WAL - Western Alliance Q3: The Business Is Clearly Recovering From The Banking Crisis

2023-10-24 11:23:14 ET

Summary

- Western Alliance Bancorporation has weathered the crisis and is on the mend, with its latest results beating expectations.

- The bank has recovered its Q1 deposit loss and its deposits are down only 2.5% from last year, performing better than the industry average.

- WAL's funding mix has shifted to a more normal footing, and its loan book is benefiting from rising yields and increased lending.

Earlier this year, Western Alliance Bancorporation ( WAL ) came under significant pressure. Following the failure of Silicon Valley Bank and First Republic, markets were searching out what other banks could be vulnerable to same deposit flight. With its Western focus and noninterest bearing deposits, WAL was seen as particularly vulnerable, sending shares cratering. While they have recovered, they are still down meaningfully this year. However, its latest results show the bank has weathered the crisis and is on the mend.

{kind=link}

Seeking Alpha

In the comp any’s third quarter reported on October 19th, it earned $2.30 in adjusted EPS, handily beating consensus of $1.91. This was down from $2.42 a year ago as the bank experienced net interest pressure. The bank’s net interest margin ((NIM)) did rise 25bp sequentially to 3.67%, but that is down from 3.78% last year. Still, just 11bp of NIM compression after what WAL went through earlier this year is impressive in my view. And its quarterly NIM rebound is also consistent with a normalization in its funding sources.

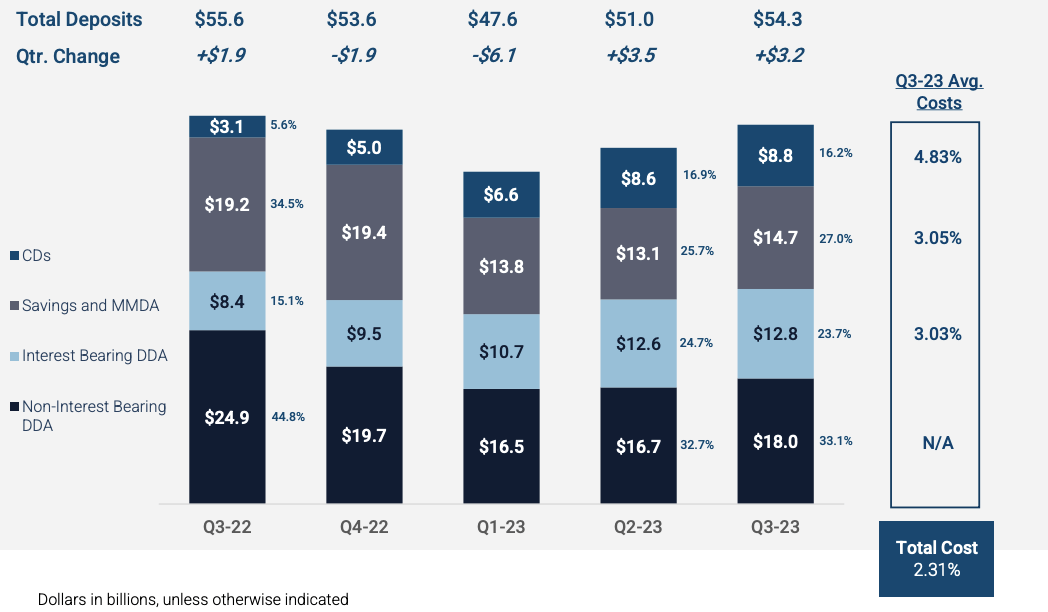

As you can see below, the bank added $3.2 billion in deposits during Q2. Over the past two quarters, it has fully recovered its Q1 deposit loss, and deposits are down $1.3 billion, or about 2.5% from last year. Industrywide, commercial bank deposits are down 2.4% from last year. Given the particular pressure WAL came under, to be an industry-average deposit performer is a fairly good outcome. I would also note that 82% of its deposits are now insured, which provides a stable base from which WAL can operate its business.

{kind=link}

Western Alliance

Now, WAL has seen a notable shift in deposits. While deposits are down just $1.3 billion over the past year, its non-interest bearing ((NIB)) deposits are down $6.9 billion, forcing it to sell more CDs to offset this. This shift has increased its overall funding cost. It has been encouraging to see NIB deposits recover though over the past two quarters whereas many other banks are still registering declines.

In a 5% world, deposits where you pay nothing are increasingly valuable. Most NIB accounts are transactional accounts (i.e. those a company uses to make payroll every two weeks), and because certain balances are needed to make those transactions, there is a theoretical floor to how low they can go. As rates were rising, customers had an incentive to bring those balances closer to the floor to shift funds into interest-bearing accounts. This process appears to be largely complete for WAL. It also may be winning back some customers who fled in Q1 during the panic, helping balances to recover.

