XLU - WEC Energy Group: An Attractive Name For The Long Term

Summary

- Nothing is certain in life except death and taxes, but also recessions.

- Given the aggressive Fed, most anticipate a recession in 2023 that can make defensive sectors relatively attractive.

- Since most anticipate this already, most utilities are still trading at some elevated valuations - sticking with quality like WEC Energy Group, Inc. can still provide long-term success.

Written by Nick Ackerman. A version of this article was published to members of Cash Builder Opportunities on December 26th, 2022.

Utilities have been flirting back and forth in the prior year between losses and gains. Eventually, the SPDR Utilities Sector ( XLU ) showed slight losses for 2022, but positive total return results. With an anticipated recession this year, utilities are a common area investors can crowd into. Therefore, it makes sense that utilities have been getting a lot of love.

That can leave little room for investors to get into these defensive names now that they are crowded. I think that's why it could make sense to stick with higher-quality utilities that could still see some longer-term performance despite the higher sector valuation. Besides, a good utility play in your portfolio can always be welcomed. The only thing certain in life is death and taxes - but also recessions. They are always only a matter of time.

WEC Energy Group, Inc. ( WEC ) is a name that comes to mind. Even better, while the sector might be overvalued according to historical P/E ratios - and even more expensive than the S&P 500 based on P/E - WEC is much closer to trade near fair value. In fact, some estimates project that there could even be some upside from here.

They are a multi-utility company with operations in both electricity and gas distribution. They operate through several subsidiaries, with businesses in Michigan, Wisconsin, Minnesota, and Illinois.

WEC Group (WEC Energy)

Quick Look At Performance

Below is the YTD performance of WEC relative to XLU.

Ycharts

The last time we touched on WEC, they were in a pullback. At that time, I felt there was some good potential there. Since then, WEC has performed well. I'd say exceptionally well on a relative basis to the broader market.

WEC Performance Since Prior Update (Seeking Alpha)

While we recently missed another attractive dip, there could be some potential upside even from here. More patient investors could wait for that next inevitable dip.

Valuation And Upside

As we saw above, WEC has made some big moves higher since our last update. I think it remains a "Buy," even here, but admittedly, less tempting than it was previously. On the other hand, over a longer period of several years of the stock moving sideways, the earnings have started to catch up.

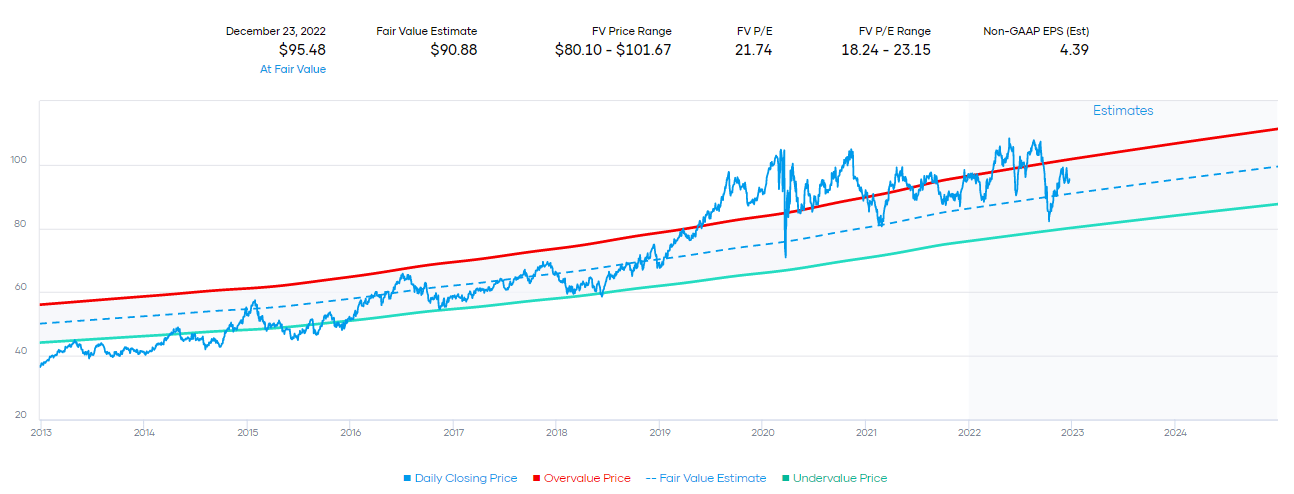

What I mean by that is WEC's fair value estimate historical P/E chart shows us that in 2019 through around 2021, WEC was trading at an overvalued level. Based on that metric, we can see that we are back in the fair value range channel.

