CA - Why I'm Still Bullish On The Westaim Corporation Stock

2024-01-05 01:19:50 ET

Summary

- Westaim is a Canadian small-cap investment holding company that provides long-term capital to businesses in the global financial services sector.

- The company's recent financials show robust performance in its operating segments.

- Westaim's valuation appears to be cheap, with an implied P/E ratio of 2.2x for FY2023 well below the sector median.

- Uncertainty always rewards companies with a valuation discount. However, I think investors will have more and more information available as the company reports through 2024 and will move the stock in the direction that this information tells them to.

- Based on the company's fundamental profile, I expect the upward trend to continue. So I remain bullish.

Introduction

At the end of October 2023 , I published an article on The Westaim Corporation ( WED:CA ) ( WEDXF ) stock, in which I described it as a hidden small-cap gem that was attractively priced at the time. Since then, the stock has been on an uptrend, but has lagged the broader market growth.

Seeking Alpha

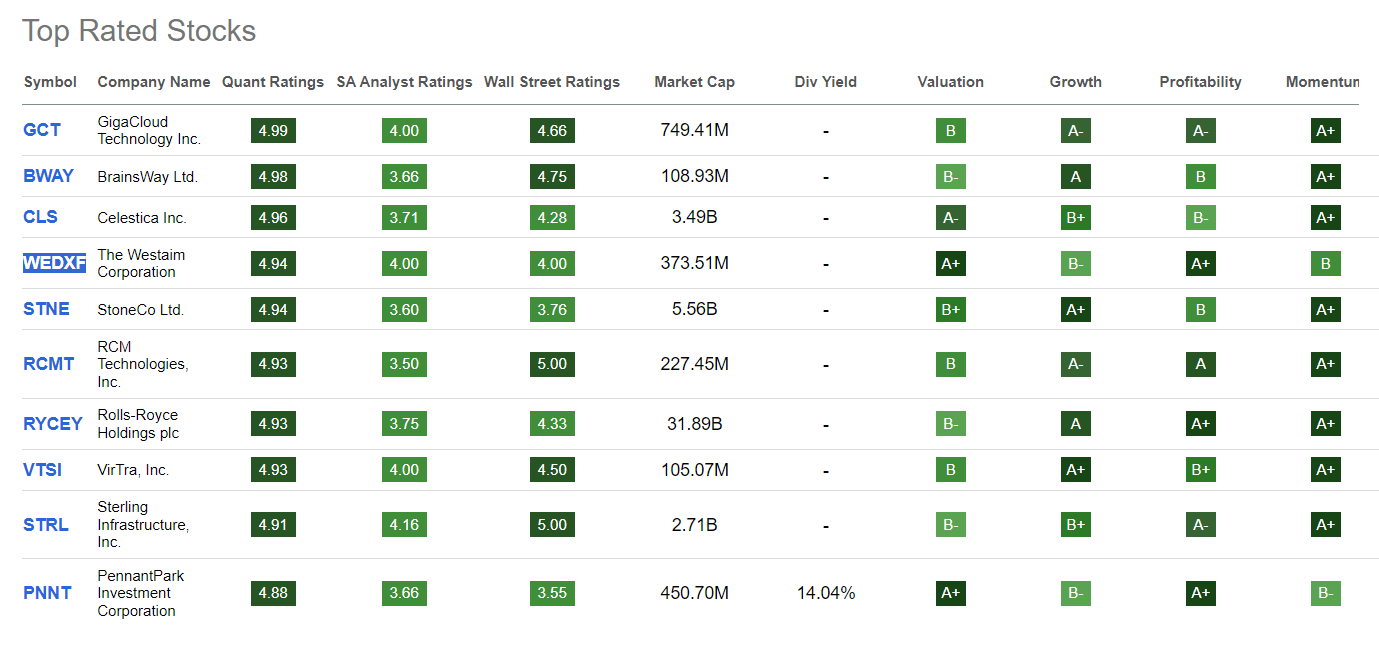

Despite underperforming the S&P 500 Index ( SPX ) ( SP500 ), Westaim Corp. maintains its status as a top stock based on Seeking Alpha's Quant System:

{kind=link}

In today's article, I want to reassess whether such a high rating among the thousands of other public companies out there is deserved. Is Westaim still attractive for a medium-term investment horizon?

