WEN - Wendy's: A Decent H1 But A Foggy H2 Outlook

2023-10-22 23:26:28 ET

Summary

- Wendy's Q2 results were a little better than I expected, with the company noting it continues to make progress growing sales in breakfast and late-night.

- That said, the upbeat commentary in Q2 came in ahead of a sharp decline in traffic in quick-service in the second half of August and September, with little improvement since.

- In this update, we'll look at Wendy's recent results, industry-wide trends, and whether the stock is worth paying up for ahead of its Q3 results.

Just over a year ago, I wrote on Wendy's ( WEN ), noting that while the stock was up sharply from its highs, the E. Coli scare had the potential to lead to a stunted recovery and this suggested there were better opportunities elsewhere, with one name being Agnico Eagle ( AEM ). Since then, WEN is down 4%, the S&P 500 ( SPY ) is up 12% and Agnico Eagle is up 23%. However, Wendy's traffic impact from the minor E. Coli scare has been more muted than I expected and it put together a solid H1, with the company noting "outsized growth in breakfast and late-night" , and much better margins domestically. Meanwhile, although unit growth is lagging expectations due to permitting delays, we should see an improvement going forward, filling a portion of the gap with larger quick-service peers. In this update, we'll look at recent results, industry-wide trends, and where the stock's updated low-risk buy zone lies.

Wendy's Drive-Thru - Investor Day

{kind=link}

Recent Results & Updated FY2023 Outlook

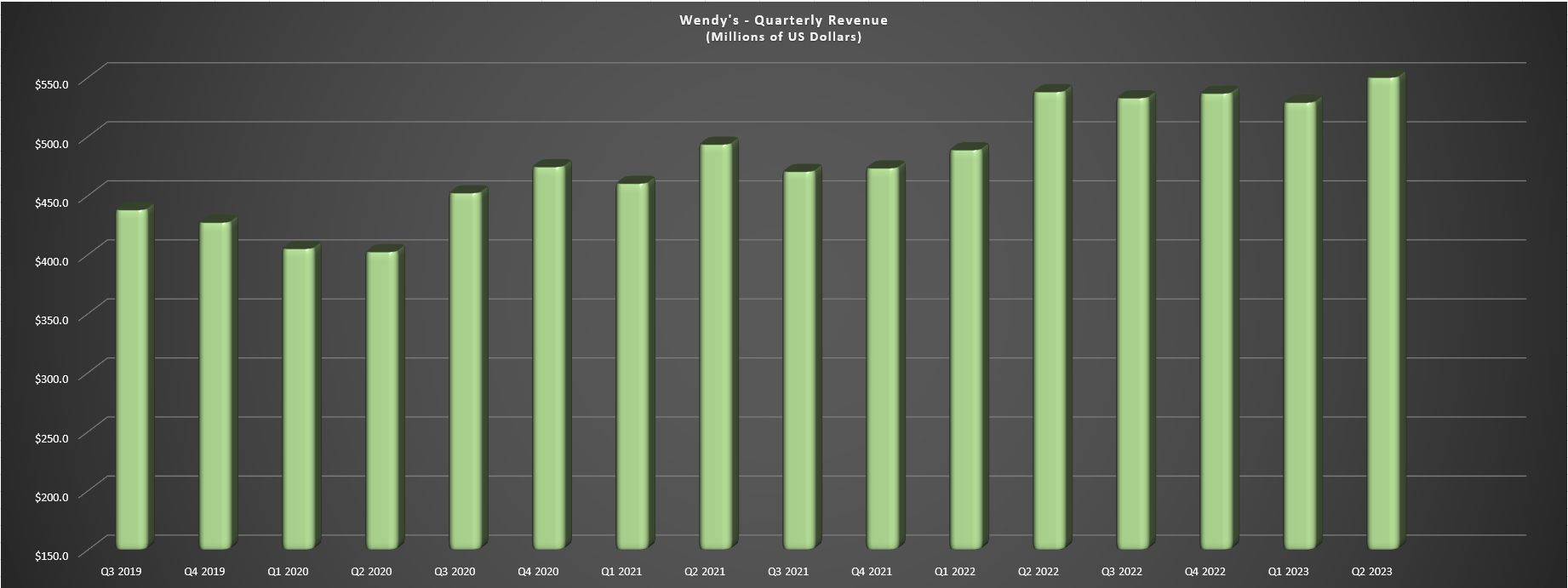

Wendy's released its Q2 results in mid-August, reporting quarterly revenue of $561.6 million, a 4% increase year-over-year. This was driven by same-restaurant sales of 5.1% across its system (1.7% United States, 14.7% internationally), and the company also reported system-wide sales growth of 6.9%. Overall, these results were decent, but overall development has continued to lag, with 80 restaurants opened year-to-date, but just 20 on a net new basis, translating to only ~0.3% growth. On a positive note, restaurant-level margins improved in the United States (+230 basis points to 17.3%) and internationally, though they are still lower on a five-year basis despite significant menu price increases (Q2 2018: 17.4%).

