WSM - Wayfair: Lowering Rating To 'Sell'

2023-06-28 10:57:37 ET

Summary

- W stock has surged by 85% since April.

- W has gained market share as some peers sacrifice share in order to keep pricing power.

- The company's expectations for positive EBITDA in Q2 despite negative sales growth could be optimistic.

Back in April , I wrote that while the furnishings industry is facing headwinds, with Wayfair ( W ) down -70%, I was neutral on the name. Since then, the stock has skyrocketed higher, up nearly 85%. Let's catch-up on the name.

Company Profile

As a reminder, W sells furniture, home décor, and houseware products primarily online, although it does own some physical stores. It runs the Wayfair, Perigold, and Birch Lane brands exclusively online through its e-commerce sites. Its AllModern and Joss & Main concepts sell their offerings online, but also have physical stores.

W generates revenue through the sale of products on its site, which includes offering from more than 20,000 suppliers. These suppliers generally ship the products sold through W directly to customers. That said, W has been expanding its logistics network. It operates an ocean transport service called CastleGate Forwarding that transports products manufactured in Asia to fulfillment centers in North America and Europe. In addition, it provides last-mile and middle-mile delivery services for large items through its Wayfair Destination Network. Net revenue from product sales includes shipping costs charged to the customer.

{kind=link}

Skyrocketing Stock

W shares saw a huge jump following its Q1 earnings in early May, rocketing 28.4% higher the next session. However, much of its gains have come since late May, perhaps spurred by a JPMorgan upgrade of the stock.

At the time of the upgrade, JPMorgan analyst Christopher Horver wrote:

"Both a positive shift in market share trends and management's newfound commitment to controlling expenses/investments should cause a significant inflection in earnings revisions from steeply negative over the past two years to positive, on top of what we view as an attractive valuation."

The move to control expenses is not new, as the company laid out a plan to save $1.4 billion in January. Of that total, the company sees $500 million coming from operational cost savings. The company says it sees 70 distinct areas of savings. Two areas it highlighted on its Q1 call were reducing parcel damage and optimizing shipping costs to get the best rates on items that fall in a gray area between a small and large parcel.

{kind=link}

The early fruits of its cost-cutting did show in Q1, both in gross margins and with other expenses. Gross margin improved 280 basis points to 29.6% from 26.8%, despite a pretty big promotional period for the company. Meanwhile, excluding restructuring and impairment charges, it was able to reduce its operating expenses by -2%.

Those cost controls helped the company reduce its adjusted EBITDA loss from -$113 million a year ago to -$14 million in Q1 2023. Free cash flow, meanwhile, improved from an outflow of-$331 million a year ago to -$234 million.

While an improvement, it should be noted that its stock comp soared nearly 40% to $144 million from $104 million a year ago, and including related taxes rose from $112 million to $151 million. While stock comp is excluded from adjusted EBITDA and doesn't impact cashflow, it is ultimately a real expense that dilutes shareholders. Over the past year, W's fully diluted share count has increased about 10%. And at current prices, those additional securities add up to over $800 million.

Shifting compensation more towards equity compensation can certainly help EBITDA numbers look better, and while it's not the only reason for the improvement, it certainly plays a big role.

The JPMorgan note also mentions W taking share. The company noted that the category as whole was down about -20%. In the U.S., W saw its revenue decline -5% while overall revenue was -7.3% lower. Active customers fell -14.6% to 21.7 million, while orders delivered fell -6.7%.

So based on that, yes W technically did outperform the market and take share. However, there are some dynamics to consider. The furnishings industry and home décor industry has seen some bankruptcies, Bed Bath & Beyond is well known in the décor space for going bankrupt, while United Furniture/Lane Home Furnishings left a $550 million void in the furniture market when it shut down.

Meanwhile, some companies like RH (RH), which I recently wrote about , and Williams-Sonoma (WSM), which I also recently looked at , have tried not to play the promotional game as much as W has. Instead, these retailers have been willing to give up some share in order to maintain pricing power.

Valuation

W currently trades around 36x the 2024 consensus EBITDA of $283.3 million and about 20x the 2025 consensus of $509.8 million.

Revenue growth is expected to fall -2% this year, and then grow around 7% in 2024 and 11% in 2025.