Westaim's Recent Financials

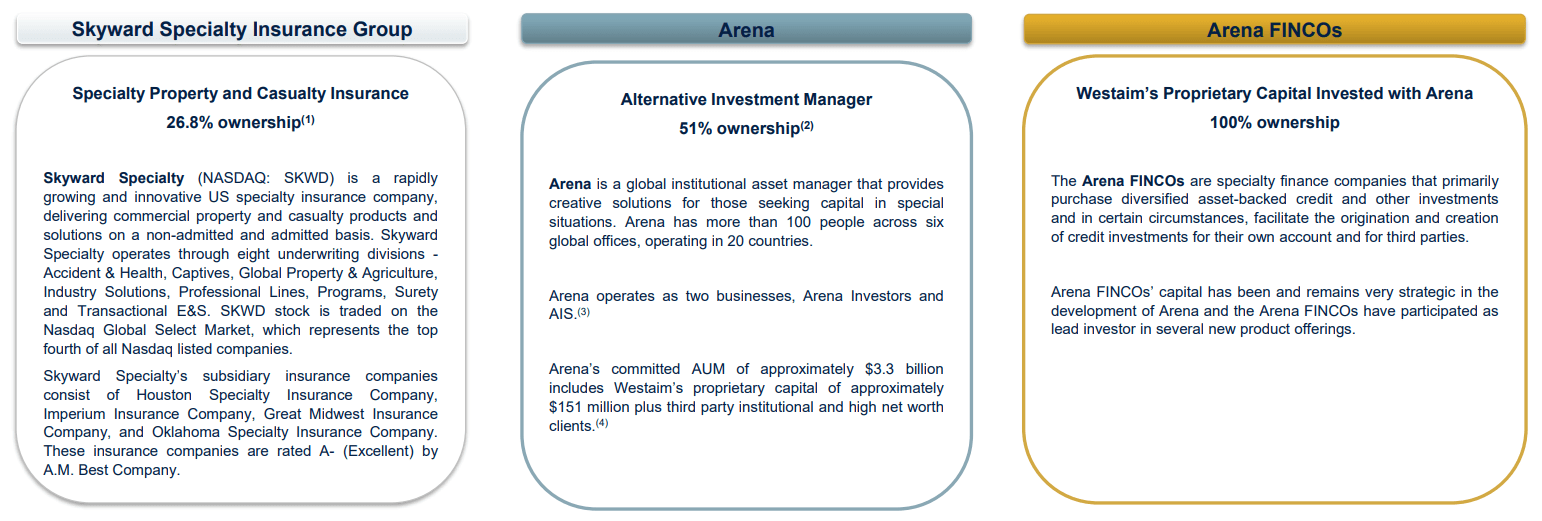

To understand Westaim's financial, one needs to understand what this company is. Westaim is a Canadian investment holding company that provides long-term capital to businesses in the global financial services sector. They seek high-quality investment opportunities, aiming to partner with businesses and management teams for long-term wealth growth and above-average returns for shareholders. As of the latest reporting date [November 2023], the company's principal investments consist of Skyward Specialty, Arena FINCOs, and Arena Investors:

{kind=link}

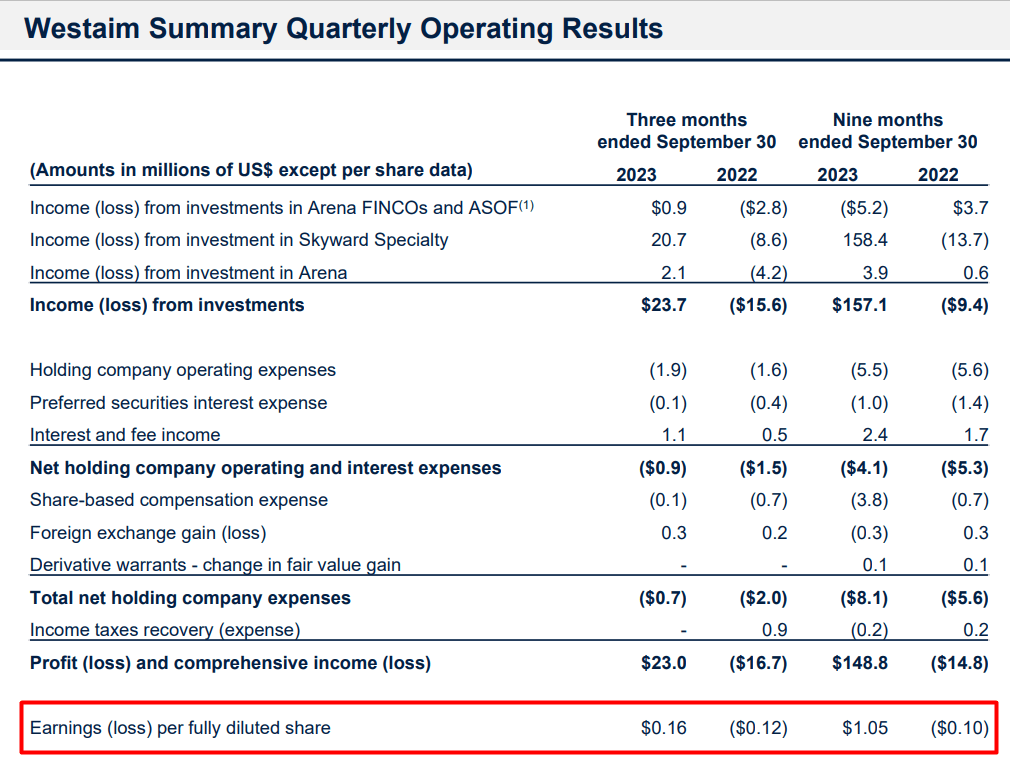

In Q3 Westaim reported robust performance across its operating segments. In the Arena segment the net income attributable to AIGH (100%) stood at $4.1 million, a significant improvement from the Q3 2022 net loss of $8.2 million. However, committed assets under management ((AUM)) decreased to $3.3 billion at September 30, 2023, from $3.5 billion at December 31, 2022. The AUM pipeline for Arena remains strong, with AIGH EBITDA reaching $4.6 million in Q3 2023, compared to a loss of $7.8 million in Q3 2022.

