VRM - Vroom: No Change To Thesis; Avoid

2023-07-05 11:54:02 ET

Summary

- Vroom is an online used car dealer with an innovative 'door-to-door' business model.

- The company's business model is structurally flawed as it incurs thousands of dollars in transportation costs that brick-and-mortar dealers do not have.

- Despite efforts to control costs, Vroom's SG&A still far exceeds gross profits, and the company is predicted to run out of cash by the end of 2024.

- Investors should avoid stocks like Vroom altogether as the business model is flawed, but the stock may be prone to short squeezes.

Back in September, I wrote a scathing review of Vroom, Inc. ( VRM ), noting that the company had a fundamentally flawed business model with lower gross margins than traditional brick-and-mortar dealers. It was also spending far too much on SG&A to be profitable. At the end of my article, I warned that the company had 18-24 months of run-way to turn around the business, based on its cash burn at the time.

With the passage of time, let us revisit Vroom to see if my diagnosis on the company was correct.

Brief Company Overview

Vroom, Inc. operates an ecommerce platform for selling used vehicles. Rather than simply connecting buyers and sellers like Autotrader, Vroom handles the entire transaction with no-haggle pricing and contact-free at-home pick-ups and deliveries.

Gross Profit Normalized; But Inventories Stuck On Balance Sheet

In my prior article, I commented that VRM appeared to have used lower gross profit per unit ("GPPU") as a lever to boost growth in order to attract a high IPO valuation. Subsequent to the IPO, VRM has been trying to rein in unprofitable growth, allowing gross profit to expand to $2,206 per vehicle in 2021 and $2,545 in 2022. However, this downshift (pun intended) in growth has come at the cost of dramatically lower sales, as the number of days to sale has ballooned to 131 from 66 in 2020 (Figure 1).

{kind=link}

The level of GPPU is now normalized to roughly 2018 levels, but inventory is stuck on VRM's balance sheet for twice as long (Figure 2).

Figure 2 - VRM back to 2018 GPPU (VRM S1 Prospectus)

