VRM - Vroom: Unfortunate Timing For Disruptive Growth

2023-04-24 14:22:36 ET

Summary

- Current economic downturn and shifting investor preference make it a bad time for disruptive tech companies with a hyper-growth strategy like Vroom.

- Vroom has faced significant selling pressure since last year. At ~$1 per share today, the stock trades at a very depressed level and close to the bottom.

- Achieving its FY 2023 outlook may unlock some upside. But investors should remain wary of the inherent risk in the business model.

In contrast with its hyper-growth tactics post IPO, Vroom has been laser-focused on executing its plan to improve profitability, liquidity, and unit economics (GPPU / Gross Profit per Unit) since the last few quarters. Given the declining growth and very depressed share price, it is obvious that Vroom ( VRM ) is in need of a corporate strategy reconfiguration.

In this follow-up coverage, I maintain a neutral rating for the stock. The worsen macro outlook and shifting investor preference from growth-at-all-cost to disciplined growth suggest that the timing is just unfortunate for tech companies on a hyper-growth path like Vroom to continue doing business as usual. Growth is expected to become more expensive for Vroom. Not to mention that it has been struggling to battle the key risk factors I highlighted in my initial pre-IPO coverage .

Nonetheless, as difficult as it is to project a fair target price for the stock in this unique situation, I feel that the price has bottomed and will only trend upward following the successful execution of its FY 2023 roadmap to improve business sustainability. I still believe that there is a massive market opportunity in redefining used car buying and selling experience.

However, Vroom should only be in a better position to start revisiting its growth strategy to capture a lot of that if they are to survive the next 18 months.

Business Model and Strategy Review

Vroom's e-commerce platform matches used car demand with the supply of used cars purchased by Vroom from wholesale auctions, dealers, or individual owners. When a customer buys a used car through the platform, Vroom earns revenue by charging a markup on the purchase price. Vroom also offers financing and warranty services, which generate additional revenue through interest charges and fees. The goal is to disrupt the traditional way of buying and selling used cars. The business process generally entails several steps:

- Buying the car: Vroom purchases its vehicle inventory from various sources, including trade-ins from individual owners, wholesale auctions, and directly from dealerships.

- Reconditioning: Once Vroom acquires a vehicle, it undergoes thorough inspection and reconditioning processes. This includes repairing any mechanical issues, replacing worn-out parts, and cleaning the car.

- Listing: After the reconditioning process, the car is photographed and listed for sale on Vroom's website. The listing includes detailed information about the car's features, condition, history, and transparent and market-based pricing.

- Selling: When a customer purchases a car on Vroom's website, they have the option to finance it through Vroom or use their own financing.

- Delivery: Vroom then delivers the car to the customer's door or arranges for them to pick it up at one of Vroom's local hubs.

The idea is that once the number of buyers and sellers in the platform is large enough, the business would benefit from a flywheel effect , which then becomes a competitive moat. The Flywheel effect will help the business achieve economies of scale, which in turn drives profitability. However, as is apparent in tech companies with similar business models like Uber ( UBER ) or Amazon (AMZN), it takes massive amount of patient investments to build up operational presences, processes, and user base that are large enough to generate the flywheel effect.

Indeed, Vroom has burned hundreds of millions of dollars of FCF annually since its IPO in 2020 while battling operational challenges and the economic downturn at the same time. Things started to take turn for the worse last year. Revenue growth has declined significantly since then, and the share price currently trading at a very depressed level.

Recent Financial and Long-Term Roadmap Review

Last May in Q1 2022, the management team published an 80-page long-term roadmap and financial goals suggesting that growth will take a back seat in favor of improved unit economics, profitability, and liquidity.

A big part of this new strategy is UACC / United Auto Credit Corporation, an automotive financing company Vroom completed the acquisition of last February. Having a captive financing arm helps Vroom to generate additional revenue stream and strategically support its core e-commerce sales growth. This is also an approach that its competitor, Carvana ( CVNA ), has taken.

