ACTV - Week On Wall Street: Caution Yes Panic No

2023-04-29 07:43:10 ET

Summary

- The bulls look to Corporate America and earnings to keep the economy stable. After a slow start, this earnings season is not as bad as feared.

- In the short term, the "glass is half full", but it's more of a "glass half empty" for the MARCO scene.

- China's recovery has just started and it can help to buoy the global economy.

- Q1 GDP is lower than expected and has the look of stagflation. Inflation remains stubbornly high and that keeps the Fed in the picture.

"Risk comes from not knowing what you're doing." - Warren Buffett

We've entered Q2, and the 2023 outlook has become less clear than it was at the beginning of the year. Inflation and the Fed remain center stage, but we've added more geopolitical turmoil and financial sector upset over a failure of bank management and financial regulators. I've already stated my base case on this situation. The turmoil we witnessed won't become a full-blown crisis, but that doesn't mean the markets will forget about what has occurred overnight. Investors will want to see stability return to regain confidence in the system. It's still early but so far that assessment has been correct. We have plenty of history where small problems in the financial sector can morph into larger issues that spread like a virus. The latest data released by the Federal Reserve on Friday, April 14, indicated that total deposit balances increased by 0.2% for the large banks and up 0.4% for the small banks. So the thought of 'bank runs" should no longer be part of the conversation.

In the recent case, it's the smaller regional banks that were guilty, and they simply don't represent the risk that we saw with the larger institutions in 2008. Let's not forget that the assets that have fallen in value, and are at the root of the problem are US Treasuries. In summary, it is a LOW probability that this will morph into a global crisis because this damage is manageable, and that is why the stock market is rallying despite this event. However, this event should keep a cap on the entire financial sector, so in the near term, we can rule out the group playing a key role in any rally.

We are now squarely entrenched in the "New Era" market environment, where the easy peaceful days are over. I expect volatility - across most markets - will remain higher than we enjoyed during the easy money days of the past. We have seen the market move from a "glass half empty" (October lows) to a "glass half full" (recent rally) mindset. I like to characterize this action as a market that at one point realizes its "Higher for Longer', and then starts to embrace the notion of the Fed cutting rates in '23. I won't bet the farm on anything the Fed is forecasting BUT remember their latest commentary;

A recession to begin this year with rapidly lower inflation next year - their inflation estimate drops to 2% by year-end 2024."

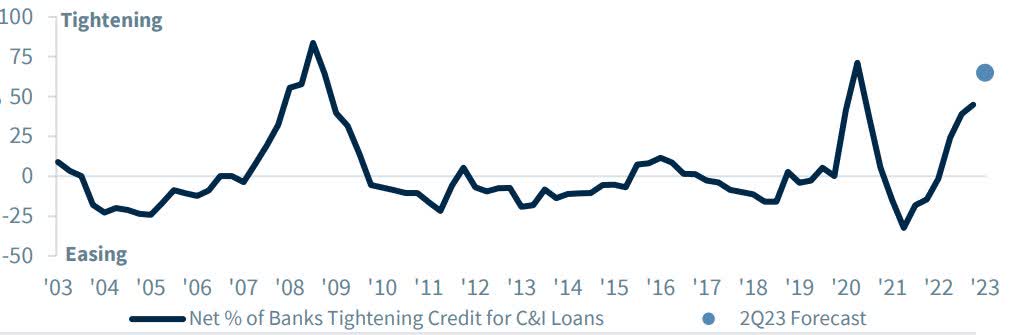

That tells me when the "glass is half full" mentality is present it's ignoring the Fed's forecast entirely. This strategy can lead to the biggest disappointments because whether one agrees with them or not, the Fed controls how long rates will remain elevated. Not to mention we are already seeing the unintended consequences of irresponsibility shown in the California Bank problems. The Federal Reserve's Senior Loan Officer Survey on bank lending practices shows a significant number of banks have steadily tightened credit

{kind=link}

We've seen this occur before -- right before a recession.

