WAL - Western Alliance: Now Trading At Book Value (Downgrade)

2023-09-14 01:57:25 ET

Summary

- Western Alliance Bancorporation shares have surged as market conditions in the regional banking sector have normalized.

- The bank has seen significant deposit inflows in Q2, resulting in a restoration of investor confidence.

- With shares of WAL now trading at book value, I have decided to close my position and take profits.

I aggressively recommended to buy shares of Western Alliance Bancorporation ( WAL ) after the regional bank saw its valuation crash following the implosion of Silicon Valley Bank in March. My core argument has been that the market turned too bearish on Western Alliance Bancorporation as well as on the broader regional banking market, resulting in an attractive risk profile for the community bank as well as significant upside potential. Shares have indeed surged as conditions in the regional banking market normalized in the last couple of months: confidence has been restored and clients are no longer pulling cash out of Western Alliance. While there may be some upside left on the table, I have decided to close out my position in Western Alliance as shares managed to claw their way back to a book valuation!

Previous rating

I recommended Western Alliance a few times since March, most recently in July after the bank reported Q2 earnings: 5.1x FWD P/E , Strong Deposit Trends, Upside Potential. The reason: I saw a unique opportunity to capture upside potential in the battered community bank's shares after investors' confidence in the sector got obliterated in March. Mostly, the thesis was driven by the recognition that shares of Western Alliance were undervalued as they were selling at a large discount to book value and that the bank was already seeing favorable deposit flows in its core business.

Fundamentally, this has changed since shares are now trading at book value which I believe limits further upside potential. For this reason, I am personally closing my long term thesis. However, investors that invest for the long term may hold on to shares as the reduction in short term borrowings could prove to be accretive to the regional bank's net interest margin going forward.

