VC - Visteon: Compelling Entry Point To A Long-Term Growth Story

2023-11-14 09:18:56 ET

Summary

- Visteon offers pure-play exposure to the trend of automotive digitization.

- The company's share price has fallen over 30% due to a slowdown in EV growth and UAW strikes but headwinds are temporary.

- Valuation models indicate compelling upside potential with a strong margin of safety.

- Visteon stock rated as a buy at current levels.

Overview

Visteon Corporation ( VC ) supplies cockpit electronics to the automotive sector.

Their share price peaked at an all-time high back in March but has since fallen over 30%. In my view the selloff was a justified response to a slowdown in EV growth, a selloff that intensified during the rolling UAW strikes.

However, I argue in this report that these headwinds are temporary and the share price has overshot fair value to the downside.

The three different valuation models we look at for this analysis indicate upside potential between 28-43%. Moreover, the primary factors that most influence VC share price are all trading at levels that historically have presented attractive entry points.

In my view, Visteon Corporation stands out as a pure-play in the growing sector of cockpit digitization and is trading at one of its most compelling points of entry in many years. I rate VC a BUY.

Visteon Snapshot

Since emerging from bankruptcy in 2010 Visteon has grown into a ~$3B market cap tier-1 supplier of automotive electronics.

As a supplier of cockpit electronics, Visteon offers investors pure-play exposure to one of the primary trends in the automotive sector : the digitisation of automobiles.

Their products include digital instrument clusters, lighting, and battery management systems, serving customers across US, Europe, and China. If you're driving a high-end vehicle with a curved digital display spanning the entire dashboard , it's quite possible it was designed by Visteon.

One of their most exciting products is SmartCore technology , which integrates the instrument cluster, HUD, and infotainment into a single controller. Over time, this will reduce wiring and weight, and most importantly, cost. VC are positioning well to become a core component of global OEM future vehicle programs.

Reasons for Selloff

VC peaked back in March and has since dropped over 30% while the sector is flat and SPX is up over 10%. The selloff occurred over multiple stages.

VC initially fell 15% after their April earnings update, despite holding guidance. Part of the selloff may have been disappointment they didn’t raise guidance, but this was consistent with the sector. More likely was an update by Mobileye at that time, citing a slowdown in EV sales in China. VC has direct exposure in China and also via EV-related sales into GM.

In July GM informed the market that they're behind schedule in the rollout of their Ultium modular battery system. VC is the primary supplier of GM's battery management system so this added to the selling pressure.

And then came the rolling series of UAW strikes which impacted the whole sector. Of the big three in Detroit, VC is most exposed to Ford. When Ford agreed to a 25% wage hike the market immediately reacted. I'm not concerned about the short-term impact - it's done and is already factored into guidance and share price, with VC stating a $25-30m impact this financial year. Indeed, we now have a tailwind to full-year guidance given VC assumed the strike would last until Thanksgiving.

All these headwinds are temporary by definition. Over time, EV growth will return at scale and GM will eventually get its Ultium battery modules launched.

My concern for VC is the impact of the UAW strikes over the longer-term, and for me this is one of primary risks to the investment thesis. Having worked at both Ford (F) (as an engineer) and GM (GM) (in Finance) I have some insight into how the OEMs will try to pass through the increased wage costs they’ve just agreed to. During my time at GM (in Australia) it was common practice to demand to see cost structures from suppliers and then dictate the price we’d pay. It was brutal but effective. And it was not a one-off exercise. We ((GM)) would demand annual cost-downs over the life of the program on the expectation that suppliers would find ways to become more efficient. The issue for suppliers of course is that these benefits then go direct to the OEM.

So here's the challenge for Visteon. The high upfront R&D costs that go into their product suite means R&D forms a significant proportion of the overall 'piece cost'. It is hard to find repeatable efficiencies at research stage, so Visteon will need to defray these costs over higher volumes to maximise the manufacturing percentage of each 'piece'. Why? Because it's the manufacturing processes that offer the most opportunities for regular cost-downs over time.

Therefore the critical success factors that I'll be monitoring over the next few quarters are the size of their new business wins. If they can grow volume in proportion to their higher R&D spend then Visteon becomes a compelling long-term growth story. Let's now look at their recent earnings update to see evidence of early progress.

