UP - Wheels Up Stock: Still Highly Speculative

2024-01-09 14:45:33 ET

Summary

- Wheels Up stock has more than doubled since my last article, but is still down 96% in the last 3 years.

- Recent developments include new capital injection and positive forward guidance, but actual results show a decline in flight revenues and memberships.

- The company's cash flows continue to look bad, and profitability remains uncertain. UP stock is considered risky and speculative.

Wheels Up Experience Overview

The last time I wrote about Wheels Up Experience ( UP ) titled Wheels Up: Time Might Be Running Up For This Company I rated the company a "Sell" and interestingly enough the stock more than doubled since then. It looks like I made a terrible call even though none of the facts I stated in the article changed in a significant way.

Stock Performance Since Last Rating (Seeking Alpha)

Meanwhile the stock is still down 96% in the last 3 years and close to 70% in the last year so it is possible that some of the bounce we saw in recent months might be more technical in nature than fundamental. When a stock reaches oversold territory a large number of traders buy it up in hopes of taking advantage of a bump and if you did that in the last few months, you probably benefited greatly from it, but the company's long-term investors are most likely still deeply in red if they bought almost any time in the last 3 years.

Before I get to more fundamentals, let me explain why I rated this stock a "Sell" last time. It was because I felt that the stock is too risky and its risk-reward structure didn't look very attractive. It's not that I thought the company would go bankrupt for sure in the next few months but that this stock is so speculative that investors should probably invest in more conservative stocks unless they really love risk taking. I didn't recommend shorting the stock since any stock has the potential to double or triple on very little to no news when sentiment supports it but I also didn't recommend buying it either.

Recent Developments

So what happened in the last few months? Actually there were a couple developments in recent months regarding the company since my last article. One of these developments was an announcement of new capital injection into the company. In my last article I mentioned that the biggest risk for this company was running out of cash before it can post sufficient growth to post profitability and it received some much needed capital from its partners and investors. Investors or traders really liked this development for two reasons. First, it gave the company a new lifeline so that it can keep its lights on and operations going for at least another year. Two and more importantly, it showed that Delta ( DAL ) and institutional investors still have faith in the company. If they didn't they wouldn't inject additional capital into the company. As a matter of fact, Delta and their investor partners now own 95% of the company due to their equity linked liquidity injections. Many investors saw this and thought that Delta and others wouldn't invest this heavily into a company that's about to go out of business. This could be seen partly as a bailout of the company and partly as a vote of confidence.

