DIS - Warner Bros. Discovery: Looking At Earnings And EPS Through A Disney Lens

2024-01-12 12:17:15 ET

Summary

- Warner Bros. Discovery has made significant progress in its restructuring efforts since the merger closed in April 2022. WBD's undervaluation compared to its peers presents a significant investment opportunity.

- The DTC business is set to transform the company and is one which builds upon WBD's multiple existing strengths as a global media powerhouse.

- DTC is poised for significant additional growth, particularly internationally, and recognition of this potential should result in investors applying a much higher valuation.

- Looking at WBD's earnings / EPS in the form that Disney and most S&P 500 firms present "adjusted earnings" leads to a much better depiction of the company's "core earnings" - it would be $0.49 per share for Q3 2023 vs. GAAP EPS of $(0.17).

Thesis

Warner Bros. Discovery, Inc. ( WBD ) is now at the latter stages of its extensive restructuring since the merger closed in April 2022 and has made significant progress on many of its initial financial and strategic objectives. WBD quickly revamped its global organization and established enhanced financial controls to better manage the integration of its diverse global businesses. The company has focused on increasing its synergies, EBITDA, and Free Cash Flow with the objective of reducing debt incurred as part of the merger transaction. It anticipates Adjusted EBITDA of $10.5 million to $11.0 billion for 2023 (vs. $7.7 billion in 2022) and Free Cash Flow of approximately $5.3 billion ($3.3 billion in 2022). Further, it has paid down $12 billion of debt since April 2022 (representing a benefit of $5 per common share), and will easily achieve its net leverage target of net debt being less than 4x 2023 Adjusted EBITDA.

WBD is very focused on adapting and being at the forefront of the "generational disruption" that CEO David Zaslav discusses that the media business is going through. Now being through most of the integration since the merger, WBD is accelerating its investments in its growth and building upon its strengths as a global media company, including producing quality movies, series and games, and at the same time working to expand its DTC business by increasing global subscribers and increasing ARPU. Despite its many financial and business accomplishments, WBD continues to be the most undervalued diversified global media company, in my opinion. One of the reasons for this is the significant GAAP losses and negative EPS that WBD has reported since its merger as a result of the $16.6 billion of charges (mostly non-cash) resulting from the merger and integration of Discovery and Warner Media. If WBD were to present supplemental non-GAAP "adjusted earnings" similar to The Walt Disney Company ( DIS ) and 95% of S&P 500 companies, its financial successes would become much more apparent in the language that many investors look to - earnings and EPS rather than EBITDA alone, and would help change the narrative of WBD's financial performance.

I continue to believe that there is significant near- and long-term upside in WBD due to the company's strong fundamentals and financial performance. WBD should get a bump in its enterprise valuation ratio and share price as it continues to achieve successes in its transformation, including growing its overall EBITDA and FCF, and perhaps most significantly, the growth and profitability of its global DTC business.

3rd Quarter Financial Results

WBD's third quarter financial results included its highest ever quarterly Adjusted EBITDA of $3.0 billion, its second highest quarterly Free Cash Flow of $2.1 billion, and debt pay-downs of $2.4 billion - bringing net debt down to $43 billion at September 30, 2023. The company also disclosed that an additional $600 million of debt was paid down subsequent to that date, bringing net debt to $42.4 billion.

CEO David Zaslav and CFO Gunnar Wiedenfels made a strong case for the company's results and prospects, but the market reacted very poorly when Wiedenfels cautioned that given intended accelerated investments in growth initiatives (e.g., Max and games), unless the linear advertising market rebounds, WBD might not reach its internal target of having its gross (not net) debt being 2.5x - 3x Adjusted EBITDA by the end of December 2024. Wiedenfels' caution wasn't a concern about WBD's financial prospects or debt pay-down objectives - he was simply being transparent by suggesting caution about the linear advertising markets that were hard to predict with any certainty. He did reiterate that the company would meet its gross debt leverage ratio over time if not by December 31, 2024, and "was not intending to guide down EBITDA for 2024 relative to where WBD is today".