Recent Earnings Update

Revenues this year will likely hit $4B , focussed across instrument clusters (~50%), infotainment displays (~25%), and climate controls. In addition, VC expects significant growth from its Battery Management Systems, with potential for $600m in revenues from this division by 2026-27.

In their latest update (October), VC reported new business wins of $5.8B YTD, up from $5B YTD in 2022. Management highlighted that one of their largest wins was a cockpit controller program with a German OEM across both ICE and EV platforms, underpinning strong growth expectations in coming years. This is good news and strengthens the investment thesis.

Investment Thesis

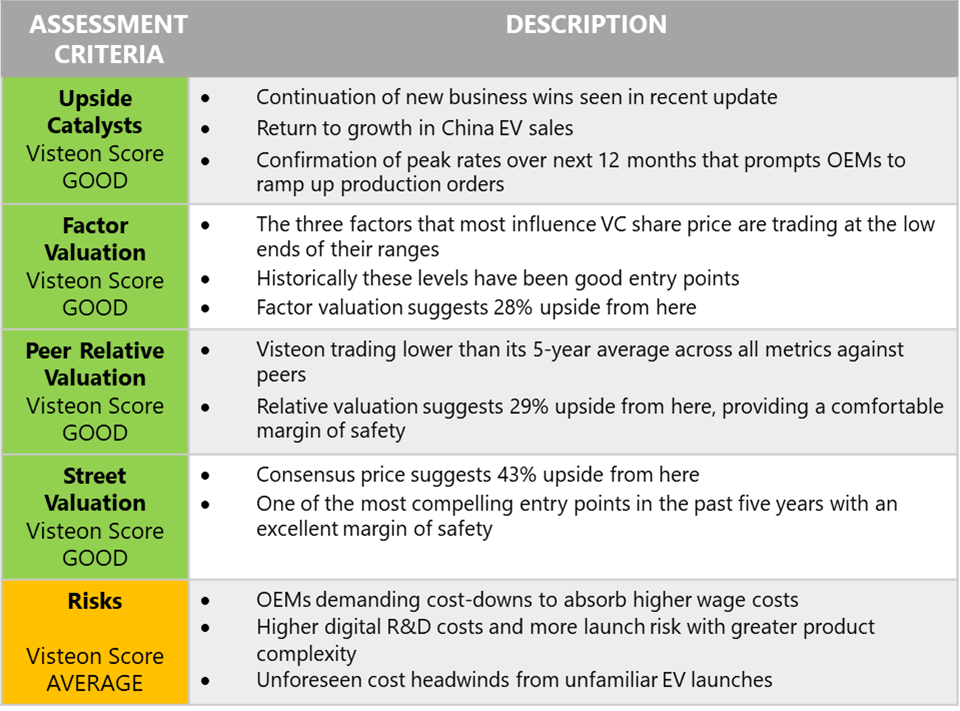

In my experience appealing investments score highly across five areas. I like candidates where both historical and forward-looking valuations combine to suggest a strong margin of safety, with clear upside catalysts, and low trade risks. For VC I have assigned four 'Good' scores, and one 'Average'. In my opinion Visteon is a 'BUY' at current levels.

Summary of Investment Thesis (FactorRank Analysis)

{kind=link}

On the following pages I explore each of these five assessment criteria in more detail.

Upside Catalysts

Summary of Upside Catalysts (FactorRank Analysis)

{kind=link}

There are a number of catalysts that could underpin a share price rally. Let's start back in August when Visteon reported results . The market received these results very positively, with price rallying almost 7% on the day. Wall St analysts also responded positively, with four immediately upgrading price targets up by an average 2.5%. Seeking Alpha analysts also chimed in, one with this excellent article . Of course, the rally was all over a few days later as the UAW strike threat emerged, but looking at VC without the lens of the UAW strike, one could argue that the market was seeing some catalysts already in place.

Going forward, I expect the most likely rally catalysts will come from continuing new business wins. It's useful to note that the new business that VC reported in their October update came primarily from cockpit-electronics rather than EV-related wins, the latter which appears to be flat YTD. Given that Visteon confirmed full-year guidance without these EV-wins, any return to growth in the EV space could arguably trigger a rally.

More generally, availability of semiconductors will likely ease over the next 12 months which will help OEMs smooth their manufacturing processes. And if interest rates do indeed peak over this time frame then OEMs may respond by ramping production to meet a potential surge in demand from consumers.