{kind=link}

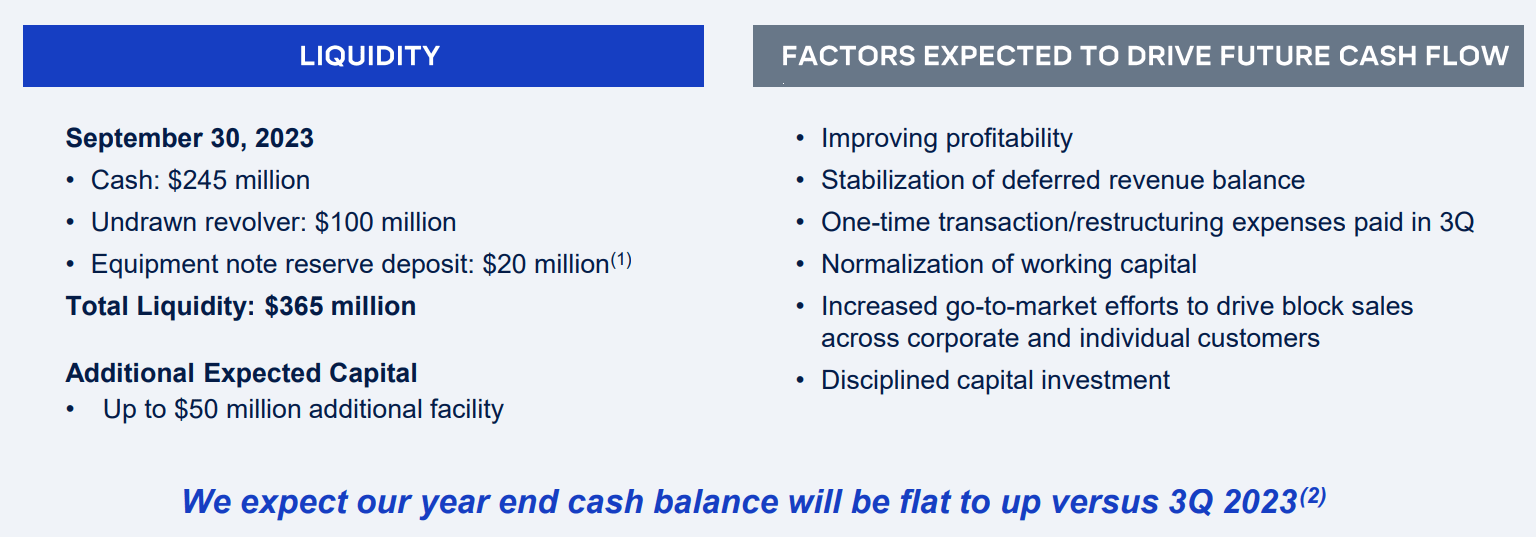

The second development that occurred for the company which helped boost its stock price is its forward guidance. There were 3 things investors seemed to like in the company's guidance. First, it guided that there would be several improvements in company's cash flow position including improving margins. Second, it guided that its cash balance would be flat or up in Q4 of 2023. This is huge considering how the company has been bleeding cash for several quarters in a row now and investors liked the idea that the company's bleeding would finally stop.

{kind=link}

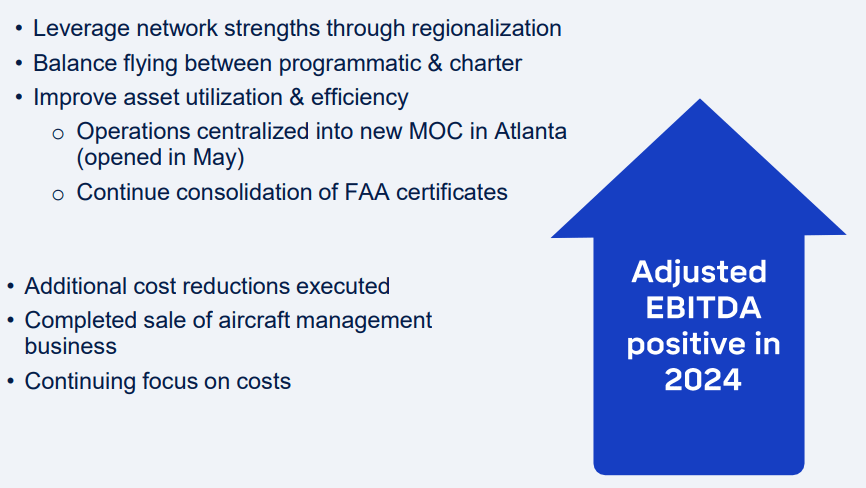

Third and most importantly, the company guided for a positive adjusted EBITDA in 2024. Adjusted EBITDA still comes with a lot of caveats and not necessarily mean that the company will be profitable. As it is EBITDA already excludes a bunch of items like taxes, interest payments, depreciation and amortization and when you add "adjusted" to this metric, you are adding even more items to exclude so that the company looks a lot more profitable than it arguably is.

