W - Wayfair's Marketplace Model: Unleashing Long-Term Potential

2023-11-03 01:58:43 ET

Summary

- The stock has gone up 38% since our initial coverage in May 2023.

- The company's recovery trajectory indicates strengthening fundamentals and potential for further upside.

- Wayfair is building a strong business on the marketplace model, a transforming force that is seen as having long-term potential and advantages over traditional retail models.

- Wayfair’s revenue performance has been more resilient compared to luxury furniture sellers RH and Williams-Sonoma.

Earnings Overview and Market Response

Wayfair (W) reported Q3 earnings this week that beat analyst estimates, sending the stock up 4%. The company showed signs of overcoming macroeconomic headwinds, with revenue growing 3.7% year-over-year despite ongoing housing market weakness. The stock has pulled back from its August high by 43% but still has gone up 38% since our initial coverage in May 2023.

This marks a couple of straight quarters of sequential revenue and gross margin improvement after bottoming out in 2022. The data indicates that demand has stabilized as the impact of interest rate hikes diminishes.

Management struck an optimistic tone on the earnings call. With free cash flow turning positive again, Wayfair is ready to reinvest in growth initiatives. This should further boost revenue and instill confidence that the company has passed the trough.

Though housing market challenges persist, Wayfair seems to be adjusting well. Its recovery trajectory points to strengthening fundamentals. If the company can sustain this momentum, its stock may have additional upside from current levels.

"Wayfair is now in a place where we can drive profitability while simultaneously investing for growth," said Niraj Shah CEO

While Wayfair grew its number of orders in Q3, its average order value declined from $325 to $297. This indicates customers are purchasing more frequently but spending less per order. Despite flat customer growth, higher engagement is a positive sign.

Benchmarked against industry peers, Wayfair's topline has been resilient. In Q2, luxury furniture sellers RH (RH) and Williams-Sonoma (WSM) saw revenues decline by 20% and 23% respectively, while Wayfair dropped just 3%. The fact that Wayfair excels among its competitors, catering to the broader consumer base, further underscores its robust performance.

Additionally, management guided to continued sequential improvement in profitability in Q4. This eases concerns about long-term margin potential, as it demonstrates Wayfair has not hit a plateau. Ongoing margin expansion should bolster confidence in the earnings growth story.

Underestimated Marketplace Model

A key aspect we're monitoring is Wayfair's evolution toward a marketplace model. Despite e-commerce's growth, the potential of online marketplaces remains underappreciated.