Factor Valuation

Factor Valuation Summary (FactorRank Analysis)

{kind=link}

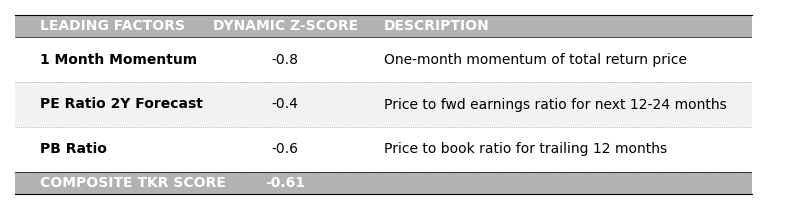

For Visteon we analysed 34 different factors (see list in appendix of this report ) to understand which have the most influence on price. For the past five years we found VC price is most influenced by three factors: one technical and two fundamental:

Leading Factors (FactorRank Analysis)

{kind=link}

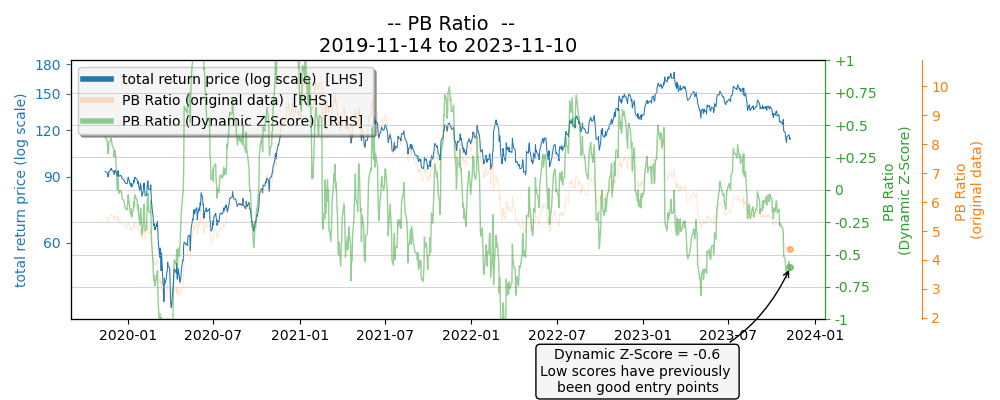

Looking at the following three charts, when these factors trade at Dynamic Z-Scores below -0.5 they have previously shown to be good entry points. See how we calculate these scores in the appendix of this report .

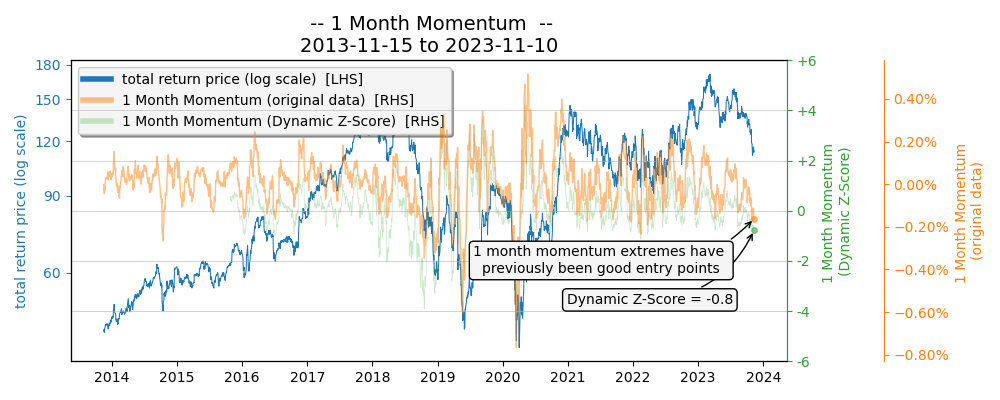

VC Factor 1: 1 Month Momentum

VC 1 Month Momentum (FactorRank Analysis)

