WEN - Wendy's Near-5% Dividend Yield Is Quite Tempting

2023-03-09 05:13:35 ET

Summary

- Wendy's innovation efforts have worked wonders on its global same-store sales growth.

- The firm's loyal customer base keeps coming back to eat its beloved square burgers, and Wendy's has also been able to attract younger consumers.

- We're huge fans of Wendy's ~4.6% dividend yield, which remains supported by its free cash flow generation.

- The company's large debt load, intense rivalries in the burger business, and a concentrated shareholder base are concerns.

- Still, we think Wendy's is a strong idea for income consideration, but it is not without meaningful risks.

By Valuentum Analysts

Wendy's ( WEN ) has quietly executed a fantastic turnaround, and along with the fundamental improvement has come a very attractive dividend yield. Recently, the company doubled its quarterly dividend to $0.25 per share ($1.00 annualized), which now amounts to a forward estimated dividend yield of ~4.6%. McDonald's ( MCD ) and Chick-fil-A may be dominating the fast-food landscape, but Wendy's is doing more than just holding its own.

As measured by traffic share, Wendy's is currently the second-largest quick-service food provider in the hamburger category, and that means that rivals will always be fighting to gain share against the company. The number of competitors in the hamburger segment are too many to count, but in our view, very few have the momentum of Wendy's financials at the moment.

At the end of the third quarter of 2022, more than 400 Wendy's locations were operated by the firm, while nearly 5,600 were operated by franchisees. We like the rich royalty streams earned by Wendy's mostly-franchised revenue model, but the company still remains exposed to inflationary pressures via its owned restaurants. Though last year was difficult on its profit levels, the firm showed a near-300 basis point increase in its company-operated restaurant margin in the fourth quarter of 2022 versus the first quarter of that year.

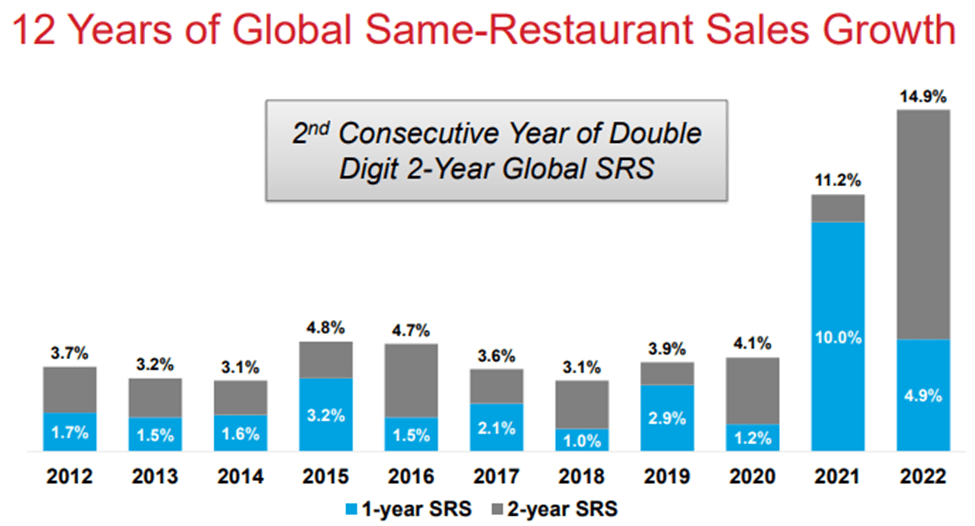

That's not all. 2022 also marked the second straight year that worldwide same-restaurant sales advanced double-digits on two-year stacked basis, as it opened 275 restaurants across the globe. Nelson Peltz of the Trian Fund is also the largest shareholder of Wendy's, and the famous investor is "strongly supportive of (Wendy's) capital allocation strategy." For investors seeking a large dividend payer in the restaurant arena, Wendy's ~4.6% dividend yield could be a very interesting idea.