Describing the target leverage for a specific date as a multiple of Adjusted EBITDA becomes circular with multiple unknowns. It would be much more straightforward for WBD to simply say that in 2024 it intends to reduce its debt by another $4 billion to $6 billion (which is well in excess of 2024 scheduled debt maturities of $1.8 billion) - resulting in a reduction of its net debt to approximately $34.5 billion to $36.5 billion (with gross debt approximately $2.5 billion higher), and that it intends to continue to reduce its debt until the gross debt leverage target of 2.5-3.0x Adjusted EBITDA is achieved.

The company maintained its guidance for full-year 2023 Adjusted EBITDA to be at $10.5 billion to $11.0 billion. Given that $7.7 billion of Adjusted EBITDA was reported for the nine months ending September 30, 2023, this implies a fourth quarter Adjusted EBITDA of approximately $2.8 billion to $3.3 billion. Wiedenfels indicated that Free Cash Flow for 2023 is expected to be approximately $5.3 billion. Since FCF for the nine months ending September 30, 2023 was $2.8 billion, this implies a fourth quarter FCF of approximately $2.5 billion. Given this level of FCF, the company's net debt at December 31, 2023, should be approximately $40.5 billion (equal to September 30, 2023 net debt of $43.0 billion less $2.5 billion of fourth quarter FCF).

As mentioned in my previous article , WBD has an extremely attractive low-cost, fixed-rate (4.66% WAC) long-term debt structure with long and staggered maturities extending out to 2062 with an average life of 15 plus years as of September 30, 2023. The company is insulated from increases in interest rates and doesn't have any looming debt maturities or refinancing risks. Consistent with its $12 billion of debt reductions accomplished to date, WBD intends to continue to reduce its debt much faster than its scheduled debt maturities. Of the company's remaining debt (post September 30, 2023, prepayment on its term loan): $40 million was due on December 15, 2023, $1.8 billion is due during 2024, $3.7 billion is due in 2025, $2.3 billion is due in 2026, $10.0 billion is due between 2027 and 2031, $6.7 billion is due between 2032 and 2041, and $20.1 billion is due between 2042 and 2062.

Looking at WBD's Earnings Through a "Disney Lens"

To date WBD has focused its earnings presentations on Adjusted EBITDA and Free Cash Flow and has made tremendous improvements in both these improved financial metrics since the merger closed. However, I believe these are largely underappreciated by the "market" in valuing WBD's equity and are certainly ignored by the media which has a difficult time putting EBITDA and FCF in context.

Many investors and financial media reporters prefer to focus on earnings and P/E ratios as a way to gauge a company's performance over time and to compare companies. However, due to the significant (mostly non-cash) charges resulting from the merger and integration of Discovery and Warner Media, WBD has reported continuing significant GAAP losses and negative EPS. Over the 18-month period ending September 30, 2023, WBD recorded approximately $16.6 billion of acquisition-related charges - including $11.0 billion (all non-cash) of amortization expense of acquisition-related intangibles, $4.3 billion (approximately $3.0 billion non-cash) of restructuring and impairment charges, and $1.3 billion (all cash) of transaction and integration expenses. As a result of these charges, WBD's traditional GAAP net income (loss) and GAAP EPS disclosures are not particularly meaningful since these charges create huge distortions in its GAAP earnings (loss).

Presentation of Adjusted Earnings

WBD was ahead of its media peers when it began taking restructuring charges soon after its merger closed in April 2022. The company's peers (Disney, Paramount Global ( PARA ) and Comcast Corporation ( CMCSA )) have since made similar moves in terms of taking write-downs, and have also made acquisitions in the past that have resulted in significant amortization expenses relating to acquisition-related intangibles. What these companies do differently from WBD is that they present a supplemental non-GAAP presentation of "Adjusted Earnings" and EPS that excludes these non-recurring charges and acquisition-related amortization charges in order to assist investors in analyzing their core financial results. I believe WBD should similarly present supplemental reporting of non-GAAP earnings / EPS in order to provide a more insightful presentation of the significant improvements in its core earnings.