Q4 presentation - VRM objectives

{kind=link}

The company discussed a lot of the details of its execution so far as per Q4 2022, the most recent quarter, during the earnings call. The company spent most of 2022 improving its profitability and de-emphasizing growth, though it announced the intention to resume growth in FY 2023.

{kind=link}

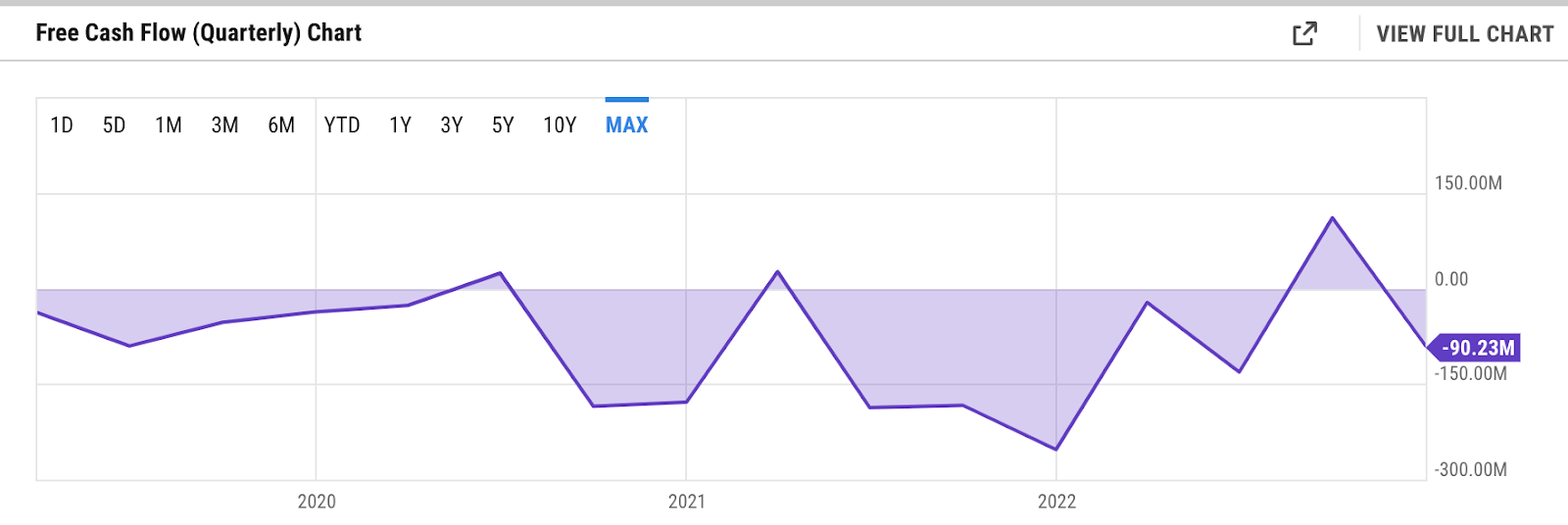

In its most recent quarter Q4 2022, Vroom reported revenue of $209.35 million, a 77.6% decline YoY. It also missed its revenue estimate by $58.86 million. However, we notice how FCF overall trended up throughout FY 2022 despite its volatility. In Q3, Vroom even had a positive FCF. Q3's FCF was $110.5 million.

