KO - Vita Coco: Moats And Tailwinds To Drive A Secular Growth Story

2023-04-10 09:05:04 ET

Summary

- Vita Coco is the leading producer of coconut water.

- The company is operating since 2004 and has more than 50% of the market share in the U.S.

- Operating in an under-penetrated and fast-growing market, I expect COCO to benefit from its strong supply chain moat combined with margins recovery and innovation initiatives potential.

Investment Thesis

The Coconut water market is a fast-growing market expected to grow at a mid-double digit for the five upcoming years. This market is very concentrated and I expect The Vita Coco Company ( COCO ) to remain the top-tier actor in this industry. Despite the recent strong YTD performance (+53%), the firm has in my view still more room to perform. Indeed, it will be supported by strong tailwinds and assets such as the consumer shift toward healthier products, the decrease in freight prices, and its strong supply chain moat. I initiate coverage on COCO with a Buy rating and a target price of $26 representing a 25% potential upside.

Company Presentation

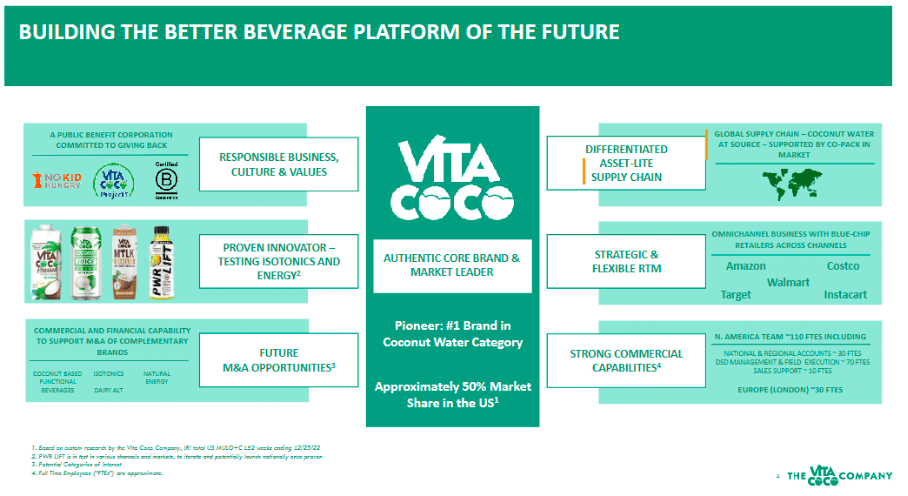

Founded in 2004 by Michael Kirban and Ira Liran two childhood friends, COCO is a leading producer and distributor of coconut water and other coconut-based products. Today, COCO is a globally recognized brand, operating in more than 30 countries and producing over 200 million liters of coconut water annually. The firm main product is its 100% natural coconut water, which is sourced from young green coconuts grown in Southeast Asia, South America, and the Caribbean. The company offers its coconut water in various sizes, from 330ml cartons to 1-liter tetra packs, as well as in flavors such as pineapple, peach and mango, and lemonade. In addition to coconut water, COCO also produces coconut milk, coconut oil, and coconut vinegar. In terms of distribution, the firm's products are sold through a wide range of channels, including grocery stores, convenience stores, health food stores, and online retailers. The company has also secured partnerships with major beverage companies such as PepsiCo ( PEP ), which distributes COCO products in certain markets.

Market Overview: Would you like some more coconut water?

According to the Daedel Research report:

The global coconut water market was valued at US$5 billion in 2021 and is expected to be worth US$11.72 billion in 2027. The global coconut water market is determined to grow at a CAGR of 15.27% over the forecasted period of 2022-2027.

Coconut water and its incredible properties are now unanimous. This product is becoming more and more popular for various reasons:

- Its refreshing taste and the possibility to use it in various cases whether to drink or to cook makes it an element of choice to have in our fridge. Furthermore, coconut water is known for being a natural and refreshing drink that offers numerous health benefits. Indeed, it is very low in calories, rich in nutrients, and can help to support hydration, digestion, skin health, and athletic performance.