A recent HBR article "Mind the GAAP" indicated that over 95% of S&P 500 companies report both GAAP and non-GAAP earnings, showing its widespread acceptance. As described in the article, "Non-GAAP earnings are a customized version of earnings calculated after excluding earnings components that don't require cash payments or are otherwise not important for understanding the future value of the firm. Firms first report GAAP earnings. Then they detail each item that was added or subtracted from GAAP earnings to arrive at non-GAAP earnings."

Presenting supplemental non-GAAP earnings and EPS doesn't change the substance of a company's financial performance - but can provide a better framework for investors to analyze a company by excluding non-recurring charges and non-cash amortization charges relating to acquisition-related intangibles. Some companies also exclude non-cash compensation charges. It's important to note that this is a supplemental disclosure and does not replace traditional GAAP disclosures.

Disney's Presentation of "Diluted EPS excluding certain items"

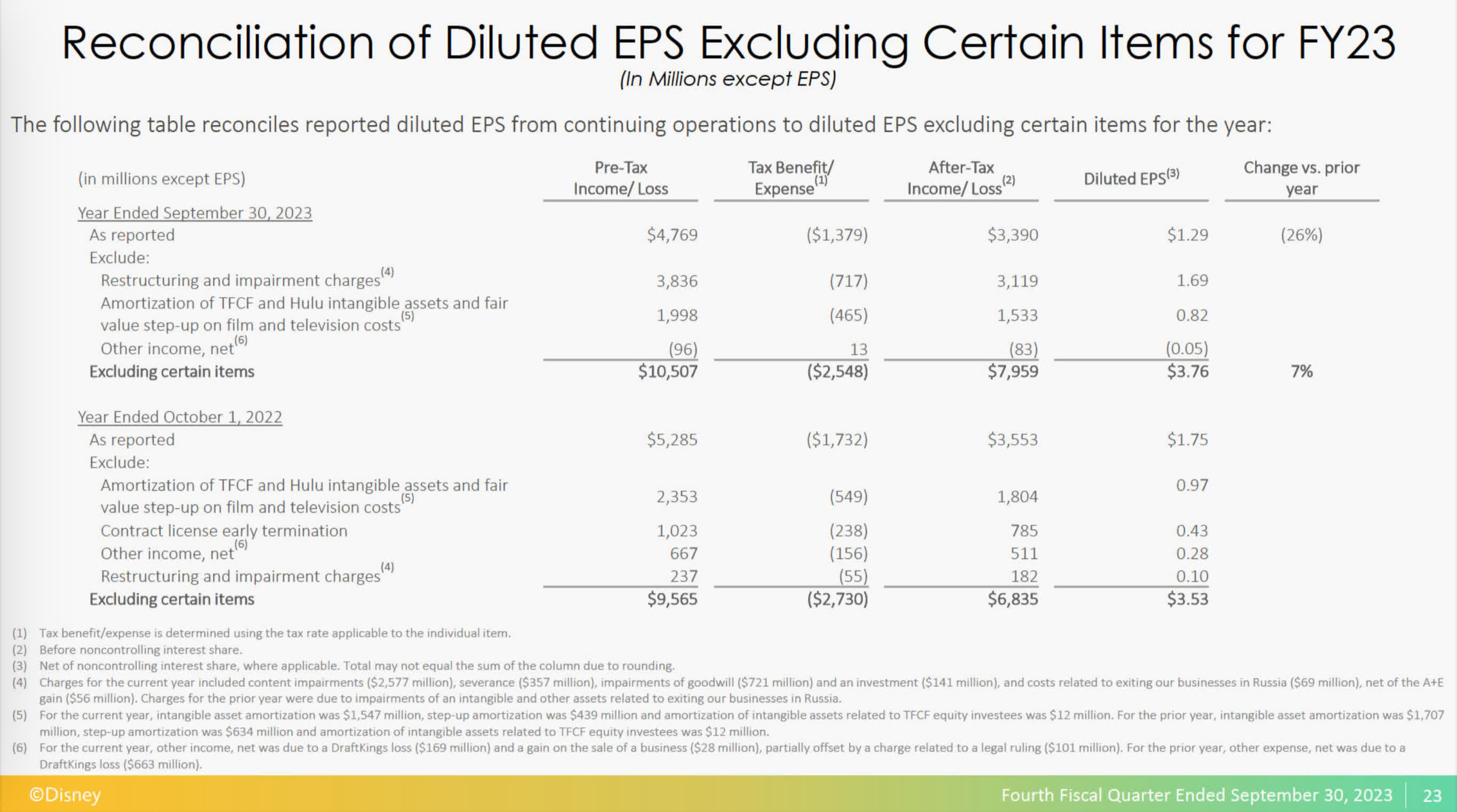

Disney is a great example of a media company showing a supplemental non-GAAP adjusted earnings / EPS presentation, which it refers to as "Diluted EPS excluding certain items". For its fiscal year ending September 30, 2023, Disney excluded $3.8 billion of restructuring charges and $2.0 billion of amortization charges relating to its acquisition of 20th Century Fox and Hulu.

The following chart shows Disney's reconciliation of "After-tax income/loss and EPS" (as reported) to "Diluted EPS excluding certain items" for the fiscal year ended September 30, 2023. For this period, the company reported EPS excluding certain items of $3.76 per share versus GAAP EPS of $1.29 per share.

Disney Presentation of "Adjusted Earnings / EPS" (Disney Earnings Presentation for Fiscal Year ending 9/30/23)

{kind=link}

Disney's presentation of "Diluted EPS excluding certain items" provides a much more meaningful picture of Disney's core earnings performance and is the principal earnings-related metric that is followed by the market and the media.