While many have declared victory over inflation given that the rate of inflation has been coming down, that has also come at a time when energy and agricultural commodity prices have mostly been going down. And yet even with that helping to ease costs, prices have still been going up at a clip well above the Fed's target. If we start to see oil/gas and food inputs like wheat, corn, and soybeans once more become larger contributors to inflation, that may put a damper on the market's view that we may just have one more hike before the much-anticipated "pause."

Since the onset of this BEAR market, we have never had to contend with this exact combination of risk factors before. I believe the change in sentiment and volatility we have witnessed in both the stock, bond, and commodity markets over the past year all derives from the unsettling fact that NO ONE has a solid idea of what is going to happen in the next few months. Even if they do have a sense of how the markets might react, it is obvious they don't have any conviction behind their approach. Investors should be prepared for anything, and for some, that is very stressful.

Macro Risk Factors

Employment Scene

While job growth remains resilient, economic undertones suggest that employment gains are starting to fade. For example, withholding tax collections are slowing, large-cap tech companies (i.e., Amazon, Meta, Google) are announcing layoffs and now we see companies like GM, Walmart, and Disney joining this scene. If this forecast comes to pass, It will be the beginning of the "other shoe" dropping. How fast unemployment rises and consumer spending slows will determine the onset and depth of any recession. With the S&P hovering around the 4200 level, I'm not sure the stock market has priced any recession in.

Political

This an ever-present risk, but with the debt ceiling debate ahead of us, the risk to US sovereign creditworthiness as a result of political shenanigans will increase in the months ahead. It is something that will eventually fade into the sunset, but investors need to be aware of the near-term effect on the markets.

Speaker McCarthy (R-CA) made a speech at the NYSE claiming he has 218 votes for a plan to raise the debt limit for 1 year if coupled with cutting federal spending to 2022 levels and capping spending growth at 1% per year for the next decade while imposing work requirements on government aid recipients and oil & gas subsidies. The proposals also include energy, and permitting legislation, and the repeal of several Biden administration priorities. (including student debt relief, green energy tax credits, and boosts to IRS funding).

It turned out to be more than a "claim" as the House voted and passed a bill to raise the debt limit and rein in spending. To describe that slate as a non-starter and DOA in the Senate and White House is an understatement; we are still in the "jockeying for position" phase of this particular policy fight and will be for some time to come it seems. There is still substantial room for negotiation before "extraordinary measures" run out and force an outright default. However, there hasn't been any negotiation since this issue presented itself earlier in the year.

Goldman Sachs is forecasting the US could hit the Debt ceiling as early as mid-June. Goldman explains that tax receipts were down 29 percent for April and the main culprit was lower capital gains taxes. The wealth effect took a hit last year in the form of a BEAR market in stocks some say the stock market doesn't matter because only the wealthy benefit and the wealth effect isn't as important as some make it out to be. Those same folks now realize their government "income" was just taken down a notch, and the wealth effect does matter.

We can expect this issue to go down to the 11th hour. I never make this issue an "actionable" item but I make sure my seat belt is fastened tightly.

Geopolitical

Russia/Ukraine continues and while it is not market-affecting, it is yet another situation that demands monetary support from the U.S. By itself, it is a situation that the US can deal with BUT there is potential for further entanglement given the tensions between China and Taiwan. First, let me establish that I have no idea what is going to happen between China, Taiwan, and the United States. It seems war is certainly a possibility at some point but "war" can also mean many different things.

There are degrees to war and how it would play out is going to affect the potential financial market impact. I'm also not going to get into the "what-if" game, because most of what we conjure up never happens, and it's a never-ending situation. I'm not an automatic "seller" of the market when it comes to any "conflict". But rest assured the markets are always "sell first", then assess the situation. Similar to Russia/ Ukraine there could be opportunities presented.

It's being mentioned now because it is part of the MACRO scene that all investors need to be aware of. If you are TRULY worried, then the first thing I would do is try to directly avoid investing in companies that do a lot of business with China, particularly those with an abundance of sales from there. That in itself is a huge task and a BIG decision because there are plenty of big-name U.S. stocks with deep roots in China.

