BIG - Why Did Big Lots Stock Recently Drop To All-Time Lows And What Is The Outlook?

2023-06-06 09:30:00 ET

Summary

- Big Lots is currently trading at multi-decade lows following poor results that included a suspension in their quarterly dividend.

- While results were disappointing, the factors driving the weakness weren't all unique to BIG. I, therefore, view the significant pullback as overdone.

- Recently announced initiatives, such as the closure of their forward distribution centers, could trickle into margins later in the year.

- Combined with an expected moderation in markdowns and further tailwinds in the freight environment, the bar for a surprise rebound appears low.

- Shares are viewed as a "buy" for more risk-tolerant investors, given current trading levels.

On the day of their earnings release , Big Lots ( BIG ) dropped to a 30-year low following poor results and the announcement of a suspension in their quarterly dividend.

As a heavily shorted stock, the declines on the day of earnings were even more pronounced. Over the past year, shares in the stock have now lost three quarters of their value.

{kind=link}

Seeking Alpha - 1-YR Returns Of BIG

Whether the company faces an existential threat is up for debate. The company is one of the largest and most nationally recognized discount retailers. To see the stock fail to recover some, or perhaps even all, of their lost value, then, appears unlikely.

One can point to failed retailers such as Bed Bath & Beyond ( OTCPK:BBBYQ ) as one case of why nothing is out of the realm of possibility. While true, I view BIG as better positioned to overcome their current challenges.

For one, a major hurdle in the current quarter was simply weather conditions. The unfavorable conditions forced a late start to the spring selling season, which in turn forced aggressive markdowns to clear the seasonal inventory. The abrupt closure of their largest vendor last year also negatively affected product availability, resulting in poor product mix. The demand equation from the consumer angle is trickier but this isn’t unique to BIG. Looking ahead, I can see shares rebounding later in the year as their current initiatives trickle through earnings. With much of the fear already priced in, I view shares as an attractive “buy” for more risk-tolerant investors.

BIG Stock Key Metrics

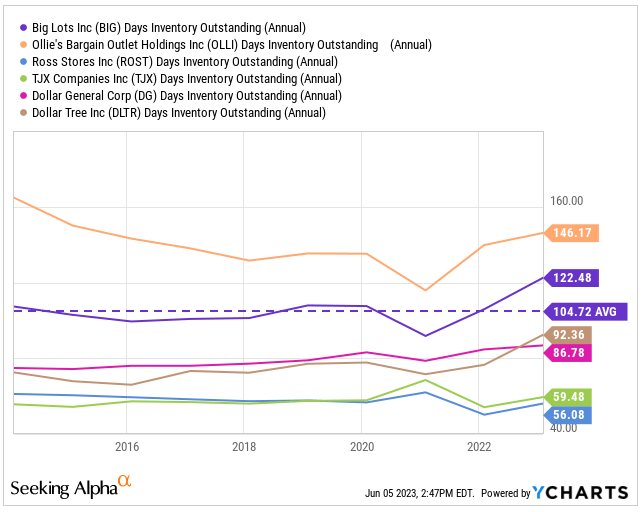

The turnover of inventory is viewed as a key performance metric for BIG. At the end of the first fiscal quarter of 2023, BIG held +$1.1B of inventory. Though the balance was down 18.8% from the same period last year, days outstanding was still elevated from historical averages.

Currently, inventory is turning every 120 days. Looking ahead, a return to the 100-day range is most desirable. One peer, Ollie’s ( OLLI ), turns even more slowly at just under 150 days. But the rate of their slowdown is less pronounced than that reported by BIG.

{kind=link}

YCharts - Days Inventory Outstanding Of BIG Compared To Peer Set

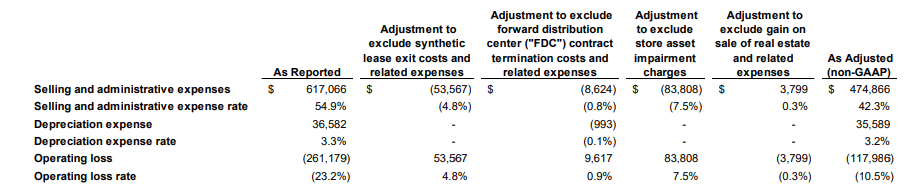

Another relevant metric is their margins. In Q1, BIG reported an unadjusted operating margin of negative 23.2%. And even when considering adjustments relating to lease exist costs and asset impairment charges, adjusted margins still came in at a negative 10.5%.

Driving the decline here was increased markdown and promotional activity, which dragged gross margins down 180 basis points (“bps”) to 34.9%. Though these initiatives contributed to an inventory decline in-line with the decline in sales, it clearly came at a cost to the bottom line.

{kind=link}

Q1FY23 Earnings Release - Summary Of Quarterly Operating Margin

The overall cash and debt position of the company is also of heightened importance. In Q1, for example, the dividend was suspended in an effort to shore up liquidity. Their current capital allocation plan also sees +$80M in capital expenditures (“CAPEX”) for 2023. This is down from previous guidance of over +$100M.

In addition, the company announced the closure of all four of their forward distribution centers. Altogether, they expect to raise more than +$340M via asset monetization efforts, which includes the sale/leaseback of their corporate headquarters.

On a net basis, this is expected to haul in +$240M. These proceeds are then expected to be used to pay down their outstanding debt on their asset-based lending (“ABL”) facility, which has a total capacity of +$900M, but is currently +$500M drawn.