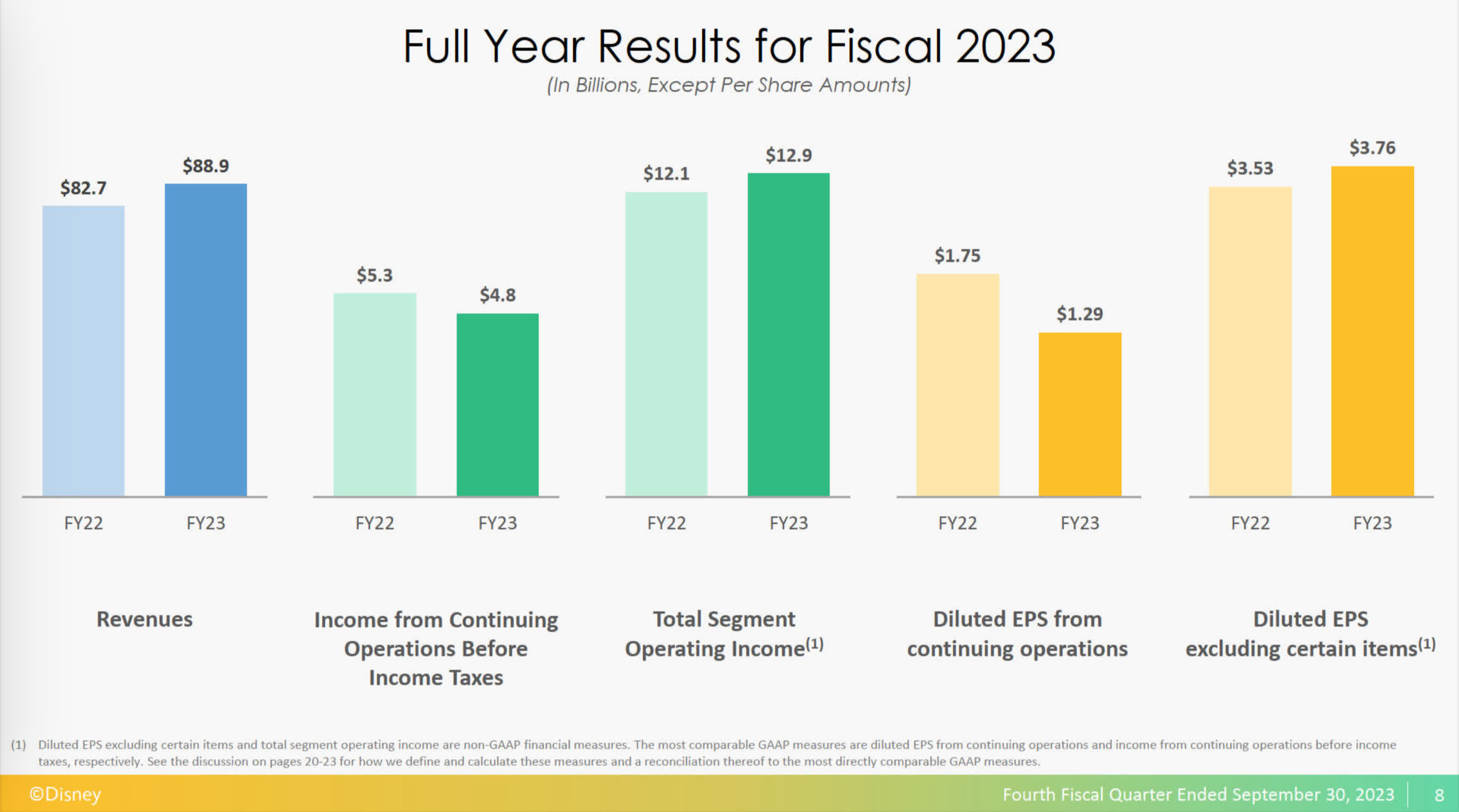

Disney Presentation of Results for Fiscal 2023 (Disney Earnings Presentation for Fiscal Year ending 2023)

{kind=link}

Adjusted earnings and EPS presentations get headline status and GAAP EPS disclosures, restructuring and amortization charges get minimal mention in Disney's presentation and management discussion on its earnings call. In the earnings conference call for the quarter ending September 30, 2023, Disney's Interim CFO Kevin Lansberry's initial comment was: "Now to dive into this quarter's results. Diluted earnings per share, excluding certain items, increased versus the prior year to $0.82 in the 4th quarter, and $3.76 for the full fiscal year."

Analyst use of non-GAAP EPS disclosures

Analyst estimates are generally for adjusted earnings so it's important for companies to present a non-GAAP earnings presentation in order to create a core earnings baseline on which analysts can base their future earnings estimates. Analysts are unlikely to estimate "adjusted earnings" for a company if the company doesn't itself present its presentation of "adjusted earnings". It's nearly impossible for analysts and investors to anticipate restructuring charges and acquisition-related amortization charges unless specifically guided by a company, so for analysts trying to estimate only GAAP EPS can frequently miss on their earnings estimates.

Though I'm not an expert on all of the nuances of quantitative trading, I suspect that many quantitative models are taking feeds from I/B/E/S (and similar financial database services) without making adjustments to GAAP earnings to provide better peer-to-peer comparisons. As an example, multiple EPS estimate misses and negative momentum trends have adversely impacted WBD's quantitative rating on Seeking Alpha - where WBD currently gets a "C-" for "Momentum", and a "C-" for "Revisions".