Being reliant on China for sales/revenue and important inputs will be extremely risky for any company if there are significant disruptions. Yet, that also means that some domestic companies could benefit from the "reshoring" as manufacturing and other inputs are switched back to the U.S. War is not always 100% "bad" in terms of the financial markets.

I don't plan on treating this "what if' situation any differently from others. I will continue to trade and invest the same way I always do. That includes my Chinese holdings. I do expect big Tech companies would be disproportionately hurt by any sort of loss of business with China, and the indices could take a large hit as a result, given their weighting. Ironically, many investors shy away from Chinese equities because of the perceived "risk". I can assure you favorites like Starbucks ( SBUX ), Nike (NKE), Apple ( AAPL ), et al will get obliterated if the "what-if" becomes reality.

Any conflict with China could be an event that impacts the MACRO scene for quite some time. However, I don't think it's smart to just wildly bet on that happening either.

Summary

There are major issues present in the economy that will continue to affect the MACRO view. Analysts and investors are still wondering if the S&P will revisit the October lows. There is enough evidence to suggest that we have to keep it on the radar as a probability, but I'm not going to worry about that possibility today. The same goes for the recession/no recession debate. We can waste plenty of energy being overly concerned about issues we can't control.

My expectation of a sustained period of below-trend growth , driven by some combination of tight monetary policy and anti-business sentiment with a mild dose of banking sector distress, argues for caution, but no panic. Corporate America continues to provide the growth that investors are looking for. How long they can keep that going given the challenging MACRO economic backdrop remains to be seen. The one issue that goes a long way in offsetting some of the negatives was the change in Congress that has for the moment neutered the "tax and spend" regime.

Global Scene

Europe has successfully navigated its energy crisis, thanks to a warm winter and its unprecedented shift away from Russian natural gas. Lower fuel prices have helped households maintain spending levels even as higher interest rates have begun to have an impact. That is an issue I and many other analysts did not factor in and why I missed the recovery in the EU markets. But its recovery must now survive tighter monetary policy as European Central Bankers focus on stubbornly elevated inflation and a tight labor market. Higher rates, tightening lending standards, and a housing downturn may expose financial vulnerabilities.

The probability of a recession in Europe and the US remains HIGH. History suggests that US-based companies are more adept at navigating slowdowns. Therefore, despite the analyst's calls to increase EU exposure, I still prefer the US over developed international markets. Emerging market equities are a different story. China is in the first inning of its post-COVID reopening, and the potential for robust growth still exists. Their economy is just now beginning to accelerate, and the probability is HIGH that it continues to improve well into 2024. China is also in excellent shape when it comes to inflation. The acceleration will nonetheless be an important source of support for the global economy in these challenging times.

Finally, higher oil prices will benefit Latin American indices.

The Week On Wall Street

The trend of tight trading ranges and light volume spilled over to this week. The S&P rose 3 points on Monday in what I described as watching paint dry. Coming into Tuesday, the S&P had traded in a sideways range for 15 days gaining all of 13 points. That was giving the appearance of a market that was coiled for a strong move in either direction. When the dust settled on Tuesday the initial move was a break lower. It was a sea of red as every index and all eleven sectors were sold. The S&P 500 shed 1.8%, the Russell 2000 lost 2.4%, and the NASDAQ gave back 2%. Eight sectors lost more than 1%, and six of those had losses greater than 1.5%.

That weakness bled over to the Wednesday session with all of the major indices posting losses except the NASDAQ. Big tech earnings had come to the rescue for the technology sector ( XLK ) as the group was the only one posting a gain on Wednesday. It sure appeared the rebound rally was slipping away.

More positive earnings reports and the buyers re-emerged on Thursday. The BEARS fumbled the previous day's opportunity and it was off to the races. The S&P added 2% and the NASDAQ added another 2.4% to its weekly gains, and even a discouraging PCE inflation report couldn't keep the buyers at bay.

Except for the Russell 2000, all of the indices posted gains for the week. The BEARS wondered how they let an opportunity slip away, while the BULLS were caught smiling heading into the weekend.

