WFG - West Fraser: Expecting Momentum To Continue Post Upcoming Q2 Earnings Report

2023-07-18 22:36:26 ET

Summary

- We have maintained a 'Buy' rating in West Fraser due to its strong return on capital trends, low valuation, and bullish technicals, despite shares remaining rangebound for 18 months.

- The company generated $1.446 billion of operating cash flow over the past four quarters, with a trailing 12-month free cash-flow number of $963 million, indicating a strong profitability trend.

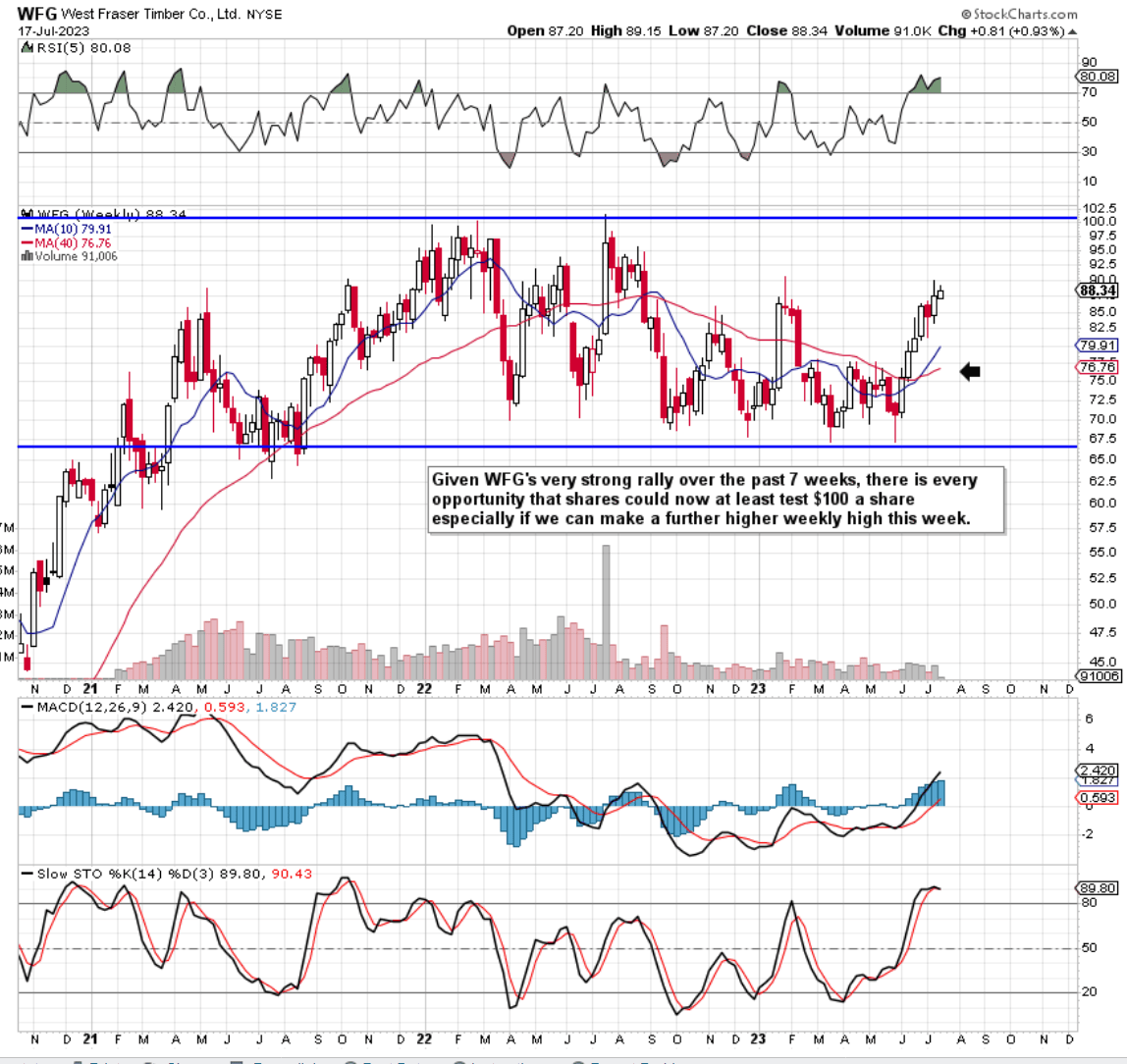

- West Fraser is currently trading with a trailing free-cash-flow yield of almost 13% and an adjusted return on capital of over 20%, with shares in bull mode over the past seven weeks.

