W - Wayfair Returned To Growth (Upgrade)

2023-09-07 10:20:32 ET

Summary

- Wayfair showed improving trajectory in Q2 with reaccelerated revenue growth and returning to free cash flow breakeven.

- Wayfair remains unfavored by many investors and short sellers.

- Short interest remains high at 24%, indicating divergence in opinions.

- Wayfair maintains a competitive edge in the furniture market, as evidenced by high app ratings and an asset high turnover rate over its peers.

Wayfair Q2 Results Show Improving Trajectory

Wayfair ( W ) showed sequential improvement as it reaccelerated revenue growth and returned to free cash flow breakeven during the quarter. The company also showed confidence from debt holders as it successfully refinanced its long-term debt.

Wayfair Remains Unfavored by Many Investors

However, Wayfair continued to be unfavored by Seeking Alpha analysts as you can see we are the only one who gave out the buy rating despite that Wayfair stock was up 108% since our coverage.

Seeking Alpha

Meanwhile, according to Seeking Alpha, Wall Street maintained an average rating of buy for the stock. Short interest remained high at 24%. This indicated that there are certain degrees of divergence.

Seeking Alpha

Our Original Bull Thesis Remains Intact

Our original bull thesis has not changed. A couple of short-term catalysts continue to trend favorably toward our thesis including:

- BNPL Provides Boost Amid Lower Furniture Demand:

BNPL (Buy Now, Pay Later) allows consumers to purchase goods and services immediately and pay for them over an installment plan. BNPL providers partner with retailers to offer interest-free payment plans, typically over 4 payments over 6 weeks. Unlike credit cards, some BNPL providers earn revenue through merchant marketing fees instead of interest from consumers. This allows BNPL plans to offer 0% interest installment loans, making them an attractive payment option for consumers facing financial pressures in the high inflation economy.