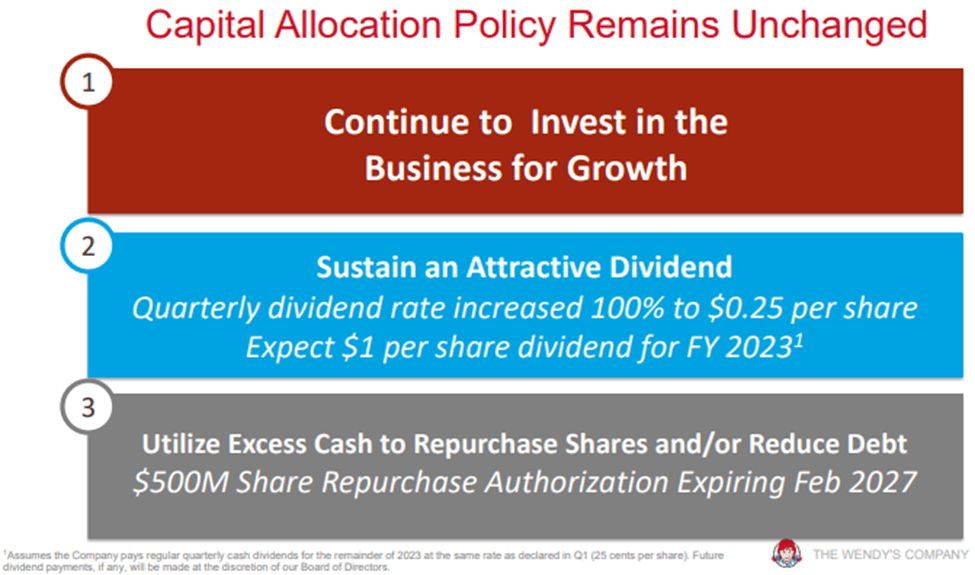

Wendy's capital allocation policies remain attractive. (Image Source: Wendy's)

{kind=link}

It may be difficult to believe given how long Wendy's has been around relative to some new burger concepts, but the company's same-restaurant growth has been highly encouraging of late. In the U.S., for example, same-restaurant sales growth jumped 3.9% for the full year 2022, and this followed a 9%+ increase in 2021. International same-restaurant sales growth also was impressive for the year, advancing more than 12% after an impressive near-18% leap in 2021.

In the past, we've been hesitant to think of Wendy's of the caliber to be included in the so-called "burger wars" between McDonald's and Burger King ( QSR ), but we think that has changed of late. Burger King, for example, has struggled to connect with fast-food goers more recently, in our view, while the strength of Wendy's profits has been solid. Adjusted EBITDA at Wendy's advanced ~20% during the fourth quarter of 2022 and 6.6% for the full year.

Innovation Has Been the Key to Wendy's Success

Wendy's has become one of the best innovators out there in the restaurant business, in our view. The company may not have innovated as well as perhaps Taco Bell during the latter part of the 2010s, but Wendy's chili, baked potatoes, fresh salads, and Frosty desert remain favorites. Kids absolutely love its Frosties!

The company's burgers perhaps aren't as liked as McDonald's Big Mac or Burger King's Whopper either, but Wendy's nonetheless has carved out a loyal following. The firm's marketing endeavors have been resonating, too. Recently, Wendy's reinvented Friday the 13th into FRY-day the 13th, which offered a free order of fries to customers with a purchase. The promotion is just one example that has kept hungry fast-food goers coming back to Wendy's.

Wendy's has also made some interesting moves with its menu, too. The restaurant's Italian Mozzarella chicken sandwich, pretzel bacon pub cheeseburger, and new peppermint and strawberry Frosties have been extremely successful, in our view, as has been the launch of its French Toast sticks for breakfast.

Though it is clearly difficult for restaurants to compete with McDonald's 2 for $2 sausage McMuffins for breakfast, Wendy's has done well with its 2 for $3 croissant marketing initiatives. Wendy's digital efforts have also been effective of late, and its recent surge in global same-restaurant sales expansion has been nothing short of awesome.

Wendy's same-store sales have surged of late. (Image Source: Wendy's)

{kind=link}

Some of Wendy's strength can probably be attributed to the WallStreetBets crowd and their use of the term "tendies," which has become another name for Wendy's chicken nuggets, but things, in our view, are looking up and up at the fast-food restaurant chain.

