SHEL - Volta: Bad Story Ends

Summary

- Volta accepts an offer from Shell for $0.86 per share in cash.

- The EV charging station network was running out of cash while burning over $65 million per quarter.

- The stock is a sell with Volta trading at the acquisition price and no likely bidding war to take place.

In a horrible ending for investors stuck in Volta (VLTA) since the SPAC deal closed, the EV charging station company accepted a minimal buyout price. Considering the ongoing operating losses, a deal with Shell USA Inc. (SHEL) was probably the best possible outcome at this point. My investment rating is now a Sell, with the stock trading at the deal price in a sharp warning to investors in other EV charging station stocks.

Source: FinViz

Down Over 90%

Volta went public back in August 2021 in a SPAC deal with Tortoise Corp II. The company just accepted a deal to be acquired by Shell for ~$169 million at a price of $0.86/share in cash .

The stock hit a low of $0.30 at the end of 2022 on tax loss selling, so shareholders probably lucked out a large energy company wanted to own a charging station operator. The move is odd in that these charging station companies don't generate much in the way of gross margins questioning why Shell doesn't just buy from the market.

Amazingly, Volta traded up to $15 prior to closing the SPAC deal. The market fell into the EV charging station hype due to the shift towards clean energy, but the sector remains on the bleeding edge failing to generate much in the way of gross margins while wilding spending on sales and marketing expenses.

