LYV - Vivid Seats Stock: Undervalued And Ready To Rally Higher

Summary

- Vivid Seats is benefiting from strong demand for live event tickets.

- The company reported Q2 earnings which beat expectations.

- We like the stock following its recent selloff as shares appear undervalued while supported by overall solid fundamentals.

Vivid Seats Inc ( SEAT ) is a leading online events ticket reseller and marketplace platform that became publicly traded in 2021 following a reverse SPAC merger . The company is profitable with solid growth this year benefiting from pent-up entertainment demand amid easing Covid restrictions. On the other hand, the stock hasn't been immune to the broader market selloff with shares down more than 40% from its post-debut high.

Still, we like SEAT at the current level which appears undervalued next to its industry competitor and well-positioned to rebound higher. This is an industry supported by several tailwinds and a positive long-term outlook. Vivid Seats is well positioned to consolidate market share and capture several new growth opportunities.

SEAT Earnings Recap

The company recently reported its Q2 earnings with a net income of $24 million or EPS of $0.12, which was $0.06 ahead of market estimates. Revenue of $148 million, up 28% year-over-year, is in the context of deeper pandemic disruptions during the period last year. Adjusted EBITDA of $30.3 million was down 16% y/y, but favorably up 44% sequentially from Q1. The result this quarter reflects a ramp-up in marketing and an expansion in headcount to support higher growth.

{kind=link}

A key operating metric is the marketplace gross order value (GOV) which reached $815 million, up 18% y/y, and a Q2 record for the company. Management notes a strong performance across all event categories like concerts, sports, and theaters. Vivid Seats also partners with third-party companies including Groupon Inc ( GRPN ), American Airlines ( AAL ), and Caesars Entertainment Inc ( CZR ) among others for distribution which added to the momentum.

{kind=link}

Another important update is the company's progress in integrating its new fantasy sports platform "Vivid Picks", rebranding from "Betcha". The idea here is to generate some synergies among consumers buying and selling tickets to sporting events with an extra form of engagement. While the initiative is still a small part of the business, the expectation is for the segment to contribute positively going forward.

A strong part of the company's investment profile is the solid balance sheet. Vivid Seats ended the quarter with $288 million in cash and equivalents against $266 million in long-term debt. Liquidity is supported by positive underlying operating cash flows. In May, the company announced a small $40 million stock buyback authorization, although no shares were repurchased in Q2.

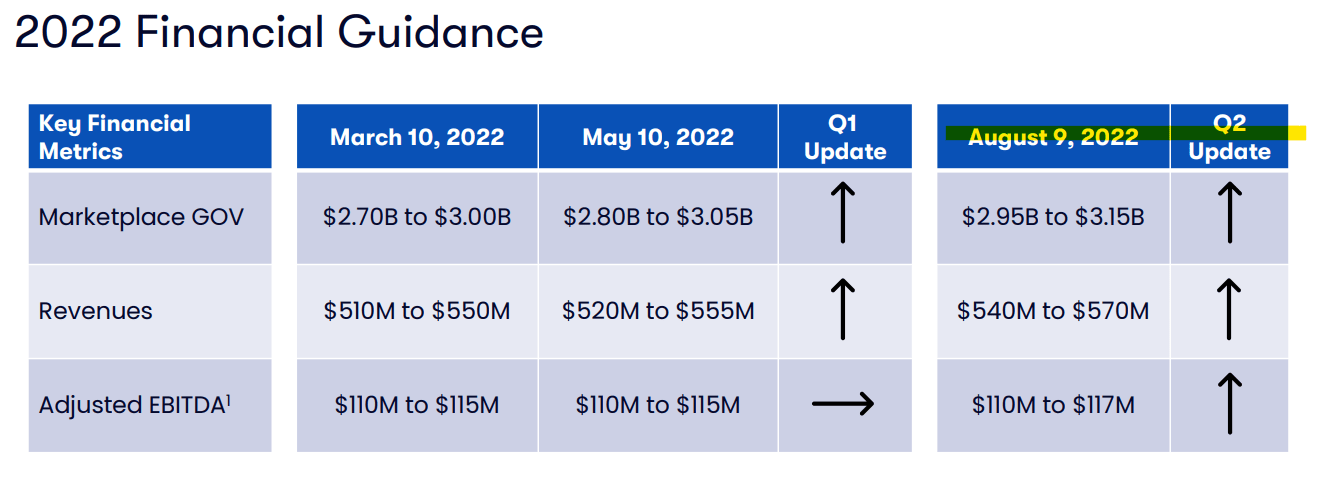

In terms of guidance, management has hiked its full-year 2022 revenue, GOV, and adjusted EBITDA targets for the second consecutive quarter. A forecast for revenue between $540 and $570 million, at the midpoint, represents an increase of 25% from 2021. The adjusted EBITDA estimated at around $114 million, if confirmed, would be above the $110 million result last year.