Wendy's - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, the company shared in Q1 that it was growing its share with higher-end customers and maintaining share with less affluent customers, and this trend appeared to be similar based on Q2 commentary. Meanwhile, the company noted that it has seen no pushback from consumers to date on pricing (~7% effective pricing for 2023 with recent menu price hike in May), also a positive development considering that Olive Garden owner Darden ( DRI ) noting it was seeing some potential signs of check management in its most recent results. Meanwhile, the company shared that it saw double-digit sales sequentially and year-over-year in the late-night day part and believes it gained share in late-night, with 90% of its restaurants (higher on weekends) now open until midnight or later. Overall, the wins in breakfast and late-night are positive, and investors can look forward to learnings in future updates after its first Next Gen restaurant opened in Q2.

According to the company, its new Next Gen restaurant design will place an emphasis on "convenience, speed, and accuracy across drive-thru, dine in and digital order pick-up". It will be equipped with a high-capacity kitchen at busier locations with a dual-sided kitchen design, with additional sandwich production areas and dedicated space for digital orders, and reduced travel distances for team members.

Finally, as for recent developments, although the ghost kitchen growth assumptions turned out to be a flop (REEF Kitchens), the company appears to be confident in its new voice AI potential (Wendy's Fresh AI) with Google ( GOOG ). In fact, the company noted that it launched trials in June with a goal of improving speed of service in drive-thru and that it is helping its team members do their jobs better. That said, this wouldn't be as much of a margin opportunity if implemented, but repositioning labor within its restaurant according to the company, helping to improve speed/accuracy. And while the company could certainly use labor savings like Kura Sushi ( KRUS ) has benefited from, faster drive-thru times mean greater customer satisfaction and typically higher AUVs, so there is room for sales leverage if implemented successfully.