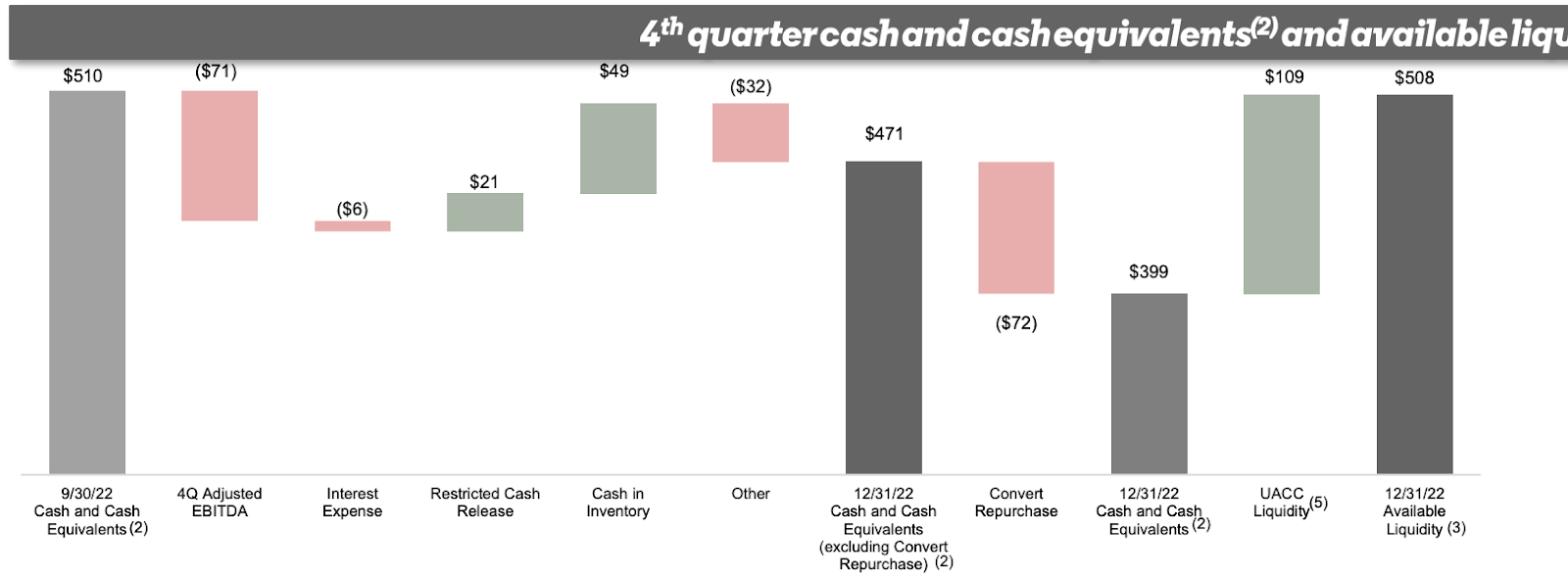

Q4 presentation - VRM liquidity

{kind=link}

As intended in the plan, Vroom also reduced its debt in 2022 by repurchasing its $198 million convertible notes for $72 million, resulting in a ~$127 million one-time gain that contributed to a positive net income of $24.76 million. The company finished FY 2022 with $399 million in cash.

Overall, I think the company has done its best to deliver an improved financial outlook as per its promise in the FY 2022 plan - to prioritize unit economics, improve costs, and maximize liquidity. There was visible progress across all fronts.

For FY 2023, the management expects to make a higher level of improvements by also resuming growth and reducing cost further on a per unit basis, in addition to continuing the FY 2022 plan.

Valuation / Pricing

Entering FY 2023, Vroom remains in a transformation mode where it is difficult to project how each of its financial items will trend, let alone future share price. To better understand where the overall business may stand at the end of FY 2023, I have come up with simple bull vs bear forward-looking scenarios that go over its three key financial pillars - growth, profitability, and liquidity.