{kind=link}

Reality Checks

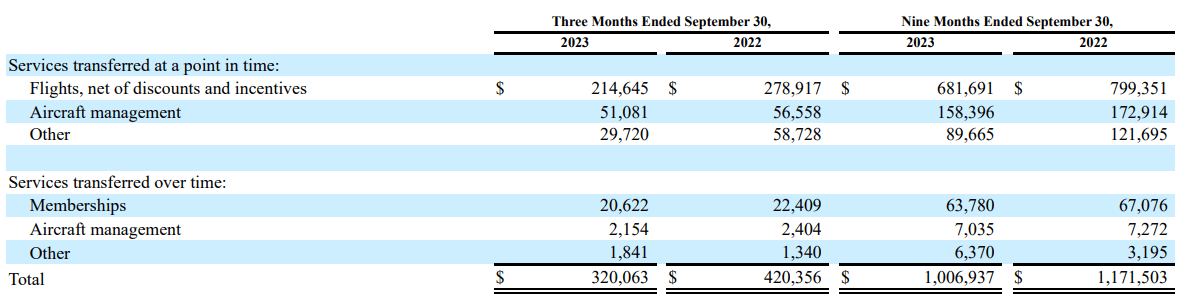

Now it's time for some reality checks. When the company announced its actual results in November for the third quarter, the results didn't look all that impressive especially for a "growth" company. It posted a significant drop in flight revenues (down from $279 million to $214 million representing a drop of 24%) and it posted an almost 10% drop in its memberships. The company's total revenues actually dropped significantly from $420 million to $320 million from last year.

{kind=link}

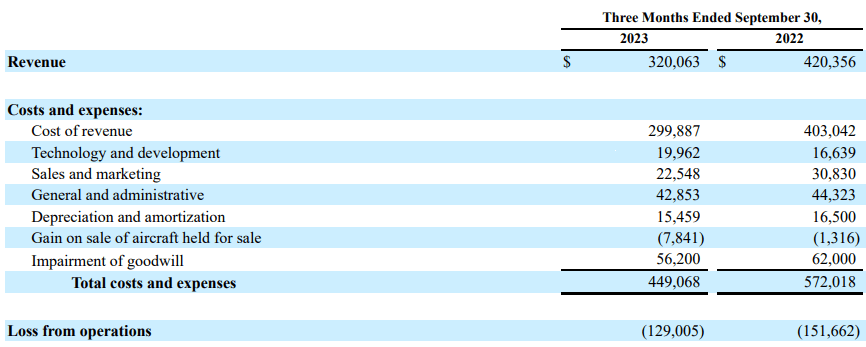

The company posted a smaller operating loss than the year before ($129 million vs $151 million) but this was "achieved" by having fewer flights due to less demand. Its gross margin came barely at 6.4% which indicates that it was selling tickets almost at cost with very little hope of making a profit and even this couldn't increase the demand for its flights. The number of flights were actually down -21% and revenue per flight was down another -2%.