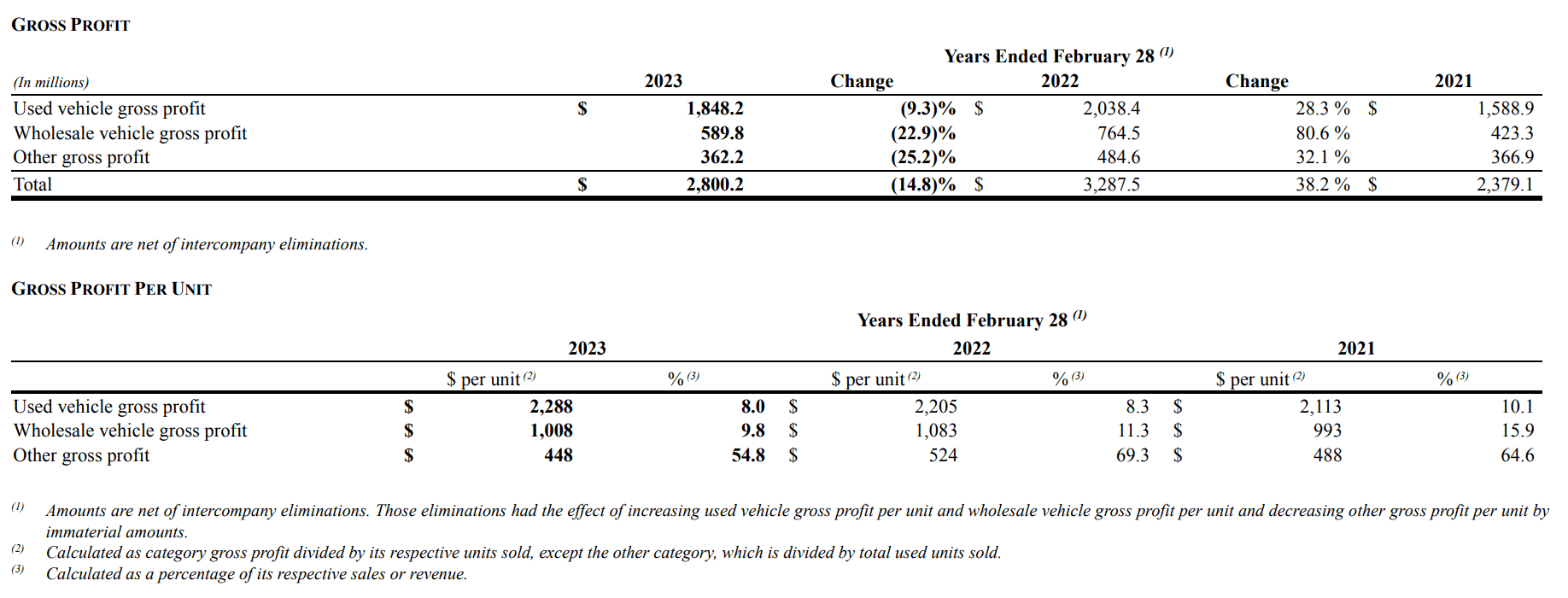

Another interesting observation on VRM's gross profit is the composition of that figure. We can see that in 2022, Vroom's average vehicle derived 2/5 of its gross profit from the actual vehicle sale, while 2/3 is derived from 'Product Gross Profit'.

This is dramatically different from how other retailers like CarMax ( KMX ) calculate and present their gross profit per unit, which is simply sale price less purchase price (Figure 3).

Figure 3 - KMX reports only vehicle price in gross profit (KMX 2022 10-K)

{kind=link}

So apples-to-apples, we should be comparing VRM's 'Vehicle Gross Profit' per unit of $1,033 against KMX's ~$2,200 per unit gross profit.

To re-iterate, VRM's business model operates at a fundamentally lower gross profit per unit because it must incur 'inbound transportation costs' and 'outbound transportation costs' to ship vehicles to and from its regional hubs compared to traditional used car dealers where customers visit brick-and-mortar stores.

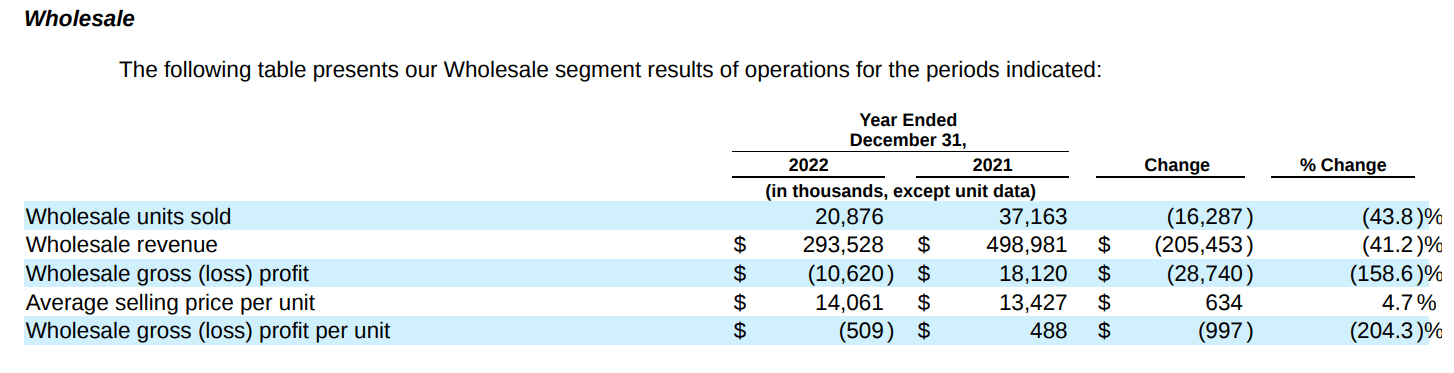

Vroom's high-cost business model also explains why its wholesale business generated 'negative' gross profits per unit in 2022 compared to ~$1,000 gross profit per unit for traditional used car dealers (Figure 4).