A key driver of Western Alliance's revaluation: deposit base restoration

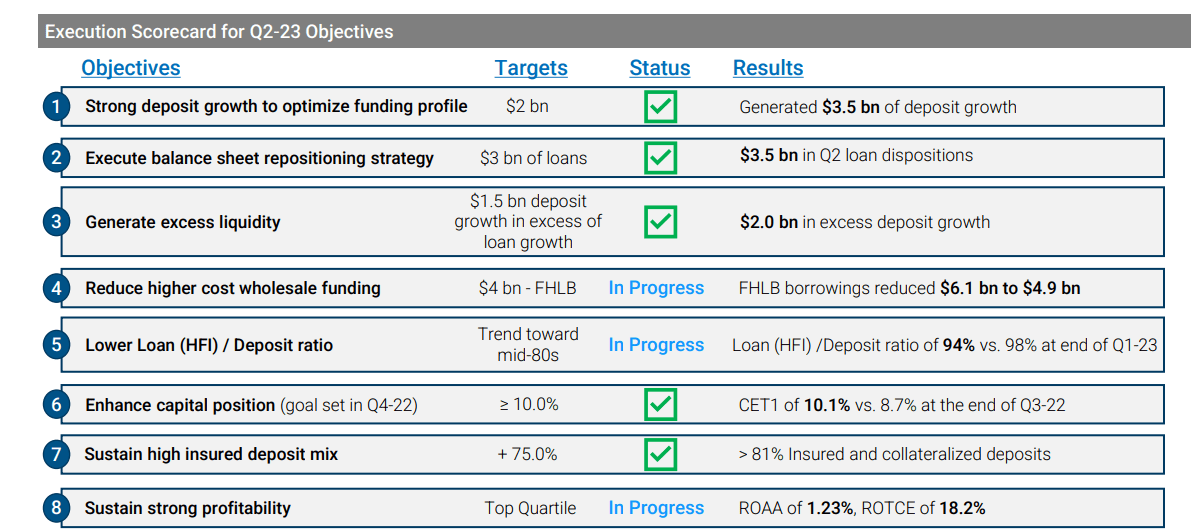

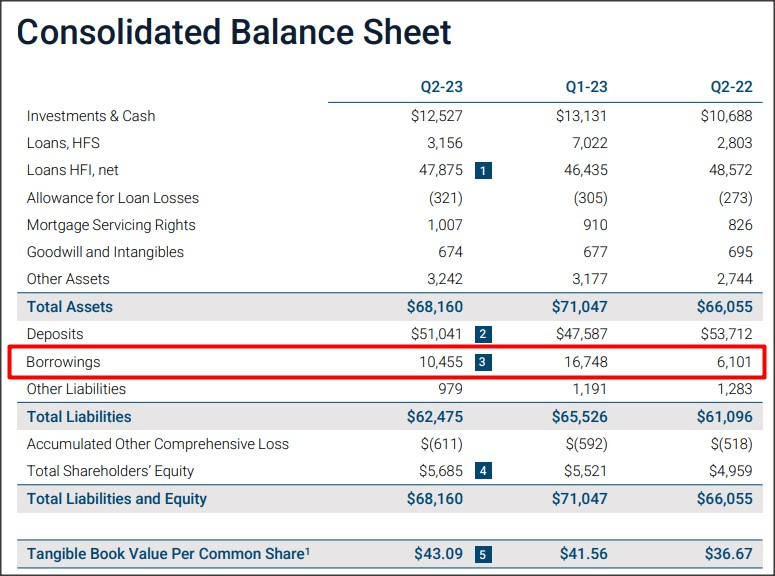

As I indicated in my last work on the regional bank, Western Alliance saw $3.5B in deposits flowing back to the bank in the second-quarter, in part because clients regained confidence that their deposits were safe. Achieving strong deposit growth was one of the most important take-aways of Western Alliance's Q2'23 report and I believe that Western Alliance may be able to further grow its deposit base. Total deposits were $51.0B at the end of the second-quarter and down $2.6B since the end of FY 2023. Still, Western Alliance managed to attract deposits back to its balance sheet which I considered to be a major win. However, I also believe that the big money now has also already been made with shares of Western Alliance seeing a huge revaluation since March.

{kind=link}

A new value driver may emerge: balance sheet deleveraging

What could be a value driver for Western Alliance going forward could be a change in funding mix. Like many other regional banks, Western Alliance increased its short term funding from the Fed as well as the Federal Housing Loan Banks in order to be prepared for deposit withdrawals, especially in its venture segment. With the situation in the regional bank market now stabilizing, Western Alliance could lower its borrowings going forward, thereby removing a costly funding source from its balance sheet.

Western Alliance Bank Corporation has seen a drastic increase in its borrowings in the first-quarter. Borrowings in Q1'23 soared to $16.7B, although the regional bank repaid $6.3B in the second-quarter and should be able to gradually reduce its borrowings to the Q4'22 level of around $6.1B. The removal of a costly funding source would likely improve Western Alliance net interest margin and boost the bank's book value growth.

{kind=link}

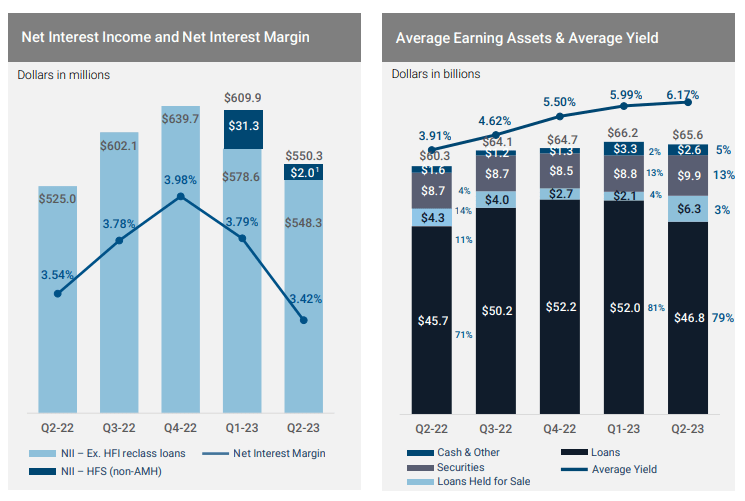

The bank's net interest margin declined 37 basis points to 3.42% in the last quarter, partially because the bank put more short term borrowings on its balance sheet. According to the bank's guidance, Western Alliance sees a net interest margin of 3.50-3.60% in the second half of the year, so an uptick in NIM is expected. I don't expect Western Alliance to sell any more loans (the bank did so in Q2 in order to raise cash for its balance sheet restructuring). In fact, I believe Western Alliance may have some surprise potential if the bank continues with its deleveraging in the second half of the year.

{kind=link}

Western Alliance: now finally trading at book value

Western Alliance traded at a truly excessive discount to book value in the early stages of the regional banking crisis in March of this year, but shares have recovered to about $50 now, up from a 1-year low of $7.48. Shares of Western Alliance are now trading at a comparatively small 13% discount to the 1-year average P/B ratio. While there may still be some upside left on the table here, I believe Western Alliance has already had an extremely impressive run lately. Shares are now trading at book value and I have taken profits. While I took profits with Western Alliance, I still own other regional banking franchises such as U.S. Bancorp ( USB ) ( Source ) or KeyCorp ( KEY ) ( Source ).

Risks with Western Alliance

There is a certain risk with a sell recommendation insofar as Western Alliance's recovery rally may continue. The bank has been one of the most punished regional banks during the March meltdown and the bank may have more upside, especially if the bank puts a solid Q3'23 earnings report on the table and focuses on reducing its short term borrowings. Since shares have revalued to book value, the risk profile has deteriorated.

Final thoughts

Western Alliance has seen a major share price re-evaluation since I first recommended the regional bank in March. Although Western Alliance is still selling at a discount to its historical valuation, I believe the majority of revaluation gains have already accrued. Going forward, Western Alliance may continue to grow its deposit base and I see potential earnings growth resulting from a decrease in short term borrowings, which soared during the first-quarter due to market circumstances. Western Alliance may have further upside related to its balance sheet restructuring (NIM improvement), but I see the regional banking market no longer as profoundly underrated and undervalued.

For further details see:

Western Alliance: Now Trading At Book Value (Downgrade)