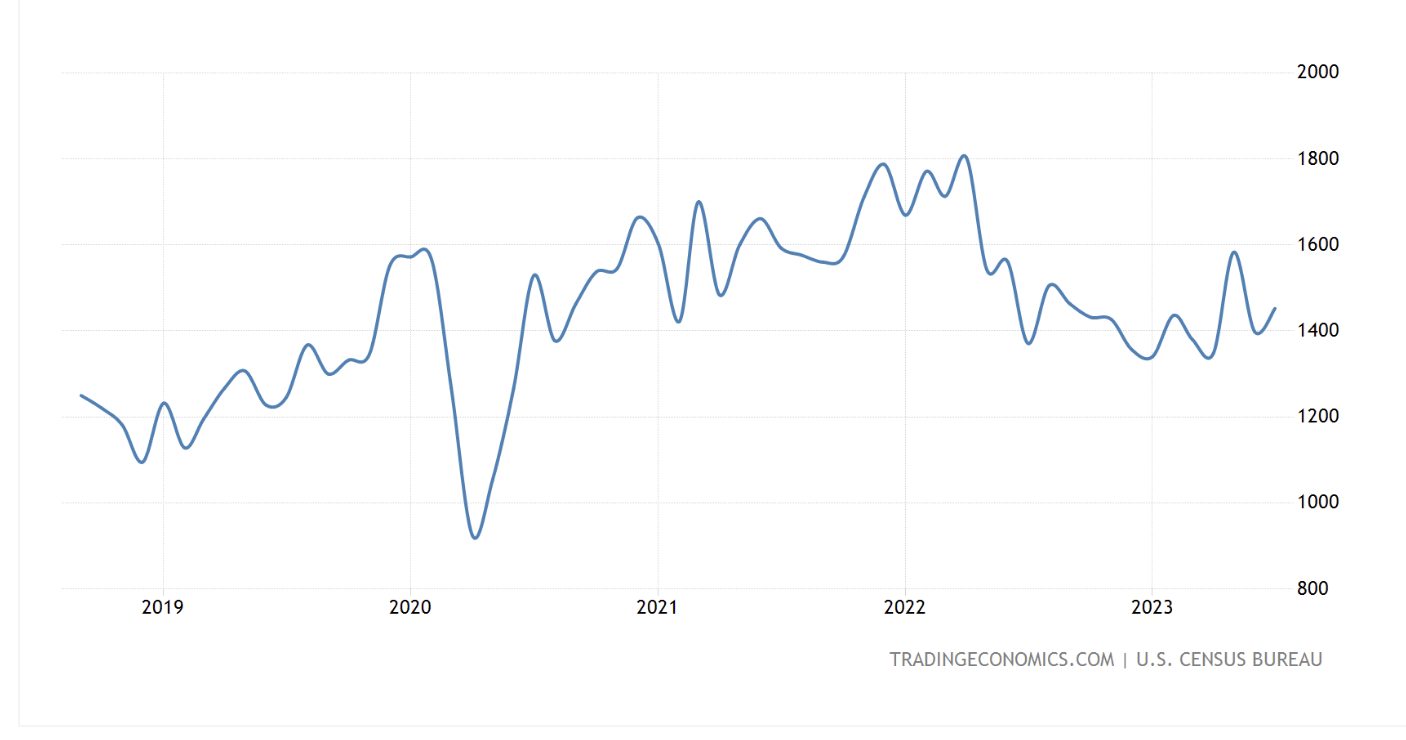

BNPL is likely a boost to mitigate demand lowered by weak furniture market demand as a result of higher interest rates and a high inflation environment. Wayfair partnered with major BNPL firms such as Klarna, Afterpay, Affirm, etc. The estimated value of the global buy now pay later market is $129.7 billion in 2022, and the market is anticipated to increase rapidly at a CAGR of 49.7% during the forecast period. For example, Affirm recently reported an impressive quarter as its GMV grew by 25% during the quarter. We think this trend is developing well as we expected as the BNPL firms don't rely on deposits to grow their loan assets, instead partnering with institutional investors to sell loans and focus on merchant ad dollars rather than post heavy interest loads on consumers, which is a great way to grow in this environment. - Bottom in Housing Starts Should Help Furniture Demand: US housing starts seemed to be bottoming out in 2023 based on government data. In addition, Warren Buffett initiated a position in real estate developers such as Lennar ( LEN ) sending a similar message.

{kind=link}

US housing starts: We think that as housing prices already rebounded from lows in 2023 to continue trending up, developers have more incentives to start new construction and this is likely to boost demand for furniture directly.