Wendy's Capital Allocation Priorities Remain Sound

We think Wendy's capital allocation policy is sound, too, and it breaks down into three core components: 1) to drive expansion in the operations, particularly pursuing growth in its breakfast daypart, 2) accelerate its digital and rewards platform, and 3) grow its restaurant portfolio. Here's how the company describes its three pillars of growth in a recent 10-Q :

Breakfast

Wendy's long-term growth opportunities include investing in accelerated global growth, which includes building upon our breakfast daypart. Since the launch of breakfast across the U.S. system in March 2020, systemwide sales have benefited from this new daypart, with average weekly U.S. breakfast sales representing approximately $2,600 per restaurant during the nine months ended October 2, 2022. The Company launched breakfast in Canada in May 2022, which has increased the percentage of global systemwide restaurants serving breakfast to approximately 95%. The Company expects to fund a total of $16.0 million of incremental advertising during 2022 to support the breakfast daypart, which the Company expects will continue to drive trial and acceleration of the Company's breakfast offering in the U.S. and Canada.

Digital

Wendy's long-term growth opportunities include accelerated implementation of consumer-facing digital platforms and technologies. The Company has invested significant resources to focus on consumer-facing technology, including activating mobile ordering via Wendy's mobile app, launching the Wendy's Rewards loyalty program and establishing delivery agreements with third-party vendors. The Company's digital business represented approximately 10.1% of global systemwide sales during the nine months ended October 2, 2022. The Company is also partnering with key technology providers to help execute our digital, restaurant technology and enterprise technology initiatives and support our technology innovation and growth.

New Restaurant Development

Wendy's long-term growth opportunities include expanding the Company's footprint through global restaurant expansion. To promote new restaurant development, the Company has provided franchisees with certain incentive programs for qualifying new restaurants, including technical assistance fee waivers and reductions in royalty and national advertising payments. In addition, the Company has development agreements in place with a number of franchisees that contractually obligate such franchisees to open additional Wendy's restaurants over a specified timeframe.

During the nine months ended October 2, 2022, the Company and its franchisees added 131 net new restaurants across the Wendy's system. During the first nine months of 2022, the Company reevaluated its development plans resulting in a reduction in its expected net new restaurant growth, primarily related to non-traditional restaurants. As a result, the Company now expects net new restaurant growth of 2.0% to 2.5% in 2022 and expects to reach 8,000 to 8,500 systemwide restaurants by the end of 2025 (as of October 2, 2022, the company had 7,080 restaurants in its system).

We're fans of Wendy's capital allocation approach, which includes targeting a dividend payout ratio of greater than 50%, and such a target has been supported by free cash flow generation, too. For example, during 2022, Wendy's hauled in $259.9 million in cash flow from operations, while it shelled out $85.5 million in capital expenditures, good for $213.1 million in free cash flow (after adding back its advertising funds impact of ~$38.8 million), which handily covered its ~$106.8 million in dividends paid over this time period.

{kind=link}

The company ended 2022 with $745.9 million in cash and cash equivalents, and while the company has a large ~$2.8 billion long-term debt position, its liquidity supports the payout, and excess free cash flow can be used to pare down its debt to more comfortable levels in coming years. Looking to 2023 , global systemwide sales growth is expected in the range of 6%-8%, while free cash flow is targeted in the range of $265-$275 million, which is meaningfully higher than the $213.1 million mark in 2022. Free cash flow growth for 2024-2025 is expected in the high-single to low-double digits, a pace of expansion we like.