The Economy

Q1 GDP posted a 1.1% growth rate, weaker than expected, versus 2.6% in Q4 and 3.2% in Q3. The core PCE rate accelerated to 4.9% from 4.4% and is the highest since the 5.6% climb in Q1 2022. The latter is not good news in the inflation fight. Business investment cratered in Q1 and overall the report had all the earmarks of "stagflation".

This GDP print is much more in line with my expectations. I continue to see subpar growth going forward, eventually morphing back into negative prints as we saw in Q1 and Q2, 2022.

Inflation

The Fed's key metric to measure inflation - PCE continues to show stubborn inflation embedded in the economy. Excluding food and energy, the PCE price index increased 4.6 percent from one year ago. No change from February.

Manufacturing

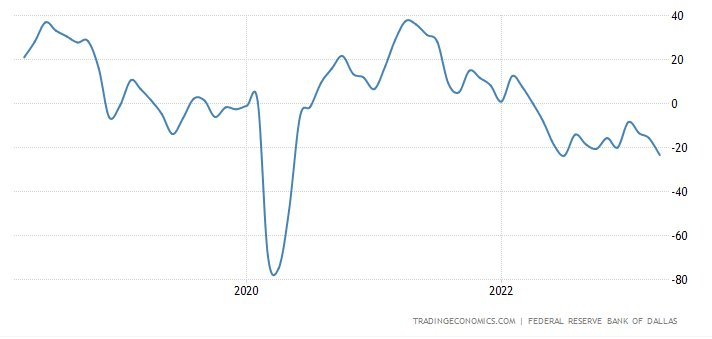

The Dallas Fed headline index plunged to a 9-month low of -23.4 in April from -15.7 leaving that measure just above the 2-year low of -23.7 in July of 2022. The components were stronger than the headline, and the ISM-adjusted Dallas Fed fell more modestly to 49.0 from a 3-month high of 50.2. Today's Dallas Fed headline dip, alongside weak Philly Fed and component data but Empire State gains suggest a modest April sentiment bounce that is still consistent with a broad pull-back in sentiment from robust peaks in November of 2021. Most of the various component categories across surveys are in contraction territory.

{kind=link}

The index has spent the last 12 months BELOW pre-pandemic levels.

Dallas Fed Commentary on the Machinery manufacturing sector;

"There is a definite slowdown. New orders virtually stopped. We are starting to see a real slowdown. We are hoping it is short lived."

Chicago PMI rose to an 8-month high of 48.6 from 43.8 and left the measure further above the 3-month low of 43.6 in February, though analysts now have eight consecutive sub-50 readings. The Chicago PMI rise joins a big Empire State gain but declines for the Richmond Fed, Dallas Fed, and Philly Fed, to leave an April bounce after outsized deterioration in most measures in March.

Manufacturing remains in a recession.

Housing

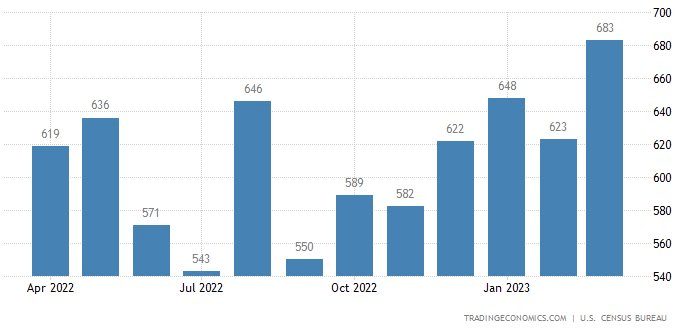

New Home Sales grew more than anticipated in March, as a lack of existing homes continued to bolster demand in the market for new properties.

{kind=link}

Sales of new single-family houses picked up 9.6% to an annual rate of 683,000 last month, seasonally adjusted.

Pending home sales dropped 5.2% to 78.9 in March, below forecast, after rising 0.8% to 83.2 in February. This breaks a trend of three straight monthly gains. Three of the four regions posted declines. Pending sales are down 23.3% year over year. The -37.7% y/y clip from November is an all-time low.