Media coverage of non-GAAP earnings disclosures

The media generally reports what companies report in their earnings releases and conference calls without a lot of their own independent analysis. If adjusted earnings are reported by a company, the financial media tends to highlight "adjusted EPS" over GAAP EPS. As a result, it's extremely important that a company present its financial results to the investment community and media in a meaningful way, including its presentation of non-GAAP adjusted earnings and EPS disclosures to supplement GAAP disclosures.

The financial media also reports how reported earnings (GAAP or non-GAAP) compare versus Street estimates, which are usually focused on "adjusted earnings". Since WBD does not present adjusted earnings or EPS, WBD has experienced multiple EPS estimate misses which get reported by the media as negatives - putting WBD at a significant disadvantage versus Disney and its other peers in the investment community - and contributing to WBD's low relative valuation.

Presentation of WBD's "Diluted EPS Excluding Certain Items"

WBD has attracted more than its share of negative press (e.g., too much debt, massive losses, write-off of Batgirl, etc.) which impacts the narrative about WBD. Presentation of adjusted earnings in a manner similar to the way its peers present adjusted earnings would help change the negative tone of so much media coverage of WBD. Although WBD is very transparent in its detailed financial disclosures and management presentations, not presenting "adjusted earning/EPS" has resulted in the company being viewed by the investment community and the media in a much worse light than its peer group.