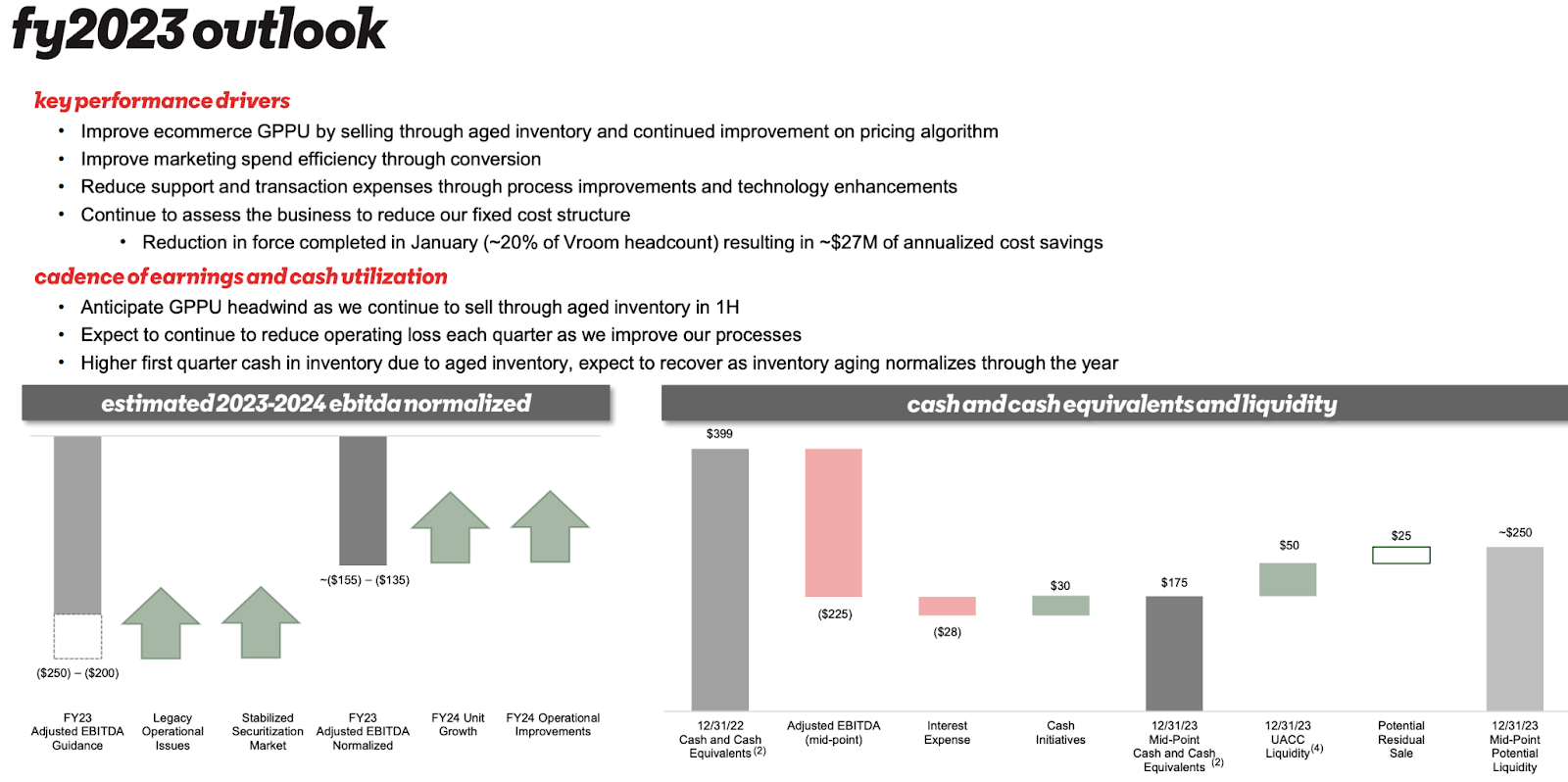

Q4 presentation VRM - FY 2023 outlook

{kind=link}

1. Bull Scenario: I expect Vroom to at least complete all of its deliverables as promised in FY 2023 outlook with no execution issues. This would be the bare minimum for most normal companies, though it would be the best possible case for Vroom.

- Growth: management suggested that growth is expected to resume in 2023. Unit volume is expected to ramp up, though neither revenue nor unit guidance was provided by the company.

- Profitability and unit economics: Vroom expects an adjusted EBITDA loss of $200 - $250 million, a $112 million midpoint improvement YoY. In FY 2022, Vroom realized an EBITDA loss of $337 million. Reduction in marketing and logistics cost per unit, two of the most significant SG&A items, is expected to continue. When it comes to GPPU, there are two parts to this outlook. In the first half of FY 2023, Vroom will still be dealing with the reduced GPPU due to selling through aged inventory with the current titles. This was a problem created by the titling and registration issues back in FY 2022. In the second half, GPPU is expected to normalize to Q2/Q3 2022 levels. I would assume that GPPU will be somewhere at the higher end of the range between +$3600 to +$4200, but not higher, considering Q3's record-high GPPU of $4206.