- The COVID-19 pandemic caused production plants to shut down, impacting the food and beverage industry. The crisis and its consequences also led many consumers to prioritize healthy living and nutritional products, creating new opportunities for the coconut water market. The pandemic accelerated the trend towards plant-based diets, driven by concerns regarding health, sustainability, and ethical treatment of animals. As a result, the demand for functional and immunity-boosting products like coconut water has substantially increased and is expected to continue.

In my view, consumer awareness about coconut water benefits is growing. Consumption habits are evolving and coconut water is also becoming more popular amongst younger generations that are concerned about health and earth/ethics related themes. For these reasons, I identify the Coconut water market as an attractive long-term growth opportunity.

Vita Coco's positioning: The biggest nut of the tree

COCO is the leader in the Coconut water industry. Indeed, the firm has 50% of the market share within the US. This position is well deserved and is built to last. In my opinion, the firm has a clear moat in terms of supply chain. During the last decades, it has been very difficult for big companies like Pepsi and The Coca-Cola Company ( KO ) to get into the Coconut water market due to supply chain constraints.

Thus, COCO decided to build long-term exclusive supply contracts with most of the world's largest producers of coconuts. Wisely, the company is not only buying coconut water on the open market but also some other byproducts from the coconut industry such as coconut milk, and shredded coconut. The firm is buying byproduct and has exclusive rights to it. Note that the group has diversified where it buys its coconut to have a large variety of tastes and also to reduce its risk. Thus, the firm supply is coming from several countries such as Brazil, Sri Lanka, Philippines, Thailand, Malaysia.

In terms of marketing strategy, COCO is centered around promoting the health benefits of coconut water and positioning the product as a natural and healthy alternative to sports drinks and sugary beverages. This strategy is currently paying out. Indeed, the firm has gained important notoriety, especially after partnerships with several high-profile celebrities and athletes, such as Rihanna and Rafael Nadal.