Figure 4 - VRM wholesale operates at negative GPPU (VRM 2022 10-K Report)

{kind=link}

Q1 Showed Worrisome Decline In Gross Profit Per Unit

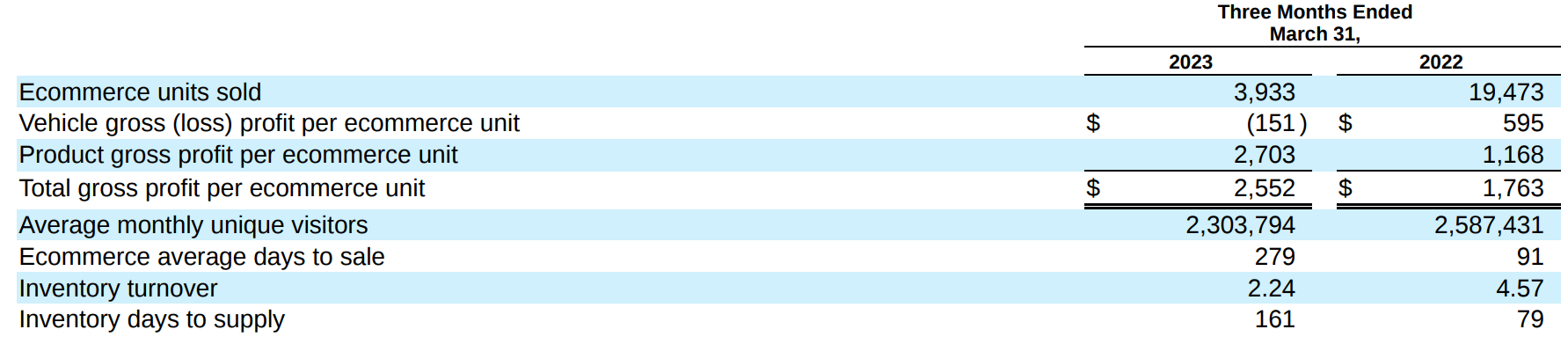

In fact, Vroom's latest reported quarter showed some worrisome developments in its gross profit figures. Although GPPU was steady at $2,552, the composition showed that Vroom was operating at -$151/unit vehicle gross profit, and made it up through an unusually high $2,703/unit product gross profit. Furthermore, inventory turnover slowed even further, with vehicles sitting in VRM's inventory for over 5 months (Figure 5).

{kind=link}

Cars Do Not Age Like Fine Wine

As many readers have no doubt encountered in their personal lives, cars depreciate the moment they leave a dealer's lot. In Vroom's case, the cars are rapidly depreciating as it sits on Vroom's balance sheet, leading to the contraction in vehicle gross profit.

In the recent Q1 conference call , management noted that 77% of Q1 sales were from 'aged inventory' and that a significant portion of upcoming Q2 sales will be from aged units "which will put significant pressure on GPPU in the second quarter" .

This shocking decline in vehicle gross profit per unit is yet another example of management not having a firm grasp of the fundamentals of operating a used car business.