{kind=link}

The fair value above on P/E fair value puts the shares at $90.88, a bit lower than where we are right now. However, considering other factors, such as the dividend yield history and analysts' consensus estimates, we get a different figure at just over $100 or a 1-year target price of ~$101.

WEC Price Target (Portfolio Insight)

In that case, we can see some upside potential.

Growing Earnings

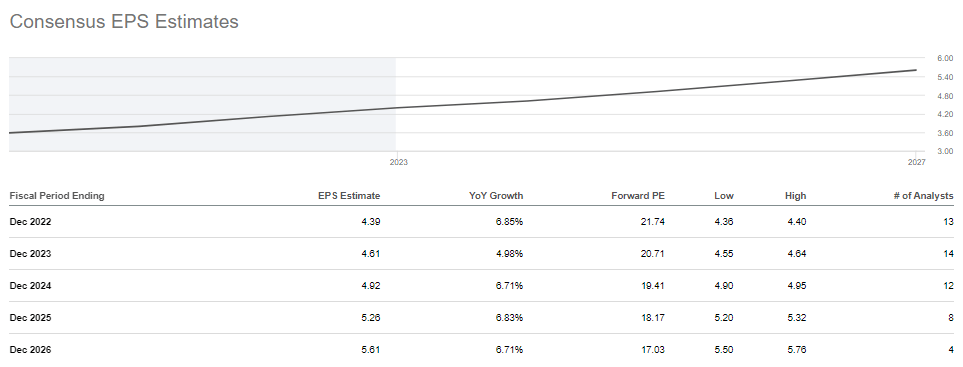

One of the reasons for the upside potential going forward is earnings growing. That's about as basic as we can get for investing, which is a reason why utilities can be such an amazing investment. They are predictable and super simple to understand. Analysts expect WEC to be able to deliver anywhere from around 5% to 7% in earnings in the next five years.

{kind=link}

If EPS rises over time, eventually, investors should be able also to get a rising share price. A rising share price isn't always an important factor for investing, but it can help longer-term income investors. With lower yielders such as WEC, I would anticipate the upside being an important part of returns and dividend growth, too, of course.

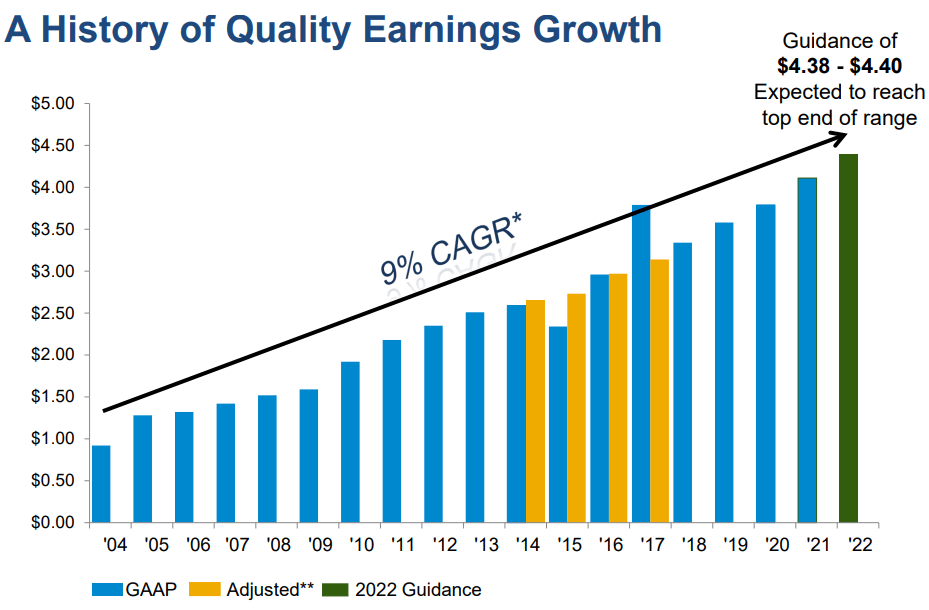

The earnings growth above is encouraging, but WEC has an even more impressive track record than is suggested above. They've provided a CAGR of GAAP EPS of 9%.