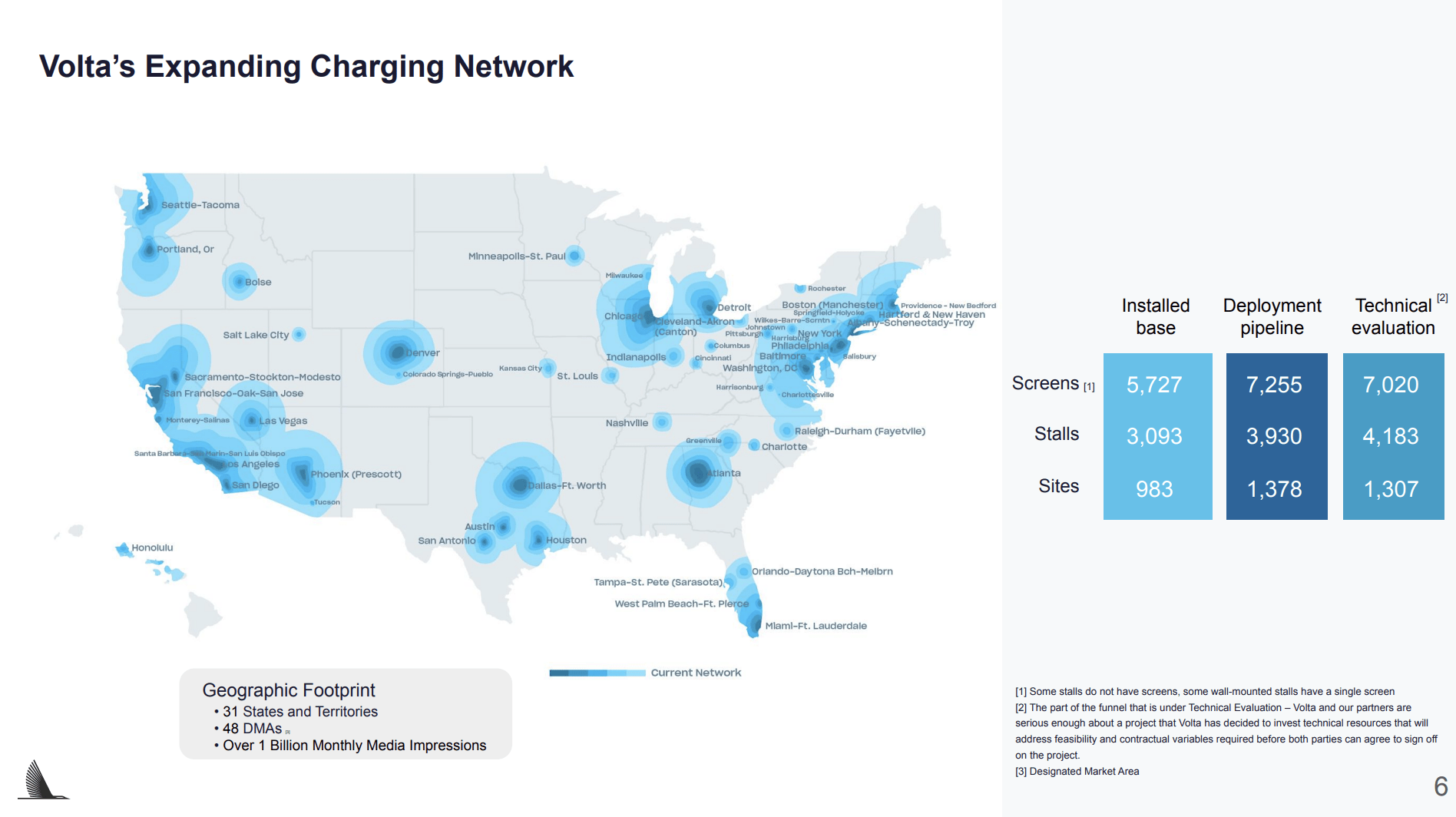

The energy giant possibly sees some potential in the media model where Volta has failed in the last year since going public. The company recently reported Q3'22 results where revenues were only $14.4 million for a business with a network of 5,700 screens delivering charging solutions to EV owners and one billion monthly impressions to the advertisers.

The problem is that Volta actually had higher gross margins with cost of sales only in the $8.8 million range. The issue is that the charging station company is spending over $40 million quarterly on SG&A costs.

No company can survive very long with revenue growth having stalled and operating expenses are vastly higher than the revenues. In fact, Volta technically makes no money when factoring in depreciation and interest expenses before even approaching the large SG&A costs to presumably build out the charging station network and make sales deals for the media network.

Everyone understands the need to invest in order to build the network. The issue is matching revenues with the spending level. Any company has to have a reasonable path to reaching cash flow positive and Volta failed on this metric in part to revenues not materializing as projected.

No Cash

Investors should learn from the Volta story with other SPACs regarding cash balances and burn rates. The company reported a Q3'22 adjusted EBITDA loss of $30.9 million, up from $22.1 million last year. The charging station network company has an EBITDA loss of $105.7 million for the YTD period.

The problem is that Volta only generated Q3'22 revenues of $14.4 million and the analysts predict the company generating just $18.2 million in the strong media quarter of Q4. Volta doesn't have cash and the company still has to pay for the charging stations in order to install new ones requiring a massive amount of cash to fund network development and operating losses.

The company ended September with a cash balance of just $15.6 million with debt levels already at $28 million. The problem is that cash burn has averaged over $65 million per quarter in 2022 due to the $119.6 million loss from operations this year through September and another $80.2 million loss on the purchase of equipment without even mentioning software and technology patent costs of $5.4 million.

At this level of spending, Volta needed to raise magnitudes of more cash when the selling price was $10 per share. The company would need another $500 million to cover similar cash burn rates for the next 2 years alone.

At one point, Volta could've potentially benefitted from this large development pipeline. The company had a network of over 14,000 screens in development to push the total network to nearly 20,000 screens providing the network potentially more attractive to media customers.

Source: Volta Q3'22 presentation

{kind=link}

A big lesson here is that former SPACs are especially vulnerable to these scenarios where a promising business model will fail due to a lack of capital. One of the major weaknesses of the SPAC process was the unknown cash raise due to redemptions on the approval of the deal.

Takeaway

The key investor takeaway is that Volta shareholders should take the deal from Shell and run. An investor should cash out of the stock and use the proceeds for a financially stable company beaten down by the market over the last couple of years. Don't roll the money into another EV charging station company burning cash, trying to build out a network, or sell charging stations at no margin.

For further details see:

Volta: Bad Story Ends