WFG - West Fraser Timber: Why I'm Buying After Earnings

2023-05-03 08:34:55 ET

Summary

- West Fraser Timber announced its Q1 2023 results on April 25, which came in below forecasts.

- The company has had a history of balanced capital allocation and has returned capital to shareholders via dividends and buybacks in the past.

- West Fraser stock trades at a discount to its mid-cycle average multiple and is well positioned to navigate a challenging demand environment with its strong balance sheet.

(Note: all '$' figures are CAD, not USD, unless stated otherwise.)

Introduction

After record prices of over $1400 per thousand board feet, lumber prices have now fallen to $350 which have led to negative earnings for producers like West Fraser Timber ( WFG:CA ). Following record years of profitability in 2021 and 2022, the company has experienced weak quarters as market fundamentals have deteriorated and as timber prices have fallen.

However, while some investors may view the weak quarters and negative earnings as cause for concern, West Fraser has been balanced in its capital allocation strategy and conservative with its balance sheet which have situated the company as well-positioned to navigate a challenging demand environment. With its strong track record of profitability and ability to weather difficult market conditions in the past, I believe the company is prepared to come out ahead when the market turns around.

Recent Quarter

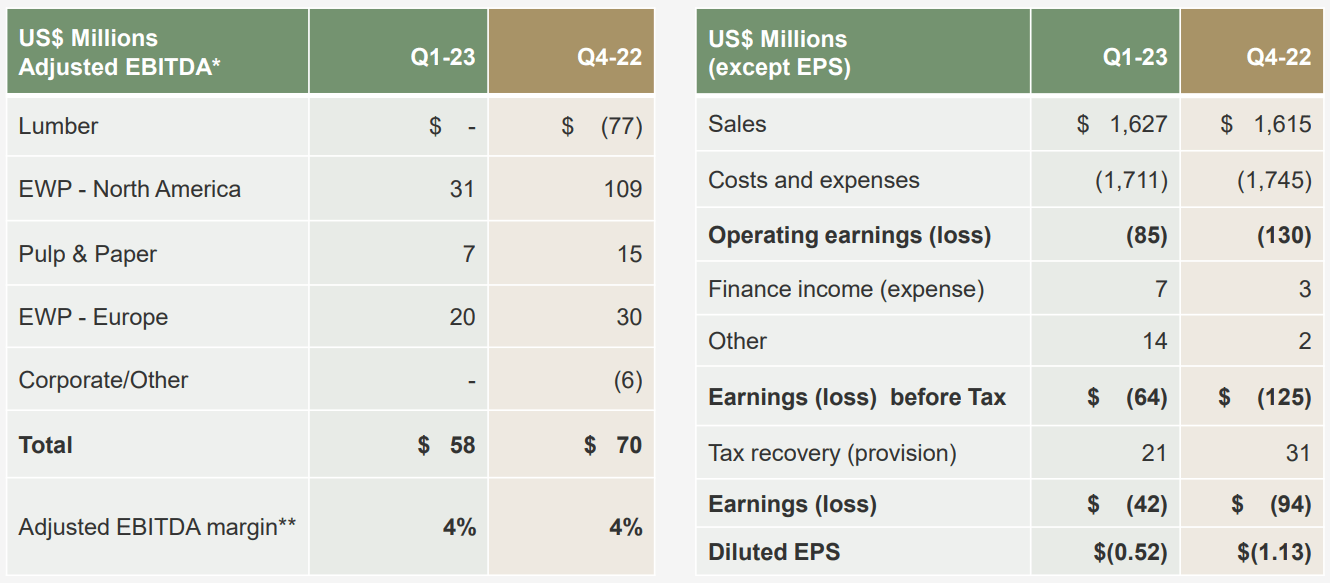

On April 25, West Fraser announced its Q1 2023 results with earnings per share coming in at -$0.52 USD a miss of $0.42 USD. Much of the weakness in the quarter (along with previous quarters) has been as a result of softer demand in the lumber space. EBITDA for the lumber segment was basically zero as a result of lower lumber prices despite a positive tailwind from inventory revaluations from the prior quarter ($45 million) and cost relief from lower BC and Alberta stumpage and less competition for US South logs. While Western Canada lumber shipments were up 11% and 9% respectively for the quarter, they were essentially flat year over year. On the earnings call , management noted that it is sticking with its current shipment and capex guidance ranges ($500 million to $600 million of capital expenditures in 2023), after having had negative revisions to guidance in the previous two quarters.

