ACTV - Week On Wall Street: Hand Grenade Or Time Bomb

2023-04-15 07:20:00 ET

Summary

- Inflation reports are showing improvement, but there is more work to be done.

- A Bear market has never bottomed before a recession begins.

- Projections for slower economic growth translate into a negative effect on corporate earnings.

- Banks aren't lending because uncertainty and a slowing economy have curtailed demand.

“We have met the enemy and he is us.” - Pogo

The Macro View

For going on two months now, we’ve been hearing nonstop about how inflation has remained stubbornly high following the post-COVID surge. I would be the first to agree that current levels of inflation are too high, but what were people expecting? Inflation doesn’t just instantly disappear, and that was the message when it first surfaced as a problem. Just as the process of reaching multi-decade highs last year occurred over months, the decline from those highs will take time. In most cases, though, the rate of decline has been just as fast or even faster than the rate of increase. Remember we are coming down from 40-year highs, and some of the excessive stimuli are still sloshing around in the system.

While we see forecasts for rate cuts very soon, no one acknowledged what the Fed believes the path to lower inflation will be. The Fed published the quarterly update of its Summary of Economic Projections on March 22nd, in which it forecast that core PCE inflation would fall to 3.6% by the end of this year, to 2.6% by the end of 2024, and to 2.1% by the end of 2025. By the Fed’s projections, then, it may be nearly three years before it has successfully slayed the inflation dragon.

Now let's also be realistic. These projections, just like all the others out there, aren't cast in stone. It may be as good or as bad as any of the others and I'm not suggesting we blindly follow that path. However, I also do not think it's wise to follow the notion that rates will be coming down anytime soon because inflation will be 2% anytime soon.

Let's also realize that when inflation does finally show enough evidence that it will indeed drop to 3%-4% or lower, the Fed won't be backing off immediately. They will never take the chance of reversing too quickly for fear of reigniting inflation. The Fed will continue to watch the data (probably for months), and the upshot is that the market will also remain highly sensitive to the incoming data flow.

The economic normalization process (from excessive easing in Covid to excessive tightening post-Covid) is likely to be lumpy with confusing data along the way. And given investor uncertainty on its path and the stakes being so high, we have already seen sentiment swings occur. I believe that will be the norm for a while longer. There will be excited periods where stocks rally and disappointed periods where they pull back. Until inflation is down, it will be difficult for stocks to move substantially higher.

The Hand Grenade

We've covered the list of issues that are potential hazards for the economy and we were just tossed another "grenade" to deal with. I chose that description because recent financial issues have to do with how some banks have chosen to manage their deposit liabilities in an environment of rising global interest rates. That isn't the time bomb I'm concerned with. Policymakers are amply able to deal with liquidity squeezes. Credit spreads have behaved well and this tells me this isn't systemic.

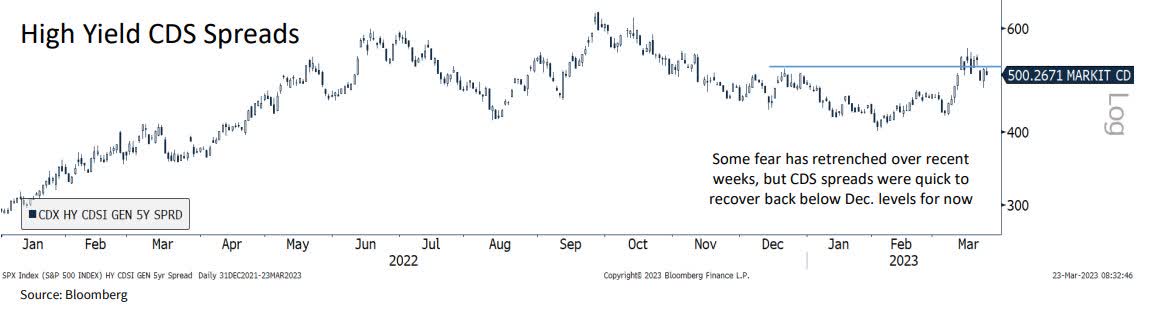

CD Spreads (www.bloomberg.com)

{kind=link}

However, the foolish actions of a couple of banks changed the scene, and market psychology was shaken. The investment community sees this event for what it is and has for the most part shaken it off. That being said this can have further ramifications which could result in the next step.