{kind=link}

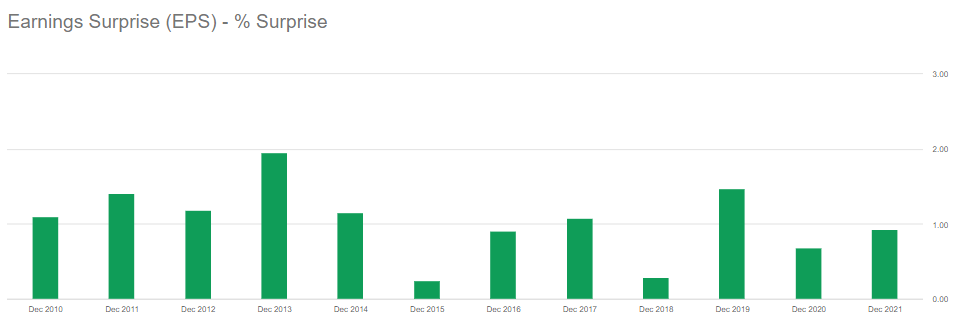

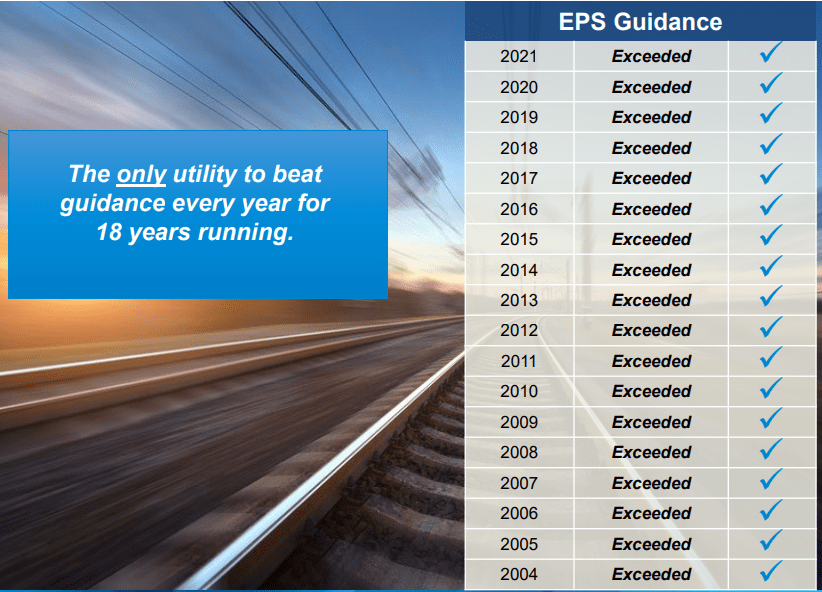

They recently updated guidance for 2023 of EPS between $4.58 and $4.61. That's right where analysts were expecting. Except, they have a history of exceeding analysts and exceeding their own guidance. They've surpassed analyst expectations for the last eleven years running.

{kind=link}

That's as far back as the data on Seeking Alpha shows. When looking at WEC's guidance, they've exceeded their guidance 18 years in a row now.

{kind=link}

Suffice it to say that $4.58 to $4.61 is almost assuredly conservative guidance that they will ultimately beat.

Dividend On Target And Growing

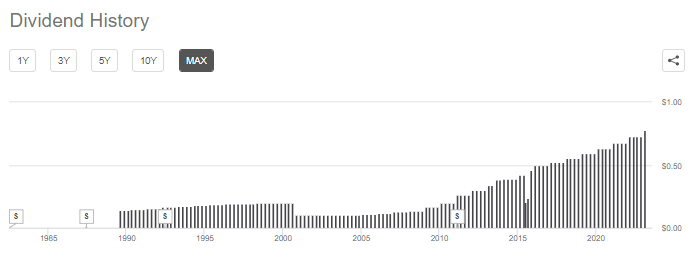

As those earnings grow, so do the dividends. That's ultimately why I invest in WEC in the first place. The consistency that it can deliver in earnings produce consistent dividend boosts. The latest was a strong 7.2% increase, going from $0.7275 to $0.78 per share a quarter. This puts the current dividend yield around 3.27%. That will also bring them to 20 years worth of increasing dividends - barring a cut in the coming year.

{kind=link}

They target a payout ratio of 65 to 70% of earnings. Being in that range currently means that dividend growth should follow along with EPS growth going forward. They expect longer-term EPS growth to be in the range of 6.5 to 7% annually through 2027.

Renewable Push

Like most utilities, most of their CAPEX going forward will be dedicated to renewables. This is either by choice or force through regulations. However, that isn't all bad news for utility companies. They are finding ways to deal with this, and some are taking this transition well, such as WEC or NextEra Energy ( NEE ). Then others haven't been able to deliver this transition as smoothly, such as Dominion Energy ( D ). At least as far as share prices are concerned.