Quarterly Financial Results (Investor Presentation)

{kind=link}

One thing I would note is that with negative earnings, quarter over quarter results don't matter much when we are in the trough of the market cycle. After record profits last year and in 2021 for the company, we are likely close to the bottom of the market cycle than we are to a mid-cycle. With lumber prices now below $350 per thousand board feet, North American lumber markets are struggling for traction and it's likely that current prices remain below cash costs, even as log costs moderate. In my view, this is temporary and not sustainable. With various sawmill closures, particularly in BC, West Fraser has not been immune and has also announced curtailments at Cariboo Pulp and Paper.

Outlook

Going forward, the lumber industry is likely to continue to see challenges in the coming months leading us into the end of the year. With further rate hikes from central banks, ongoing labor tightness, and the potential for softer demand due to housing affordability, West Fraser faces pressure on its earnings and profitability in the near term.

However, there are some positives as well. Inflationary cost pressures have moderated across much of the supply chain, including raw materials such as energy, resins, chemicals and fiber. The company expects this trend to continue through the remainder of 2023. While this may alleviate some of the cost pressures faced by the company, it remains to be seen whether it will be enough to offset the challenges outlined above.

One positive development is that inflationary cost pressures have eased in many parts of the supply chain. This includes raw materials such as energy, resins, chemicals, and fiber, which are all critical inputs in the production of wood building products. On the earnings call, management anticipates that this trend of moderated cost pressures will continue throughout the rest of 2023.

In my view, this could potentially provide some relief to the company's bottom line, as it may result in lower input costs and improved profitability. With mortgage rates easing and homebuilders indicating that the spring season is improving , this may indicate that much of the pain may be in the rear view mirror.

Balance Sheet and Capital Allocation

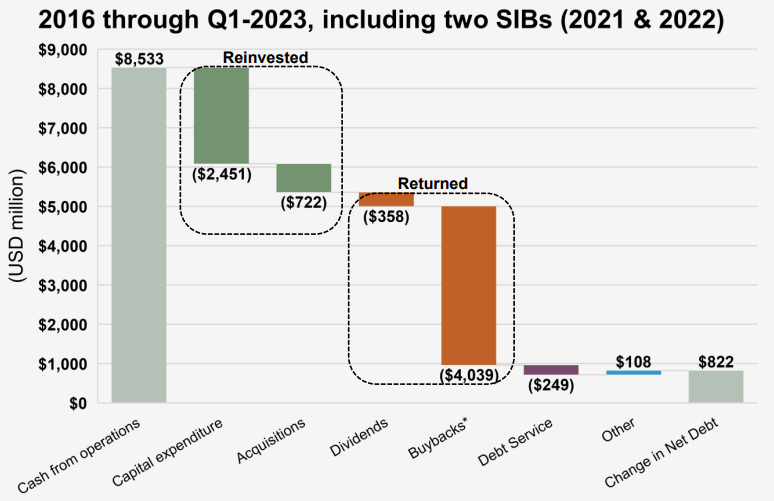

West Fraser has a track record of disciplined and balanced capital allocation and has the balance sheet to weather any potential headwinds. Since 2016, about 51% of cash flow has been returned to shareholders via dividends and share repurchases, 29% reinvested back into operations, with the remaining cash retained or used for debt reduction. Its average share repurchase price in 2021 and 2022 was $95.25 and $112.98, respectively, both of which are above the current share price. While the company has currently paused buybacks, I expect West Fraser will resume buybacks sometime next year, should the market improve and management continuing to view share repurchases as an appropriate return of capital.

Capital Allocation (Investor Presentation)

{kind=link}

On the balance sheet front, West Fraser has $1.1 billion USD of available cash with another $1 billion USD available on bank lines. Debt to Equity is very low at 7.1% however its debt (comprised of senior notes at 4.35% and a floating interest rate term loan) matures in the back half of 2024, which is likely why West Fraser has maintained a large cash position. I view this conservative approach to the balance sheet as important for the company, as it provides the company with a strong financial position to weather any potential challenges or uncertainty in the market. With low leverage ratios and available cash it can draw on through its revolver, I believe West Fraser has a significant cushion to cover any unexpected expenses or short-term cash needs.