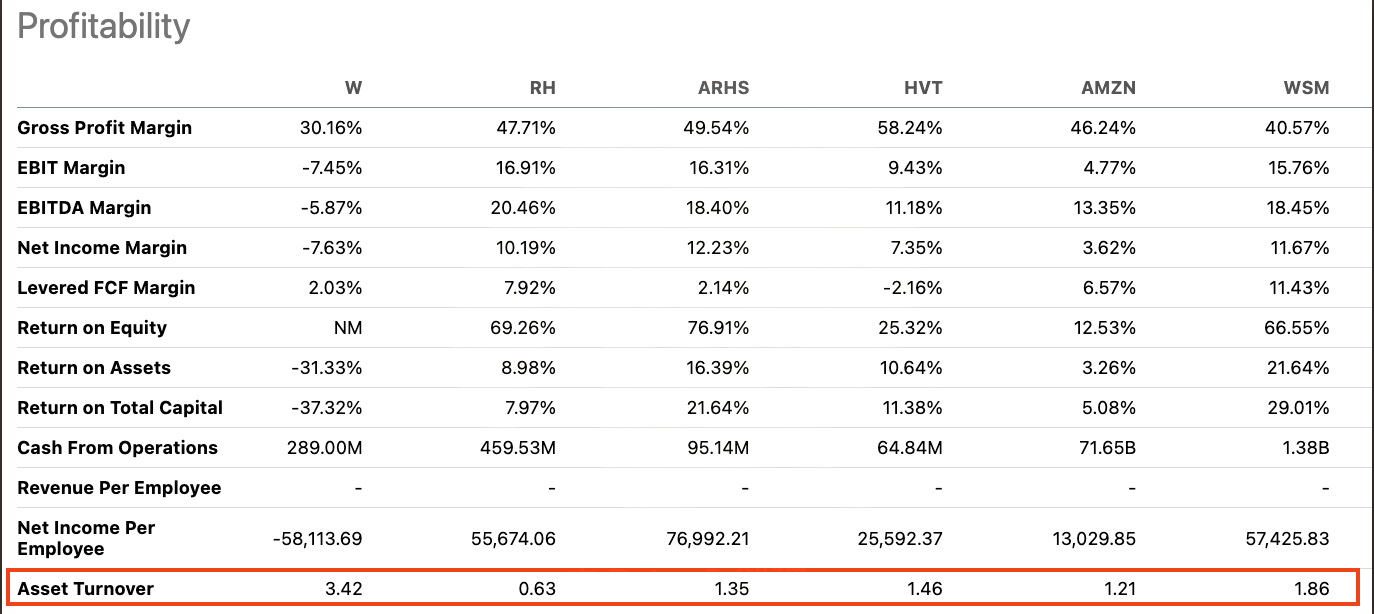

We believe asset-light marketplaces will become the dominant retail model long-term. Wayfair's asset turnover already far outpaces traditional retailers that hold inventory.

{kind=link}

It's important to differentiate between e-commerce and online marketplaces.

Take Amazon ( AMZN ) for example, Amazon started as a traditional retailer model that holds inventory and sells goods online. However, in recent years, Amazon started to shift its business mix more toward the marketplace model, indicated by the below chart that its third-party seller unit mix percentage continued to increase from 2020 to 2023.

Third party seller unit mix % of total (AMZN)

{kind=link}

Advantages of the Marketplace Model

The advantage of the marketplace is obvious. First, Amazon can increase revenue streams such as third-party seller services (shipping, etc) and advertising services. In fact, we see these two business streams are growing at a strong double-digit rate and become a core contribution to Amazon's retail growth in recent years. The additional revenue streams can further fuel more promotional room for Amazon to gain market share in events such as Prime Day or Black Friday, thus securing its cost advantage.

Second, the marketplace offloads the inventory burden of the retailer. The question investors should think about is first why do retailers hold inventory in the first place? Because in the traditional retailer model, it is very hard to track the performance and consumer feedback of suppliers of the retailers. For instance, a supplier in China should have a hard time understanding how their products perform in Walmart's retail locations in Minnesota. It's just too hard to track the sales and adjust production based on consumer feedback in the traditional model. That's one of the main reasons retailers bought out the inventory in the first place.

However, the emergence of e-commerce has solved this issue as now consumer footprints are traceable in real-time. Hence, the emergence of the marketplace is the revolution of the retailer model as now the retailer doesn't need to carry the inventory. Suppliers of retailers can trace everything through the marketplace platform and adjust their product strategy and inventory levels in real-time. As consumers are now more comfortable buying things online, the marketplace model saves friction costs through the value chain by connecting consumers with suppliers directly. This cost reduction will enhance the competitive advantage of the marketplace compared to traditional retailers over time. Hence, we are very optimistic about the long-term opportunity of Wayfair's marketplace model.

Valuation

Our $95 price target for Wayfair remains unchanged based on the DCF model. This target indicates significant upside potential from current levels.

On a comparable basis, the market is still underestimating Wayfair's long-term marketplace potential, in our view. Profitability currently lags peers, but we see a runway for margins to expand well beyond current levels.

