WEN - Wendy's: Good Growth Prospects Ahead

2023-06-08 15:12:01 ET

Summary

- Wendy's is expected to see revenue growth due to price increases, digital platform expansion, and a focus on breakfast and late-night sales.

- The company is poised to benefit from margin growth through price increases, moderating inflationary pressures, and productivity gains from digital-focused restaurants.

- Wendy's current valuation represents a discount to its historical average P/E ratio, and with an attractive dividend yield of 4.5%, the stock presents an appealing investment opportunity.

Investment Thesis

The Wendy's Company ( WEN ) is expected to see revenue growth as a result of price increases and its focus on leveraging digital platforms and technology to enhance the customer experience and attract new customers. The company's initiatives targeting breakfast and late-night sales are anticipated to drive market share gains. Additionally, global expansion of the restaurant footprint is expected to contribute to sales growth.

On the margin front, Wendy's is poised to benefit from price increases, the moderation of inflationary pressures, and productivity gains stemming from improved staffing and digital-focused restaurants. Furthermore, the company's current valuation represents a discount to its historical average price-to-earnings (P/E) ratio. Coupled with an attractive forward dividend yield of approximately 4.5% and a positive outlook for revenue and margin growth, Wendy's presents an appealing investment opportunity.

Revenue Analysis and Outlook

In recent years, Wendy's has experienced sales growth driven by increased consumer mobility following the easing of travel restrictions and heightened demand. The company's focus on digital and delivery channels has also contributed to customer acquisition.

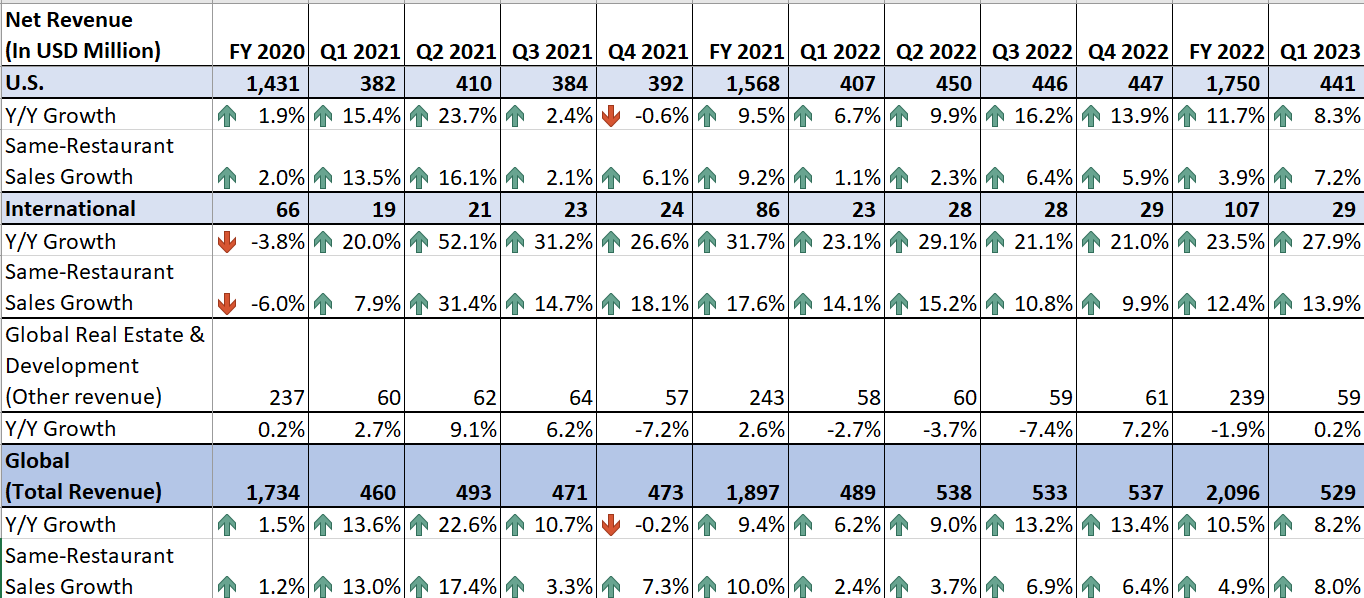

The positive sales growth trend continued in the first quarter of 2023. Wendy's achieved sales growth through expanding digital channels and benefiting from approximately 7% price increases. Additionally, the introduction of new value meal offerings led to a 1% increase in traffic. Sales growth was further supported by expansion in the breakfast offerings. As a result, net sales increased by 8.2% YoY to $529 million. On a same-restaurant sales basis, revenue grew by 8% YoY, with a 7.2% YoY growth in the U.S. and a 13.9% YoY growth internationally.

{kind=link}

WEN’s Historical Sales (Company Data, GS Analytics Research)

Looking forward, I believe WEN should continue its same-restaurant-sales momentum benefiting from price increases, growing digital channels, increasing traffic across different times of the day, and new unit expansion.