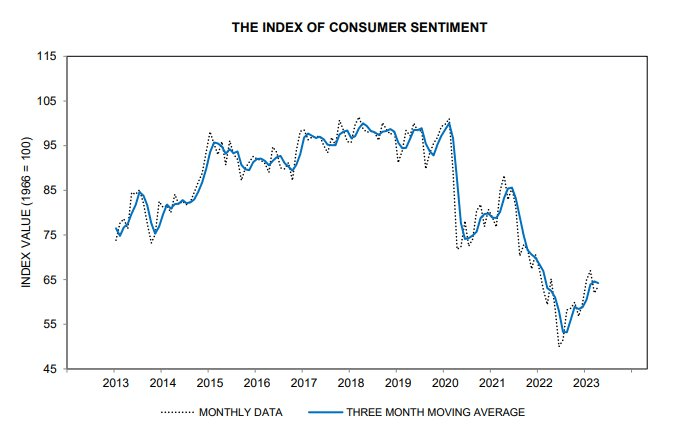

Consumer

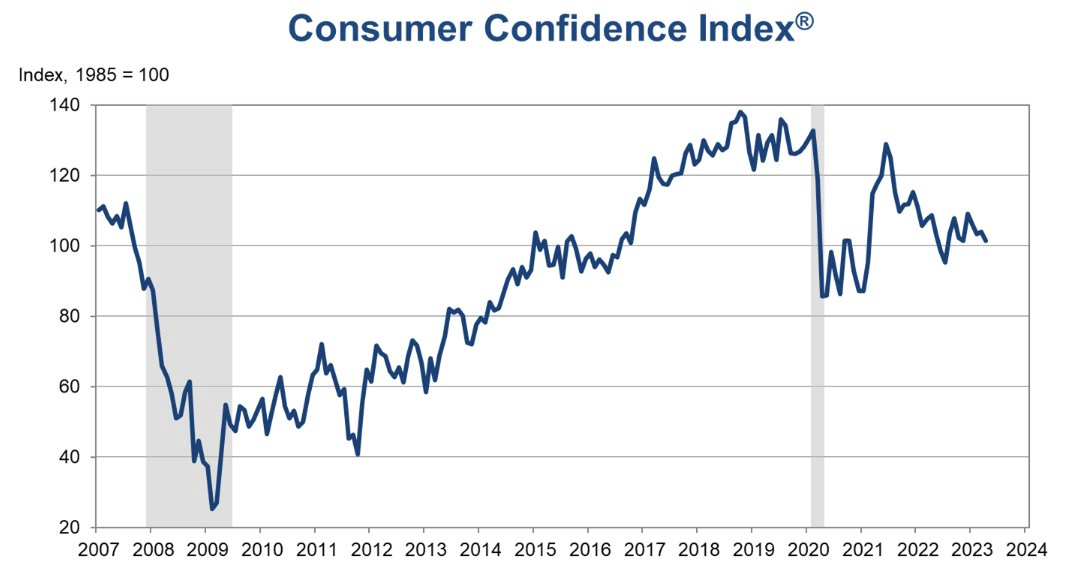

Consumer confidence dropped to a nine-month low coming in at 101.3.

{kind=link}

The index remains well below pre-pandemic results.

The final Michigan sentiment report revealed an unrevised headline bounce to 63.5 in April. Michigan sentiment is oscillating below the early pandemic bottom of 71.8 in April 2020, but above the all-time low of 50.0 in June of 2022. The Michigan sentiment survey and the IBD/TIPP sentiment report are fluctuating around historically weak levels.

{kind=link}

The index has been in a steep decline since 2021 and is a far cry from levels seen before the pandemic.

Earnings

In a note to subscribers last Tuesday I noted;

After a slow start, earnings season is in full swing as ~ 60 companies reporting results this morning. These companies have combined sales of $350 billion, and the results have been very positive. The EPS beat rate is at 77%, while the revenue beat rate is still high at 73%. Additionally, only two companies have lowered their guidance, while five companies have raised theirs. It's only one morning of results, but this does NOT look anything like an earnings collapse."

I can now add that this earnings season has been an analyst's nightmare because they have been HORRIBLY wrong.