A Time Bomb

A case can be made that this sets off a dynamic that likely raises the odds of a recession. Part of the problem is what we discussed last week. The financial system is now under scrutiny. Bank regulators were embarrassed, the congressional finance committees are calling for hearings, and it's highly probable we will get an overreaction on the regulatory side. If that does occur it will be another mistake that will add more stress to the economy.

It's poor management and poor regulators. Banks do not need more regulations; they need more competent regulators . Adding more stress by micro-managing the first mistake is certainly avoidable, but in an already over-regulated environment, it is highly probable. Until proven otherwise this is an isolated event, and the stock market agrees. Does anyone actually believe the S&P would be trading closer to the old highs if there was a financial crisis brewing?

Even before Silicon Valley Bank (SIVBQ), there was little to no loan growth. Who is expanding in this uncertain environment? Who is going to go out on the risk curve with lending costs appreciably higher? As we will see when we cover the Small Business report later, businesses are telling us this is one of the worst times to expand since the Great Financial Crisis. Banks aren't lending because they have "issues". They aren't lending because there is less demand.

Now added scrutiny will keep them vigilant and will force them to reduce lending for households and businesses, which could further slow economic growth. Chair Powell conceded that tightening financial conditions could have the same impact as another quarter-point rate hike—or possibly more—from the Fed.

If that is true and the Fed's interest rate cycle to tackle inflation hits the economy at the same time, it presents a huge problem. Unfortunately, the Fed is boxed in. It must respect inflation and do what is needed (higher rates) to combat inflation, which remains at elevated levels. In that same summary of the economic expectations report, the Fed also reduced its forecast for real GDP from 0.5% to 0.4% in 2023 and from 1.6% to 1.2% in 2024. Perhaps they see what I just described coming to fruition.

I will admit that is the way I have seen this situation developing for a while so it is easy for me to buy into that projection. Slow or no growth is a huge factor that is going to add more problems for the Fed. Along with inflation, it has been the crux of the negative Macro scene that is in place. Like all other projections, that forecast doesn't have to come to pass either, but it is a clue as to how the Fed sees policies that offer no growth and add to the inflation issue.

Therefore, we have an economy that is going to struggle. "Official" recession or not, the projections reveal abysmal growth and it will affect corporate earnings. We now see the reason I was warning about spending, inflation, and forcing Fed involvement to specifically fight inflation. That worst case has come to pass, and we are now dealing with it.

The stock market is now going to try to figure out which force is more important; Stable (but still high) interest rates or a weakening economic picture. Equity prices are driven by corporate earnings and for the time being, they appear to be stuck in a recession. The other piece of this pricing puzzle is also confusing and uncertain.

The market is implying a scenario with large numbers of rate cuts that lead to a Fed Funds rate below 4% by year-end being twice as likely as a scenario where rates are raised twice more before being held steady. The point is that the market is pricing a huge shift from the Fed, despite repeated statements to the contrary in recent weeks.

I am not ready to buy into the rate-cutting theories unless we see one of two things. Inflation and/or the economy falls off a cliff. Before we start to see a durable market upside, it will take a degree of clarity on inflation, Fed policy, and the economy, and I don't see that occurring anytime soon. For P/E multiples to expand substantially, we need inflation to come down and bond yields to subside/stabilize. Eventually, I believe this will occur, and that P/E multiple expansion will drive positive equity market returns. The problem is I don't envision that to occur in the near term.

The Week On Wall Street

For a second straight trading session, stocks staged a modest but persistent comeback on Monday. A "gap down" was followed by a charge higher to send the indices to the best levels of the day at the close. The indices were 'flat" but the resiliency of this market was very obvious. It was more of the same on Tuesday as the "inflation watch" was on. All except the Russell 2000 were once again flat on the day. The small cap index, however, increased its two-day gain to 1.8%.

Investors yawned after the CPI report on Wednesday and it took a while before the market started to react positively to the PPI report. The 2 and 10-year treasury yields drifted lower and the "growth" trade was in full swing. Every index was higher by more than 1%, with the NASDAQ Composite leading with a 2% gain on the day.

The Economy

Inflation

The 0.1% March U.S. CPI saw a 0.4% core increase, leaving encouraging headline restraint but with continued firmness for the core. The lean March CPI headline gain reflected a big -3.5% drop for energy prices (that may reverse in April) with flat food prices, a -0.5% drop for medical care services that marks a third consecutive drop, and a 0.5% rise for owners' equivalent rent that marks a moderation from recent big gains.