In the last few quarters, the company has been raising its menu prices to tackle inflationary input costs. These price increases are helping to boost same-restaurant sales. The company expects 7% of price increases for the full year and have plans to take further price increases in the second half of 2023. These incremental price increases and carryover impact from last year’s pricing should continue to benefit the same restaurant sales in the coming quarters as well.

In addition to increasing prices, the company is also focused on growing its digital platform. Post-pandemic digital channel has helped increase consumer awareness and brought in new customers to the brand. In the first quarter of 2023, global digital business continued to grow at a rapid pace, with digital sales increasing by more than 25% year on year and reaching a sales mix of more than 12% for total company sales. Customers in the United States and around the world are increasingly opting for online ordering, as consumer preferences have shifted significantly towards online services since COVID. This combined with Wendy's advertising campaigns to raise brand awareness, resulted in a digital sales mix of nearly 19% globally and more than 11% in the United States. Moreover, according to management, digital customer satisfaction scores significantly increased versus the prior year, and delivery wait time and order accuracy sequentially improved in comparison to the previous quarter, leading to a 5% increase in total loyalty members and a nearly 10% increase in monthly active users YoY in the first quarter.

The company also launched a one-to-one marketing program last quarter, which should aid in identifying key customer behavior and influencing customer engagement through personalized advertising. Moreover, the company is going digital, not only through online platforms but also by equipping its restaurants with digital tools to enhance customer experience. The company partnered with Alphabet ( GOOG ) ( GOOGL ) to pilot Wendy's Fresh AI, a voice AI solution for drive-through ordering that utilizes Google Cloud's generative AI and large language model technology. This should help the company increase service speed while also decreasing employee time spent taking orders and allowing them to focus on providing food service. I expect that these digital initiatives and increasing traction on online platforms to continue supporting the topline growth.

In addition to digital growth, the company’s initiatives to build its breakfast market through launching and advertising new breakfast items as well as leaning heavily on promotional efforts for breakfast items have also benefited the company in gaining a share in the breakfast market as compared to its peers. For, instance, the company launched French toast sticks and also promoted a $3 croissant in the fourth quarter which is gaining good traction among customers and is driving traffic. These initiatives aimed at boosting breakfast item sales have led to good demand for WEN’s food items and increased brand awareness. After successfully launching breakfast services in the U.S., the company launched its breakfast menu in Canada in May 2022, and according to management, it has helped Wendy’s gain market share in Canada faster than other QSR burger brands over the last year. The company expects to launch breakfast offerings in other countries internationally in the coming years, which should help it gain global market share to support sales growth.

Moreover, seeing the success of breakfast launch initiatives, the company is now also focused on the late-night market. Management believes as restrictions have fully eased and late-night traffic has returned to pre-pandemic levels, late-night offers an opportunity to bring new customers to the brand and gain market share. The company will promote various value offers and advertise its core menu focusing on late-night hours moving forward. This should also help in gaining market share moving forward and support top-line growth, as late-night binging has become a trend among young customers.

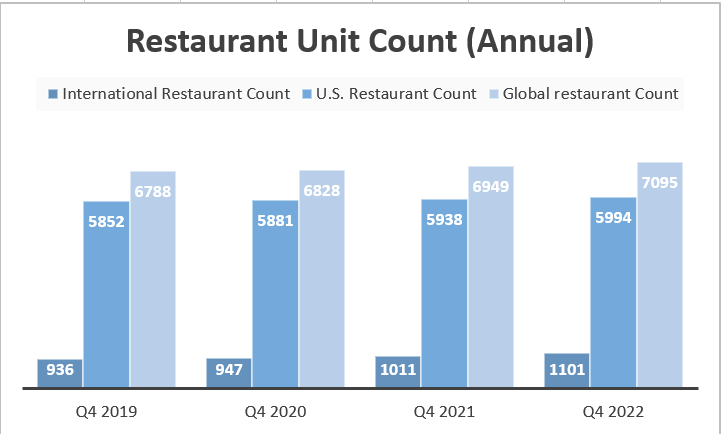

Lastly, growing new units consistently is a major catalyst to drive long-term sales growth for the restaurant sector. Over the past few years, the company has been heavily focused on expanding its global footprint as it increased international restaurants by 18% since the beginning of 2020.

{kind=link}

WEN’s Historical Annual Restaurant Unit Count (Company Data, GS Analytics Research)

The company has further plans to open restaurants both in the U.S. and internationally and targets 2% to 3% global net unit developments for 2023. It also has ~45% of the new restaurant pipeline for 2023 open or under construction through the end of the first quarter. Furthermore, the company has long-term targets of 3% to 4% global net unit growth beyond 2024 with 70% of the growth coming from international expansion. To achieve these targets the company has launched various incentive programs to improve the unit economics of new restaurants, attracting franchises across the globe to build and expand Wendy’s footprint. One example of these incentive programs is the Pacesetter Development program in the U.S. and Canada launched in February 2023, which will provide for waivers of royalty, national advertising, and technical assistance fees for up to the first three years of operation for qualifying new restaurants and reducing the payback time by 35% for two years. I expect these initiatives to expand its restaurant footprint globally should help in sales growth in the long term.