{kind=link}

Is SEAT a Good Investment

There's a lot to like about Vivid Seats which has an established business in a growing segment. The evidence this year is that events like concerts and shows are in high demand with its core demographic valuing "experiences". The idea of trading tickets is not new, but there is still room for more consumers getting both familiar and comfortable with the concept of a secondary marketplace highlights the long-term runway. The ecosystem supports both pricing transparency while adding convenience.

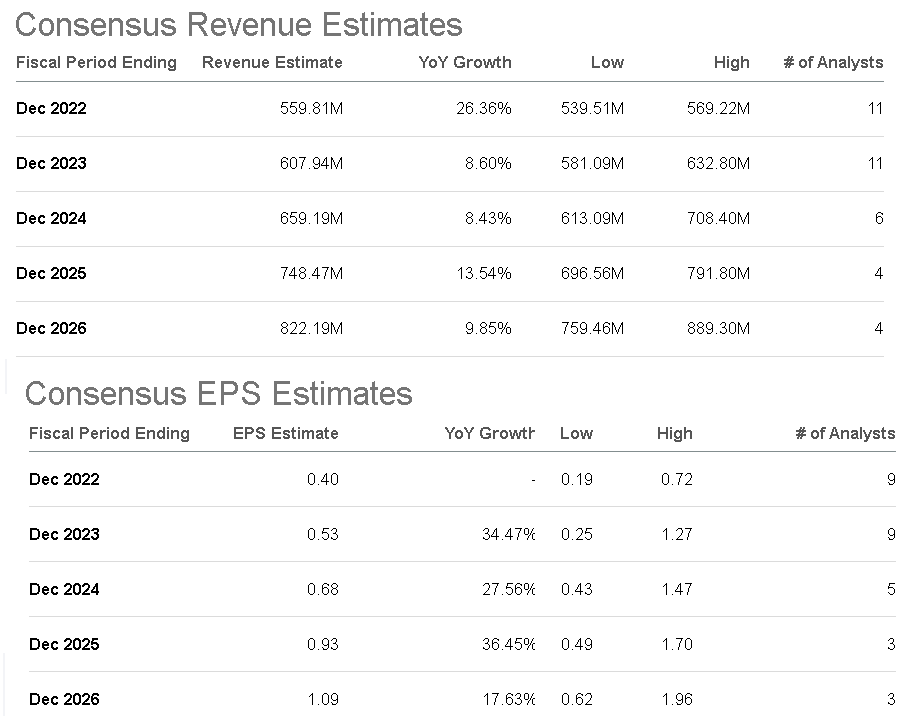

We like the valuation of SEAT which is currently trading at about 20x forward P/E multiple on the consensus 2022 EPS of $0.40. This level is particularly attractive considering the outlook for sales to climb 26% this year and average 10% growth per year between 2023 and 2026. The forecast for earnings growth is even stronger at nearly 30% annually over the period with an expectation that margins scale higher.

{kind=link}

In terms of comparables, Live Nation Entertainment Inc ( LYV ) is the industry leader through its "Ticketmaster" platform as a direct alternative to Vivid Seats although the company has a more diversified business including the direct promotion of concerts. We can also bring up privately-held " Seat Geek " and "Stub Hub" which are both in the planning stages for an IPO. In this case, SEAT trades at a large discount to LYV given its higher current profitability. In terms of the EV to forward EBITDA ratio, SEAT at 13.4x compares to Live Nation's 16.2x. We see room for this spread to converge higher as part of the bullish thesis for the stock.

While it's a contested industry Vivid Seats is recognized as offering a differentiated buying experience including through a unique rewards program . Customers gain rewards for each purchase that can be applied to future discounts and even free tickets in the future. Management believes the successful program has added to brand loyalty and supports its long-term outlook.

{kind=link}

SEAT Stock Price Forecast

As mentioned, shares of SEAT have been under pressure all year, although notably making a series of higher lows since early May. In this case, it's encouraging that Q2 earnings not only beat expectations but management also projected an optimistic outlook. In our view, the company is fine with shares simply up against poor market sentiment and concerns of slowing economic conditions. The bullish case here is that economic conditions rebound stronger and faster than expected which should provide a runway for Vivid Seats to generate higher growth.

We rate SEAT as a buy with an initial price target of $11.00 representing a 17.5x EV multiple on the 2022 consensus EBITDA guidance. Updates from the company regarding its Vivid Picks rollout can add some incremental growth and help results exceed expectations.

In terms of risks, naturally, a scenario where unemployment surges and consumer spending dries up would hit the stock through lower demand for event tickets. Weaker than expected earnings could also open the door for another leg lower in the stock. We're a bit more optimistic about the macro-outlook and expect the overall positive fundamentals to support the stock and limit the downside. Monitoring points through 2023 include GOV trends and the adjusted EBITDA margin.

{kind=link}

For further details see:

Vivid Seats Stock: Undervalued And Ready To Rally Higher