The y/y CPI measure fell to 5.0% from 6.0%, while the core y/y gain rose to 5.6% from 5.5% . Analysts tentatively assume April CPI gains of 0.3% for both the headline and core, leaving y/y gains of 5.0% for the headline and 5.4% for the core.

More good news on the inflation front. Headline PPI dropped 0.5% in March and the core rate dipped 0.1%. Last month's numbers are the weakest since April 2020. The annual headline pace decelerated to 2.7% year over year from 4.9% y/y, the slowest since January 2021. And the core rate slowed to 3.4% y/y from 4.8%, the weakest since March 2021.

Much of the decline in PPI was attributed to energy prices plunging 6.4% from 0.3% in the prior month. With energy prices rebounding in April it will be interesting to see if these levels hold.

Consumer

Retail sales dropped 1.0% in March and fell 0.8% excluding autos, both weaker than expected. Sales excluding autos, building materials, and gas slid -0.2% from a prior 0.1% gain. Weakness was broad-based.

Retail Sales (www.tradingeconomics.com)

Sales have posted negative results in four of the last 5 months.

Consumer sentiment bounced 1.5 points to 63.5 in the April preliminary print, recovering a portion of the 5.0-point plunge to 62.0 in March on the heels of the banking debacle. The current conditions index improved to 68.6 from 66.3. The expectations component rose to 60.3 from 59.2. Meanwhile, the 1-year inflation gauge surprised, surging to 4.6% from 3.6%. This is the highest since November's 4.9% clip.

Michigan Sentiment (www.sca.isr.umich.edu/charts.html)

As the chart indicates, sentiment remains at historic lows.

Manufacturing and Small Business

Industrial production increased by 0.4% in March after edging up 0.2% in February. All of the strength last month was in utilities where production jumped 8.4%.

The NFIB Small Business Optimism Index decreased 0.8 points in March to 90.1, marking the 15 th consecutive month below the 49-year average of 98. Twenty-four percent of owners reported inflation as their single most important business problem, down four points from last month. Small business owners expecting better business conditions over the next six months remain at a net negative 47%.

NFIB Chief Economist Bill Dunkelberg;

“Small business owners are cynical about future economic conditions. Hiring plans fell to their lowest level since May 2020, but strong consumer spending has kept Main Street alive and supported strong labor demand.”

NFIB (www.nfib.com)

Within that report, the percentage of small businesses saying now is a good time to expand dropped to levels only seen at the depths of the Financial Crisis in March 2009 while the index for hiring plans dropped to its lowest level since May 2020. In other words, small business sentiment is not particularly optimistic.

The Global Scene

In Europe, Retail Sales for February fell 0.8% on a month-over-month basis, but that was actually in line with expectations.

EU Retail Sales (www.tradingeconomics.com)

When it comes to the ravages of inflation, China remains the envy of other global economies.

China CPI (www.bespokepremium.com)

Both the "Headline" and "Ex-food/Energy" are well under 2%.

Here is a positive sign for the global economy. China's March trade data showed exports surging 14.8% YoY versus an expected 7.1% decline. China’s trade surplus was the second-largest ever every month in March and a record in Q1. That’s despite surging petroleum imports, with crude imports surging 8.5% from January to March and 15.2% from August to March.

The FOMC Minutes

Well, what a surprise, the Fed has uttered the "R" word.

In addition to their overall take on the economic situation where nothing was shocking, the Fed staff projected a mild recession starting later this year due to the impacts of the banking stresses. Of note, a downturn in growth was only seen as a "possibility" in February.

Earnings

Well, it looks like earnings season has kicked off on a positive note. Of the six Financial companies reporting Friday morning, all of them topped EPS forecasts, and PNC was the only one that had weaker-than-expected revenues. Even here, though, the miss was extremely narrow.

Brian Gilmartin - Fundamentalis Research;

Q1 ’23 expected sector EPS growth ranked strongest to weakest:

- Consumer Disc: +36.4% (Tesla and Amazon, homebuilders, etc.) Consumer Disc EPS fell 27% in q1 ’22, most likely due to Amazon.

- Industrials: +17.9% vs +40% growth in q1 ’22, tough compare.

- Energy: +13.7% vs +269% growth in Q1 ’22.