{kind=link}

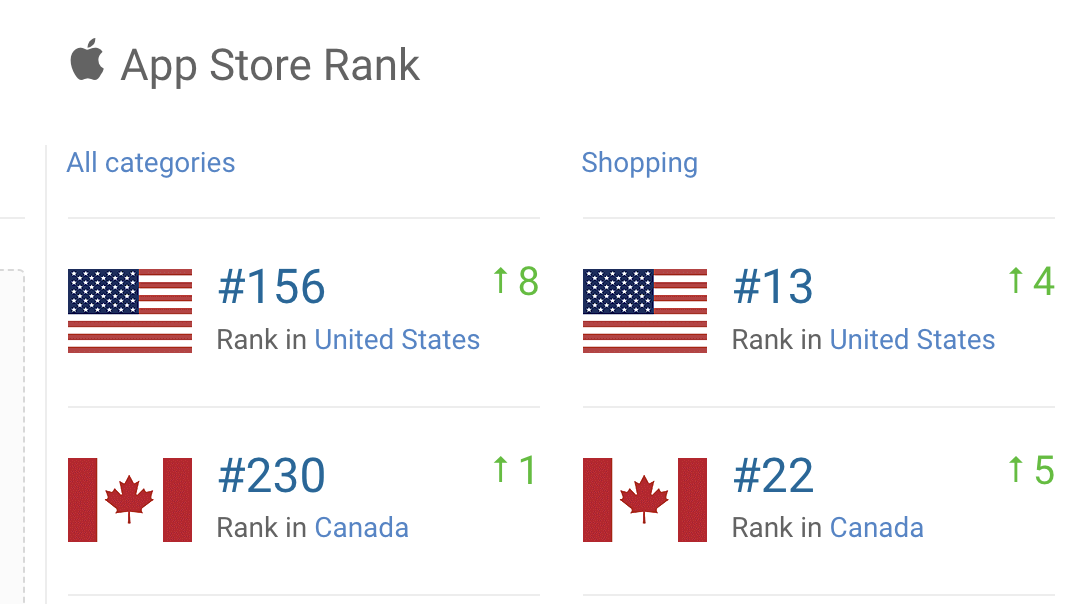

Wayfair Remains Competitive in Furniture Space

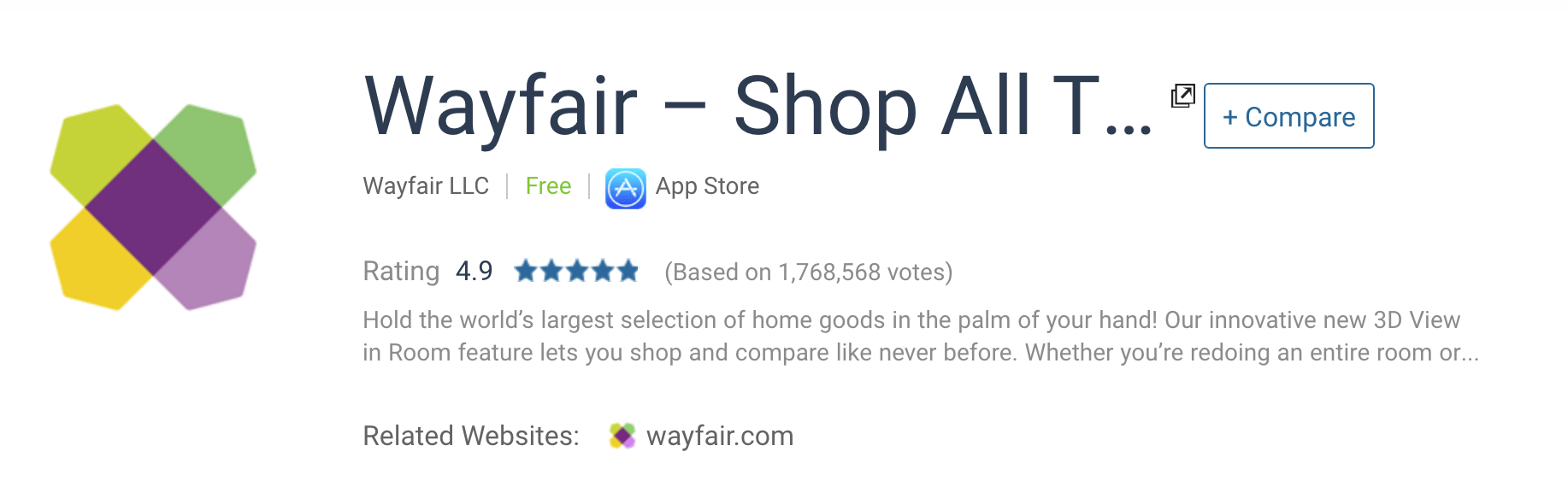

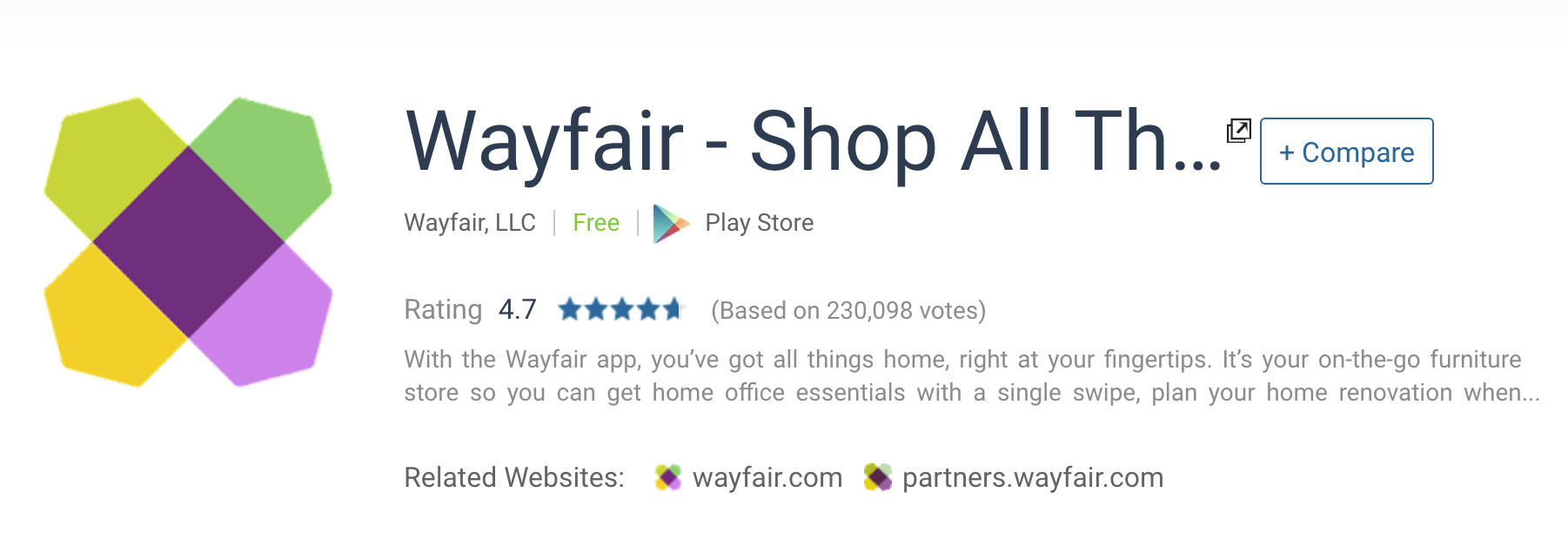

Regardless of the short-term catalysts, we like Wayfair for obvious reasons. It remained competitive in the furniture space. As evidenced by its high ratings and rankings in the iOS and Google stores, consumers love Wayfair.

Similiarweb Similiarweb Similiarweb Similiarweb

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Return to Positive Free Cash Flow Calms Bankruptcy Fears

The company's return to free cash flow positive is the first step to calming bear fears, as the company can now maintain operations without going bankrupt.

Long-Term Prospects Remain Bright Despite Lack of Profits

So what about the long-term prospects? Many skeptical investors also believe Wayfair is not a profitable company so they will never be profitable and the stock should fall to zero. We urge our investors to leave this wrong philosophy behind as this logic never works in stock analysis.

Improving Gross Margins Reflect Pricing Power

Contrary to many investors' belief that Wayfair is an unprofitable company due to furniture delivery being a stupid idea, we think that as consumers love it and the company has demonstrated pricing power against consumers, long term the model will work.

First off, Wayfair showed better gross margins, going from 23% in 2018 to somewhat lower in 2021-2022, then returning to 31% in Q2 2023, despite ups and downs throughout COVID and following an increase in inflation.

Annual gross margin (Gurufocus) Quarterly gross margin (Gurufocus)

Its shipping and fulfillment costs are also included in COGS. The upward trends in gross margin show that Wayfair has been strengthening its negotiating position with customers.

Operating costs can leverage

Its operating costs such as customer service and operations team expenses are mostly fixed in nature and can be leveraged as Wayfair increases its topline. Its quarterly operating margin also showed sequential improvement.

Gurufocus

As the furniture market is relatively fragmented and transacts mostly offline, Wayfair as the leader in online space does not have many strong competitors.

Dominant position online

As Wayfair once again proved they can maintain free cash flow improving to breakeven under the online furniture model, they will continue to dominate this space for a while. Its US market share is only 4% in 2022. We think they are well positioned to grab more share long term.

