W - Wayfair Doesn't Need A Chinese Buyout

2023-12-29 17:27:30 ET

Summary

- Wayfair Inc. is struggling to stabilize sales post-Covid, but the company is optimistic about its potential for returning to double-digit growth.

- A potential buyout by a Chinese retailer is unlikely due to Wayfair's improved business model and the low valuation of the company.

- The stock should rally as Wayfair hits 10% growth targets, though economic weakness in 2024 could delay such a goal.

Wayfair Inc. ( W ) is another online retailer still struggling to right-size the business for the normal sales pattern post-Covid. The online furniture platform saw a massive flood of sales in 2020 with consumers stuck at home needing furniture for home offices and students learning from home. My investment thesis is Bullish on the concept turning the corner in 2024, with the very unlikely outcome of a buyout by a Chinese retailer.

Source: Finviz

Limited Excitement

Not long ago, Wayfair was an exciting online furniture business with superior supply chain dynamics taking on e-commerce giant Amazon ( AMZN ). The business saw sales surge during the early stages of Covid, with Q2 2020 sales jumping 84% to $4.3 billion, sending the stock to over $300.

The company has now struggled for years to stabilize quarterly sales around just $3 billion, with Q3'23 sales reporting the first YoY gain since Q1'21 at a small 3.7%. Wayfair has finally turned the corner back towards growth mode, though the U.S. economy could struggle in 2024, raising questions about the size of and durability for e-commerce growth in the year ahead.

Consensus analyst estimates aren't forecasting much in the way of growth in the years ahead, with a peak of 8.6% in 2025. Though, the upside potential is from Wayfair continuing back on the path of grabbing market share in a growing shift towards online purchases.