Although WBD doesn't present a non-GAAP net earnings / EPS calculation in its press release or earnings presentation, it includes in its quarterly earnings presentations the information required to make such a determination. As an example, from the second bullet point on the first page of the 3rd Quarter Press Release :

- "Net loss available to Warner Bros. Discovery, Inc. was $(417) million, and included $1,758 million of pre-tax amortization driven by acquisition-related intangibles and $269 million of pre-tax restructuring expenses."

The following chart shows a non-GAAP presentation for WBD presented similar to Disney's "Earnings excluding certain items". This presentation shows a dramatically different story than just looking at WBD's traditional GAAP earnings and EPS - which, as discussed earlier, are relatively meaningless.

Pro Forma Calculation of EPS "Excluding Certain Items" (Author based upon WBD Trending Schedules and Press Releases)

This presentation provides a much better picture of WBD's core earnings away from its restructuring and acquisition-related amortization charges. It would be very advantageous for WBD to begin presenting this supplemental information since the company would be perceived in a much better light than it is now by just showing its continuing GAAP and EPS losses.

- For the 3rd quarter ending September 30, 2023, WBD's non-GAAP Earnings excluding certain items would be $1.2 billion and EPS excluding certain items of $0.49 per share, as compared to the reported GAAP Net Loss of $(417) million and EPS of $(0.17) per share.

- For the 12 months ending September 30, 2023, WBD's non-GAAP Earnings excluding certain items would be $2.6 billion and EPS excluding certain items of $1.08 per share, as compared to the GAAP Net Loss of $(4.8) billion and EPS of $(1.98) per share.

The contrast in presentation is startling and there is no rational reason for WBD not to present a supplemental non-GAAP presentation of Earning/EPS like Disney, its other media peers and most public companies. Doing so can only help change the narrative of WBD's financial performance and help give the company credit for the significant accomplishments achieved since the merger closed last year. For a company that prides itself in "storytelling" in its studios, I think WBD owes it to its shareholders to do a better job in this area of investor communication.

The benefits of disclosure of adjusted earnings are many. Most importantly it presents WBD's earnings and EPS in a more realistic view of its core earnings and on the same footing as its peers. By doing so analysts and investors can better estimate adjusted earnings/EPS for future periods - resulting in fewer earnings estimate misses that have plagued WBD since its merger. Many investors and financial media representatives utilize P/E ratios as a fundamental valuation metric in accessing the relative value of companies. WBD's negative GAAP EPS results in being not meaningful for investors considering the company using P/E ratios, but using adjusted EPS, the application of P/E ratios as a valuation metric becomes doable. As an example, Disney has a PE/Adjusted EPS ratio of 24x for TTM - applying the same multiple to WBD's TTM adjusted EPS of $1.08 would suggest a price of approximately $26 per share.

WBD Continues to be Significantly Undervalued

WBD has made tremendous progress in integrating, rationalizing, and improving its businesses for the future. Almost since the transaction closed, the company has faced general macroeconomic and media market/industry headwinds which it has responded to with experience, good management, hard work and creativity. In addition to focusing on achieving efficiencies, WBD has focused on ways throughout its businesses to monetize its diverse content - from embracing theatrical releases of its movies, to licensing content to other media firms, to offering multiple price points and products in its streaming business, etc.

WBD's Enterprise Valuation

At a share price of $11.20 (the closing price as of January 5, 2024), WBD's enterprise valuation is approximately $70 billion (equity market capitalization of $27.3 billion plus pro forma current net debt of $42.5 billion). The midpoint of the recent guidance for 2023 EBITDA is $10.75 billion - resulting in an EV/EBITDA ratio of 6.5x. WBD's enterprise valuation and EV/EBITDA are extremely low by any measure relative to its media peer group, as seen in the following chart.

WBD Peer Valuation Metrics (Author based upon respective company disclosures and Seeking Alpha )

Each member of the peer group has its own uniqueness, but it stands out how cheaply WBD is valued on a relative basis across various valuation metrics. Similar EV/EBITDA ratios (based on forward EBITDA estimates) for Disney, Paramount, Comcast and Netflix are 12.0x, 10.8x, 7.2x and 29.5x, respectively.