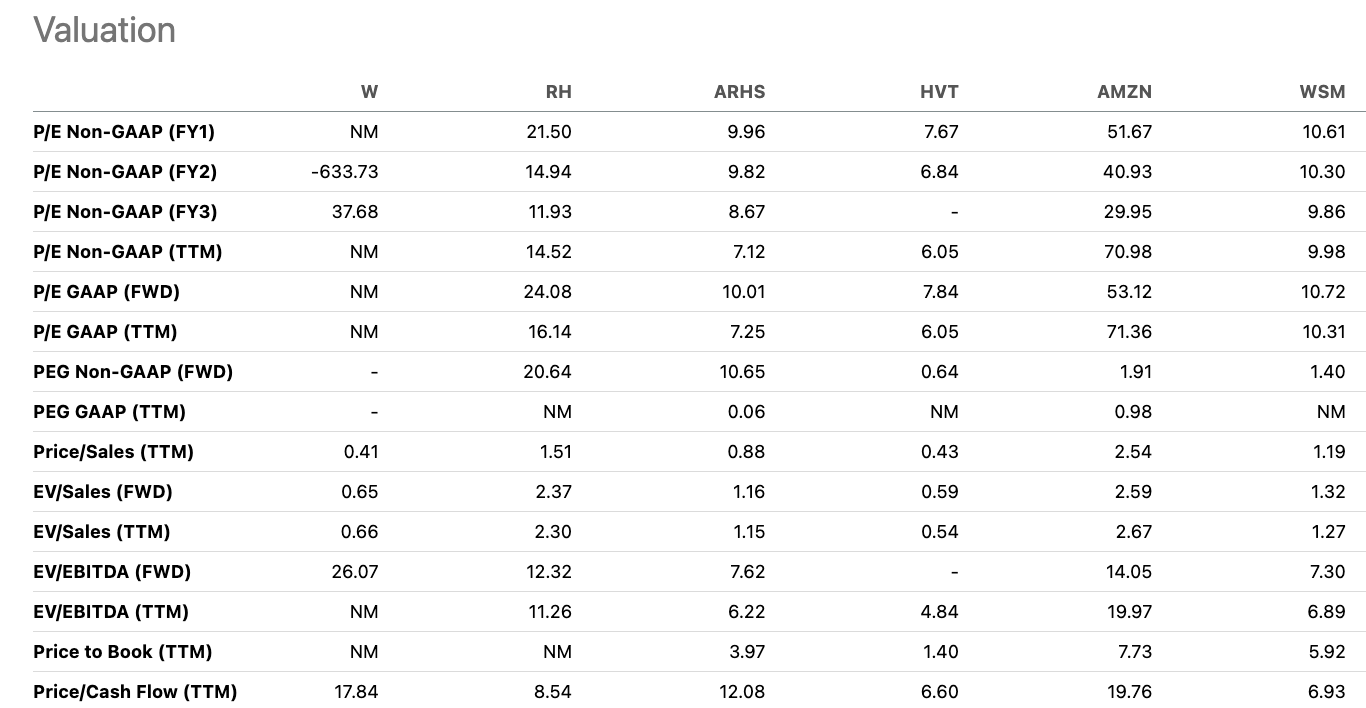

Additionally, the price/sales ratio of just 0.41x reflects an overly pessimistic outlook given Wayfair's resilient topline growth versus luxury furniture retailers.

{kind=link}

As Wayfair makes further progress on its marketplace transition and demonstrates operating leverage, we expect the valuation gap to close. Our analysis suggests sizable appreciation potential as the market recognizes Wayfair's strengths.

Competition and Brand Equity

Competition from Amazon is a common investor concern for Wayfair. However, we believe Wayfair has cultivated strong brand equity and network effects that defend its position.

With over 22 million active customers, Wayfair has around 6% household penetration in the U.S. and Canada. Given furniture is a lower-frequency purchase category, this level of penetration is quite solid.

Once a marketplace achieves critical mass, network effects help sustain organic growth. Wayfair's large customer base and order volume generate data that improve its service and selection - advantages a new entrant would struggle to match quickly.

Conclusion

Wayfair management has executed well and delivered on its commitments to regain revenue growth and expand margins. We remain confident in the company's ability to drive further profitability improvements in the years ahead.

Moreover, we believe the long-term growth potential of Wayfair's marketplace model is underestimated by the market. Despite significant macro headwinds, Wayfair continues gaining market share - a testament to the strength of its platform.

While inflation has weighed on sentiment recently, we believe current challenges are transitory. As the headwinds abate, Wayfair's strong competitive positioning and resilient model should drive a rebound.

Given the attractive valuation and long runway for growth from its early-stage marketplace, we reiterate our Strong Buy rating on Wayfair. The company's fundamentals remain strong, and we see significant upside for patient investors at current levels.

For further details see:

Wayfair's Marketplace Model: Unleashing Long-Term Potential