{kind=link}

Vita Coco's Fertilizers: Innovation, Margins Recovery and a New CFO

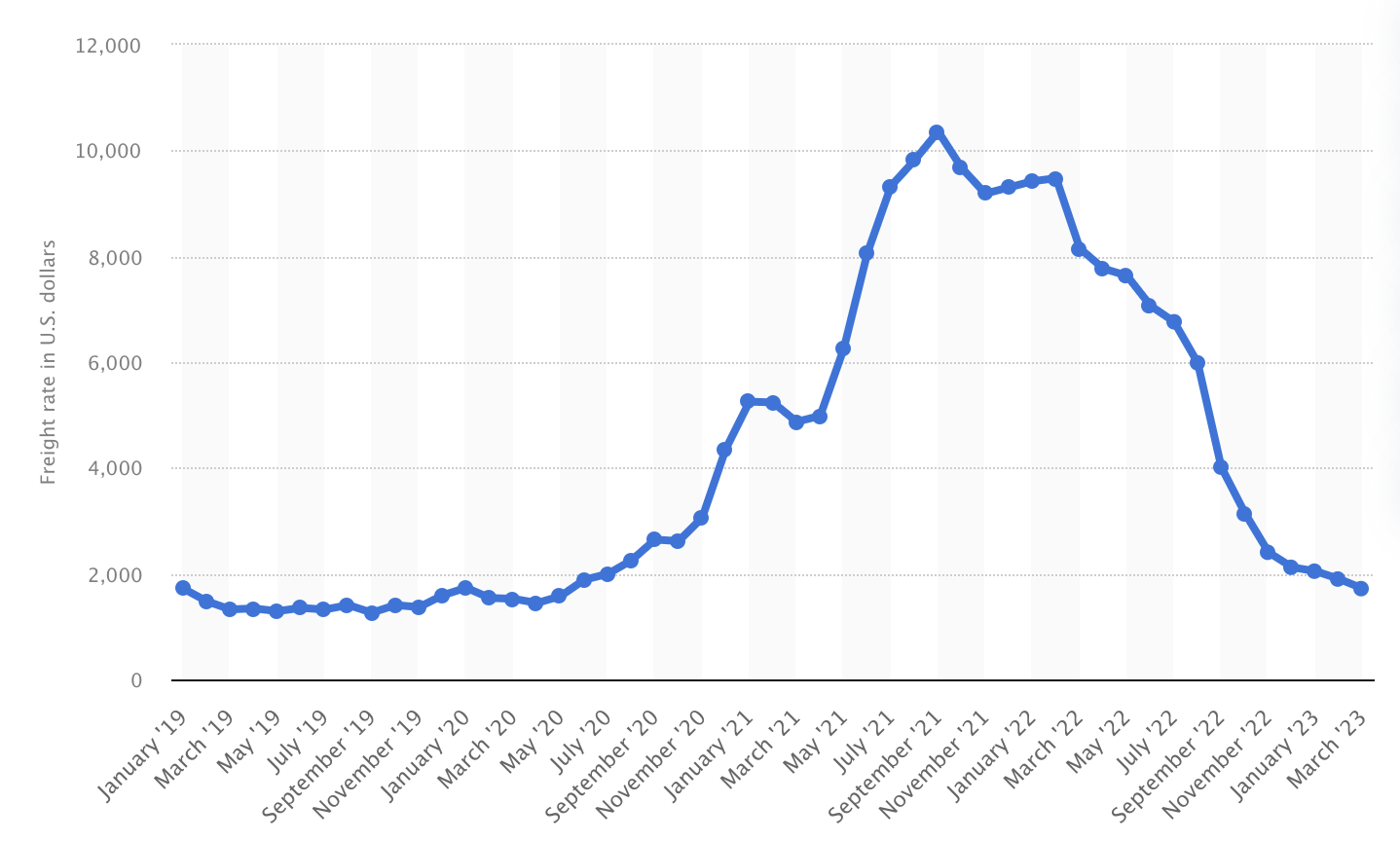

COCO's strong market positioning should be supported by other key elements for the upcoming years. In 2022, COCO margins were close to 24% when they were almost at 30% for the year 2021. Margins have mostly been impacted by the sharp rise in freight costs. Now, these costs have sharply decreased; thus, I expect the firm's margin to recover quickly.

Global container freight rate index from January 2019 to March 2023 (Statista)

{kind=link}

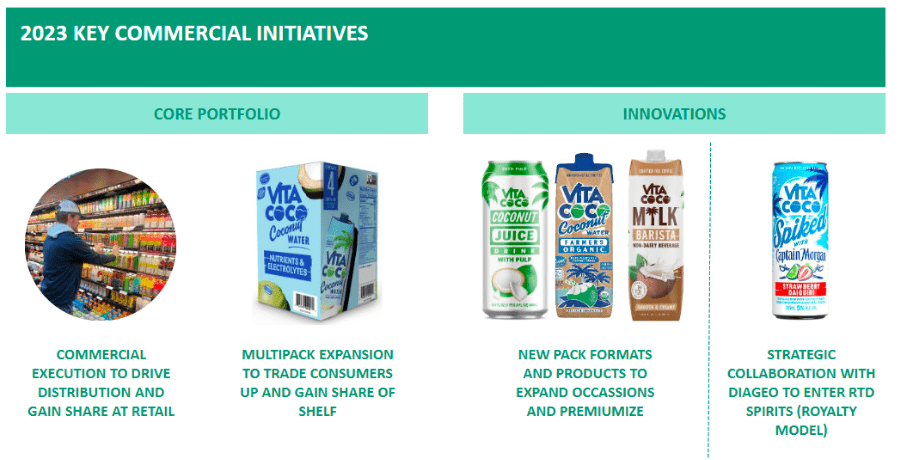

Growth and innovation-oriented, the firm should also benefit from its multi-pack expansions with new cans and packs.

{kind=link}

Finally, the firm announced recently the nomination of Corey Baker as the new CFO of COCO. Baker has strong experience and has been working for 16 years at Pepsi. This represents in my view a promising choice as he will be able to bring his experience and the knowledge, he acquired at one of the world's most known and efficient staples firms in the world.