- Liquidity: Vroom expects to finish FY 2023 with $150 - $200 million of cash. This would take the company back to its pre-IPO level. In FY 2018 and FY 2019, Vroom finished the year with ~$162 - $217 million of cash.

2. Bear Scenario: Vroom to under-deliver on its FY 2023 outlook. In the worst-case scenario, we will even see an unexpected key C-level departure and severe operational challenges, either in the e-commerce business or in UACC.

- Growth: I assume that growth will at best be flat. Vroom continues to be in firefighting mode, deprioritizing sales ramp-up activities and revising the initial growth plan downward in the process.

- Profitability and unit economics: I expect an overall underwhelming performance across savings initiatives, especially across marketing and logistics. GPPU growth will be flat as the aged-inventory sales extend into the second half of FY 2023. Given the lack of visibility into the end of the economic downturn, UACC's default rates and delinquencies will also see a further increase, putting downward pressure on EBITDA. I expect a surprise EBITDA loss of $300 million.

- Liquidity: The $300 million EBITDA loss alone is to set end-of-year cash back to at most $100 million.

With the stock trading at a depressed level of ~$0.93 per share and the business undergoing transformation, it is also relatively difficult to assess Vroom's fair value in a more traditional way.

Vroom's negative profitability metrics mean it would be irrelevant to analyze its P/EBITDA or EV/EBITDA multiples.

The volatile revenue growth also makes any conclusion derived from the P/S analysis less reliable - the stock's ~0.066x P/S multiple makes the stock look bizarrely undervalued. Yet, it does not fully capture the overall risk picture of a business with an irregular revenue trend.