Valuation

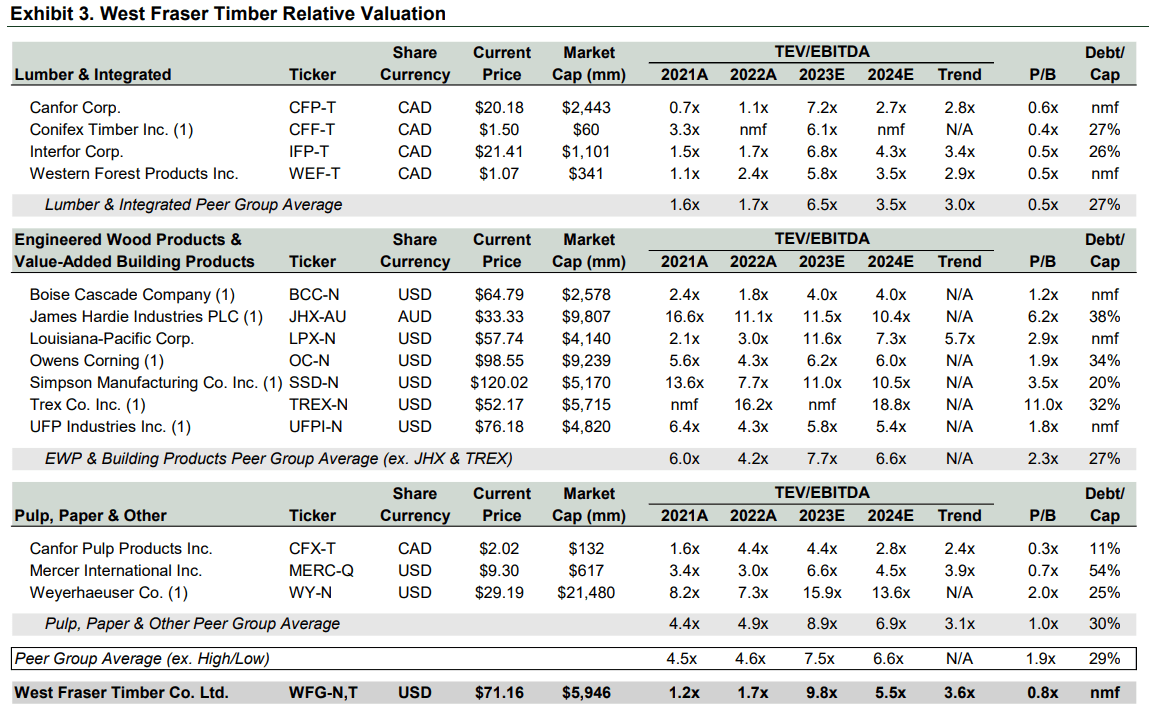

It's difficult to value West Fraser, considering it overearned in 2021 and 2022 with high lumber prices and is reporting negative earnings now with activity in the space down considerably. When looking at 2024 estimates, the company is trading at about 5.5x 2024 EV/EBITDA which is a fairly reasonable valuation in a mid-term cycle. As the long-term average trend multiple is about 6.0x and shares basically unchanged over a 5 year period, the company seems like a decent buy at the current price. While it does trade at a premium compared to its Lumber & Integrated peers, West Fraser has lower debt and has had a higher ROCE of ~25% since 2016. It trades at around a 1 turn discount to its Engineered Wood Product and Pulp & Paper peers.

{kind=link}

Conclusion

In summary, West Fraser has demonstrated that it can perform well in both good markets and bad markets. With lumber prices having now stabilized after a wild 2021 and 2022, demand has fallen considerably which has put a damper on earnings in the near term. While the company is seeing short-term pressures from rate hikes, labor tightness, and ongoing issues related to housing affordability for consumers, inflationary pressures are easing and West Fraser is in a strong position to weather any near term headwinds with its balance sheet. With a proven track record of balanced capital allocation and the outlook for 2024 unchanged, I believe taking a contrarian view and buying at the trough of the market cycle makes sense for long-term investors.

For further details see:

West Fraser Timber: Why I'm Buying After Earnings