COM - W&T Offshore: A Q3 Beat Could Be A Catalyst For This Undervalued Stock

2023-10-19 05:38:58 ET

Summary

- Despite some current headwinds, W&T Offshore is significantly discounted relative to its underlying asset value.

- Going into Q3 earnings, the conditions appear favorable for a beat that could provide some catalyst action.

- In the medium term, higher natural gas prices and oil prices defending their current levels could help unlock additional value.

Investment thesis

W&T Offshore ( WTI ) is small and undervalued offshore oil and gas producer in the U.S. Gulf of Mexico. Based on a recent precedent transaction, the implied value of W&T's hydrocarbon reserves could be at least $1.5 billion which significantly exceeds the enterprise value of $845 million. For the valuation gap to close, the share price would need to appreciate from the current $4 to about $8-$9, reflecting a 200% gain.

While W&T has struggled this year due to unexpected operational problems and weaker oil and gas prices, the stock seems to have found a bottom in April and has since been hovering in this support region:

TradingView via Seeking Alpha

With the "Holy Grail" drilling prospect out of the picture until 2024, WTI is still in search of a catalyst. In the meantime, the renewed strength in oil prices ( CL1:COM ), on the back of the Saudi/OPEC+ cuts and the geopolitical risk premium, has created a favorable setup for a Q3 earnings beat and that may also spark some upward movement. The Q3 revenue estimate is $129 million, but with oil prices having topped analysts' projections, I expect actual revenue to come at $137 million at the mid-point production guidance. W&T will likely beat the EPS estimate of $0 too.

In the medium term, rising natural gas prices and oil prices proving they are able to hold their current levels will provide further tailwinds going into 2024.

Note: I have previously covered WTI on Seeking Alpha. For additional context, readers can reference my prior articles .

Is W&T Offshore a value stock?

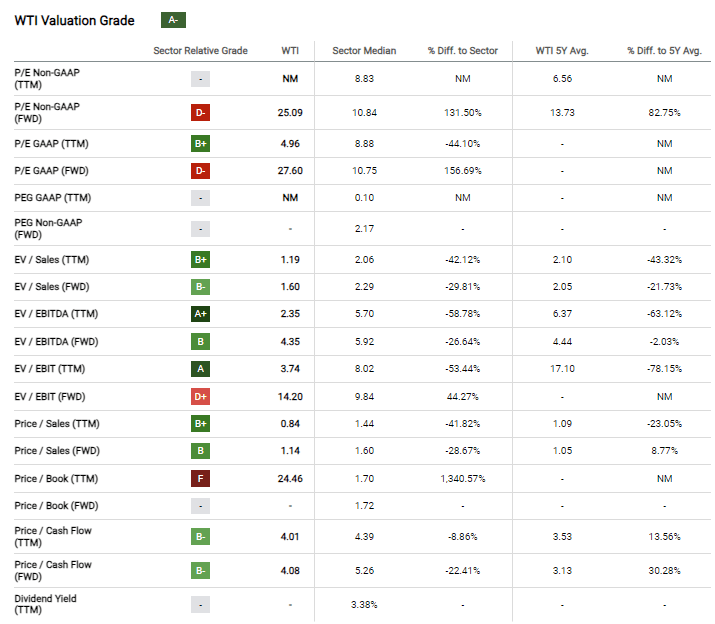

"Value" can mean different things to different people but it is usually associated with low pricing multiples. Seeking Alpha scores the company "A-" on valuation based on how W&T's ratios compare to the peer sector:

{kind=link}

However, while "A-" looks pretty good, it doesn't capture W&T's full potential. These ratios are based on flow measures (EBITDA, EBIT, Sales) and W&T is currently underperforming on these dimensions due to temporary factors :

- Weak Q1 production due to planned and unplanned downtime; this is impacting the production numbers for the whole year too;

- Unfavorable gas hedges which W&T had to enter to be able to refinance its debt not so long ago; this caused the company to miss out on the natural gas windfalls in 2022. Currently, about 2/3 of W&T's gas production remains hedged;

- Falling legacy production as W&T has had to manage cash tightly and has deferred its probably most promising drilling prospect (namely, the Holy Grail well at Garden Banks 783 in the Magnolia Field).

Yet, while investors value current profits, an oil and gas company is also a claim on the underlying reserves. Therefore, a company can also be a value stock if it trades at a discount to its net asset value (or NAV). In my view, this has indeed been the case and W&T's discount to its NAV is significant.