Management expects 6%-8% system-wide sales growth in 2023 driven by mid-single digit same-restaurant sales growth. I believe the guidance is achievable given the company’s price increases, growing breakfast and late-night sales, and strength in the digital channels. Moreover, I believe that the company should be able to weather tougher macroeconomic headwinds and concerns around consumer demand by attracting consumers of all income groups through its promotional and value meals across all price points. Hence, I am optimistic about WEN’s sales growth prospects.

Margin Analysis and Outlook

Since the second half of 2021, Wendy's margins have encountered challenges due to inflationary pressures on commodity and labor costs. The company has also made significant investments to support the expansion of its breakfast offerings and the development of new restaurants, which have impacted margin expansion. However, in the past few quarters, Wendy's has successfully increased its margins year over year by implementing price increases.

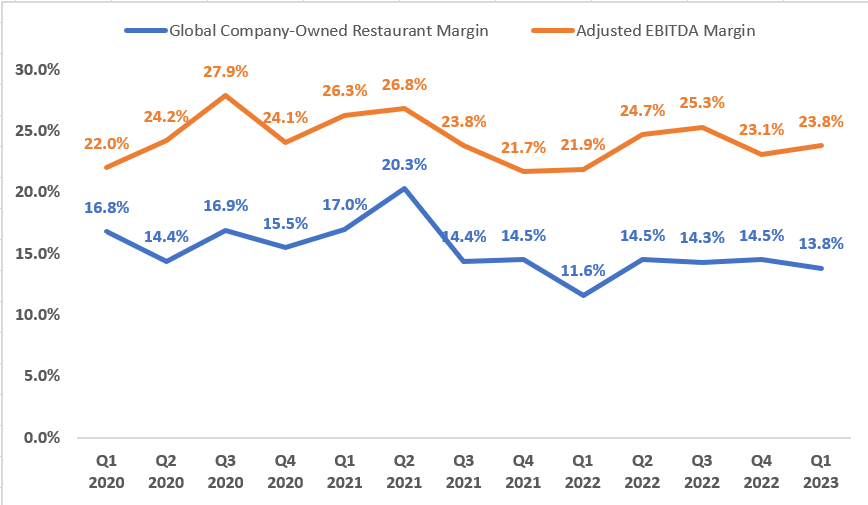

In the first quarter of 2023, Wendy's continued to face inflationary headwinds from rising commodity and labor costs, which increased by 7% and 5% respectively compared to the previous year. However, the company was able to offset these headwinds through menu price increases of 9.5%. As a result, the global company-owned restaurant margin increased by 220 basis points year over year to 13.8%, and the adjusted EBITDA margin increased by 190 basis points year over year to 23.8%.

{kind=link}

WEN’s Historical global Company-Owned Restaurant Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking ahead, I anticipate that Wendy's will be able to achieve margin growth. The additional price increases planned for the latter half of the year, coupled with the carryover impact of previous price increases, should help offset the impact of elevated costs. While commodity costs are expected to remain elevated on a year-over-year basis, there should be a sequential moderation in these costs. In the first quarter, the company experienced 7% commodity cost inflation and 5% labor cost inflation. However, going forward, Wendy's expects mid-single-digit inflation for both commodities and labor, indicating a gradual moderation in inflationary input costs and reducing the headwinds for margin growth.

Furthermore, the partnership with Alphabet to implement AI-powered tools, as mentioned in the revenue analysis, is expected to contribute to margin growth. These advanced technological tools installed in Wendy's restaurants will drive efficiencies and enhance labor productivity by saving time and improving service speed. Management anticipates that these digitally-forward restaurants will lead to a 10% reduction in operational costs, supporting margin expansion in the future. Additionally, the company is witnessing an improvement in labor turnover, which will help reduce new hiring and training costs while further boosting the productivity of existing employees. Therefore, I expect these productivity gains, along with sales leverage from increasing revenue, to contribute to Wendy's margin expansion going forward.

Valuation and Conclusion

Wendy's is currently trading at a forward price-to-earnings (P/E) ratio of 22.55x based on the FY23 consensus EPS estimate of $0.98 and 19.64x based on the FY24 consensus EPS estimate of $1.13. These valuations are significantly below its historical 5-year average forward P/E of 30.44x. Considering the company's growth prospects, it is poised for further expansion.

Wendy's strategic initiatives to strengthen its breakfast and late-night sales, allowing it to gain market share compared to its peers, bodes well for future growth. Additionally, the company's focus on digital channels and new unit expansion, coupled with the moderation of inflation, should drive both top-line and bottom-line growth.

In addition to the promising growth prospects and lower valuation, Wendy's offers an attractive dividend yield with a forward dividend yield of approximately 4.5%. This compelling dividend yield further enhances the investment case for the stock.

Given the combination of growth prospects, lower-than-historical valuation, and attractive dividend yield, I believe Wendy's stock is a good buy.

For further details see:

Wendy's: Good Growth Prospects Ahead