- Financials: +5.2% vs - 17% decline in Q1 ’22) JPMorgan, Goldman, etc. had very tough capital market and investment banking comparisons in Q1 ’22;

- Cons Staples: -4.8% vs +8% in Q1 ’22;

- Real Estate: -8% vs +25% in Q1 ’22;

- Utilities: -9.9% vs +24.6% in Q1 ’22

- Communication Serv: -12.6% vs -2.8% in Q1 ’22. Mostly Meta (META) and Alphabet ( GOOG );

- Tech -14.4% vs +14.6% in q1 ’22, but "software" was already weakening in late Q4 ’21.

- HealthCare: -18.8% vs +18.3% in Q1 ’22;

- Basic Materials: -33.5% vs +46.3% in Q1 ’22.

- SP 500: -5% vs +11.4% in Q1 ’22.

Food For Thought

Energy

The Lower Energy Costs Act , announced by the House earlier this month, proposes to slash environmental regulations, expand oil and gas drilling on public lands and waters and repeal parts of Democrats' signature climate law. Senate Majority Leader Chuck Schumer (D-N.Y.) called the legislation;

"A partisan, dead-on-arrival and unserious proposal for addressing America's energy needs that they have laughingly labeled H.R. 1."

The White House has also weighed in and announced that Biden will veto the bill.

This is another signal to investors that the existing energy policy will remain in place, keeping a "bid" under energy prices. Energy stocks will once again be the place to have money invested (overweight position) this year and next. Recent discussions between Exxon (XOM) and Pioneer Natural Resources ( PXD ) are an indication that many of the "explorers" are severely undervalued.

There are more reasons to keep "energy" in focus. During the drawdown of the SPR- Strategic Petroleum Reserve the Government was selling "sour" crude oil. Typically, US refiners prefer medium-sour crude , which is denser and has more sulfur but is a variety they can easily process into gasoline and other products thanks to their highly sophisticated refining plants. According to a Washington Post article, 85% of the oil the SPR has sold has been medium-sour.

Since the US hasn't built a refinery since 1976 , refining remains one of the largest bottlenecks in the oil market that eventually impacts consumers. With the SPR at a 40-year low, that "game" is just about over, and at some point, gasoline supplies are going to impact prices—the "options" for the US. Look to the "other" Medium-sour suppliers. It is currently pumped by Russia, most Middle Eastern countries, and Venezuela. Canada produces the crude US refiners need, but supply becomes limited without the Keystone Pipeline. The existing pipeline infrastructure is and has been operating at total capacity.

We can now pick our poison.

EVs

The Electric vehicle revolution is in full swing. Ford (F) joins an unenviable auto group that doesn't produce an EV profit as they announced a 3 billion dollar loss in their EV business. Taxpayers picked up that tab when the Green New Deal (China Stimulus) a.k.a. Inflation Reduction Act was passed last year.

The obsessive push for EVs already has impacted the economy in the form of government spending on subsidies. We can expect this "phenomenon" to continue, and it will be a drag on growth. The expenditure to keep this initiative which is at least a decade away from mass adoption is staggering. All while keeping costs for "energy" required to perform daily activities and generate the electricity needed for this EV revolution extremely high.

Bottom Line: The "plan" as proposed adds to the inflation conundrum.

LNG Exports

Despite its advantageous location in the Pacific, California has no LNG (Liquified Natural Gas) facilities. An LNG export site on the West Coast is considered a money-maker because most LNG export facilities are located in the Gulf of Mexico, which means ships must go through the Panama Canal to reach customers in Japan, China, and other Asian markets. But cargoes originating from a facility on the Pacific can skip paying tolls at the canal and arrive at their destinations in about half the time.

It's no secret that California's Governor and Energy Commission are waging war on fossil fuels. Combine that with their onerous "permitting " policies, and companies have gone elsewhere to fill the need for a West Coast Terminal.

Enter Mexico. U.S.-based Sempra Energy is getting its much-desired liquefied natural gas export facility on the Pacific Coast in Baja, Mexico. There are plans to build eight LNG facilities in Mexico and if all come to fruition, the country will become the world’s fourth largest LNG exporter, behind the United States, Australia, and Qatar.

This "missed" opportunity will be a huge loss of economic growth for the U.S., at a time when growth is hard to come by. The ramifications of policies led by "green first" are being ramped up exponentially.