Management Reining In Costs; But Not Enough To Matter

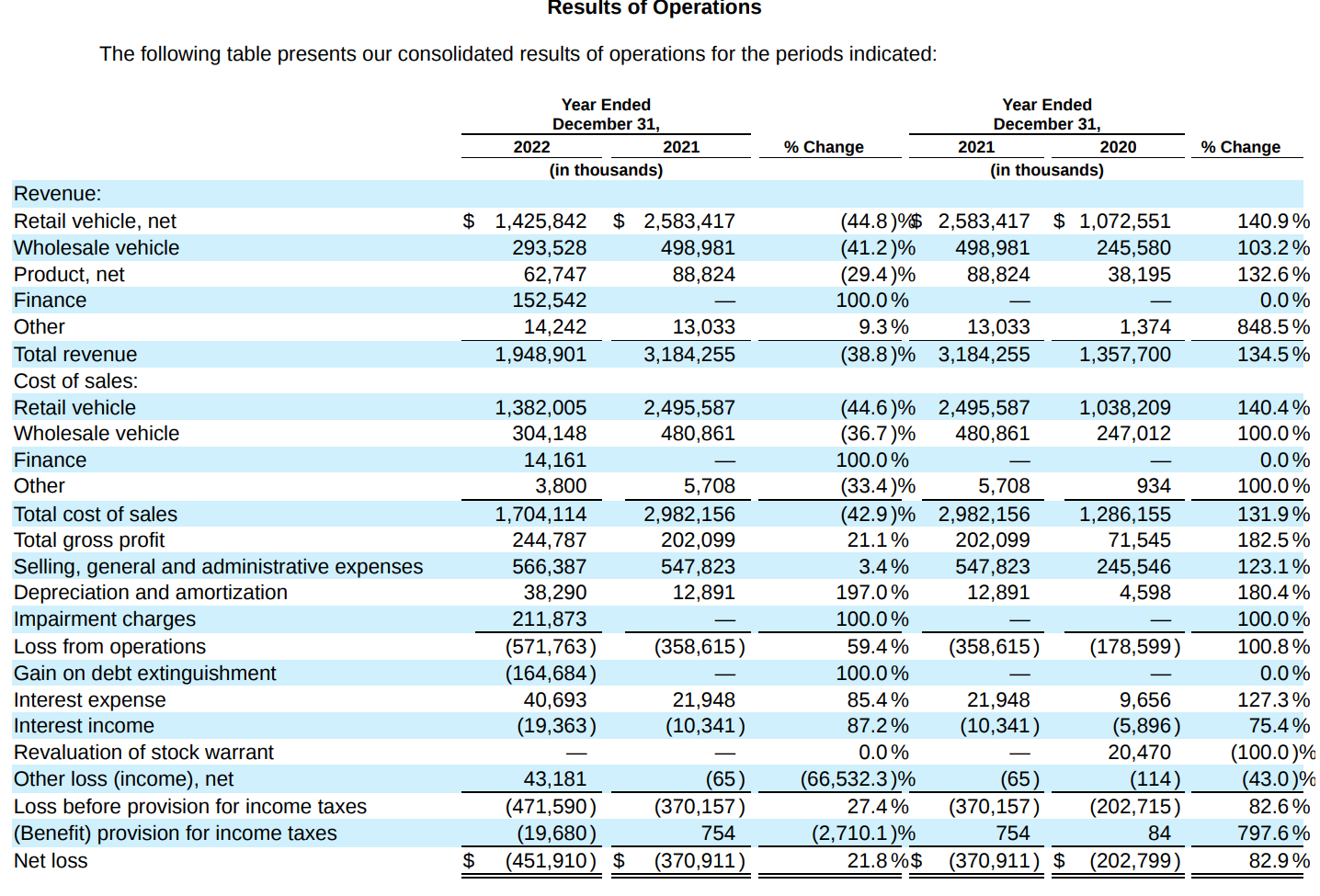

My other main criticism of VRM's business is its ridiculous levels of SG&A compared to gross profits. In 2021, VRM spent an eye-watering $548 million in SG&A compared to only $202 million in gross profit (Figure 6). This figure was improved slightly for the full year 2022, as SG&A only grew 3.4% YoY to $566 million while gross profit grew 21% to $245 million. However, total SG&A was still more than double gross profits.

Figure 6 - VRM 2022 financial summary (VRM 2022 10-K Report)

