WAL - Western Alliance Preferred Shares: High-Risk Bet Alongside Citadel Advisors

2023-03-17 06:39:01 ET

Summary

- Western Alliance Bancorporation is a regional bank based in Phoenix, Arizona.

- Given WAL's recent collapse in share price, we have seen Citadel Advisors swoon in and make a large common equity purchase.

- The situation is very much muddled at the moment, with the common equity having the ability to chop around significantly as more clarity is established with respect to the institution.

- The bank has $67 billion in assets, and as per its 8-K statement, 50% of its deposits are uninsured.

- We feel investing in WAL is highly speculative at the moment, but a retail investor willing to take that bet is better served by looking at the preferred shares which are trading distressed.

Thesis

Western Alliance Bancorporation ( WAL ) is a regional bank based in Phoenix, Arizona. The bank has around $67 billion in assets, and is fairly young, having been incorporated in 1994 in Las Vegas, Nevada. The institution has recently been caught up in the regional banks crisis, with its stock down -44% year to date.

In a capital structure, the common equity is the one that benefits the most from an increase in profitability and net income, but at the same time common shareholders are the ones that suffer most when a company is reeling. Given WAL's recent collapse in share price, we have seen Citadel Advisors swoon in and make a large common equity purchase , betting on a 'return to normal'.

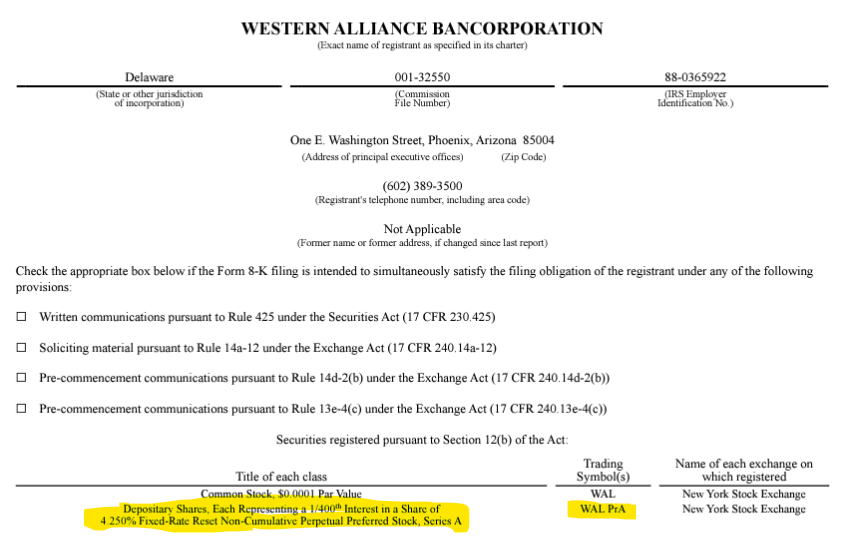

The situation is very much muddled at the moment, with the common equity having the ability to chop around significantly as more clarity is established in respect to the institution. A more conservative way to play the survival of Western Alliance alongside Citadel Advisors is via its preferred shares, namely the 4.250% Fixed-Rate Reset Non-Cumulative Perpetual Preferred Stock Series A ( WAL.PA ):

{kind=link}

Preferred shares offer less of an upside, but in our mind are a better risk-reward in this situation. Even if the bank survives, one is hard pressed to see where the common equity is going to end up in terms of pricing. Make no mistake - the trauma of this bank run will leave its marks, and Western Alliance will see much lower profitability going forward until the environment stabilizes. Why? Because it will have to pay more on its deposits to keep customers, and all the liquidity facilities that it might access will come at a cost.

There is a clear differentiation going on currently in the wider regional banks' preferred shares:

Preferred Shares Snapshot (Author)

On one hand you have institutions where the market is telling us there is stress but they are still viable, and on the other hand there are a couple of names where the outcome is binary based on survival. Western Alliance falls in the binary category. With its preferred shares trading at less than half of their liquidation preference, the market is telling us it is unsure if the bank will make it.

Current State of Preferred Securities Investments

Investing in preferred securities used to be a fixed income play driven by rates. They merely represented a take on interest rates, with minute default risk given the investment grade status of the bank and high Tier 1 capital ratios.

Today's bank runs have completely changed that landscape. In the case of a number of names from the table above it is more of a question of whether they will make it or not through the crisis. And their preferred shares embed that view, trading on price rather than yield now. We feel it is better to bet via the preferred shares on WAL's survivability simply because you can quantify the upside - i.e. the upside is the liquidation preference. For the common shares, even if the bank survives , the trepidations of the fall can severely impact the future profitability of the bank.

One thing should be crystal clear in an investor's mind - we are watching 'live' a bank run in progress, and while the regulators have backstopped depositors, they will not bail out any investors. If Western Alliance falls, expect complete wipe-out of the common shares and the preferred securities.

Balance Sheet Details

The bank is pulling all the necessary stops to ensure its survival :

Since the statement we released last week, Western Alliance has taken additional steps to strengthen its liquidity position to ensure that we are in a position to meet all of our client funding needs, including increasing our borrowing capacity. As of this morning, cash reserves exceed $25 billion and are growing, while deposit outflows have been moderate. Including accounts eligible for pass-through insurance, insured deposits exceed 50% of total deposits."