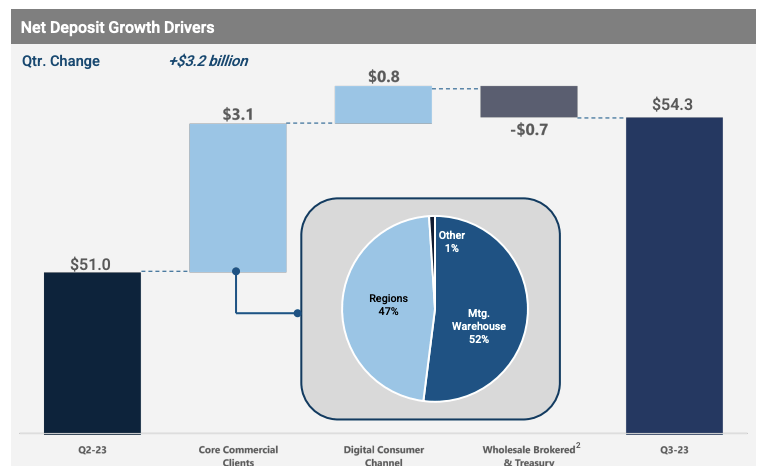

Additionally, given the rise in interest rates, WAL is paying more for its interest-bearing deposits. Deposit yields rose 41bp to 3.49% during the quarter, but total funding costs fell from 2.85% to 2.8%. This contributed to the recovery in NIM. When deposits plunged earlier this year, WAL had to rely on more wholesale funding, which costs about 6%. This quarter, as NIBs recovered, it paid down 6% wholesale funding. Its funding mix shift is now on a more normal footing, and it should not return to previous lows in NIM, barring another deposit shock (which given its increased insured funding mix appears unlikely). Indeed as you can see below, it was able to pay down about $700 million in wholesale funding as its core deposits rose by just over $3 billion in the quarter.

{kind=link}

Western Alliance

At the same time, WAL’s loan book continues to benefit from rising yields as most of these loans are floating rate. Loan yields rose 25bp to 6.73%, due to the July Fed rate hike. Additionally, loan growth has resumed. In Q1 as deposits fell, straining its balance sheet, WAL had to pull back on lending. With deposits recovering, lending has returned to a more normal footing. Loans rose 3% to $49.4 billion, primarily via increased business lending. Still, they are down over 10% from last year, far outpacing the decline in deposits. I would expect loans to continue to grow, and increased lending in this rate regime should be accretive to net interest income ((NII)) . Due to a wider NIM and more interest-earning assets, net interest income rose from $550 million to $587 million, still below the $602 million of last year due to the 11bp decline in NIM and smaller loan book. NII has likely troughed, putting WAL ahead of most banks this cycle as others like Regions ( RF ) and Citi zens Financial ( CFG ) are guiding to a further decline in Q4. WAL experienced a much worse February-April than most banks, but that harsher fall seems to mean it has pushed through the declines more quickly than peers.

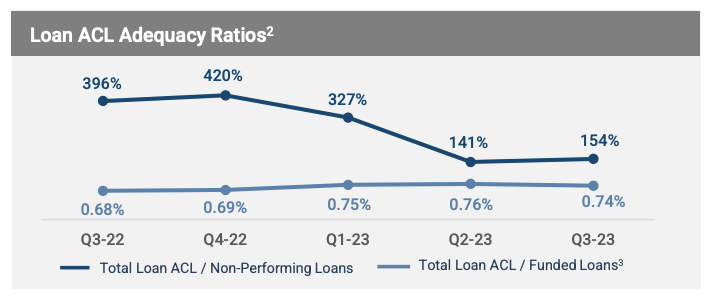

WAL’s credit quality remains strong with charge-offs just 0.07%. The bank took $12.1 million in provisions, against $8 million in charge-offs for a $4 million build in reserves. Western Alliance has reserves of $376 million, which covers about 0.74% of total loans. As you can see below, it has coverage for 154% of non-performing loans. Last year, the bank was reserved very conservatively in anticipation of a deteriorating macroeconomic environment, and so coverage of NPLs has declined as they’ve risen as expected

{kind=link}

Western Alliance

154% coverage is a bit lower than I like to see, though this is complicated by the fact about 22% of WAL’s loans are insured or have government guarantees, mitigating the potential losses it can see from its loan book. As such, it tends to see higher recoveries on defaults than many banks, which is why charge-offs are so low at just 0.07%. That said, this coverage is a bit low in my view, and I do see a risk that WAL will need to build reserves more. To get to 200% coverage, which I would view as a safer level, WAL would need to add about $25 million to reserves each quarter through 2025. That would be about a $0.19 headwind to EPS, which is quite manageable.

WAL is also strongly capitalized, and it has a common equity tier 1 ratio (CET1) of 10.6%, up from 10.1% last quarter, as it has not been buying back stock. WAL wants to get CET1 past 11% because it is gradually approaching $100 billion in assets. At that point, it will need to gradually phase in the unrealized losses on its securities portfolio. Today, that sits in accumulated other comprehensive income and is about $733 million, which would make its CET1 ratio below 9%. Now as these bonds mature, its AOCI loss will decline. This in combination with retained earnings leave WAL well positioned to hit 11% CET1 and over 9% including unrealized losses next year even as it grows its loan book. I would expect repurchases to begin again in 2025, though they could start slowly late in 2024.