They will become the leading issue that keeps a 'ball and chain" on the economy, having the potential to affect the Macro scene for years.

Sentiment

We've experienced poor sentiment among investors all during this Bear market. What was once a great "contrarian" signal became rather insignificant, and didn't help investors solve the confusing action.

This latest nugget was an eye-opener. The Commitments of Traders report showed futures positioning data as of last Tuesday showed that traders were the most bearishly positioned in S&P 500 futures since September 2007 when 18% was net short.

The Daily chart of the S&P 500 ( SPY )

It's a "glass half full", and the S&P is making another run at the February highs. That's a fairly critical level that both the Bulls and Bears will be watching.

{kind=link}

Investment Backdrop

Investors were focused on the avalanche of data that was reported this week. CPI and PPI provided a catalyst for the Bulls to grasp onto and they moved the indices higher.

When retail sales and Bank earnings were announced on Friday it turned out to be a "wash". Bulls were hoping that the good news from the Banks would then add to the positive mood. One day doesn't make a trend, and while the market rewarded the financial sector the general market seemed to care little.

After a significant run-up in share prices to start the year, earnings reports from mega-cap technology companies will loom large over the market in the coming days. The heavy weighting of such companies as Apple Inc. and Microsoft Corp. in the S&P 500 make results from them particularly influential in the direction of the overall stock market. It is hard to justify that tech stocks are on an upward swing while earnings expectations are lower. We'll now get a reality check when earnings start to come out.

Last Wednesday marked the six-month anniversary of the October lows. Analysts have struggled to determine how to call what the market has done over the last six months. In that time frame the S&P 500 managed to stay above its prior low from December (positive), but in the rally that followed it has yet to move above its February high. That’s just another reason many are perplexed. New bull market? Bear market rally? Or is it more of a no man’s land?

The S&P 500 has been in an 85-point trading range for the last nine days. Something has to give. I get the feeling the market wants to take another shot at this year's high at 4179. We'll probably get that answer next week.

Bifurcated Market

While everyone wants to be fixated on Large caps versus Small caps and Growth versus Value, I have concentrated my efforts on a different strategy. The place to be is in the sectors that are in Long term Bull trends. I've recently added both the Gold and Silver markets as they have moved into a Bull trend as well. After that, whether they be Growth/Value, Small/Large cap, I want individual companies that are in Bull market trends.

If an investor wants to increase their odds of success in this Bear market backdrop they are the place to concentrate investment dollars. I'll leave the bottom picking for others. First, I do not excel at that strategy, and two, I'm not interested in waiting around for a "turn" in the situation. For sure if you guess right you are getting in on the bottom floor. Guess wrong and you will find yourself in the basement that is taking on water.

I want stocks that are moving from the lower left to the upper right of my computer screen. If and when other sectors start to move back into a more positive technical configuration, I'll consider adding exposure to those groups.

Sectors

Defense and Aerospace

Hers is a sub-sector that has been strong for a while now. The Defense ETF ( ITA ) is on the cusp of a new all-time high. If it fails to do so the subsequent pullback would represent an entry point. Individual stocks like Lockheed Martin (LMT) and Raytheon ( RTX ) are standouts. Full Disclosure: I have owned both for a while and continue to Hold.

Energy

The recent news that OPEC announced Oil Production cuts can and will be dissected in many ways that will lead to an abundance of different scenarios. Oil prices are difficult to predict so let's keep it simple. Bottom line -- more oil is off the market. That can't be supportive of lower prices. At the very least investors have another 'put' that should keep oil prices stable, if not push them higher. I'm not running to buy more oil stocks today, (my position is already overweight) but I sure wouldn't advise selling any either.

For those that don't have an overweight position, here is your opportunity. I advise concentrating on the big dividend "Explorers" first. Many of those stocks have come down from highs on the notion that they will be cutting their outsized dividends because oil prices drifted lower. That "notion" may have just gone out the window.

Financials

The Financials ( XLF ) are always considered a "key" sector when speaking to the general market situation.

So far there has been no "contagion" exhibited in the banking system and that fits in with the notion that what we just experienced was the actions of irresponsible managers and regulators at the California institutions. However, that doesn't alleviate my fears about what comes next -- an overreaction that increases overregulation.

