COST - Voss Capital - Alta Equipment Group: Continuing Their Steady 'Beat And Raise' Cadence

2023-03-08 01:00:00 ET

Summary

- One investment idea that has grown to nearly 5% of the portfolio is Alta Equipment Group.

- We believe a proven core competency of Alta's is making accretive acquisitions, especially in times of economic uncertainty.

- One misperception in the marketplace is the belief that Alta relies on cyclical residential or commercial real estate development.

- We view Alta as a great business with favorable macro exposures to e-commerce and large infrastructure projects.

The following segment was excerpted from this fund letter .

Alta Equipment Group ( ALTG )

One investment idea that has grown to nearly 5% of the portfolio is Alta Equipment Group. Alta is a heavy equipment dealership and rental business, that sells, rents, and services forklifts and heavy construction equipment. The company has 65 full-service locations across 11 states, with a concentration in Michigan, Illinois, New York, and Florida, along with locations in Quebec and Ontario, Canada. Alta's business model revolves around selling new and used equipment at relatively low gross margins (16% on New Equipment Sales and 27% on Rental Fleet Sales in the most recent quarter) to maximize the amount of equipment in the field. Having an active fleet provides Alta with a long, multi-year tail of higher margin Parts & Services revenue (35% gross margins on Parts and 55% on Services). 7

Alta typically receives exclusive geographic coverage on both equipment and replacement parts from their top OEM (original equipment manufacturer) partners, such as Hyster-Yale (the leading forklift manufacturer) and Volvo ( VOLAF - heavy construction equipment). This creates barriers to entry for competitors in what could be described as a regional monopoly for brand sales granted by Alta's OEM partners. Alta holds about 15% market share of all HysterYale sales in North America, and in their home state of Michigan, where they've operated for a much longer time, they have maintained over 35% of the forklift market share for 15+ years.

Alta started as a family-operated business with a single forklift dealership in Detroit, but current CEO Ryan Greenawalt had grander ambitions. In 2017, Greenawalt raised capital from Goldman Sachs ( GS ) to recapitalize the business, buy out his family members, and enact an aggressive growth plan. We believe a proven core competency of Alta's is making accretive acquisitions, especially in times of economic uncertainty. In 2009, in a strategy led by the current CEO, Alta aggressively played offense when competitors were reeling, acquiring and successfully integrating four companies in a 60-day period. They invested heavily into the Covid downturn as well and have acquired an additional 12 companies since coming public in early 2020. As far as we know, they have not paid over 5x EBITDA for an acquisition, with the multiples much lower on a pro forma basis as some of these companies have grown by over 100% since their acquisition.

In a trend that we think greatly benefits Alta, both of their two largest OEMs (Hyster-Yale and Volvo), that combined account for ~35% of revenue, have made concerted efforts to consolidate their dealer networks into the hands of fewer, stronger dealers such as Alta. Hyster-Yale has gone from over 60 dealer ownership groups nationally to less than 30, even as the number of dealer rooftops overall has grown. Additionally, Hyster-Yale has consent rights on who an existing dealer can sell themselves to, which has also benefited Alta since they have established themselves as a credible buyer and successful integrator and operator. Alta plans to continue their acquisition strategy of buying dealerships with exclusive rights to certain brands over large territories. Consensus estimates do not typically contemplate any additional EBITDA contribution from future M&A, despite this being a clear part of the business plan, thus potentially positioning Alta to continue their steady "beat and raise" cadence. Plenty of organic growth opportunities remain as well. For example, a dealership we recently visited in Tampa was expanding from 6 service bays to 14 by using excess space in the parking lot that had been sitting empty but will now significantly enhance P&S throughput.

An additional important element of the company's success and our investment thesis is Alta's ability to recruit and retain skilled technicians to grow their dealers' higher margin Parts & Services revenue after they've consolidated it. Given its national presence, Alta employs full-time recruiters in addition to the mechanic and technician recruitment they have built into their branch managers' incentive structures. Each local branch manager's bonus is partially based on their ability to develop relationships with local vocational schools and community colleges, go to job fairs, etc., and recruit new employees. Alta's employee turnover is 67% less than that of other auto dealerships (10% vs 30-35% for the auto dealers), evidencing the success of their impressive culture. 8

On the Material Handling side, Alta has a ~30% attachment rate on a guaranteed maintenance program that consists of 3-5 year contracts. Another 45% of customers sign up for a preventative maintenance program with month-tomonth contracts, providing further stability and predictability to their P&S profits.