WBD is also very cheaply valued from a Free Cash Flow perspective - WBD had $5.3 billion of FCF ((TTM)), which is higher than Disney's $4.9 billion ((TTM)), and much higher than Paramount's negative FCF of $(900) million for the past 12 months. Disney generates more cash flow than WBD but has a continuing need for significant investments in its Parks & Entertainment segment, resulting in less FCF. Disney recently announced that it intends to invest $60 billion in Parks & Entertainment over the next 10 years.

Prospective WBD Valuation

With most of the significant restructuring activities behind it, WBD is expected to continue to increase its EBITDA and FCF. Based upon the second half of 2023, WBD is now running its Adjusted EBITDA at an approximate $12 billion annual rate despite the impact of the dual strikes, with upside as revenues and synergies increase. The company's initial objective for merger "synergies" was $3 billion - and it has now achieved $4 billion of synergies, with an expected $5 billion of synergies for 2024 and beyond.

WBD should get a bump in its enterprise valuation ratio and the share price as it continues to achieve successes in its transformation, including growing its overall EBITDA and FCF, continued debt reductions and, perhaps most significantly, the growth and profitability of its global DTC business.

Let's conservatively assume that WBD's Adjusted EBITDA for 2024 will be $12 billion to $13 billion, and that its net debt to be reduced by December 31, 2024, to approximately $35 billion ($5 billion less than the expected level as of December 31, 2023). Conservatively applying an EV/EBITDA ratio of 8.5x - the median for media companies - results in an Enterprise Value of approximately $102 billion to $110.5 billion, and equity capitalization of $66 billion to $75 billion - equivalent to approximately $27.50 to $30.95 per share - or 146% to 176% higher than WBD's current share price. Using an EV/EBITDA ratio similar to either Disney (12.0x) or Paramount (10.8x) would result in a much higher price.

WBD's extremely low valuation and EV/EBITDA ratio suggest that investors are valuing the company primarily on its linear TV business. This business remains profitable and a generator of significant EBITDA and FCF but is expected to decline over time as the number of cable subscribers decline and linear advertising revenues decline. WBD is dealing with these declines by focusing on minimizing costs and maximizing profitability, while at the same time looking to expand the profitability of its Studio segment (including games), and its DTC segment, and generally looking to enhance monetization of its expansive content library.

WBD's DTC Business will Expand WBD's Enterprise Value

WBD's DTC segment is the business that will truly transform the company and is a business which builds upon WBD's multiple existing strengths as a global media powerhouse. The segment is poised for significant additional growth in the next few years and recognition of this potential should result in investors applying a much higher valuation ratio for WBD, resulting in a much higher enterprise valuation and share price.

WBD has the critical scale to be profitable and has turned around its streaming business so that it is now profitable, and now expects DTC segment profits of $1 billion plus in 2025. The company is extremely well-positioned to add subscribers globally and increase DTC profits. It has a similar number and mix of subscribers as Netflix did about 6.5 years ago - about 95 million subscribers - similarly split 50/50 between domestic and international. The market capitalization of Netflix was about $75 billion at the time, greater than WBD's current valuation.

Looking at the historical growth of Netflix's subscribers provides a good guide for WBD's DTC growth potential. The chart below shows the growth of Netflix subscribers over the past 6.5 years (from March 31, 2017 to September 30, 2023) - from approximately 95 million subscribers to 251 million. Over this period, Netflix added 20 million additional subscribers in the US & Canada and 130 million additional subscribers internationally.

Growth of Netflix Subscribers by Geographical Area (Author based upon Netflix financial statements)

This highlights that the huge opportunity for Max is to grow its international subscriber base from its current 42.5 million international subscribers. Perhaps more than any of its peers, WBD is the best-positioned global media company to expand its international DTC subscriber base over the next few years. WBD has a huge advantage that its broad content, franchises and brands are already globally known through its 100 years of movie production and distribution - plus existing content licensing deals that have potential subscribers already watching WBD content. In addition to its enormous library, WBD has a steady stream of new series and a robust movie pipeline that will feed into Max after completing their theatrical windows. To further bolster its content for Max, WBD has recently begun licensing content from other parties - including A24 Productions . WBD already has a global organization through its international movie distribution business and its existing international streaming operations (Max and Discovery), which under Zaslav's leadership are motivated to work together.