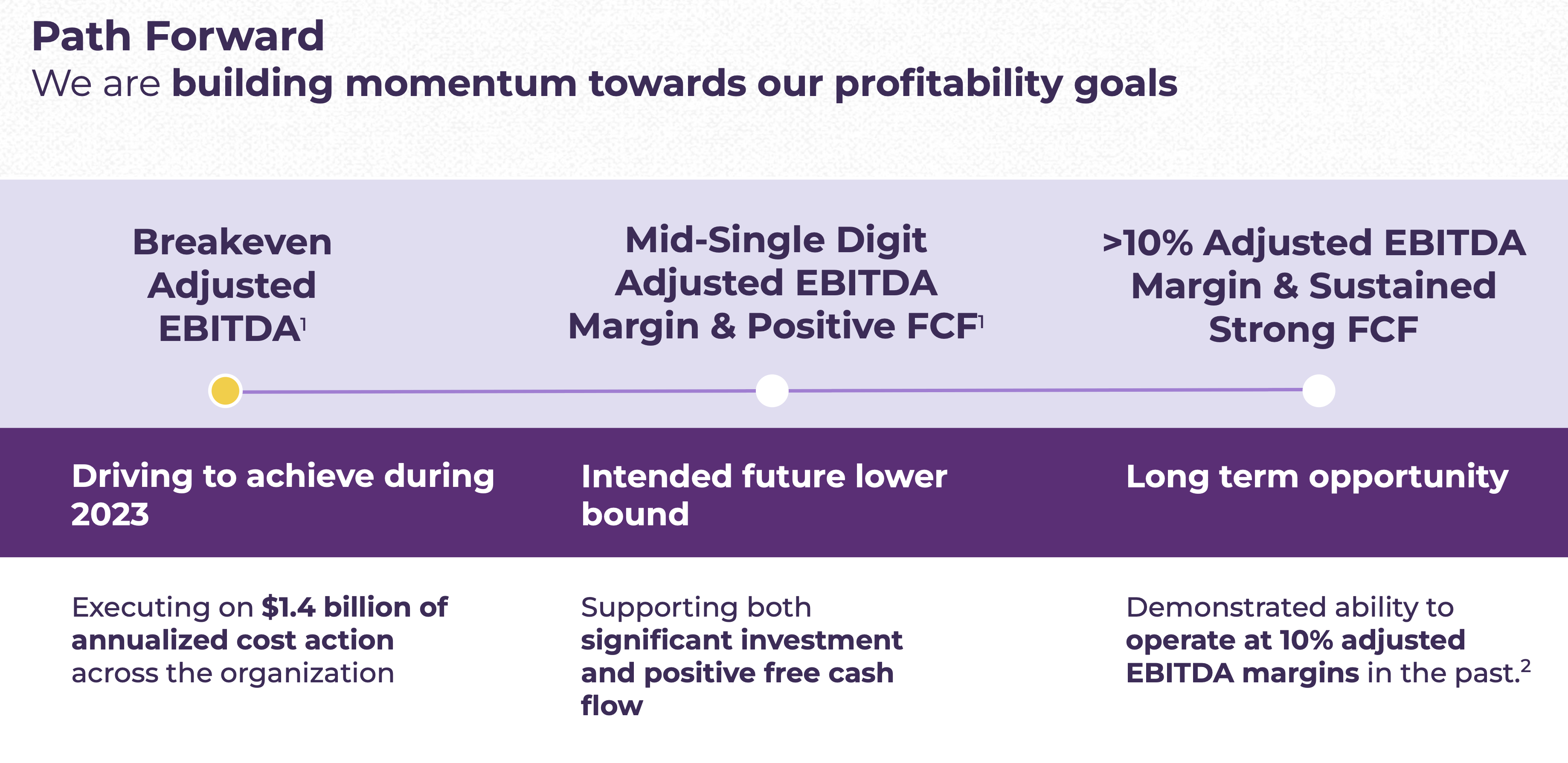

W has guided for adjusted EBITDA to be around breakeven for 2023. It is looking for a mid-single adjusted EBITDA margin and to be positive free cash flow ("FCF") in the near term. Longer term, it is looking to get to over 10% adjusted EBITDA margins and to generate strong FCF.

The company trades many multiples above other furniture retailers, including Overstock.com (OSTK), which may be its closest peer.

Conclusion

The only time W has been able to show a profit was during one of the greatest home furnishing environments we've seen when there was just a lot of pull-forward demand due to Covid. Today's environment is much different, and while the company may have been able to take some share, there are certainly some reasons behind this that likely aren't sustainable in the long run.

The company's expectations to see positive EBITDA in Q2 despite at the time of its call seeing negative high-single-digit quarter-to-date sales seems a bit optimistic. Of course, the company is looking for stock-comp and related taxes to come in at a whopping $170-200 million in Q2. A year ago, the company had stock comp and related tax expenses of $133 million, so that's a 39% increase at the mid-point and shows the continued shift away from cash expenses in favor of stock comp.

Investors right now don't seem to care about W basically shifting expenses from cash to equity, instead celebrating its march to "positive" EBITDA. This seems more like a parlor trick than the company meaningfully improving its operations in my view. With the stock skyrocketing off its lows, I'm going to lower the stock to "Sell."

For further details see:

Wayfair: Lowering Rating To 'Sell'