WAL - Western Alliance Q3: High Earnings Yield Growing NIM Strong Deposit Growth

2023-10-25 04:39:46 ET

Summary

- Western Alliance reported strong Q3 earnings, but shares dropped 8% following the earnings report.

- The bank fully restored its deposit base, increasing deposits by $7.6B in Q3. The bank's net interest margin increased Q/Q.

- Western Alliance reduced its short-term borrowings by $820M Q/Q, creating a better balance sheet. The bank has further potential to move high-cost debt off its balance sheet.

- Shares trade at an unreasonably large 19% earnings yield.

This earnings season has so far not shaped up to be good for regional banks as deposit growth remained overall weak and higher interest rates weighed on results. Western Alliance Bancorporation ( WAL ) did much better than other banks, but the regional bank’s shares dropped more than 8% after it submitted earnings for the third-quarter: the bank beat top line estimates, fully restored its deposit base (two quarters after the financial crisis hit the regional banking market in Q1’23) and continued its balance sheet restructuring that resulted in sequential income growth. Given the much better trend in core fundamentals (deposits, NIM, earnings growth), I see the current drop as a new opportunity to engage!

Previous rating

I rated Western Alliance a hold previously for one specific reason: the bank's shares traded up to book value . While results from the banking sector were not great so far, Western Alliance's third-quarter earnings card showed that the bank made considerable progress in re-attracting commercial deposits and the bank’s balance sheet restructuring leaves room for considerable earnings growth. Western Alliance also saw an increase in its net interest margin.

Western Alliance's Q3 earnings, growing NII, balance sheet restructuring paying off

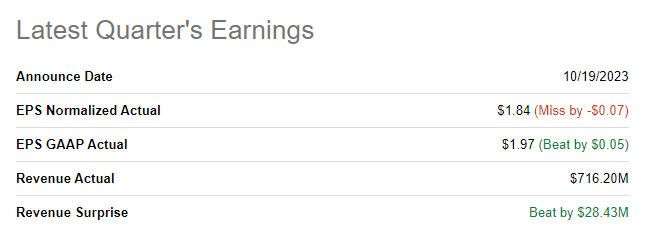

Regional bank Western Alliance reported better than expected earnings last week, yet shares dropped 8%. The regional lender saw a slight EPS miss of $0.07 per-share while it beat on revenues: the top line came in at $716.2M, beating the consensus estimate by $28M.

{kind=link}

Source: Seeking Alpha

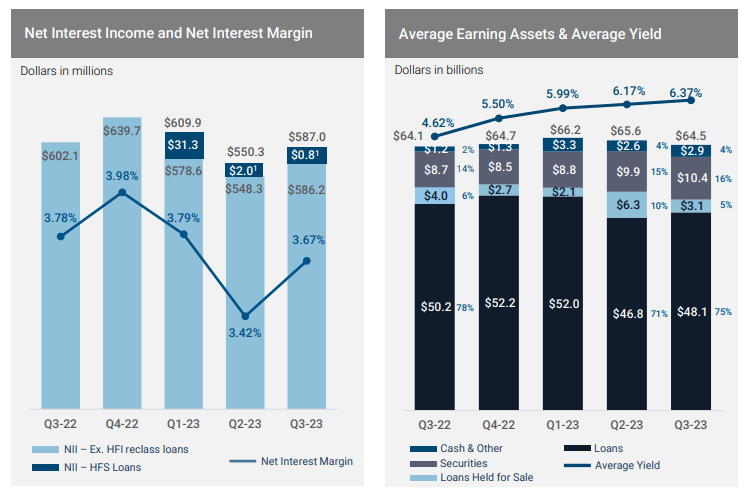

Western Alliance saw an increase in its net interest income in Q3'23 which soared 6.7% quarter over quarter to $587M and the increase was due both to higher interest income and lower interest expenses. The bank's net interest income increased $36.7M Q/Q because the bank lowered its expensive short term borrowings which is where I see more value going forward. The biggest surprise for me was the rather large increase in the net interest margin which grew from 3.42% in Q2'23 to 3.67% in Q3'23.