{kind=link}

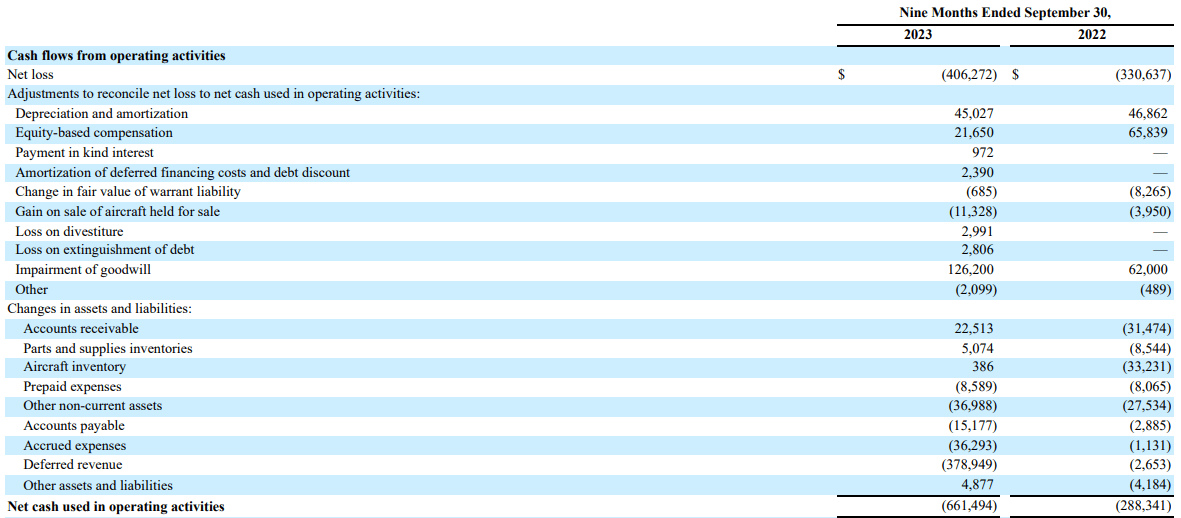

The company's cash flows continue to look bad. In the first 9 months of 2023, it posted an operating cash flow of negative $661 million. Considering that the company was given a lifeline of $500 million by Delta and its investor partners, this money will only last them about 7 months at the current rate of burning cash. The biggest item in the company's operating cash flow was deferred revenues at $378 million but even if we exclude this item, the company was still bleeding close to $400 million at an annual rate and this is not sustainable.

{kind=link}

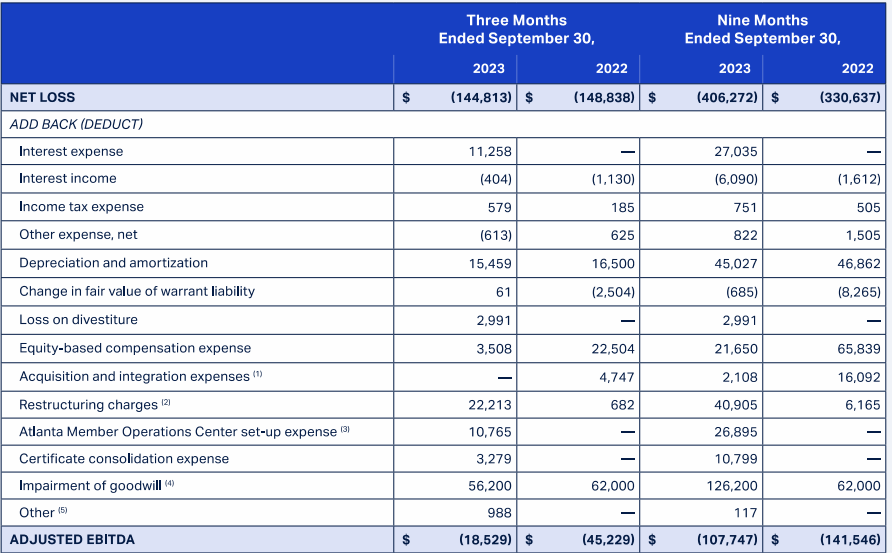

The company says it will reach flat cash flows and "adjusted EBITDA" profitability in 2024 so we will have to see how they will achieve this. In the last quarter's report, the company's adjusted EBITDA calculation included exclusion of 14 line items including equity based compensation, restructuring charges, Atlanta Member Operations Center expenses, impairment of goodwill and other things. These adjustments moved the company from a loss of $144 million to a loss of $18 million.

{kind=link}

Is UP Stock A Buy Now?

Moving forward the company will have to do something significantly different because you can't have cash injections forever. Many times investors don't mind if a company is not particularly profitable at its growth stage because it's investing its time and resources into scaling up to be profitable in the future. Yet, this company didn't post any growth in 2023. It posted a decline in number of flights, revenue per flight and number of active memberships. Then we can't call this a growth company when it posted drops in 3 most important growth metrics.

Then where will profitability come from? The company is already selling tickets almost at cost and if it raises prices it could lose even more demand in my view. It could try to cut costs aggressively but there is only so much you can cut without affecting your operations especially in the airline industry. Delta and its partners can't possibly buy more equity either in my opinion because they already effectively own 95% of the company. It is possible that Delta could just buy the whole company and take it private before it runs out of cash which could give the stock some more boosting.

I still see this stock as too risky, or speculative at best. Having said that, it is dangerous to short stocks like this because they can easily double or triple in a short term. The stock already jumped a lot in recent months and it can jump again in the future especially considering that it's down 95% in the last 3 years and some people think there is a floor under it with Delta supporting the company. Still, this is probably not a good investment for most investors in its current shape and form.

If the company were to show signs of growth and its cash burn were to slow down significantly, I would change my thesis accordingly but it may take a while before this happens.

For further details see:

Wheels Up Stock: Still Highly Speculative