Why Did BIG Stock Drop Following Their Earnings Release?

BIG reported dismal quarterly results, which included a worse than expected drop in quarterly revenues of 18%. In addition to the poor topline figures, management announced the suspension of their quarterly dividend and held off on providing a complete full-year outlook. This was enough to drive shares down to multi-decade lows immediately following the release.

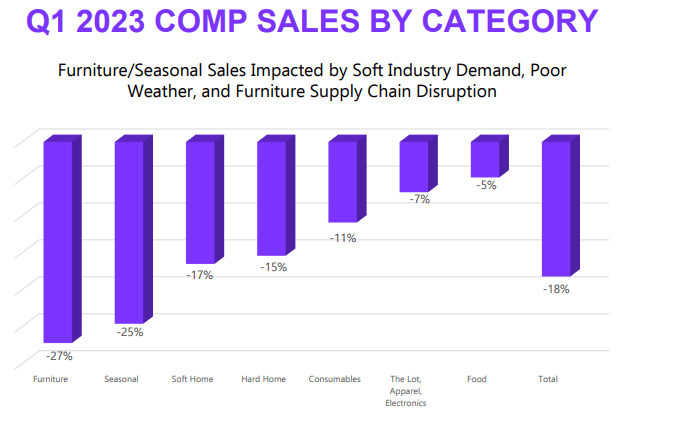

BIG was stung particularly hard by the pullback in big-ticket purchases, such as in furniture and patio sets. These were categories that the company previously excelled at, especially during the height of the COVID pandemic.

{kind=link}

Q1FY23 Earnings Presentation - Summary Of Comparable Sales By Category

Poor weather was one primary culprit for the decline. Seasonal items, such as their lawn and garden offerings, for example, accounted for about a quarter of their comparable sales decline during the period.

The declines in these items then resulted in a greater number of promotions, which is notable since the seasonal offerings are one of their highest margin categories. The unfavorable product mix paired with the increased promotional activity ultimately resulted in weaker gross margins in the low 30% range.

Compounding the negative effects from the weather was a general malaise in consumer spending. This headwind was amplified further by lower tax refunds, which customarily are a significant driver of first quarter sales.

Aside from the weather and the state of the consumer, headwinds from the closure of their largest vendor, United Furniture Industries, in November of last year topped off their trifecta of issues during the quarter. The abrupt closure resulted in product shortages in key furniture lines. The negative effects here knocked back comparable sales significantly and also created indirect headwinds in other areas, such as home textiles and houseware assortments.

On the release, management announced several cost cutting initiatives and provided a general sense of the outlook moving forward, which appears more positive than what they incurred in Q1. But it clearly was not enough to shake off investor doubt in the stock.

What Is The 2023 Outlook?

The outlook for the remainder of the year incorporates a significantly more challenging macroeconomic operating environment, one where consumers are increasingly hesitant to make higher ticket purchases. The more challenging landscape is even more relevant since the company’s target customer base is primarily on the lower end of the income spectrum.

A more promotional selling environment, therefore, is expected. But this is expected to normalize as the year moves on, particularly in the later months of the fiscal year. Comparative sales are also seen improving in the back half of the year following their merchandising and marketing actions.

The lower level of markdown activity later in the year in combination with significantly lower freight costs are expected to drive gross margins higher. Though a return into the upper 30% range is unlikely in the nearest term in Q2, management is confident of a potential return in the Q4 reporting period.

In addition to the improvement to their liquidity position, the closure of their forward distribution centers is expected to contribute meaningfully to the +$100M of identified savings in selling, general, and administrative (“SG&A”) costs. Combined with other initiatives, management has identified a path of over +$200M of opportunities across both gross margin and SG&A.

Is BIG Stock A Buy, Sell, Or Hold?

There’s no denying that BIG’s results were disappointing. Announcements relating to their dividend and other efforts to shore up liquidity could also be viewed as a concern. The lack of complete full-year guidance further added to negative sentiment. The drop, then, to multi-decade lows no doubt appeased those short on the stock.

With shares where they are, I view the fears as overly priced in. Aside from the suspension in the dividend, the company has scaled back their CAPEX plans, refrained from share repurchases, and has lined up several sale/leaseback transactions for existing properties. All considered, this is expected to raise their available liquidity into the +$500M range, which is consistent with their historical targets.

Their capital initiatives are also expected to contribute significantly to lower SG&A costs in future periods. Later in the year, the company is also expecting less markdowns and is also expecting even greater tailwinds in the freight environment. Together, this is projected to improve margins back to targeted levels.

The turnover of inventory is one metric that needs realignment. And I do expect this metric to improve in the back half of the year through the normalization of their on-hand stock from their current promotional activities.

The capture of dislocated customers from Bed Bath following their ultimate closure could also improve traffic levels at their store. Recently, the company ran a campaign to honor their 20% coupons, and upon doing so, they generated 90M television and radio impressions. At the very least, this enabled BIG to sign up more loyalty customers.

Though many would still hesitate to initiate on the stock, the bar for a rebound higher is low. Any rebound could also be amplified due to the level of short interest in the stock. At present, the stock is trading at just 0.039x forward sales. For perspective, their five-year average is about 0.23x. Even at a 0.10x multiple, shares would be valued at about $15.50/share. That’s materially above where shares are currently trading at. For investors with a higher degree of risk tolerance, a dive into BIG may prove worth it over the long haul.

For further details see:

Why Did Big Lots Stock Recently Drop To All-Time Lows And What Is The Outlook?