Intro

We wrote about West Fraser Timber Co. Ltd. ( WFG ) approximately 12 months ago when we initiated a 'Buy' rating on the stock just prior to the announcement of the company's fiscal second-quarter earnings of 2022. Strong return on capital trends, a low valuation, as well as bullish technicals, led us to believe that an earnings beat was on the cards (which consequently would lead to a higher share price over time).

Although management announced an earnings beat for the second quarter last year (Q2 GAAP EPS of $7.59), shares failed to push on once the numbers became known. In fact, shares have remained rangebound for the best part of 18 months now, although recent share-price action has been really encouraging. We state this because of the strong rally we have seen over the past seven weeks or so, resulting in a bullish crossover of the stock's intermediate MACD indicator. Suffice it to say, if shares can print a further higher high this week, it would stack the odds in favor of West Fraser of at least testing its 2022 highs of approximately $100 a share.

{kind=link}

Cheap Free Cash-Flow

Therefore apart from the bullish technicals which we have in play, we are reiterating our 'Buy' rating in WFG due to how the relationship between the stock's valuation and profitability trends continues to stack up. If we look at free cash flow, for example, we see that West Fraser generated $1.446 billion of operating cash flow over the past four quarters. When we subtract capital expenditure of $483 million, we get a trailing 12-month free cash-flow number of $963 million. When we divide this number into WFG's current market cap of $7.44 billion, we get a very attractive trailing free cash-flow multiple of 7.72. A few takeaways, we can garner from this multiple.

Firstly, management on the recent Q1 earnings call went into its capital allocation strategy where sustained investment, debt reduction, and shareholder compensation remain priorities at the firm. In fact, since 2016, the lion's share of the company's cash flow has been diverted to shareholders (Through dividends & buybacks). Suffice it to say, given how shareholder equity has expanded quite rapidly in recent times, it is evident that management's goals are aligned with the company's shareholders (which is a trend that is always welcome).

Secondly, in terms of the free cash-flow multiple discussed above, this multiple essentially demonstrates the cost at which West Fraser can generate cash flow. This means long investors currently receive just under $0.13 of free cash flow for every dollar invested in the company. This is a great start because as mentioned, these funds can be used to continually reward shareholders as well as invest in growth opportunities when they arise.

Return On Capital

Being able to generate consistent cash flow is one thing but allocating that capital in order to generate high returns on capital numbers is another story altogether. However, when we look at WFG's strong balance sheet and see the operating income which continues to be generated from the company's assets, we continue to see strong profitability trends and above-average returns on capital.

At present, West Fraser's trailing reported return on capital percentage comes in just below 8%. However, by using the formula below, we can eliminate the ramifications of the interest coverage ratio on the income statement as well as WFG's tax rate which can vary over time. The formula's denominator only focuses on the assets which contribute to the company's earnings (Meaning the company's cash balance is excluded on the working capital side).

{kind=link}

Therefore by dividing WFG's trailing 12-month EBIT of $1.093 billion by the sum of the company's net working capital & net fixed assets ($1.087 billion + $3.987 billion), we get a very impressive adjusted trailing ROC of 21.54%.

Conclusion

To sum up, West Fraser stock is currently trading with a trailing free-cash-flow yield of almost 13% and an adjusted return on capital of well over 20%. Furthermore, shares have been in bull mode over the past seven weeks so it will be interesting to see if the company's upcoming second-quarter earnings report can keep the momentum going. Earnings revisions over the past 30 days have stabilized somewhat which is encouraging. We look forward to continued coverage.

For further details see:

West Fraser: Expecting Momentum To Continue Post Upcoming Q2 Earnings Report