Industry-Wide Trends

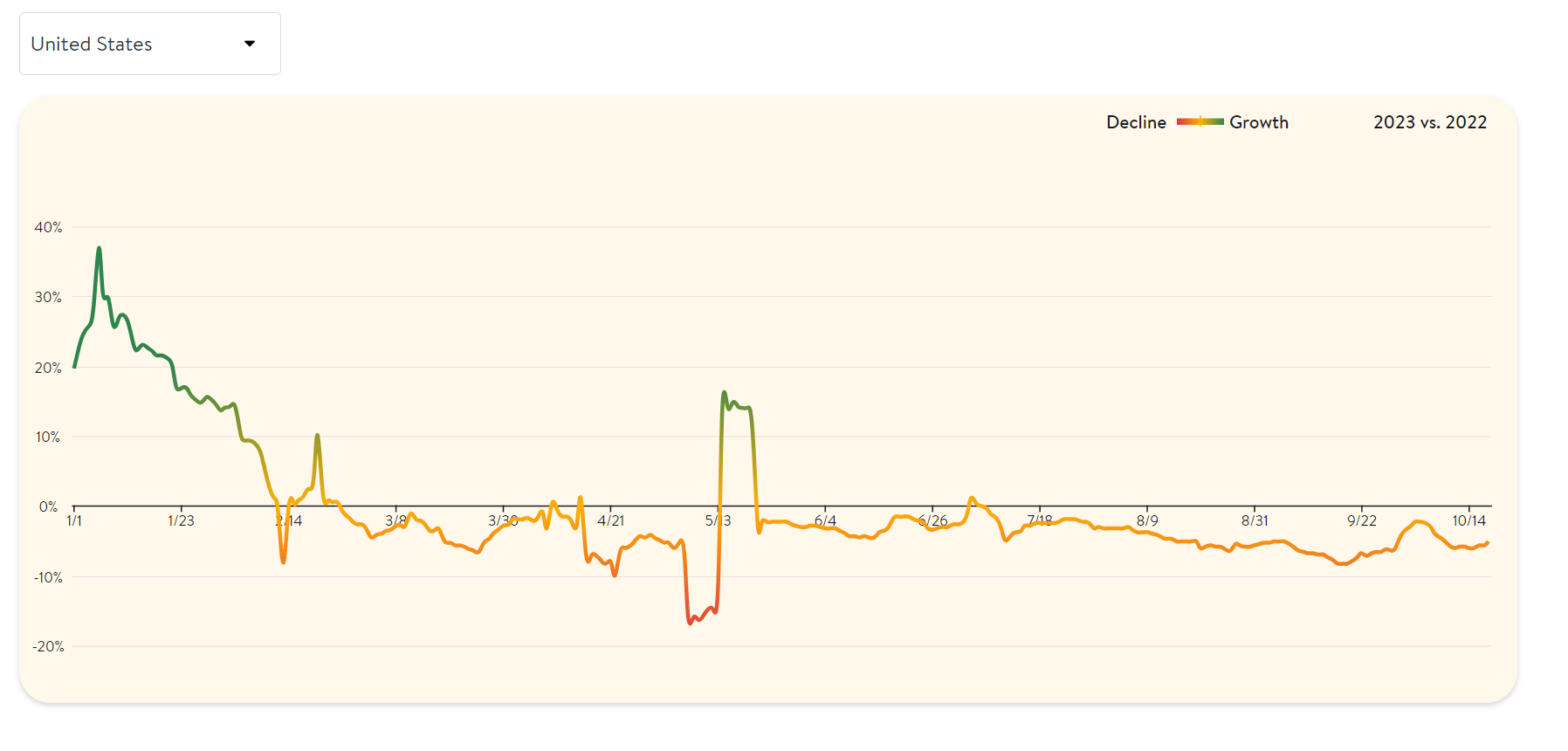

While commentary was positive overall, the solid trends weren't overly surprising given that quick-service was holding up relatively well in H1 with positive traffic that meaningfully outpacing traffic in casual dining (continuing a trend of some trading down that we've seen over the past 18 months). Unfortunately, this trend has not continued into H2 and has worsened materially recently. In fact, quick-service traffic has flipped from positive growth in June and July to down sharply in August and September, and this trend doesn't look likely to have improved in October if at all correlated with OpenTable data, which suggests that overall traffic in the industry has continued to soften. Hence, while Wendy's might have appeared set up for a beat in Q3 vs. sales estimates of $557 million judging by upbeat commentary, it's now difficult to be as optimistic.