{kind=link}

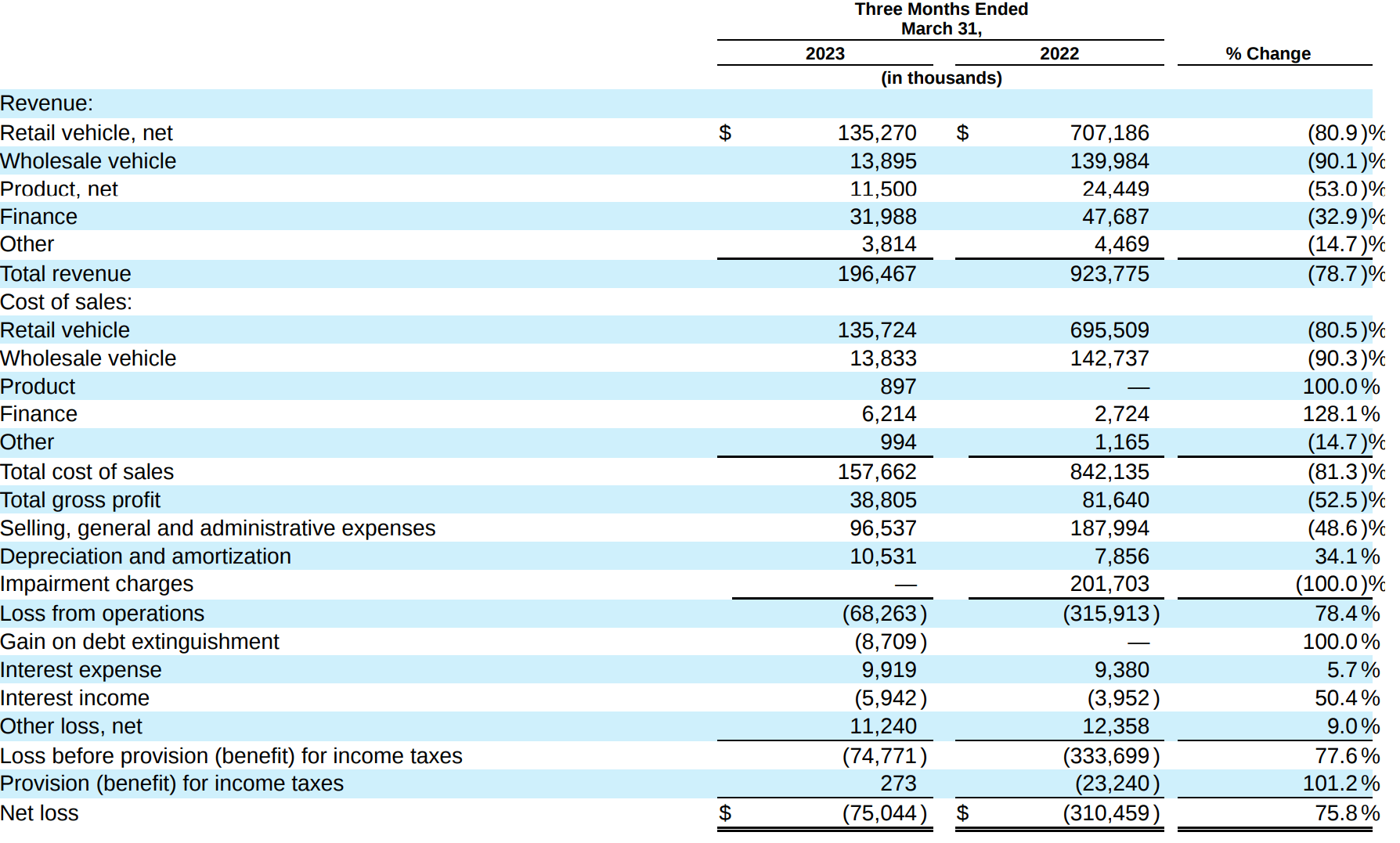

Fast-forward to Q1, it appears management's focus on cost control is finally having an impact, as SG&A declined 49% YoY to $97 million. However, there was also a dramatic decline in revenues and gross profits, so Vroom's SG&A/gross profit ratio actually worsened YoY to 2.5x, from 2.3x in Q1/22 (Figure 7).

Figure 7 - VRM Q1/23 financial summary (VRM Q1/23 10-Q Report)

{kind=link}

In my prior article, I wrote that Vroom needed to expand volumes 4 to 5 times without incurring additional SG&A in order to turn profitable and change my opinion.

Unfortunately, it appears Vroom has chosen to shrink its business, with Q1/23 revenues declining 79% YoY to only $196 million while SG&A only declined 49%. True, operating losses excluding impairment charges declined 40% YoY to $68.3 million, but I do not believe Vroom can shrink itself to prosperity unless it makes more dramatic cuts to SG&A.

Balance Sheet Deteriorates Further

One thing that shrinking the business does provide is more time. With an operating loss of $75 million in Q1/23 compared to cash and restricted cash of $389 million, I estimate Vroom has an updated 5-6 quarters of run-way before its cash runs out (i.e., end of 2024), a slight improvement compared to my prior estimate of 18-24 months of runway from September 2022 (middle of 2024).