{kind=link}

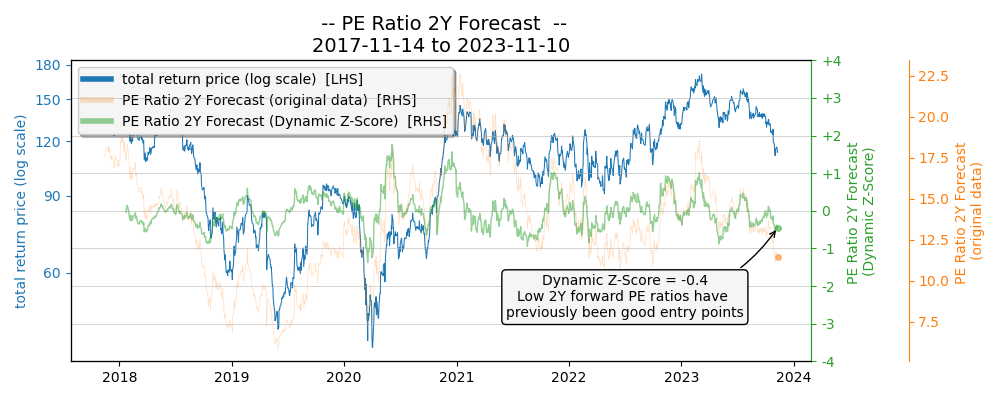

VC Factor 2: PE Ratio 2-Year Forecast

VC PE Ratio 2Y Forecast (FactorRank Analysis)

{kind=link}

VC Factor 3: PB Ratio

VC PB Ratio (FactorRank Analysis)

{kind=link}

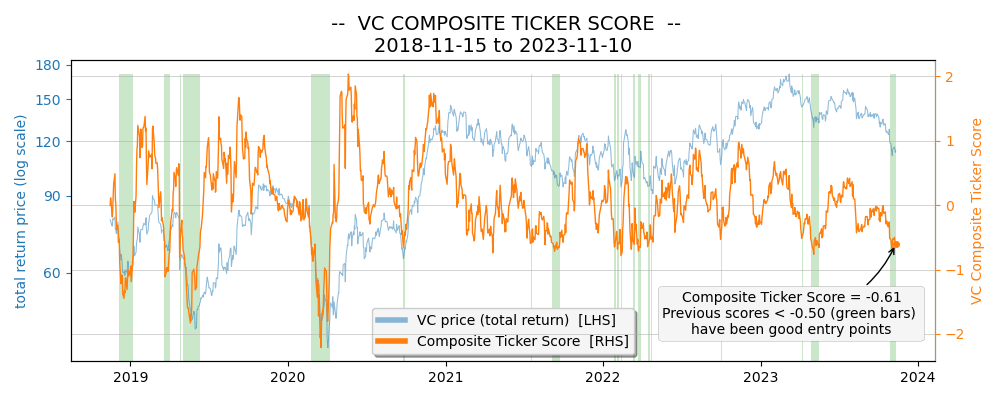

When combined into a Composite Ticker Score (orange line below) we can see that previous scores below -0.5 (green bars) have generally been good entry points. At time of writing we're sitting at -0.61 which is compelling support for the investment thesis.

VC Composite Ticker Score (FactorRank Analysis)

{kind=link}

Assuming our two leading fundamental factors (PB and Forward PE ratios) return to their 5-year averages we calculate an implied share price of $146.40, or 28% potential upside from here.

Factor-Based Implied Share Price (FactorRank Analysis)

{kind=link}

This is an appealing upside that I believe brings an acceptable margin of safety, hence I assign a 'Good' score to the Factor Valuation component of the analysis.

Relative Peer Valuation

Relative Peer Valuation Summary (FactorRank Analysis)

{kind=link}

Peer group members are from the same industry, show strong correlation and/or cointegration, and have good data quality. The peers for this analysis are [[VC]], [[ADNT]], [[APTV]], [[BWA]], [[DAN]], [[FOXF]], [[GNTX]], [[LCII]], [[LEA]], [[MOD]], and [[PATK]].

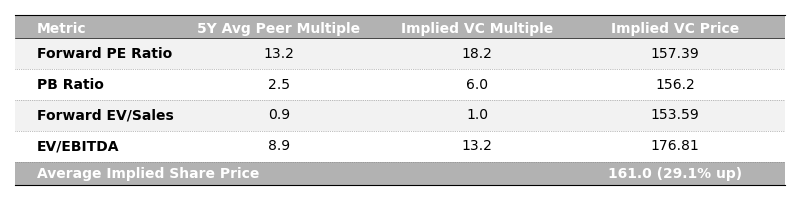

Across all metrics, VC is trading lower than its 5-year average relative to peers ( peer list in appendix):

Historical Range Chart (FactorRank Analysis Based on Peer Company Data)

A quick interpretation of this range chart using 1-year forward PE ratio (top line) as an example: During the past 5 years VC traded at a 38% premium to peers; during this period it ranged between a 33% discount and a 166% premium to peers; it is currently trading at a 14% premium after falling 24 percentage points.