{kind=link}

Source: Western Alliance

Full deposit base restoration

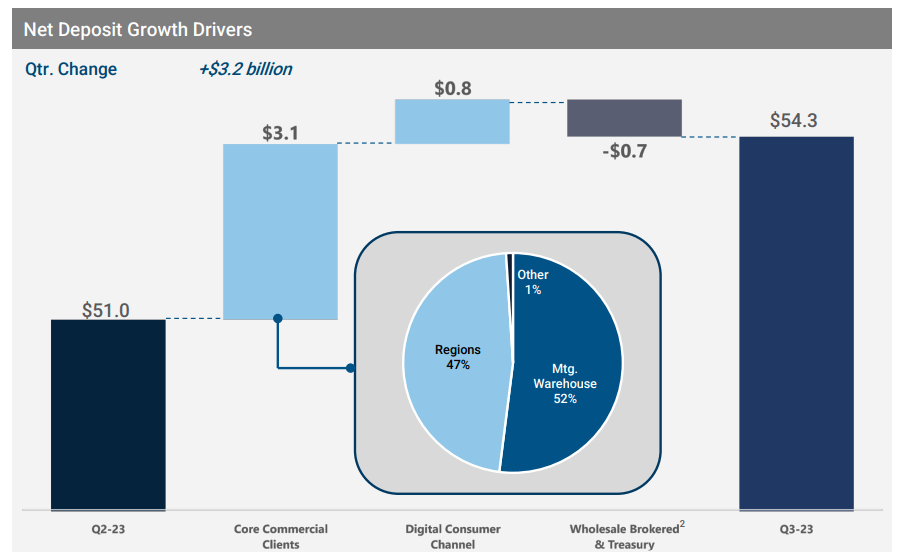

One key investment driver for Western Alliance has been that the regional bank had an opportunity to fully restore its deposit base after the first-quarter crash that occurred in the regional banking market. In the third-quarter, Western Alliance finally achieved this and the regional lender reported $54.3B in deposits at the end of September quarter.

During the first-quarter, the bank’s deposits dropped as low as $46.7B meaning deposits have since increased by a massive $7.6B. In Q4’22, Western Alliance had deposits of $53.6B meaning WAL has now a higher total deposit balance than before the Q1'23 financial crisis. Based off of the bank's outlook, Western Alliance is expecting up to $500M in deposit growth for the fourth-quarter.

{kind=link}

Source: Western Alliance

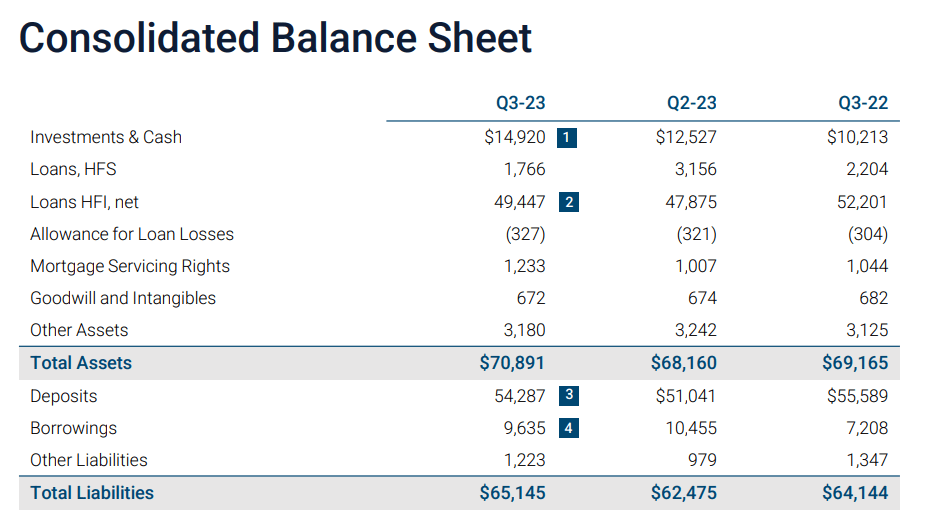

Western Alliance has an opportunity to grow earnings going forward by cutting down its short term borrowings that the bank pulled onto its balance sheet earlier this year. These borrowings are expensive and a repayment of those would likely have a positive earnings impact on Western Alliance in the near future. In the third-quarter, Western Alliance lowered its short term borrowings by $820M in Q3'23… which is the equivalent of an 8% reduction compared to the second-quarter. In Q2’23, Western Alliance repaid CLO and EBO repo facilities and borrowings from Federal Home Loan Banks. My estimate following Q3'23 earnings is that WAL could further reduce its borrowings by at least $1.5-2.0B which in turn would further take pressure off of its net interest income.

{kind=link}

Source: Western Alliance

Crucially, Q3’23 was the first quarter in a year in which Western Alliance’s total cost of funds decreased (which was driven by a decline in borrowings as discussed above). The decline in borrowing costs was marginal, 0.05 PP compared to Q2’23, but it nonetheless shows that the bank has an opportunity to grow its earnings going forward.