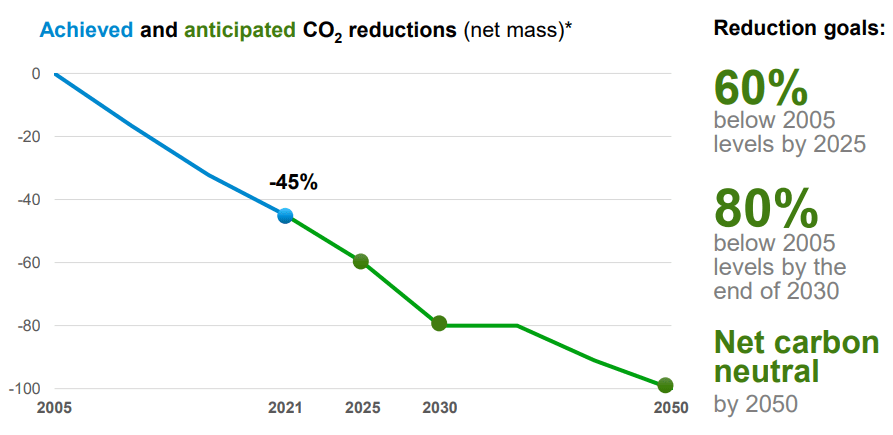

Their goal is to retire their coal plants. They have retirements planned on three different units in the next few years. By the end of 2030, they anticipate that coal will only be a backup fuel. The ultimate goal is to eliminate coal as an energy source by the end of 2035. Eventually, being net carbon neutral by 2050.

{kind=link}

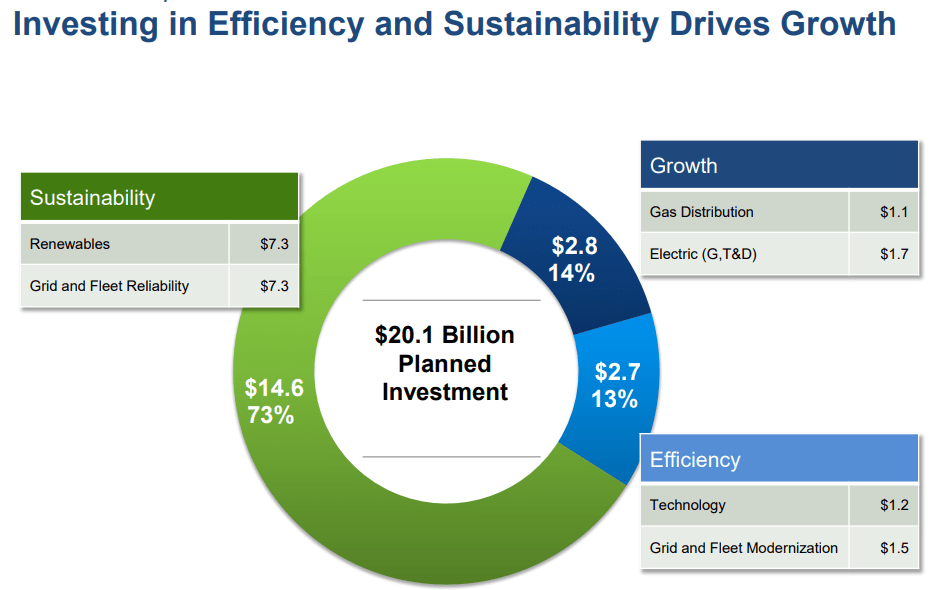

They are looking to invest $5.4 billion in regulated renewables from 2023 through 2027 or $7.3 billion in all renewables. In total, that's around 27% to 36% of their planned $20.1 billion in CAPEX planned. This was an upped amount of CAPEX that was announced in their last earnings as well .

That's more than 13.5% above our previous 5-year plan. Now as we look forward, I will describe our growth trajectory as long and strong. In fact, our plan will now support compound earnings growth of 6.5% to 7% a year over the next 5 years without any need to issue equity. And as you've come to expect from us, this projected earnings growth will be of very high quality.

Highlights of the plan include a significant increase in renewable energy projects for our regulated utilities from roughly 2,400 megawatts of capacity in our previous plan to nearly 3,300 megawatts in this plan. And as we continue to decarbonize our system, it's important to point out that passage of the Inflation Reduction Act is a real true game changer for customer affordability.

{kind=link}

I think their goals represent realistic expectations. Long enough transition time to ensure that consumers won't be left cold in the winter.

Risks to the transition would be construction costs. As inflation is pushing up the cost of everything, it can take a larger and larger amount of capital to get the projects they've committed to up and running. There is always the risk that regulators get even more aggressive, pushing even more aggressive targets on utility companies.

Conclusion

WEC Energy Group, Inc. has moved up quite a bit since our last update. That is particularly true when looking relative to the broader markets. While I think it remains a "Buy," I'm obviously not as enthusiastic if you have a shorter-term time frame. On the other hand, with a potential recession in 2023, utilities can still provide a defensive tilt that investors cling to. I think buying for the longer term a quality utility company makes a lot of sense, and that would be more of my main focus here for WEC Energy Group, Inc.

For further details see:

WEC Energy Group: An Attractive Name For The Long Term