Given our view that the VC selloff is temporary we will assume a return to trading at historical peer multiples for this calculation. In this case we get an average implied share price of $161, or potential upside of 29%.

Again, this is an appealing upside that we believe brings an acceptable margin of safety, hence we assign a 'Good' score to the Relative Peer Valuation component of the analysis.

Relative Value-Based Implied Share Price (FactorRank Analysis)

{kind=link}

Street Valuation

VC Street Valuation Summary (FactorRank Analysis)

{kind=link}

Twelve analysts have updated their target prices since VC reported October earnings. One upgraded their rating from Hold to Buy.

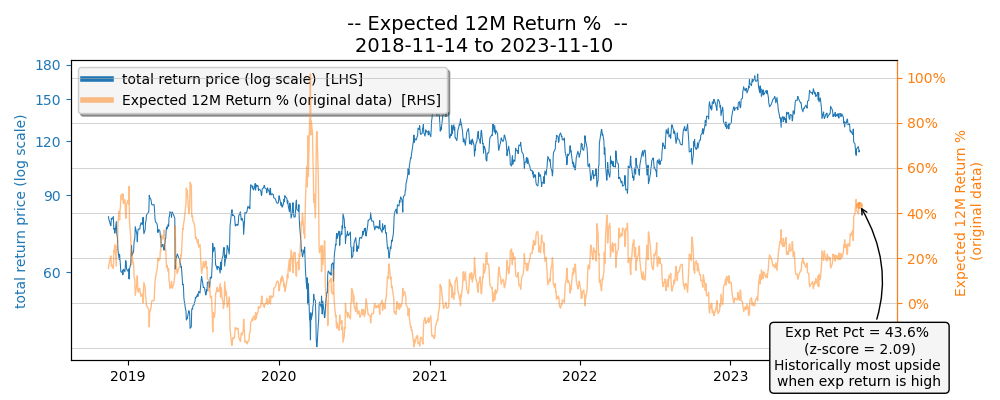

Expected 12M return is now 43% which is the highest it's been since the COVID plunge in 2020. As the chart below shows, previous upside extremes of this metric (orange line) have been good entry points.

This is a compelling upside that we believe brings a strong margin of safety, hence we assign a 'Good' score to the Street Valuation component of the analysis.

VC Expected 12M Returns (FactorRank Analysis based on Analyst Target Prices)

{kind=link}

Risks

VC Risk Summary (FactorRank Analysis)

{kind=link}

One could argue that the majority of risks facing Visteon are 'business-as-usual' for a growing technology-based sector. The outlier however is the risk from OEMs demanding cost-downs to help absorb their higher wage costs. In my view this is likely to be a real and unrelenting challenge for the next 3-5 years.

As I discuss here , the primary risk to this investment thesis is the pressure on VC for cost-downs that all OEMs will place on their suppliers after the recent UAW wage agreements. Suppliers delivering parts that have a high proportion of manufacturing costs will find it easier to find efficiencies than suppliers like Visteon where R&D is a higher proportion of cost. Visteon will need to defray these costs over high volume, which necessitates ongoing new business wins. In my view, this is the key area to monitor going forward.

In addition, with EV launches still presenting problems new to the industry, Visteon is likely to experience unforeseen cost headwinds in this area. Containing these will be critical to cost management.

On the upside however, the exciting developments in VC's product suite may accelerate new business wins as OEMs recognise the value of offerings such as SmartCore .

In addition, assuming interest rates start to level off or even fall, OEMs may respond by ramping production to meet increasing demand. The speed of rate cuts however is a hot topic that is dividing Wall St .

There are no material credit risks of note. VC is sitting around the industry standard for Debt/Equity Ratio and Interest Coverage (FactorRank Analysis based on company and peer data).

Conclusion

After exploring this investment opportunity, I rate Visteon a BUY.

They offer investors a pure-play exposure to the growing trend of automobile digitalization. Their recent selloff has overshot fair value, presenting compelling valuation upside.

The investment is not without risk however, and the size and cadence of their forward new business wins is, I believe, going to be one of their critical success factors going forward and a key area to monitor.

For further details see:

Visteon: Compelling Entry Point To A Long-Term Growth Story