIPS currently has an RMB100mn budget for S&M available to deploy among new or inactive registered customers, in addition to the existing customer base. Even if we assume Q3 2022 adjusted marketing expense of ~RMB100m QoQ (~70bps higher as % of revenue), operating leverage gains from a recovery should allow the Q3 2022 adjusted net margin to improve to the >5% target, in my view. The margin outlook for Q4 2022 will be more uncertain, though, depending on marketing spend, but a YoY improvement to >5% should still be well within reach.

An Attractively Priced Recovery Play

The recent VIPS stock price boost following its latest earnings beat and raise could be a sign of things to come. While bears might point to VIPS' significant marketing expense cuts leaving limited room for further margin upside, the accelerating growth momentum (per management, the revenue recovery is picking up pace in July and early August) should more than compensate into Q3 2022. With revenue guidance also at a conservative -10% to -15% YoY range despite calls for an expected return to positive user growth and the YoY decline narrowing, there could be room for upward revisions down the line. Yet, expectations are low - the stock is currently trading at a discounted ~8x fwd earnings, presenting an attractive play on the improved VIPS outlook. The balance sheet also provides downside support, with net cash and investments of ~ $4/share available to fund more buybacks over the coming months.

For further details see:

Vipshop: An Attractively Priced Recovery Play