On the Construction side, Alta is the best performing Volvo dealer in the country. Their partnership with Volvo began in Michigan at a time when Caterpillar ( CAT ) had 60% market share, and they helped Volvo take half that share in their first six years as a dealer. This put Alta on Volvo's map, and Volvo has subsequently favored them to take over more dealers to help the brand grow. Volvo equipment has a standard 3-year warranty, and while the gross margins on the warranty work are lower for Alta, the service needs tend to move a step function higher after a piece of equipment has been in the field for three years.

One misperception in the marketplace is the belief that Alta relies on cyclical residential or commercial real estate development. While the largest forklift buyers in the country 20 years ago were GM and Ford ( F ), now they are WalMart ( WMT ), Costco ( COST ), and Amazon ( AMZN ). Alta is benefiting from the secular growth of e-commerce and warehousing needs, onshoring/reshoring of light manufacturing in North America, as well as large multi-year infrastructure projects. For example, the largest customers in their top Construction geography of Florida include landfills and recycling centers, phosphate miners, and commercial excavation contractors that are working on multi-billion-dollar, multiyear water management projects that are government funded and will continue regardless of the overall macroeconomic environment.

What really got us over the goal line, so to speak, with an investment in Alta was the company's operating performance in the face of the Covid lockdowns and resulting recession. Their organic revenue and EBITDA declined by only 3% sequentially in worst of the decline as the management team was proactive and able to rapidly manage costs. The downturn also confirmed the resilience of the Parts & Services revenue stream, which grew organically in Q2 2020 and provided a growth engine driven by the steadily increasing the field population of equipment Alta serves.

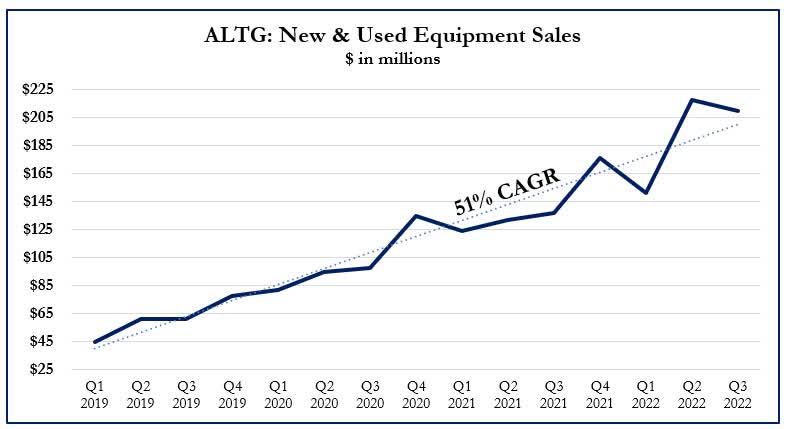

Alta's sales of new and used equipment, a leading indicator for higher margin P&S revenue, have remained impressive to us and have done a 51% CAGR over the last ~4 years.

{kind=link}

As a rule of thumb, they have done an ~ 1:1 ratio of parts and service revenue to equipment sales revenue on the Materials Handling side, and ~0.5:1 on the Construction side, with a step function higher for P&S revenue in the third year a new piece of equipment is in the field. We like this visibility of the annuity-like nature of P&S that their current equipment sales provide. By our estimation, Alta's equipment sales of $2B+ just since 2019 should generate an incremental $500M+ of gross profit over the next 3-4 years (ignoring any equipment sold before 2019). While we expect some moderation of the growth rate and gross margins on equipment sales as supply chains normalize, we believe the higher margin P&S revenue growth can continue its high CAGR (~40% since 2019) and more than offset any slowdown in new equipment revenue. Additionally, as the P&S mix increases, overall EBITDA margins can continue to rise.