Concluding Thoughts

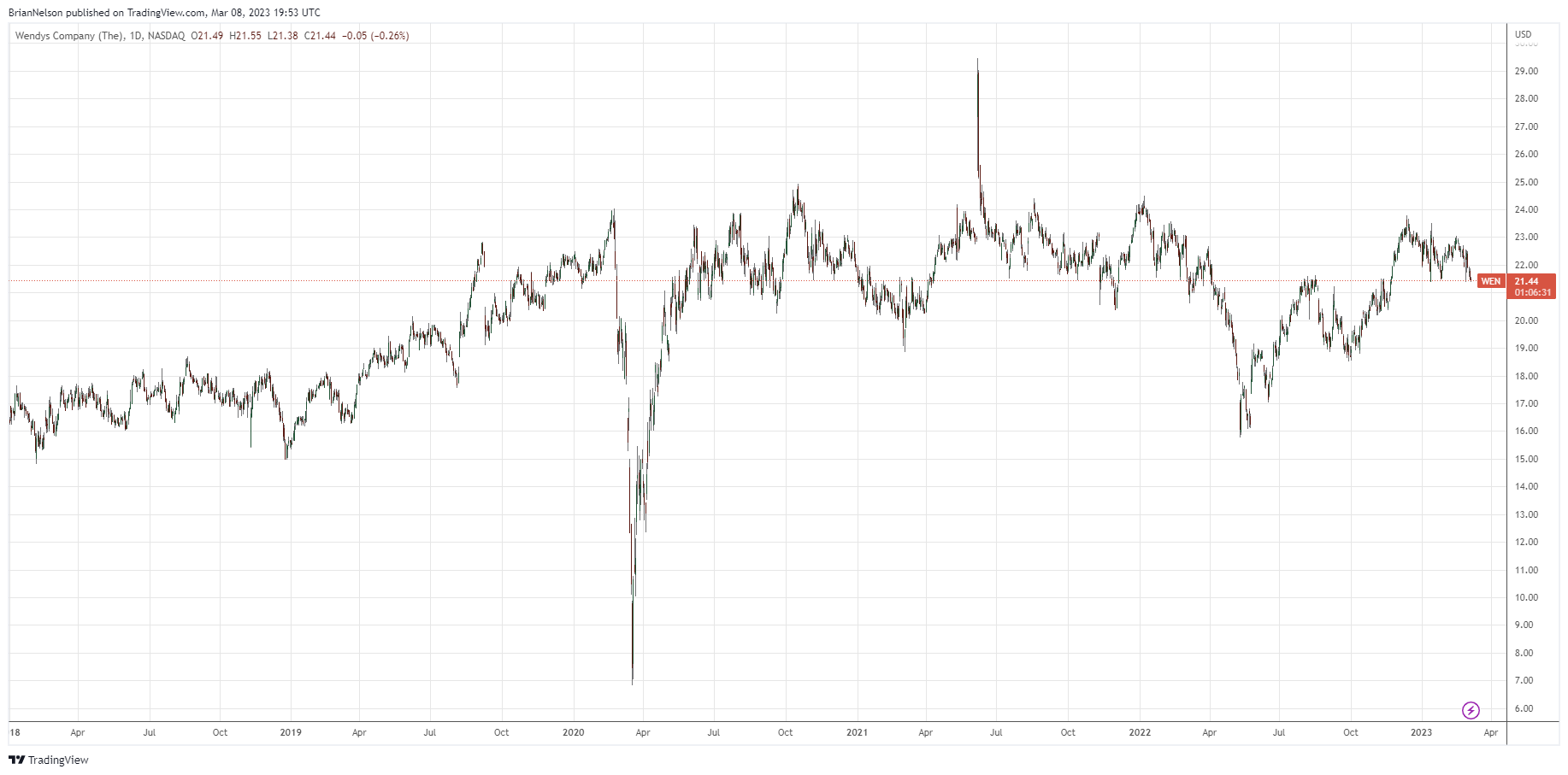

Wendy's shares have traded sideways and could be poised to breakout if the market backdrop remains strong. (Image Source: TradingView)

{kind=link}

Rivals in the burger business remain intense, especially McDonald's, but Wendy's has staying power, in our view, and we think its dividend does, too. Shares yield ~4.6% at the time of this writing, and we like the risk/reward as the broader market has priced in a lot of the risks behind Fed rate hikes, which while not done yet, will likely be more measured going forward.

Put simply, Wendy's is looking pretty good. The firm's customers keep coming back due to its innovation efforts, and it has ridden the social media wave to bring in the younger consumer, while its fresh-never-frozen, square hamburgers still please long-time customers.

The fast food company's expansion into the breakfast daypart has been a solid catalyst as well, and its digital and reward efforts are doing well. We're not too excited about Wendy's large debt load, but it has a solid cash position, and free cash flow comfortably covers its payout. We think Wendy's is a solid income idea.

For further details see:

Wendy's Near-5% Dividend Yield Is Quite Tempting