Food For Thought

Success is under attack again.

In the last two years, the wealthy have been under constant attack as "redistribution" and "equality" have drowned out the facts and what is commonly known as common sense. Wealth accumulation is the goal of every individual in a capitalist society , and when wealth and success are achieved, penalizing those individuals is the last thing that should be done. The fact is the wealthy pay the freight. They start businesses, which hire workers. The ULTRA- wealthy give more to society in the form of philanthropy than they ever get credit for. Yet it is still deemed necessary to take some of the fruits of their labor away.

The redistribution anti-capitalist mindset is now filtering down to the average American in our opinion. An individual works hard to build their credit, only to get penalized as homebuyers with higher credit scores will see higher mortgage costs. The new rule, which goes into effect on May 1 , will affect mortgages from private banks across the nation. According to The Washington Times, Fannie Mae and Freddie Mac, federally-backed home mortgage companies, will establish the loan-level price adjustments.

This is deja vu all over again. For those that may not remember, the Great Financial Crisis was born when a government-initiated program wanted to give "everyone" an opportunity to own a home by lowering mortgage underwriting standards to the point where among other relaxed rules, no documentation was required to borrow money to purchase a home. That created an army of unqualified buyers that should never have been given a mortgage to create the tsunami of mortgage defaults that led to the financial crisis.

The folks that are now defending this new discriminatory action will be the first to start blaming the banks when the next round of defaults arises. Lending standards are being relaxed with a slow/recessionary economy on our doorstep. The plan is void of common sense.

There was a reason I mentioned "capitalist society" in the opening paragraph. It is the foundation of U.S. society and is the backbone of our investment world offering opportunities for EVERYONE. No matter where an investor stands on this topic, the takeaway of this action is mind-boggling. The mere fact that a program like this is unveiled today indicates a continuation of the ill-conceived policies that have led to the current investment backdrop. Policies that treat common sense and capitalism as second-class citizens will eventually affect the economy and the stock market negatively.

The Global Scene

Prosperity is scarce without control of the energy scene.

Henry Kissinger once said, "Control oil and you control nations". Sadly the US has forfeited what was once THE dominant energy position in the world. A policy mistake that will haunt the US economy for years to come all in favor of the "green new deal". Perhaps they didn't realize or perhaps this was indeed part of the plan all along, and it just got worse for the U.S. The transition to green makes lithium the new crude oil, and those who control it will rule. Unfortunately, that compounds the mistake of abandoning fossil fuels and willingly anointed China, as it places them in control of the transition to green.

The rush to reduce global carbon emissions has been ruled by emotion. When it comes to global energy policy, it's been one mistake after another. In what can only be called a head-scratcher, Germany shut down its three remaining nuclear plants, concluding a phase-out policy that originated in 2011. Common sense would seem to agree with the opinion of the head of the pro-nuclear non-profit association Nuklearia;

"By phasing out nuclear power, Germany is committing itself to coal and gas because there is not always enough wind blowing or sun shining,"

Then again, common sense has not prevailed in this obsessive emotionally driven transition. I continue to believe these mistakes will negatively affect the global economy for years to come.

The Daily Chart of the S&P 500 ( SPY )

What a week. A rally that gave the appearance of another failure, turned into a move to challenge the February highs.

{kind=link}

The S&P closed at a new recovery high off the March lows on Friday a 4164. That leaves the next BULL target the February closing high at 4179.

Investment Backdrop

I've noted evidence (especially in the NASDAQ) where the index continues to grind higher, but breadth expansion and momentum start to slow. Such action is typical of a rally in its latter stages as fewer buyers and fewer stocks participate and traders view each new reaction high as an opportunity to reduce size.

Two weeks ago we saw the S&P 500 hit a new reaction high but it wasn't associated with heavy buying, and there was no follow-through. Instead, the averages pulled back and traded sideways. That type of pattern can keep the indices moving upward and keep everyone guessing. In this market, it's best to stay prepared and be ready for anything.

The bulls and bears were circling each other like sumo wrestlers, and the first blow was struck last Tuesday and again on Wednesday, raising the question if this will wind up being another failed rally. The next two trading days saw a complete reversal that now has the indices eyeing new recovery highs.