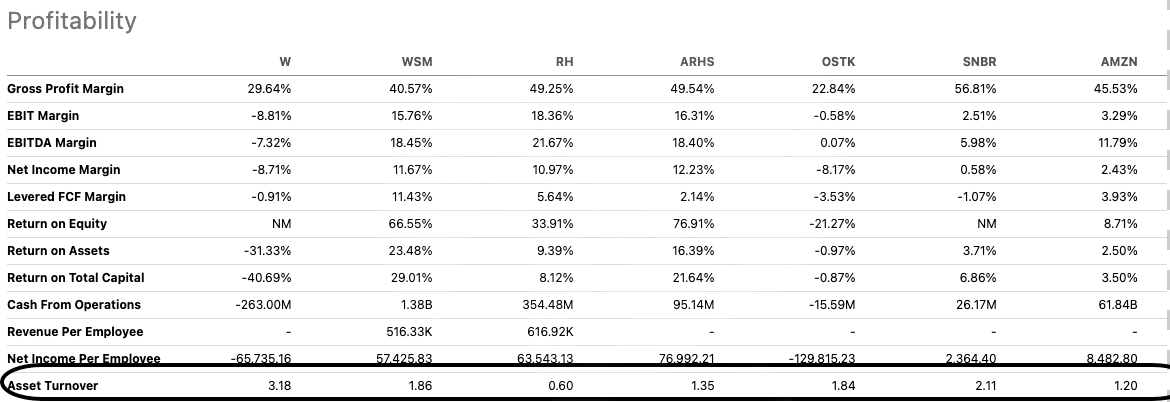

Superior Asset Turnover Showcases Advantages of Model

Wayfair's online business model is also highly competitive in its asset turnover capability. Its asset turnover of 3x is significantly higher than Amazon's ( AMZN ) 1.2x and also much higher than furniture peers such as Williams-Sonoma ( WSM ) at 1.86x or RH ( RH ) at 0.8x. This showcases Wayfair's model can actually sell furniture at a much faster rate than traditional retailers.

{kind=link}

We attribute this to (1) lower pricing as a result of the online and lean inventory model. As consumers build trust with the company, Wayfair's advantage of product assortment will be its competitive advantage over furniture peers. (2) Its dedication to the furniture category makes it the first recall for consumers when shopping for similar price ranges or style furniture over Amazon. Amazon has a large customer base and holds a strong competitive advantage in terms of customer base. However, Amazon is more like a marketplace best suited for consumers who have specific shopping categories in mind rather than a pure search engine. Wayfair's positioning as furniture only is likely to gain some advantage over Amazon when consumers choose which app to open first when they are ready to shop. As they both operate as free cash flow-positive companies, they are not necessarily zero-sum competitors. We think Wayfair is likely to continue to grow regardless of competition from Amazon or other peers.

Return to Growth is a Bull Case Catalyst

Wayfair's stock price remains range-bound around our original price target of $76, which is exactly as we expected. Our $76 target price was established based on the gloomy assumption that the company will only experience future growth at the rate of inflation.

Please refer to our original discounted cash flow model for the detailed assumptions. One of the key assumptions we are monitoring is whether they can return to growth in 2023.