Source: Western Alliance

A medium-term second earnings catalyst

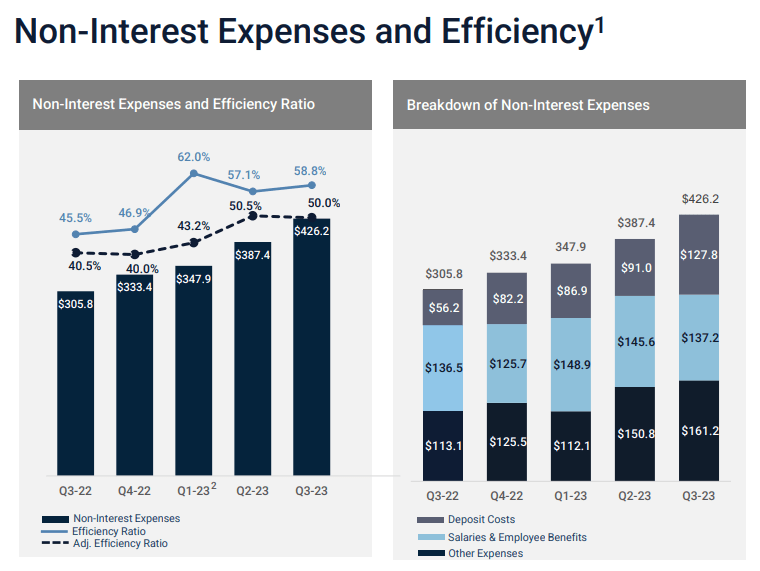

The bank's costs also increased in Q3'23 and there is an opportunity for Western Alliance to boost earnings growth going forward. The efficiency ratio, which measures a bank's control over its overhead expenses, increased 1.7% PP quarter over quarter to 58.8%. The biggest increase happened in the category of deposit costs... which I expect should decline as the Federal Reserve lowers rates. Deposit costs have risen with higher interest rates and inflated non-interest expenses. In Q3'23, Western Alliance non-interest expenses soared $38.3M to $426.2M Q/Q. In the longer term, I expect WAL's quarterly non-interest expenses to normalize around $300-320M.

{kind=link}

Source: Western Alliance

19% earnings yield plus upside

Western Alliance’s shares are again trading at an unreasonable low P/E ratio and an earnings yield converging upon 20%. Considering that Western Alliance submitted a much better earnings report than its rivals (many of whom saw a dip in BV and weaker deposit growth), I believe shares are in a new buy-the-drop situation. Shares of Western Alliance now trade at a massive 19% earnings yield, and are therefore much cheaper than other regional banks, despite presenting a much better Q3'23 earnings sheet.

With a P/E ratio of 5.2X, Western Alliance is widely undervalued. I estimate that Western Alliance could achieve $8.50 per-share in earnings next year (driven by a decline in deposit costs, lower short term borrowings and NIM growth) which implies an even lower P/E ratio of 4.9X.

Analysts expect $8.06 per-share in earnings, so I am more optimistic than the average analyst, large because Western Alliance's management out-performed during the first-quarter financial crisis and delivered better-than-guided for results. However, even based off of the consensus estimate, an earnings yield of 19% seems excessive. I also don't understand, frankly, the post-earnings drop as the bank, in my opinion, presented an overall much stronger earnings report than other regional banks.

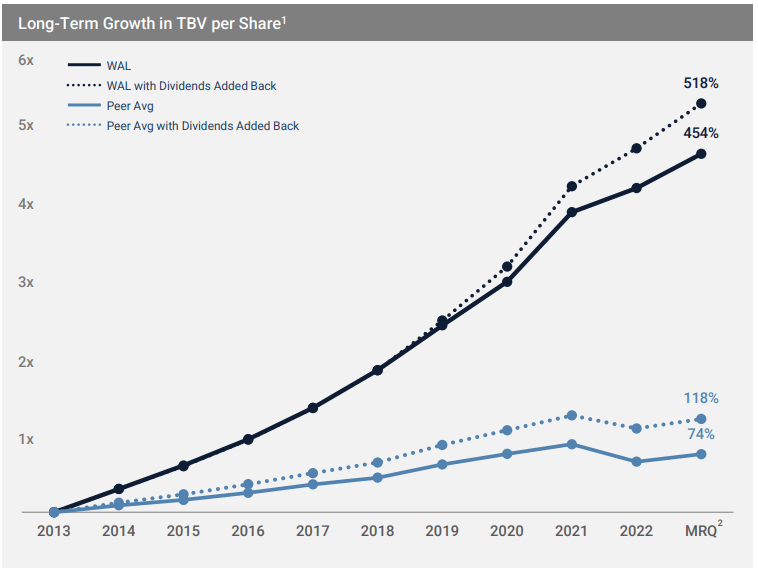

In the long run, Western Alliance’s (tangible) book value per share has consistently increased as well, showing that management's investment decisions have been prudent and risks have been controlled well. WAL outperformed other regional bank rivals in terms of TBV growth by a considerable margin in the last decade. This outperformance record is worthy of a premium valuation, in my opinion.

{kind=link}

Source: Western Alliance

Risks with Western Alliance

A contraction in the bank's net interest margin is likely the biggest risk for Western Alliance going forward. Another risk I see, generally speaking, is the risk of higher credit provisions in a recession scenario. There is also a limit to which Western Alliance can reduce its short term borrowings as a means to create an earnings catalyst going forward.

Final thoughts

I cannot see, nor do I understand, why shares of Western Alliance dropped after the bank submitted its third-quarter earnings sheet as the bank overall did a fine job, and a much better job than its rivals: deposits grew by more than 6% and the bank ended Q3’23 with higher deposits than Q4’22 (the fiscal quarter just before the crisis in the regional banking market), it successfully reduced its high-cost short term borrowings. Since Western Alliance’s key metrics are all trending in the right direction (even its NIM increased in Q3'23) and shares trade at an unreasonably large 19% earnings yield, I believe investors have a unique opportunity to take advantage of this silly sell-off and add Western Alliance as a rebound play!

For further details see:

Western Alliance Q3: High Earnings Yield, Growing NIM, Strong Deposit Growth