Seated Diners Growth Year-over-Year - OpenTable

{kind=link}

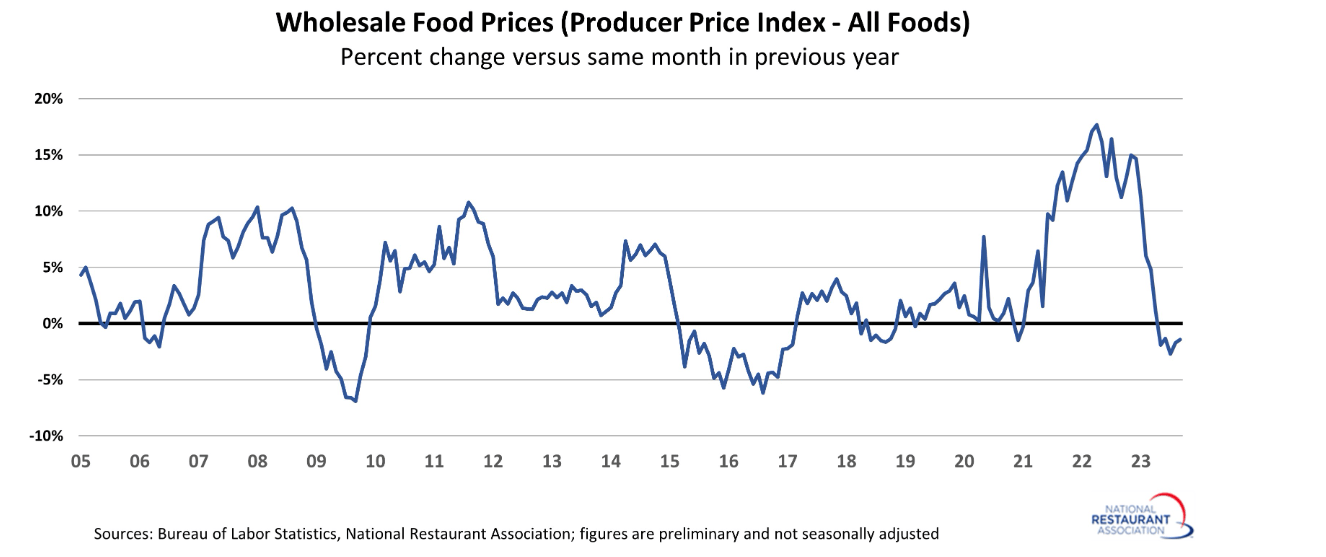

On a positive note, commodity inflation has cooled, which is helping some restaurants, and we've actually seen minor deflation in some commodities after double-digit inflation last year. That said, beef is one area that has remained elevated, which is a minor headwind for Wendy's, with beef/veal leading the commodity basket up ~21% year-over-year in September according to Wholesale Food Prices. So, although those brands with a heavier tilt towards chicken and pork are benefiting, burger names aren't seeing quite as much relief. This is a minor negative differentiator from a margin standpoint for restaurant brands with a high burger concentration, especially with Wendy's pricing being below its peers.

Wholesale Food Prices - National Restaurant Association, BLS

{kind=link}

Finally, from a labor standpoint, Wendy's and others have noted that labor is improving, with improved applicant flow and less turnover, confirmed by Wendy's in Q1, with it sharing that it saw 90-day turnover rates improving year-over-year. That said, wage inflation remains high, top-line trends aren't the most encouraging from an industry-wide standpoint, and pricing at 7-10% per year may not be as sustainable each year if we're seeing a shift in consumer behavior where even quick-service is seeing a pullback in traffic more recently (August, September numbers). And given this outlook, I see a lower likelihood of Wendy's beating its Q3/Q4 numbers, and I also think the high end of its target for 4% unit growth in 2024 is ambitious. Let's look at the valuation and see whether the risk of potentially missing on unit growth again in 2024 and a pullback in traffic is priced into the stock:

Valuation

Based on ~209 million shares and a share price of $19.30, Wendy's trades at a market cap of ~$4.0 billion and an enterprise value of ~$7.5 billion. This makes it one of the smaller capitalization names in the quick-service space, behind larger peers like McDonald's ( MCD ), and Yum! Brands ( YUM ). Meanwhile, it trades at a lower multiple than the peer group, sitting at just ~13.0x FY2024 EBITDA estimates from an enterprise value standpoint. This can partially be attributed to the company's lower unit growth rates, which are expected to come in at just ~2% this year due to continued permitting delays. However, if the stock can return to 3-4% unit growth in 2024 and 2025 like it's guided to, it's possible we could see it come back in favor and get more respect from the market, especially with its industry-leading shareholder returns (~5.0% dividend + aggressive buyback).