{kind=link}

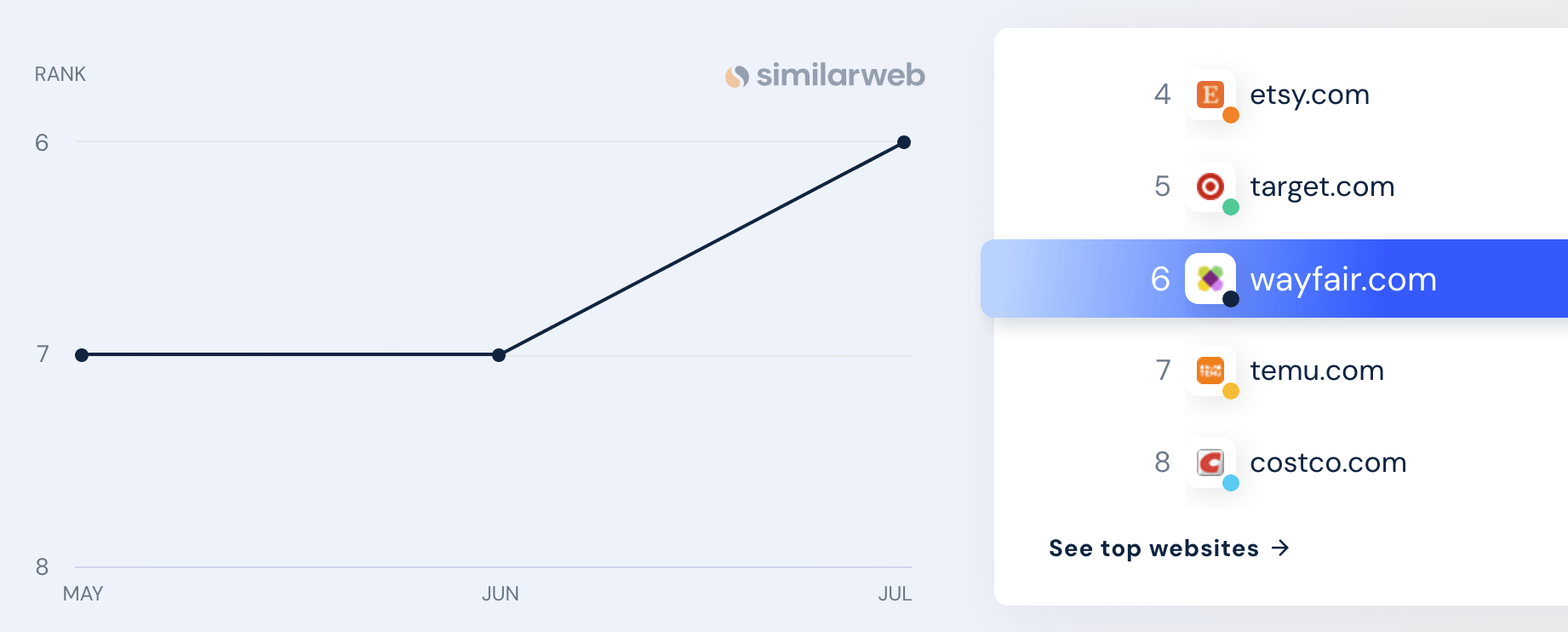

As the company guided a return to growth in Q3, we see the bull case playing out.

Quarter-to-date gross revenue has been trending positive low single digits year-over-year.

This can also be supported by recent traffic trends from Similiarweb.

{kind=link}

Thus, although the stock pulled back from its recent high of $84, we are buying more as we raise our target price from our base case of $76 to $95. We established a $95 price target in our previous article by considering our expectation for long-term market penetration to rise from 4% to 10%.

Compared to large techs such as Google ( GOOG ) or Amazon, which are monitored by many investors, Wayfair's stock is slower to react to the market. However, we think the upside potential is attractive and evidently to institutional investors, and as a result, we expect the stock is likely to be repriced very soon. We think short term, the stock is also likely to get a nice short squeeze, although we don't base our investment on other participants' behavior. As a result of the improving real estate environment and the company's return to growth, we have more visibility on the company's trajectory in the short to midterm, so we are raising our rating to Strong Buy.

Risk

Our premise was founded on two main points: (1) short-term catalysts for the housing market's revival; and (2) the model's long-term competitiveness. There can be no guarantee that the Fed will stop raising rates even though its rate strategy has caused the housing market to cool off, especially given that the price of oil has lately increased. The housing market may experience greater downward pressure if the Fed decides to raise interest rates further rather than keeping them at their current level. As a result, Wayfair may see broad headwinds that slow down its rate of expansion.

Furthermore, even though Wayfair's gross margin continued to rise, the company still has to increase its market share in the US and abroad in order to better leverage its operating expenses to increase profits and demonstrate that its business model is actually very competitive. Therefore, if progress on this project is delayed, the stock may see further downward pressure. We urge investors who are interested in the stock to monitor these factors going forward.

For further details see:

Wayfair Returned To Growth (Upgrade)