Mr. Vecchione added: "We also welcome the banking agencies' statement yesterday expressing their commitment to ensuring liquidity within the banking system, and their confidence in the strength of the banking industry. Although there have been no sales of securities to date, if adjusted to reflect unrealized losses in our held-to-maturity and available for sale investment book, our CET1 capital ratio as of 12/31/22 would be approximately 7.9%, which compares very favorably to peers and reflects the fundamental strength of our bank

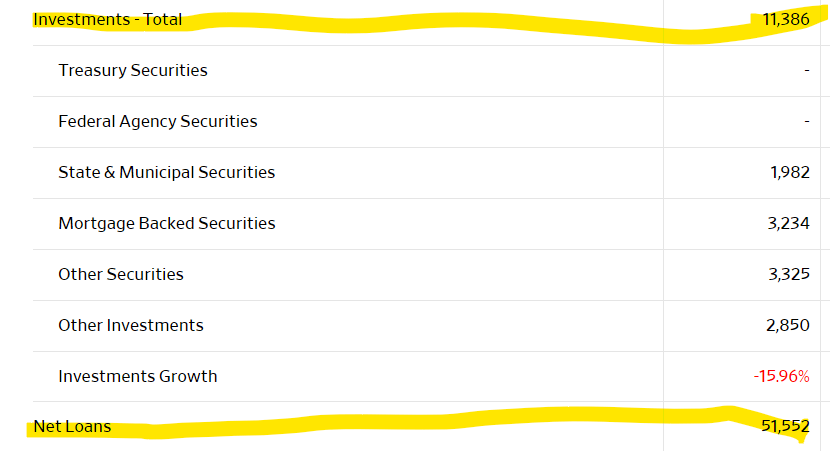

When looking at the bank's balance sheet we can see it is more focused on loans rather than investments, meaning it has less of an issue from AFS or HTM securities:

{kind=link}

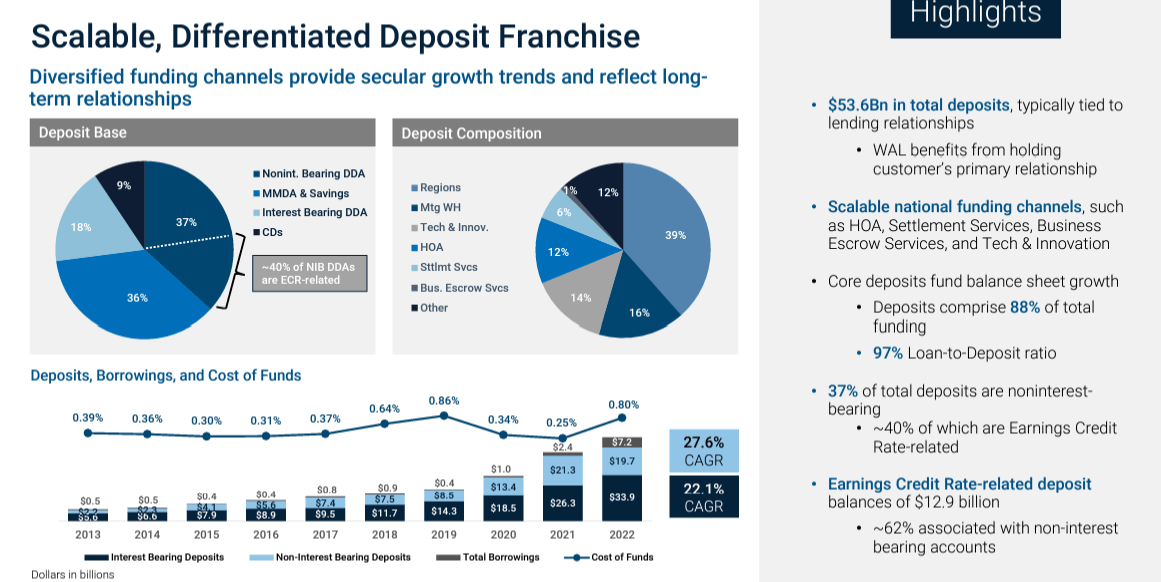

The bank provides a breakdown of its deposits, and as per its 8-K statement 50% of them are uninsured:

Deposits Details (Presentation)

{kind=link}

That seems to be the biggest issue right now. People fleeing, rather than banks being undercapitalized and having given poor loans. If a sizable portion of your depositor base leaves then as a bank you need to find the liquidity to pay them back. And that liquidity is not cheap and is hard to source.

Conclusion

Western Alliance is an Arizona based bank. The institution has an asset base of around $67 billion, with $53 billion in deposits. Around 50% of its deposits are uninsured, while the bank has an investment portfolio that is on the smaller side at $11 million. WAL has come under tremendous pressure this year, with its stock down more than -44%. Given WAL's recent collapse in share price, we have seen Citadel Advisors swoon in and make a large common equity purchase , betting on a 'return to normal'. We feel investing in WAL is highly speculative at the moment, but a retail investor willing to take that bet is better served by looking at the preferred shares. If the bank makes it through this tumultuous period, the upside is defined for the preferred securities (i.e. the $25 liquidation value), while the common equity will suffer P/E and EPS de-ratings as WAL suffers the costs of this trauma. To note that Western Alliance's Series A preferred shares are currently trading distressed at $11.5/share, embedding a binary outcome for the institution.

For further details see:

Western Alliance Preferred Shares: High-Risk Bet Alongside Citadel Advisors