Financials and Valuation

Many are concerned about COCO's current valuation, especially after its strong run on a YTD basis (+53%). After the such performance, you might be to be tempted to wait for a correction in order to spot a good entry point. I can completely understand such a view.

In any case, let's have a look at the firm fundamentals to see if the current valuation is that expensive and if it is understandable.

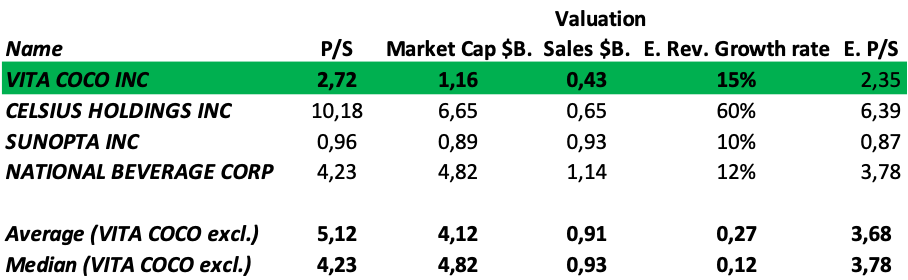

To compute my peer analysis and to make it as relevant as possible, I choose COCO small cap competitors namely Celsius Holdings ( CELH ), SunOpta ( STKL ), and National Beverage ( FIZZ ).

First, what strikes me, is the very low level of debt the firm has with a 0.03 debt/equity ratio and a 0.02 debt/assets ratio. The low debt/asset ratio is understandable as the firm works with an "asset-light model" philosophy.

This low level of debt is very compelling, especially for a fast-growing company. This should allow the firm to raise capital if it spots attractive opportunities whether in terms of organic or inorganic growth.

Regarding short-term liquidity, the firm is also in a very good position with a current ratio standing at 3.22 vs 1.89 for the peer's median.

In terms of valuation now, the firm might look expensive when looking at the P/E ratio. However, when looking at the price to sales, the firm is only trading at 1.76 times its sales versus 3.36 for the peer's average.

Finally, when looking at profitability, COCO has a lower gross margin than the peer average. However, as mentioned above, I expect margins to get closer to 30% for the year 2023 due to a decrease in the freight cost that skyrocketed in 2022. Following the same logic, I expect COCO's EBITDA Margin and Net Income margins to improve. Note that compared to its peers, the firm's bottom-line profitability stands out.

{kind=link}

Let's dive deeper into COCO's valuation. Currently, COCO trades at a 55.5% discount compared to its peers which is clearly not justified in my view given potential growth opportunities. I expect the firm topline to grow by 15% which is the coconut water sector growth rate for the upcoming 5 years according to the report mentioned above.

When looking at next year's revenues, I expect a 12% growth rate for the industry median. Such a growth rate leads us to a $0.50 billion revenue implying with the current market cap a 2.35 P/S vs a 3.68 P/S for its competitor's average.

{kind=link}

Such valuation implies a 55% discount for COCO. However, when looking at the PE, COCO trades at a slight premium of 2%.

Thus, combining these two valuation methods that I weigh equally, I reach a TP of $26 representing a 25% upside potential.

Risks

COCO might face several risks in the current environment. Here are the main ones I identify:

- Recession risks that might impact spending for COCO's products

- Tougher competition than expected

- Supply chains issues

COCO has a clear dominant position in this market. Thus, the main risks are in my opinion more macro-oriented and not specifically firm oriented.

Conclusion

I expect COCO to capitalize on its key advantages whether in terms of product quality, supply chain moat, size, marketing strategy. The firm is supported by strong headwinds and the coconut water market growth is very compelling as it is fast-growing and underpenetrated. In my view, COCO is an actor of high quality that will lead this market in the upcoming years. Another element to consider is the possibility for major actors to buy COCO which also reinforces my bullish thesis. For all these reasons, I initiate on COCO with a Buy rating and a TP of $26 representing a 25% upside.

For further details see:

Vita Coco: Moats And Tailwinds To Drive A Secular Growth Story