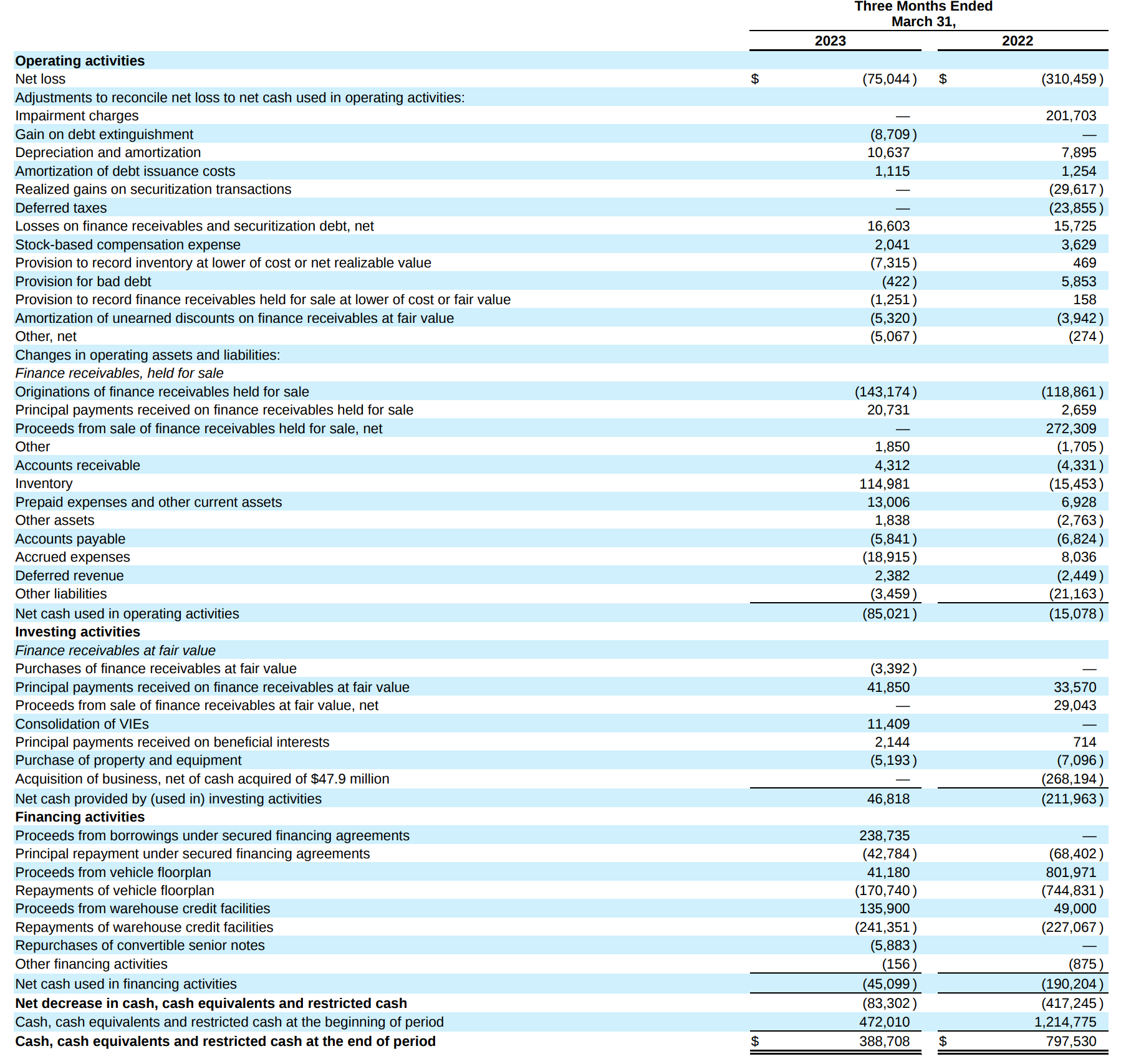

However, investors should note that on a true cash flow from operations basis, Q1/23 was actually worse than Q1/22, as stagnant inventories consumed $115 million in cash in the latest quarter and Vroom did not have the benefit from a one-time sale of finance receivables (Figure 8).

