WEN - Wendy's Looks Reasonable Value After A So-So Year

2023-12-24 04:52:57 ET

Summary

- Wendy's has had a soft 2023, with its stock underperforming amid fairly soft same-restaurant sales growth.

- Unit economics are okay here, which should help support a continuation of modest net unit growth.

- That should be good for 4-5% annual system sales growth given a low single-digit contribution from same-restaurant sales growth.

- With a 5% dividend yield, leveraging the above into high single-digit per annum free cash flow growth can lead to solid returns for investors.

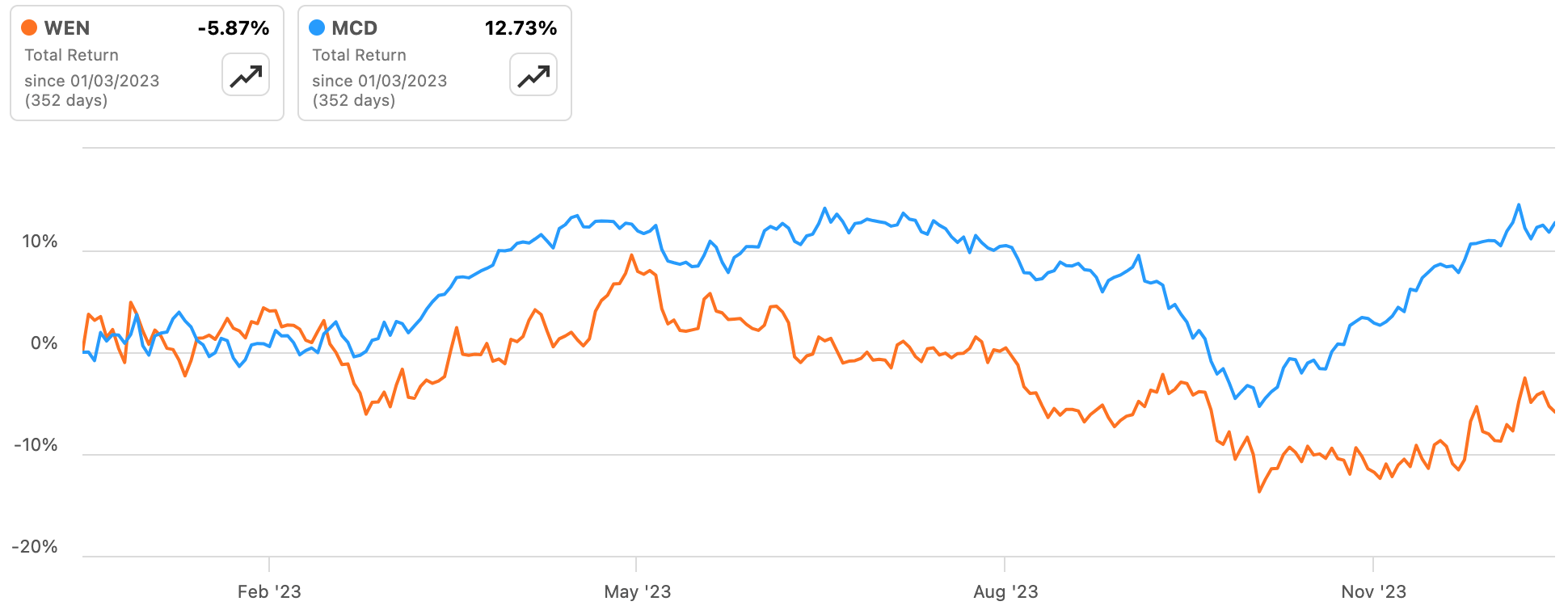

This has been a frustrating year for The Wendy's Company ( WEN ). Shares of the burger chain franchisor have fallen around 5% in that time including dividends, underperforming peer McDonald's ( MCD ) by over 18ppt amid relatively soft comps. With that leaving Wendy's on a fairly modest multiple of free cash flow and sporting an attractive 5% dividend yield, I think these shares offer just enough value to entice investors, and I open on the stock with a Buy rating.

{kind=link}

Wendy's system comprises 7,166 restaurants, 84% of which are located in the United States. The company is mainly a franchisor, with franchisees operating 94% of its restaurants as of Q3. This means the company's largest source of earnings is actually from royalty fees rather than the full restaurant-level P&L.

Through Q3, U.S. franchised stores generated $11.3 billion in total system sales on a trailing-twelve-month basis. With Wendy's reporting around 5,600 franchised stores in the U.S., average annual unit volume ("AUV") therefore lands somewhere around the $2 million mark. In terms of unit-level economics, Wendy's reported a restaurant-level EBITDA margin of 15.6% through the first nine months of the year for its company-operated stores. Franchisees typically pay 4% of sales in royalty fees to the head company, so that would mean roughly 11% restaurant-level margins on average for them. Call it roughly $220,000 in annual franchisee EBITDA per restaurant. Given the average investment needed to open a Wendy's outlet appears to land around the $1.6 million mark, this points to average unlevered cash-on-cash returns of roughly 12-13% for franchisees.