The short term always presents uncertainty and this environment is loaded with challenges. The fundamentals scream caution, while the technicals are now starting to flash green. Therefore, it's not the time to get overly bearish. For one thing, take a look at this earnings season. It is not the disaster many were forecasting. Remember that coming into this earnings season Hedge funds were holding a HUGE "short" position. Each positive EPS report brought doubt into that strategy, and what might be adding to this upside surge is plenty of short covering that feeds on itself.

I don't like to jump too far ahead of where we are today, but I think it's a good idea to be aware that some sort of top may be forming in the coming weeks. Each of us could come up with a scenario of what comes next and here are the favored options;

- This rally morphs into a FOMO situation that moves the indices higher than some expect.

- The rally ends here with another failure at resistance and the indices head back to the lower end of the trading range.

- Another option is a "start and stop" scene that keeps the confusion levels elevated.

I'll remind you the market rarely works out in a perfect, textbook manner, so be ready for anything.

Small Caps

Typically, I want to see the small caps leading the way when I am bullish on stocks. It's not "required" since we have seen occasions when the S&P 500 and other averages rise even as the Russell 2000 flounders, but for a move to have lasting power, particularly after the kind of bear market we saw last year, it is better to see the more speculative, smaller companies in rally mode. That is not what is occurring today. The Russell 2000 ( IWM ) is being weighed down by its heavier exposure to smaller banks, the prospects of higher rates, and a slowing US economy.

The index sits in the middle of its trading range and that keeps it entrenched in its BEAR market trend. I will need to see a break above resistance levels before I get more bullish on the group. Looking at the charts, we can now use hindsight to tell us that the January rally that got investors excited was a false breakout. It turned out to be another LOWER high in a continuing BEAR market.

The index looks like more of an opportunity to "short" on any rally.

Sectors

Energy

The rally off the lows in the Energy ETF ( XLE ) is now in a period of giving back some of the gains. There is plenty of support below the present price and if this pullback is contained, the Sector can start to make a move back to the highs.

Financials

It is probably as simple as the Russell 2000 is going to follow the path of the small regional banks. The underperformance of IWM has very much coincided with the poor performance of ( KRE ), the Regional Banking ETF.

No matter how we look at it, the chart for KRE is not Bullish. It appears to me that instead of any sustainable bounce, another leg lower is in the cards.

We did see a tepid bounce this week that left the ETF right up against resistance. We'll soon find out next week if the mini-rally has any momentum left.

In the meantime, the Large center money banks represented in the Financial ETF ( XLF ), did produce a bounce off the lows, met resistance, and stalled. This market is full of surprises, but I believe it's a VERY low probability investors will see a sustained move higher for ( XLF ) in the near term. I repeat last week's analysis. The group won't assist in taking the major indices higher for a while.

Commodities

Recently I mentioned that we could be entering the early innings of a large BULL cycle for commodities. That could mean a multi-year period of outperformance for this sector of the market. Commodities have entered such a period where they should outperform over the next few years against something as we saw yesteryear with the NASDAQ 100. I like the group on any pullbacks.

No change of opinion from last week;

( GSG ) is in a Long term BULL trend. Another Commodity tracking ETF ( DBC ) and the Metals and Mining ETF ( XME ) are both in BULL trends as well.'

We should also take note of the "soft" commodities. It's not just the major markets like Oil, Gold, Silver, and other Metals that everyone is familiar with. The Invesco DB Agriculture Fund ( DBA ) looks to be breaking out of a multi-month base with strong momentum."

DBA did break out last week then quickly pulled back to that breakout level.

Healthcare

A slight pullback this week in the Healthcare ETF ( XLV ) after a nice 7% rally off the lows. That puts the sector back in play to start looking for opportunities. I recently focused on a particular subsector- Medical Technology.

The Med Tech sector has struggled over the last two years as Covid was unkind (both from a demand disruption and a follow-on supply chain/margin perspective). This dynamic has disturbed Med Tech's historical growth pattern and investors and money managers shunned the group.