Following a week of hearings on Capitol Hill and conversations with Washington officials, Congress has already laid out a roadmap for the next steps for bank regulation. More regulation is coming – especially for banks between $100 - $700 billion in assets. It's early, so the timing, scope, and impact remain important parts of the conversation.

Regulators control most of the authority that they need to fully implement additional reforms (no need for Congress to act to implement/ that is a negative in itself) and they will act expeditiously. However, the required process for implementing new rules is generally a 1-2 year process. That may "save the day" in the intermediate term and reduce what could be another "policy error".

The next catalysts will be draft proposals, which frequently add uncertainty to outcomes. Beyond new regulations, we should be watching for increased enforcement and supervisory action by regulators. The FSOC should also be closely watched for new systemic risk designations. Congressional action remains less likely, outside a potential expansion of FDIC deposit insurance.

Enacting new sweeping national regulation because the action of a rogue bank and a Rogue Federal Reserve Bank in California will be another policy error. It will deter regional bank lending in an economy that is going to be stressed under the rate increases and that can accelerate the slowdown.

Unfortunately, both the Financial ETF ( XLF ) and the Regional Bank ETF ( KRE ) are looking pretty Bearish lately. The knee-jerk reaction to the headlines has been to sell the entire sector. Therefore, it remains a group that is a "no-touch".

Healthcare

After a difficult Q1, the Healthcare sector ( XLV ) has sprung back to life with a rally that has now posted four positive weeks out of the last five. The Q1 selloff in the group dropped the sector's P/E back to the "average" at around 17x. I've been resolute in my conviction that this group will remain more resilient than others in a slowing economy. No change in my opinion. This sector will pay dividends in '23.

We've seen a move back to the middle of the recent trading range, and this week's action pushed the ETF back into a Bullish mode. That adds more confidence for investors to take a look at this sector.

Biotech

This sub-sector of Healthcare, the Biotech ETF ( XBI ), is attempting to stabilize. After a rush to the exits that started in early March, the group has quietly added 4+% in the last three weeks. After a brilliant run from the June '22 lows, the short-term chart has taken on more of a trading range look. All of a sudden their "speculative" nature is being overlooked. However, I see that resistance looms and advise waiting for a pullback to support before adding.

Gold and Silver

The precious metals trade continues on its Bullish path. Both the Gold ( GLD ) and the Silver ETF ( SLV ) are setting new reaction highs, and they both look like "adds" on pullbacks.

Technology

The NASDAQ Composite and the NASDAQ 100 have been the place to be in '23. Both have led the market higher and now both are at a crossroads of sorts. Overhead resistance has stalled the latest rallies. The Bulls say it's merely a pause before the next leg is higher. The Bears suggest this move is over. I don't know who is correct, but I'm not adding to tech exposure until I see this Long Term Bear trend morph into a new Bull trend. I've labeled Tech an "equal weight" since last year and haven't changed that view.

Semiconductors Sub-Sector

The rally in the Semis ( SOXX ) has stalled. That isn't so surprising. Coming into the week the ETF was up 22% this year. Both the Daily and Monthly charts indicate the SOXX ETF is now hovering at support. We'll soon find out of that 'breakout' in the group that caught many by surprise was in fact, genuine.

Final Thoughts

The opening quote from Pogo has been used in previous articles, and it's more applicable today than ever before. Inflation and higher energy costs have been the result of "Policy" and the transition to "green" is another decision that will impact the economy for a long time. Now we can add a potential miscue resulting in a banking "crisis" that might not be a "crisis" at all, to produce more unnecessary regulations. Policy decisions have consequences.

In the last five weeks, the stock market has been marching to its own drumbeat. Any recent attempt at a selloff has been muted as there have been no 80-90% downside days. We can make a case that the S&P 500 is going to challenge the 4200 level, just as easily as we can make a case that the S&P will revisit the 3800 range. That leaves both the Bulls and Bears nervous and jerky.

The entire week's price action is another attempt at overtaking the highs for the year in the major indices. On the fundamental side, it is a situation we have talked about for months. Regarding interest rates, it should be awfully clear that "Higher for Longer" and a recession has to be part of the narrative.

The Bulls have to be concerned that the market has not come to grips with this eventuality. On the other hand, the Bears aren't sure if the market is digesting this information and just biding its time before it can look past these "issues".

Confused? Pogo has the answers.

Thanks to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

For further details see:

Week On Wall Street: Hand Grenade Or Time Bomb