Figure 8 - VRM Q1/23 cash flow statement (VRM Q1/23 10-Q Report)

{kind=link}

Penny Stocks Are Hard To Short

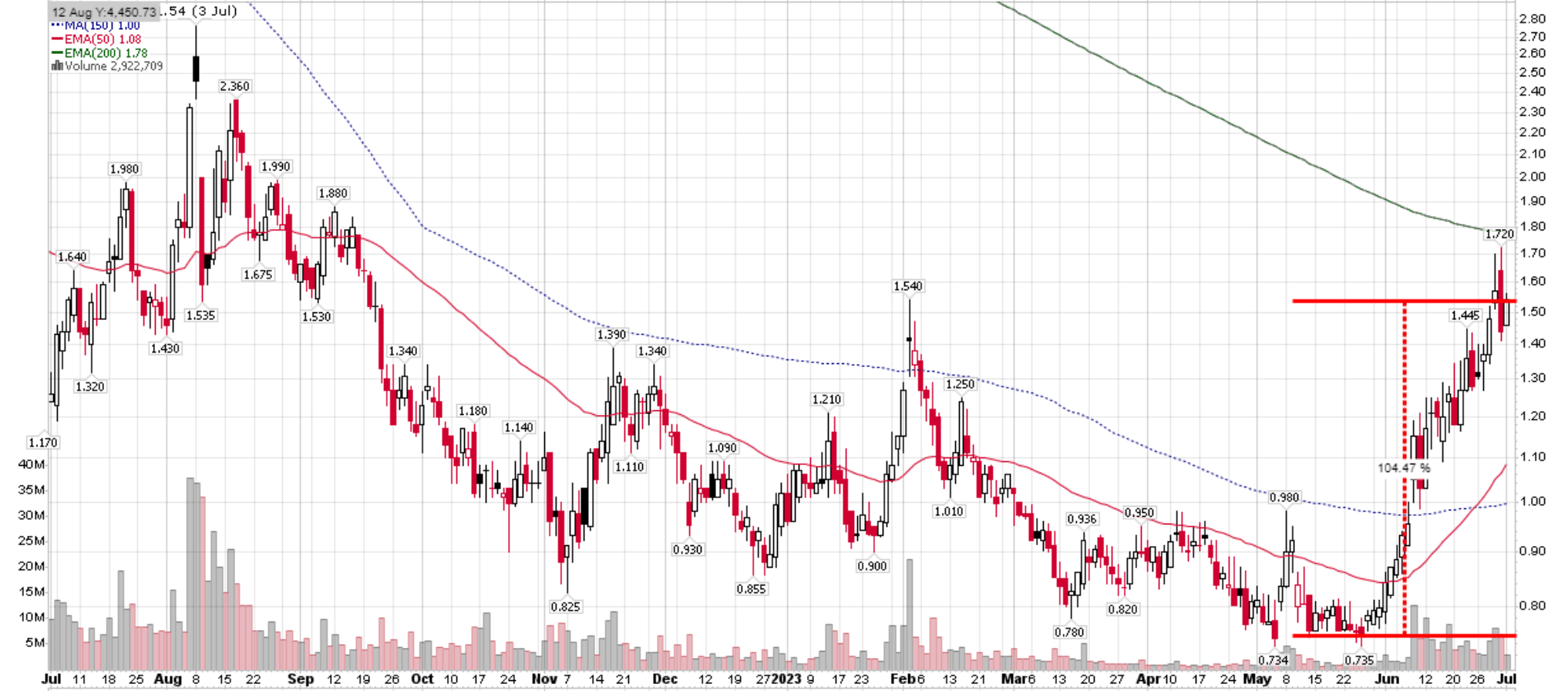

Some readers questioned why I did not recommend Vroom as a short in my prior article, given my negative view of the business. The reason was on full display recently as Vroom's shares doubled from its post Q1/23 lows of $0.74 to $1.54 in a matter of weeks (Figure 9).