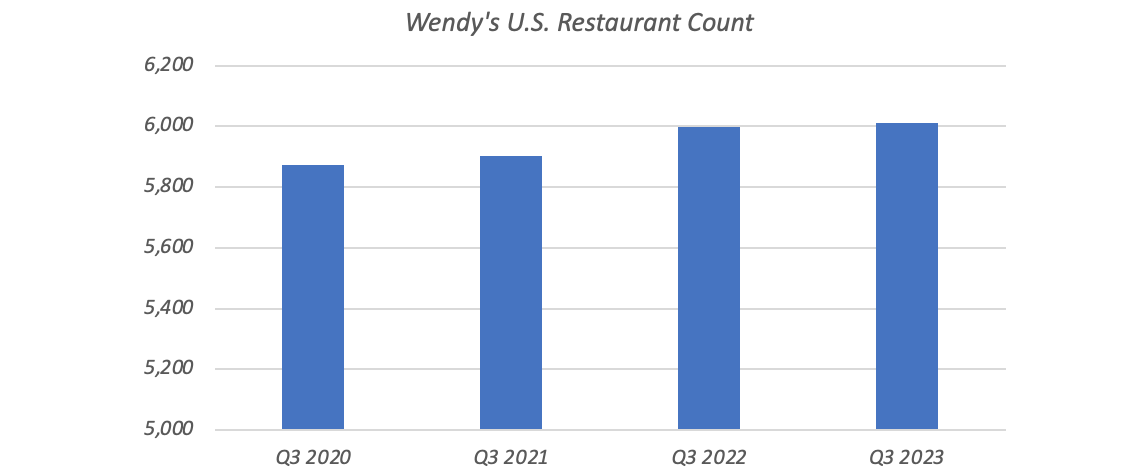

The reason I mention unit economics is to get a gauge on growth potential. Brands that generate high cash-on-cash returns are likely to spur franchisees to open up more stores. Conversely, brands with average or worse unit economics are unlikely to see much growth. 12-13% cash-on-cash returns looks just about okay, which is why Wendy's U.S. restaurant count has been tepidly expanding. Even so, Wendy's total U.S. system (~6,010 restaurants) still trails peer McDonald's (~13,440) by a considerable amount.

{kind=link}

In contrast to its domestic position, Wendy's international footprint looks fairly light to me. Unlike certain concepts (e.g. Mexican), Burger-based ones do generally travel quite well outside of the United States. McDonald's, for instance, boasts around 28,850 restaurants outside the U.S., while rival Burger King's ((QSR)) international count stands at around 12,170. In contrast, Wendy's only reported 1,156 units outside of the U.S. as of Q3. Ironically, Wendy's U.S. business is actually better business than Burger King's. AUVs are around 25% higher at the former as per my recent article on Burger King's parent company, with my calculated restaurant-level EBITDA around 40% higher for Wendy's. As a result, cash-on-cash returns are also likely to be materially higher, which is why Wendy's has been a net opener of U.S. restaurants while Burger King has been a net closer.

While you could look at this as implying Wendy's has plenty of international growth to tap into, the fact that it hasn't already would suggest to me that this is much easier said than done. Two U.S. burger chains may simply be enough for most international markets.

Wendy's recent comps have also been fairly pedestrian. U.S. systemwide same-store sales growth ("SSSG") was only 2.2% in Q3, rising to 4.7% for the first nine months of the year. That is on the low side versus peers, with McDonald's reporting U.S. SSSG of 8.1% in Q3 and 10.3% for the nine-month period. Burger King's domestic comps also landed higher, with SSSG clocking in at 6.6% in Q3 and 7.9% over the first three quarters.

Looking ahead, Wendy's growth algorithm includes mid-single-digit systemwide sales growth in 2024 and 2025, reflecting management's target of 2-3% net unit growth in 2024 and 3-4% net unit growth in 2025. It is looking to leverage that into 'high-single to low-double-digits' free cash flow growth. I think these are reasonable longer-term targets too, with low single-digit contributions from SSSG and net unit growth probably good for around 4-5% annual systemwide sales growth overall.

Franchise royalty revenue is very high margin. The $149 million that Wendy's booked in Q3 royalty sales only attracted circa $15 million in franchise support expenses. Assuming that line grows by 4-5% per annum, Wendy's revenue mix is going to shift further toward higher-margin royalties and away from lower-margin company-operated sales. That should naturally lead to an expansion in company-level margins, so growing free cash flow ahead of sales seems like a reasonable expectation to me.