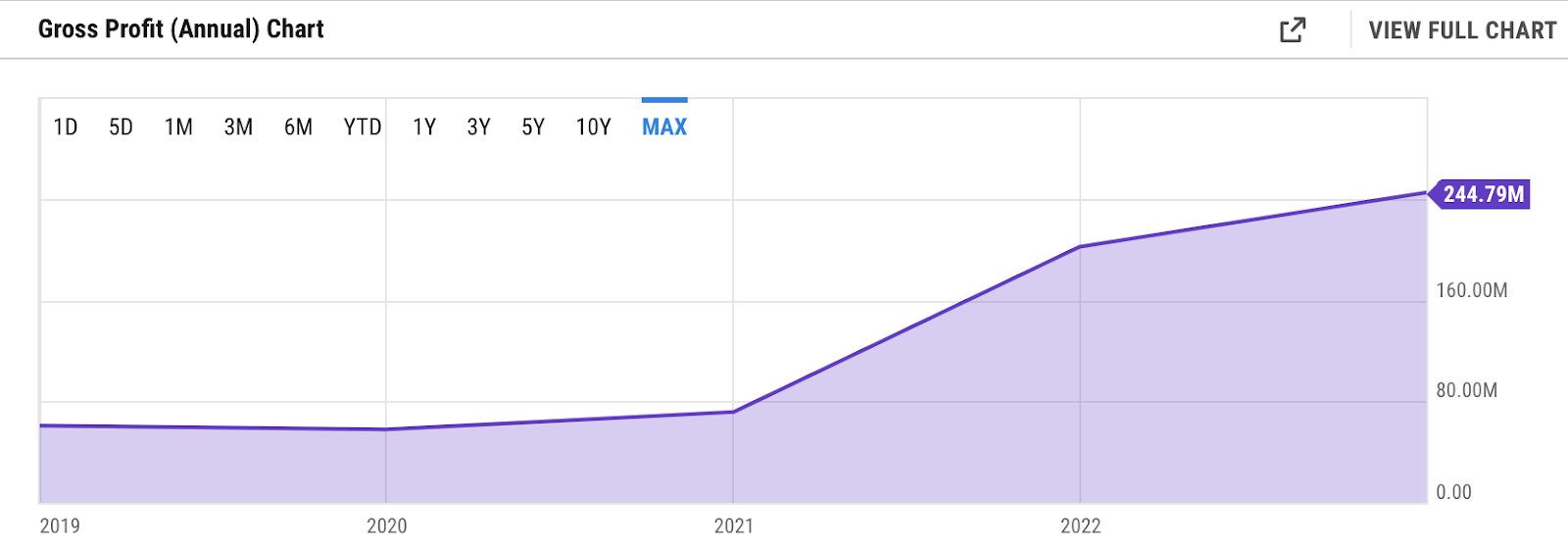

ychart - annual gross profit VRM

{kind=link}

As a workaround, I choose to analyze the stock's P/GP (Price to Gross Profit). Gross profit has been the only financial metric with a consistent upward trend over the years. The management's objective of targeting gradual improvements in GPPU in FY 2023 also means that it is a more reliable indicator of progress.

I also consider P/GP a more fair way to translate the company's current performance into the stock price. P/GP can be loosely interpreted as putting a market premium on the management's execution ability towards managing the biggest cost component in the core business, the cost of sale. Cost of sales includes vehicle acquisition, inbound transportation, reconditioning, as well as inventory valuation adjustment. Those activities are at the core of the business model. Effectively managing this cost structure will give the company a better position in eventually achieving overall profitability, the near-term goal of the company.

Taking the current market cap of ~$127 million today, I arrived at a P/GP multiple of ~0.5x. At a level approaching ~1x, the valuation looks reasonable for an under-pressure stock. Many e-commerce stocks similarly affected by the macro situation, though to a lesser extent, currently trade at higher P/S multiple than 1x, but still at low single-digit.

A year ago at the end of FY 2021 when Vroom was still experiencing high top-line growth yet a decent uptrend in gross profit, P/GP was around 7x. However, this was also a period when market confidence was already weakening toward hyper-growth business models.

Today, my view is that the share price has bottomed, and it is reasonable to expect P/GP to trade at a 1:1 ratio if the bullish scenario is to happen. I am also open to the possibility of P/GP multiple expanding to +1x if outperformance continues and brings back market confidence in the stock.

This would make the stock undervalued from a quantitative perspective, though as a caveat, it has lost its status as a growth stock for the time being. Instead, Vroom today should be evaluated as a distressed stock that merits further exploration from a more holistic point of view.

Risk

I think that e-commerce companies aiming to disrupt the automotive transaction space like Vroom and Carvana have a relatively more complex and operationally intensive business model than the other e-commerce companies. Activities such as buying, reconditioning, and delivery require the company to manage various moving parts effectively and efficiently. Those are typically where the management needs to make a decision on whether to deploy a capital or operational expense.

The next big task for Vroom is to narrow EBITDA losses gradually to demonstrate the sustainability of the business model. No matter how rosy the outlook is, there lie big operational risks in the model, where some small mistakes in the process can accumulate into sizable losses on a per-unit basis and worsen unit economics. It is possible that mistakes can happen in the next few quarters, upon which a circumstance resembling my bearish scenario may take place.

On the other hand, it is understood that Vroom's initial positioning was a hyper-growth tech company aiming to disrupt the automotive space. The strategic repositioning today means that we may be seeing a different dynamic playing out going forward, adding further uncertainty to the overall growth story.

While Vroom currently has a reasonably strong operationally-minded management team that will potentially keep costs under control for the time being, it may seem unlikely that growth can reaccelerate towards enabling the flywheel effect under a cost-optimized infrastructure.

Conclusion

Vroom has been facing significant pressure due to its hyper-growth strategy. The ongoing economic downturn also continues to make growth more expensive for Vroom. Top-line growth has declined as the management shifted the overall focus to improving unit economics and liquidity in the midst of operational challenges.

Trading at less than $1, the share price seems to have bottomed. At ~0.5x P/GP, it can be considered undervalued if the management delivers on the promised FY 2023 outlook. This can possibly expand multiple to +1x.

As an important caveat, Vroom is not really a growth stock at the moment. While the price may seem attractive, there are a number of high-risk factors associated with the stock, making it more of a distressed opportunity. I maintain a neutral rating and will remain on the sidelines while monitoring the management's execution in the next few quarters.

For further details see:

Vroom: Unfortunate Timing For Disruptive Growth