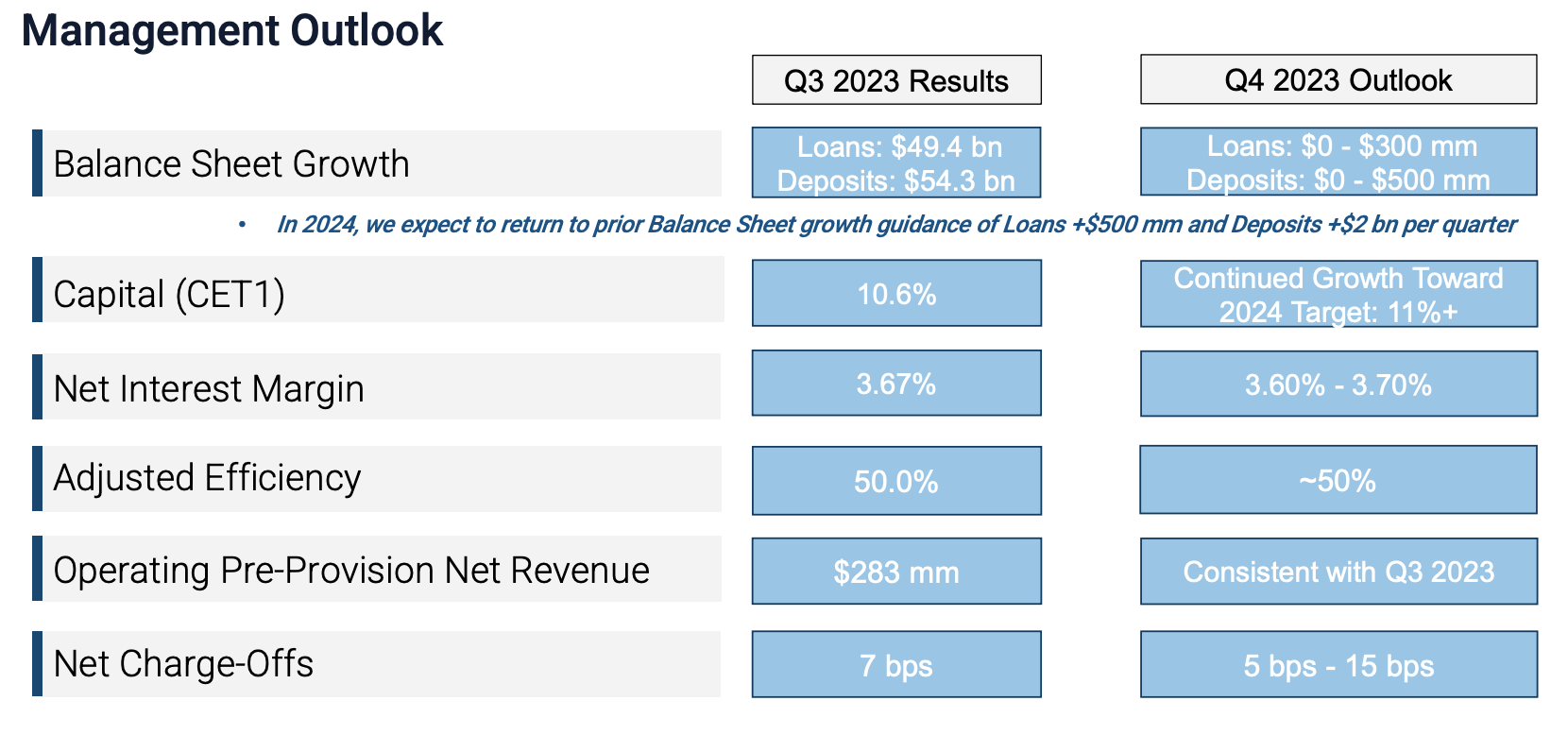

As you can see below, management expects deposit and loan growth to continue next quarter and accelerate in 2024 with its business back onto a normal footing while NIM should be broadly flat to Q3 results. That should lead to a modest increase in NII given a growing asset base, which can help to offset to some higher credit loss provisions, should they prove necessary.

{kind=link}

Western Alliance

WAL has a $43.66 tangible book value, which includes its AOCI mark to market loss. Otherwise, book value would be about $50/share. With NIM stabilizing and even assuming my $25 million/quarter of provisions, WAL has about $8.20-$8.60 in earnings power over the next year, depending on how much asset growth accelerates. Shares have just a 5x multiple and are trading around tangible book value. This discounted valuation, even to other regional bank peers, speaks to some lingering emotional scarring from investors over its Q1 challenges.

I view the situation differently. Western Alliance and its management are battled-tested, and they proved the resilience of the business during a challenging period. Moreover, whereas many other banks are still registering sequential declines, WAL is now securely on the road to recovery—there is an element of “first in, first out” to the funding crisis. I believe book value ex AOCI or ~$50 is likely to be a difficult ceiling to break though, but I expect shares to at least trade there as investors grow comfortable with the stability of its business. Combined with its dividend, that provides nearly 20% upside, making shares a buy here.

For further details see:

Western Alliance Q3: The Business Is Clearly Recovering From The Banking Crisis