Figure 9 - VRM's stock price is extremely volatile (StockCharts.com)

{kind=link}

In fact, from Figure 9, we can see VRM's stock has had many 50-70% rallies within a few short weeks, usually coinciding with general market sentiment.

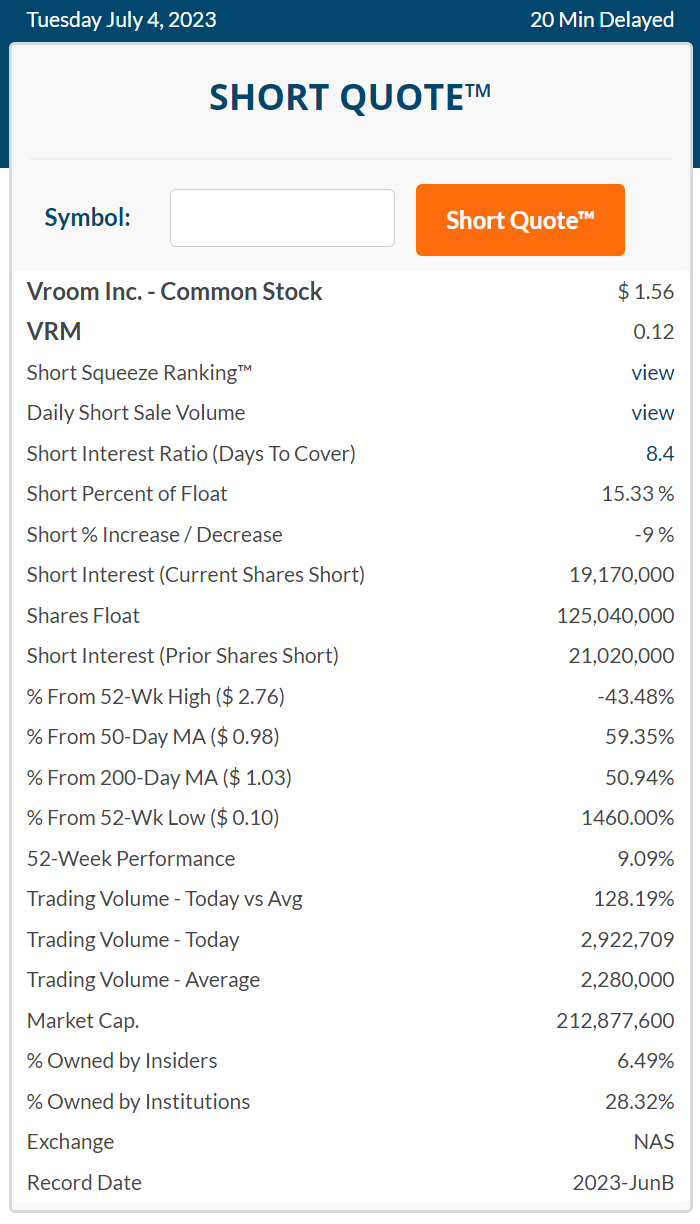

Vroom is a heavily shorted stock, with more than 15% of its float shorted (Figure 10). When short-sellers are forced to cover, perhaps because they must reduce gross exposure, heavily-shorted low-priced stocks like VRM can have outsized moves despite poor fundamentals.

{kind=link}

Investors who are late to the short thesis are better off avoiding stocks like VRM altogether rather than try to short into a face-ripping rally.

Conclusion

At this point, I believe Vroom may need a miracle to avoid bankruptcy or restructuring in the next few quarters. I simply do not see a path to profitability for the company with its bloated cost structure.

As Vroom's financials continue to demonstrate, the business model of selling used cars online with pick-up and delivery to customers' doorsteps simply does not work. Compared to traditional used car dealers, Vroom's business model starts off with a ~$1,500/unit handicap due to the high costs of transportation.

However, VRM is also a very hard stock to short due to its low stock price and high short interest. Even a slight improvement in the macro environment can cause a painful short squeeze. I recommend investors join me on the sidelines to watch this 'disruptive' company arrive at its intrinsic value of $0 in the next few quarters. I'll make popcorn.

For further details see:

Vroom: No Change To Thesis; Avoid