Overall, we view Alta as a great business with favorable macro exposures to e-commerce and large infrastructure projects, along with a high-quality management team that is executing well on their growth plans and opportunistically capitalizing on accretive M&A. Given the high rate of equipment sales in the last few years, we expect P&S revenue to continue compounding at a high rate even in a weak economic environment.

Based on our calculations, Alta's stock has 40% upside to 7.5x 2023 EBITDA, a more reasonable multiple that would still put it at a discount to its equipment dealership and rental peers. Another way to evaluate the cash flow generation of the business is to consider the FCF yield before M&A and discretionary growth investments into the rental fleet, and on this basis, even after the stock has run-up since last summer, Alta is at an 11.5% FCF yield.

Disclosures and Notices:Beginning January 1, 2020, all investment activity is conducted by the Voss Value Master Fund, LP (the "Master Fund"), which has two feeder funds, and therefore performance figures from January 1, 2020 onward are calculated based on the Master Fund. All limited partners invest in the Fund through one or more of the following feeder funds: Voss Value Offshore Fund, Ltd. (the "Offshore Fund") and Voss Value Fund, LP (the "Predecessor Fund"), each a "Feeder Fund". Performance figures for the Predecessor Fund are contributable to Travis Cocke as sole portfolio manager. Mr. Cocke maintains the same the position with the Fund and the Fund will employ a similar strategy as the Predecessor Fund. Actual returns are specific to each investor investing through a Feeder Fund. Each Feeder Fund was established at different times and has varying subsets of investors who may have had different fee structures than those currently being offered. As a result of differing fee structures, differing tax impact on onshore and offshore investors, the timing of subscriptions and redemptions, and other factors, the actual performance experienced by an investor may differ materially from the performance reported above. Portfolio statistics shown are inclusive of the Predecessor Fund and the Offshore Fund. This letter is provided by Voss Capital, LLC ("Voss", "the Firm", "the Voss Team", and "our team") for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in the Voss Value Fund, LP (the "Fund") or any other security. An investment in the Fund is speculative and involves substantial risks. Additional information regarding the Fund, including fees, expenses and risks of investment, is contained in the offering memorandum and related documents, and should be carefully reviewed. An offer or solicitation of an investment in the Fund will only be made pursuant to an offering memorandum. This communication is confidential and may not be reproduced or distributed without prior written permission from Voss. This confidential report is only intended for the recipient and may not be redistributed without the prior written consent of Voss. The information contained herein reflects the opinions and projections of Voss as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. Data included in this letter comes from company filings and presentations, analyst reports and Voss' estimates. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. Certain information contained in this letter constitutes "forward-looking statements" which can be identified by the use of forward-looking terminology such as "may," will," "should," "expect," "attempt," "anticipate," "project," "estimate, or "seek" or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results in the actual performance of the Fund may differ materially from those reflected or contemplated in such forward-looking statements. There can be no guarantee that the Fund will achieve its investment objectives and Voss does not represent that any opinion or projection will be realized. The securities contained within the benchmark indices highlighted herein do not necessarily correspond to investments and exposures that will be held by the Fund and are therefore of limited use in predicting future performance of the fund. Indexes are unmanaged and have no fees or expenses. An investment cannot be made directly in an index. The Fund consists of securities which vary significantly from those in the benchmark indexes listed below. Accordingly, comparing results shown to those of such indexes may be of limited use. The S&P 500 Total Return Index is a market cap weighted index of 500 widely held stocks often used as a proxy for the overall U.S. equity market. The Russell 2000 index is an index measuring the performance approximately 2,000 small-cap companies in the Russell 3000 Index. The Russell 2000 serves as a benchmark for smallcap stocks in the United States. The Russell 2000 Growth Index measures the performance of those Russell 2000 companies with higher price/book ratios and higher predicted and historical growth rates. The Russell 2000 Value Index measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000 companies with lower price-to-book ratios and lower expected and historical growth values. HRX Equity Hedge Index consist of Equity Hedge strategies which maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment processes can be employed to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation ranges of typical portfolios. The strategy utilized by Voss has a high tolerance for uncertainty. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable. Asset allocation may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss. Past performance does not guarantee future results. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Voss Capital - Alta Equipment Group: Continuing Their Steady 'Beat And Raise' Cadence