In the first quarter of 2024 WBD will be rolling out its Max platform in various markets around the world - initially in Latin America and select European countries . In addition, at the end of December 2023, WBD acquired 100% of BluTV , the largest streaming service in Turkey with an estimated 4.2 million subscribers.

The profitability of WBD's DTC business should continue to accelerate during and after 2025 since the company's exclusive content licensing agreements with SKY (now part of Comcast) will come to an end during that year. These pre-existing licensing agreements license HBO productions and certain Warner Bros. movies to SKY - yet restrict WBD's ability to market and offer Max to the subscriber-rich markets of England, Ireland, Germany and Italy (the agreements were with Warner Media and do not limit Discovery+, which has a presence in these markets). According to FlixPatrol data , Netflix has approximately 33 million subscribers in these 4 countries alone - highlighting the significant opportunity for Max expansion once these market restrictions end. A compelling case can be made that WBD/Max can at least double its subscriber base to 200 million or more over the next 3 to 5 years given (1) WBD's existing global business and platform (including extensive language capabilities), an enormous platform of content and new productions, integrated news platform and add-on live sports platforms, and (2) the global familiarity and acceptance of streaming platforms.

The financial implications of WBD growing its DTC subscriber base are significant. Assuming revenues of $10 per month per subscriber, adding 100 million subscribers would result in approximately $12 billion of incremental annual revenue. Assuming a 50% to 60% incremental margin, the incremental benefit to WBD's EBITDA would exceed $6 to $7 billion annually - which would significantly increase the company's value in two ways: (1) expanded company-wide EBITDA and (2) the market applying a higher EV/EBITDA ratio in valuing WBD's enterprise and market value.

Conclusion

Going forward, it is easy to see that WBD shares could increase to the mid $20s over the next 12 months as its diversified global businesses flourish, resulting in: (1) increased Adjusted EBITDA and free cash flows coming from increased revenues and synergies, (2) continued significant debt reductions well in excess of scheduled maturities, and (3) a higher EV/EBITDA valuation ratio being applied by the market as result of the company's success in accomplishing the first two objectives and growing breadth and profitability of WBD's DTC business.

WBD is a unique and very attractive "pure" play in global media and entertainment. Due to Morris Trust restrictions, WBD is not permitted to be involved in any corporate transactions until after April 8, 2024 (the 2-year anniversary of the merger). WBD would be an extremely attractive and cheap acquisition for a number of potential suitors, including Amazon.com, Inc. (AMZN), Apple Inc. (AAPL) and Comcast. Given WBD's very cheap valuation, I am of the view that an acquisition of WBD would be immediately accretive to either Amazon or Apple even if a purchase were done at double WBD's current price. It's worth noting that all of these potential buyers would be able to assume WBD's very attractive debt structure.

It's time for WBD's board of directors and management to focus on enhancing shareholder value. Given its successes in significantly reducing its outstanding debt burden by $12 billion to date, I believe that WBD should allocate a portion of its Free Cash Flow that would otherwise be used to reduce debt ahead of schedule to start to repurchase stock. Purchasing stock at its current low price would be much more beneficial than prepaying low-cost debt well before scheduled maturities, in my view. The announcement and actual repurchasing of $1.0 billion to $2.0 billion plus of stock would be accretive to EPS, WBD's share price, and would help reduce the volatility of WBD's shares.

With WBD currently trading at such a cheap price, there is the possibility that suitors and/or activist investors will begin to increase or take positions in WBD ahead of the 2-year anniversary and could try to force a sale of the company. They could also try to force the company to buy back stock as a way to increase shareholder value, or potentially block any potential acquisition of Paramount. I believe that this dynamic should bring positive momentum to the stock price in the coming months.

For further details see:

Warner Bros. Discovery: Looking At Earnings And EPS Through A Disney Lens