For 2023, management is targeting free cash flow ("FCF") of $265-275 million, equivalent to around $1.30 per share at the mid-point. That puts the stock at a circa 15x FCF multiple based on the current $19.79 share price. This also looks quite reasonable to me. Wendy's currently pays most of this out by way of its dividend, with the current $0.25 quarterly payout mapping to a yield of over 5%. That now represents a greater than 100bps spread over the 10-year Treasury yield, which might appeal to income investors and provide some downside protection for the stock.

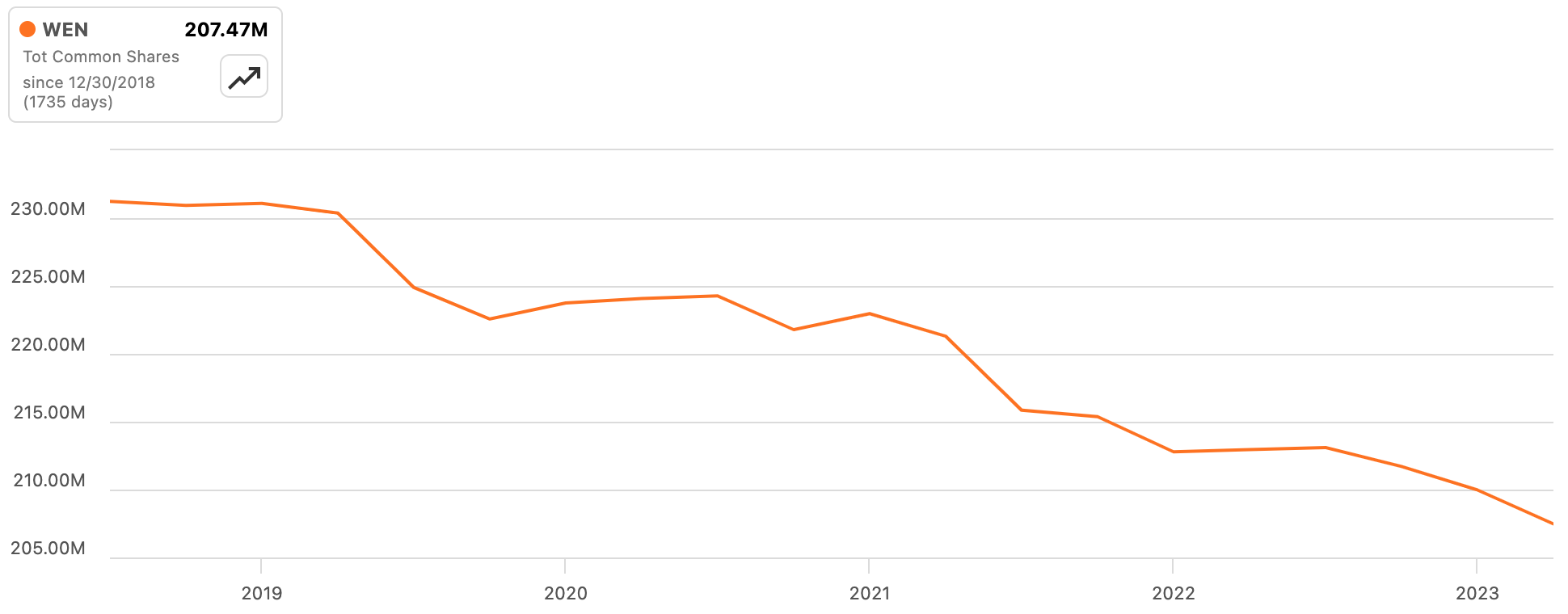

Wendy's has historically been a reasonably active repurchaser of its own shares, reducing its count by around 2% per annum over the past five years as per Seeking Alpha:

{kind=link}

The company has around $330 million left on its current buyback authorization, which expires early 2027. That would support a continuation of around 2% per annum share count reduction at the current share price, further supporting per-share dividend growth. While leverage is meaningful here, with net debt of circa $2.2 billion implying a multiple of around 4x EBITDA, the company's maturity profile is sound, with no significant repayments due before 2026 (and the rest nicely staggered after that).

I think the main risk here is to system sales growth. Restaurants can be fickle businesses, as consumer tastes and preferences can change quite quickly. Net unit growth and/or SSSG could easily land lower than anticipated, which would lead to lower system sales and ultimately FCF growth. Still, the stock's 5% dividend yield looks appealing, as does the prospect of high single-digit growth on top, and as a result I open on Wendy's stock with a Buy rating.

For further details see:

Wendy's Looks Reasonable Value After A So-So Year