With the impacts from the pandemic fading, we can expect Med Tech to work back towards its historical 5% top/10% bottom-line growth profile, punctuated by investable themes around procedure recovery and margin expansion. EPS growth will probably start to accelerate in 2H23 and into '24, which has the potential to offer a differentiated growth profile vs. the broader market. I expect this backdrop to better resonate with a broader group of investors and believe Med Tech should be better positioned to outperform the market.

The Med Tech ETF ( IHI ) is already starting to signal that future growth profile as the group recently broke to the upside. MY preferred names: Are Large Cap: Boston Scientific ( BSX ), (a savvy '23 favorite), Growth with Dexcom ( DXCM ) , and recently added "Cadillac" of medical technology, Intuitive Surgical ( ISRG ) .

Biotech

The 13% rally off the March lows came to a screeching halt as the Biotech ETF ( XBI ) ran into multiple resistance levels. So far the pullback has been mild and well-contained. The BULLS would like to see this support area hold and then spark a move back to those resistance levels. I continue to HOLD my positions.

Gold

The Gold ETF ( GLD ) broke what was a very short-term uptrend recently. Remember what was said a couple of weeks ago? GLD was approaching resistance that capped rallies in 2020 and 2022. So this pullback isn't that unexpected. Now it's a matter of the extent of this pullback and if support holds. If GLD breaks below the next support level ($178), then the probabilities are high that this rally attempt has failed (again), and the forecasts of gold moving much higher take on a lower probability of occurring.

Silver

Silver ( SLV ) was holding up better than Gold, but it has now suffered the same fate. The short-term trend is broken. I now expect silver to follow the same path as Gold, if so, the same analysis applies. In the short term, the metal will probably settle back into a trading range instead of going on to set new highs.

Technology

The investors that piled into the big-cap tech names during Q1 have been rewarded. Admittedly I wasn't part of that group, but I also wasn't a seller in '22 (many of these names are CORE positions for me). After 11 months in a BEAR trend, the technology sector ( XLK ) is on the cusp of breaking back into BULL mode. That in itself doesn't turn me into a wild-eyed buyer but if the sector can HOLD these important levels it starts to change the narrative.

Semiconductors Sub-Sector

Last week we noted the "pause" in the semiconductor rally. Is this the start of a rollover for the Semiconductor ETF ( SOXX ) or a last flush of weak hands before the group gets back into rally mode?

We got a clue this week.

The ETF has now put in back-to-back weeks of losses. That is not so unusual given the huge rally this year. As with any pullback, it's all about containing the damage and finding support quickly.

We'll see what develops next week before I decide what might come next for the group.

Final Thoughts

My goal stays the same, stay in sync with the markets as best I can to make money. In the short term , I do not care if that requires being bullish or bearish. I certainly have my opinions but if the price action does not support those opinions, I am not going to argue with it. Based on my interpretation of the balance of evidence, I have been more cautious or even at times outright bearish on stocks since February '22. Looking through as many price charts as I do, that seems to have mostly been the correct call. Yet, there are occasions, like recently, when I have seen enough to take more chances on the long side and I have also attempted to play these rallies.

An active trader has to learn to go with the flow of the markets rather than fight it. We've seen how quickly this market can turn, and that simply means any active investor can't allow themselves to get too entrenched and extended in either direction. This environment requires that no one gets too LOW on the selloffs and too HIGH on the rallies.

For all the talk about whether we're in a new bull market or still stuck in a bear, at this point it seems like neither. If you want to call it a BEAR market, it looks about as savage as a koala, and if you're going to go the BULL route, it's raging more like a cow than a bull. Suffice it to say we don't have a strong short-term trend in place either way and in my view it matters little how we define the market.

So I step back, look around, and conclude I'm not going to change the strategy of investing in what is "working". Investors should always go back to the basic principles of success, and where we are today demands flexibility and an open mind approach. Anything short of that is going to cause investors problems.

Keeping it simple lowers your stress levels. Keeping anxiety in control lessens your mistakes.

THANKS to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

For further details see:

Week On Wall Street: Caution, Yes, Panic, No