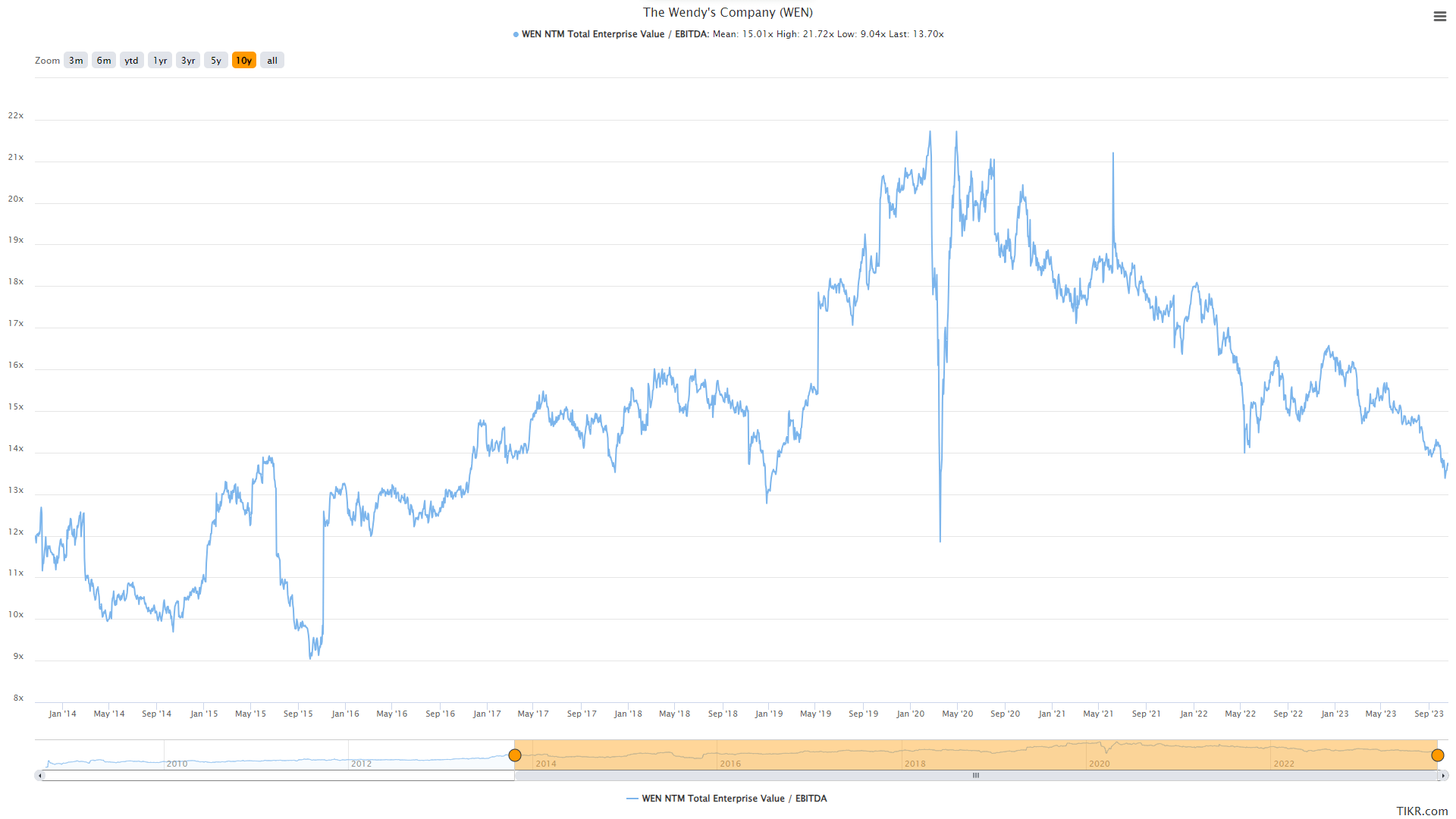

WEN EV/EBITDA Multiple & Historical Multiple - TIKR.com

{kind=link}

Looking at the chart above, we can see WEN's current valuation on an EV/EBITDA basis, which shows it trading below its average multiple of ~15.0x (10-year average). That said, I think it's hard to justify multiples of the past decade in an industry that has seen some margin damage because of above-average wage inflation and two years of near-unprecedented commodity inflation, with wage inflation remaining sticky in many markets. In addition, I think lower multiples are more appropriate in the high-rate environment we're in, suggesting a multiple of 14.0x might be more appropriate. And using FY2024 EBITDA estimates of $575 million, a fair multiple of 14.0x EV/EBITDA, and 202 million shares, WEN's fair value comes in at $23.00. Although this points to a 19% upside from current levels, I am looking for a minimum 25% discount to justify starting new positions in mid-cap names. After applying this discount, WEN's ideal buy zone comes in at $17.30 or lower.

Obviously, there's no guarantee that the stock gets this low to land in its low-risk buy zone, and it's certainly possible that the stock could bottom out in this area. However, I prefer to buy stocks when they're hated and trading deep discounts to fair value (especially if they're low-growth), and while WEN may be out of favor, it's hard to argue it's hated or trading at a deep discount to fair value just yet. Plus, the stock has an unfilled gap at $16.60, and it's had a propensity to fill its gaps in the past (08/06/19, 11/22/19, 05/05/20, 07/20/20, 03/05/21, 06/07/21). So, while the stock is certainly becoming more reasonably valued, I think the better setup to go long would be below $17.25, especially with no immediate catalyst for a re-rating given the difficult macro environment.

Summary

Wendy's reported more decent results in Q2, and it's certainly encouraging to see it reporting its highest daily breakfast sales of all time in the United States after a failed attempt at executing on breakfast previously (more SKUs, higher investment, and higher labor required in previous iteration). Meanwhile, while not a huge needle-mover, the deal with Flynn Restaurant Group in Australia for 200 restaurants through 2024 is a positive, with net unit growth in an additional market besides Canada, India, the UK, and the Philippines. Finally, the company is picking better than expected incremental sales in late-night, and while it's getting more competitive, this is another minor win. That said, while the stock is getting more attractively valued, I don't see enough margin of safety just yet. So, if I were looking to add WEN from an investment standpoint, I see the more attractive buy zone being $17.30 or lower.

For further details see:

Wendy's: A Decent H1, But A Foggy H2 Outlook