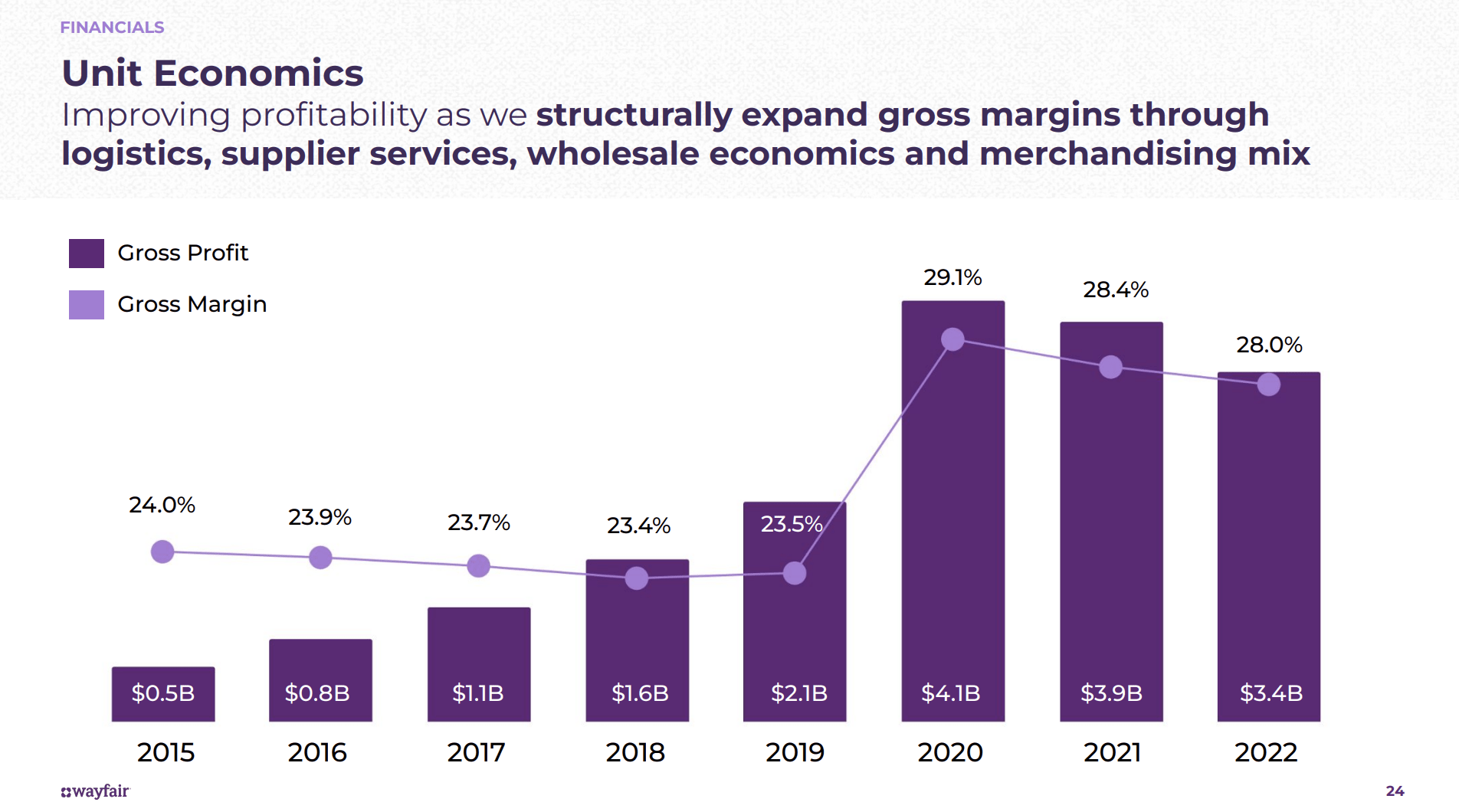

What investors do know is that Wayfair has vastly improved the business model during the Covid years. The online furniture company now has better unit economics, with gross margins of 28.0% in 2022 and reaching 31.1% in Q3'23.

{kind=link}

For Q3'23, Wayfair actually reported adjusted EBITDA of $100 million and free cash flow of $42 million. Due to the dynamics of the stock market since the Covid peak, companies haven't pushed growth initiatives in a few years to focus on the profitability and long-term stability of the business.

What the market appears to have missed is that Wayfair has been pushing the narrative of returning to double-digit sales growth. The company continually pushes the narrative of a total market opportunity reaching $1 trillion in 2030 and a suggestion the company has built a platform to grow from $10 billion to $100 billion in sales.

At the 2023 Investor Day in August, Wayfair promoted a path back to double-digit growth with at least 5% annual growth just from category growth shifting online similar to prior to Covid. When adding in market share gains from a massive market, the company is predicting a durable ability to compound growth of at least 10%.

{kind=link}

Unlikely Chinese Deal

A report by The Information suggests Chinese online retailers like Shein and Temu, owned by PDD Holdings ( PDD ), could buy Wayfair for their distribution network. While the stock only trades at $7.5 billion valuation, a Chinese company is unlikely to fork over a premium of up to at least $10 billion to buy out shareholders.

At the end of Q3, Wayfair only lists the PP&E at $751 million. The company has 17 fulfillment centers with 20 million sq. ft of fulfillment space, but the business would have to be bought at a bargain-basement price just for the assets to make such a purchase work.

The online furniture platform has built the network to deliver large, bulky items at scale and with efficiency. Wayfair would likely have no interest in being bought out by a Chinese retailer, nor would Shein or Temu likely have an interest in overpaying for an online furniture business focused on bulky delivery. Besides, the business transaction would likely come under regulatory scrutiny given that this is a Chinese business trying to acquire a supply chain and delivery network in the U.S.

Wayfair likely rallies due to a return to sales growth and the cheap valuation. As the company reaches double-digit growth and heads towards a 10% EBITDA target, the current market cap is very low.

At $15 billion in future sales and a 10% EBITDA margin, Wayfair would generate $1.5 billion in adjusted EBITDA. A simple multiple of 15x adjusted EBITDA gets to a stock valuation of $22.5 billion. The big question is how long Wayfair takes to reach those sales levels, considering the potential for a weak retail environment in 2024.

Takeaway

The key investor takeaway is that Wayfair Inc. appears on the path back towards solid growth, though a weak economy in 2024 could derail the path again. The stock has substantial upside potential once the business is back in growth mode and generating solid adjusted EBITDA margins, making the desire for a deal by a Chinese retailer non-existent.

For further details see:

Wayfair Doesn't Need A Chinese Buyout