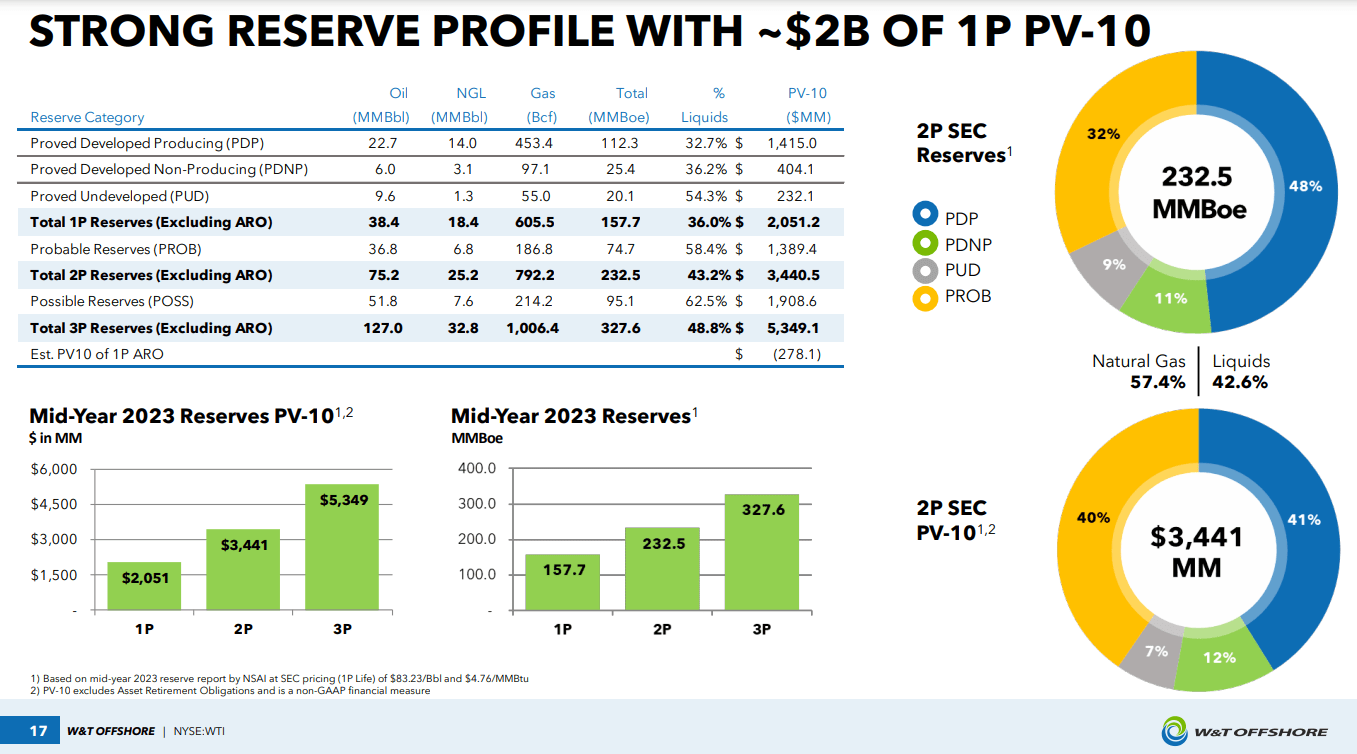

The company reports its "PV-10", a standardized NAV measure commonly used in the industry:

{kind=link}

Proved reserves or "1P" was estimated at $2 billion. Adding probable reserves increases this figure to $3.4 billion. This compares to an enterprise value of $845 million. Even focusing conservatively only on the "producing" portion of the 1P reserves suggests a PV-10 of $1.4 billion.

The PV-10 though follows a standardized methodology that uses backward-looking pricing so it isn't the same as a market value. However, W&T's acquisition last month of producing assets in the U.S. GoM provides another angle from which we can look at this.

The valuation implications of W&T's recent acquisition

Part of the reason W&T delayed drilling its Holy Grail prospect was to conserve cash that could be used for opportunistic acquisitions. It seems the company was indeed able to find suitable assets to acquire:

- Gross consideration in the recent acquisition was $32 million, funded from cash on hand (so no dilutive implications);

- Average working interest of 72%;

- Production volume of 2,400 boe/d (42% oil)

- Proved reserves of 3.2 million boe (49% oil); 100% of these reserves are proved developed;

- 2P reserves (proved + probable) of 5.1 million boe (48% oil).

This suggests W&T paid about $10.0 per 1P boe or $6.3 per 2P boe; applying these metrics to W&T's legacy reserve base implies a NAV of about $1.5 billion:

{kind=link}

More of the acquired proved reserves are producing relative to legacy W&T and the oil content is higher, but on the other hand the acquisition is only 2% of W&T's size. Scale typically drives a premium so you could also say the $1.5 billion estimate is rather conservative.

Based on W&T's capital structure, for the enterprise value to get to $1.5 billion, the stock price would need to increase from $4.14 to $8.65 for a 109% gain. The Wall Street target reported by Seeking Alpha is even north of my estimate:

{kind=link}

From a value perspective, W&T has the potential to double. The question is what could prompt the move up.

Could Q3 be a beat?

WTI is expected to report on November 1. According to Seeking Alpha, the consensus estimates are revenue of $129 million and EPS of $0. However, both oil and natural gas are tracking above the summer forecasts, so the setup for a "beat" is favorable.

The Q1 production issues have been addressed by now. Based on management's mid-production guidance plus the realized Q3 marker prices (assuming historical pricing differentials), I estimate Q3 revenue at $137 million:

Author's Calculations

If revenue is a beat even by 5%, very likely EPS will be a beat too. Further, given W&T cut its initial capex guidance for the year and 2023 is rather light on plugging & abandonment expense, I wouldn't be surprised if free cash flow comes out good too.

Looking further ahead to Q4, W&T would exit 2023 at about 3x EV/EBITDA:

Author's Calculations

Note that while 50% of WTI's production is gas, the oil price is still more important as a revenue/EBITDA driver. WTI doesn't have oil hedges. Gas is still 2/3 hedged but that mattered more in 2022. For Q3 and Q4 I don't expect significant hedging losses.

Risks

Short interest remains high:

That could be a risk which can drive the price lower but it could also be an opportunity that can magnify the effect of a Q3 beat. Given WTI has been in the same support region since April, I am starting to think that we have run out of potential sellers.

Gas prices brought WTI down from $9 last time but there are numerous signs that US natural gas ( NG1:COM ) has bottomed:

The major risk is perhaps oil heading back down to the $60s. Yet, when oil did do so in late March and again in early June, W&T was still in the same $3.50-$4.00 range. So I'm not sure how much downside is left.

Bottom line

W&T Offshore is undervalued relative to its asset base. From a valuation perspective, the stock price could double. A Q3 earnings beat could be a possible catalyst.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

W&T Offshore: A Q3 Beat Could Be A Catalyst For This Undervalued Stock