In the Arena FINCOs segment, Q3 2023 net income was $0.9 million, marking a positive turnaround from the Q3 2022 net loss of $2.6 million. The fair value of Arena FINCOs was $148.1 million at September 30, 2023, down from $160.1 million at December 31, 2022. Westaim received a cash distribution of $6.9 million from Arena FINCOs in YTD 2023, contributing to the segment's overall performance.

Skyward Specialty Insurance Group ( SKWD ) exhibited strong financial results in Q3 2023. Net Income (100%) reached $21.7 million, a significant improvement from the Q3 2022 net loss of $2.4 million. Underwriting performance remained robust with a combined ratio of 90.2% in Q3 2023. Net investment income increased to $13.1 million in Q3 2023, contributing to a total stockholders' equity of $535.4 million. The company reported a Q3 2023 annualized return-on-equity ((ROE)) of 16.4%, showcasing solid financial health and performance.

As a result of all these factors, the company recorded phenomenal EPS growth rates for Q3 and YTD:

{kind=link}

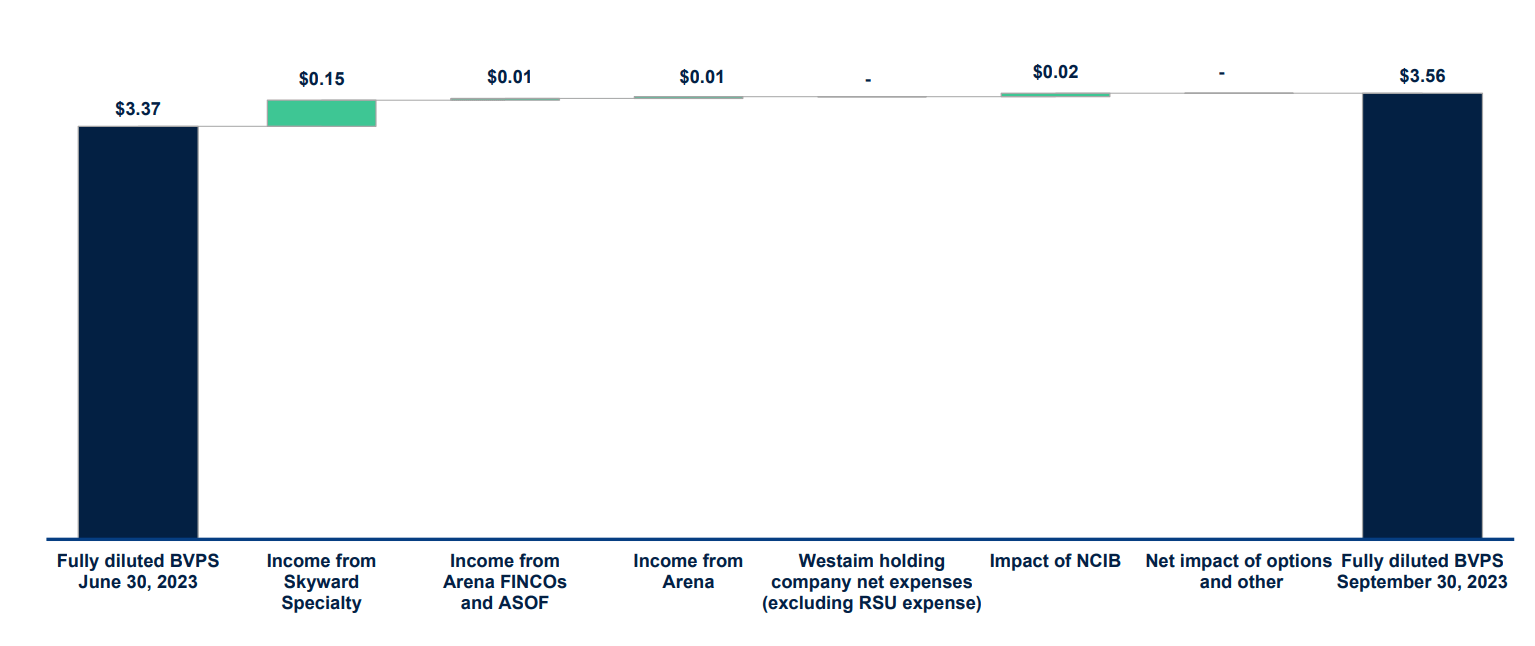

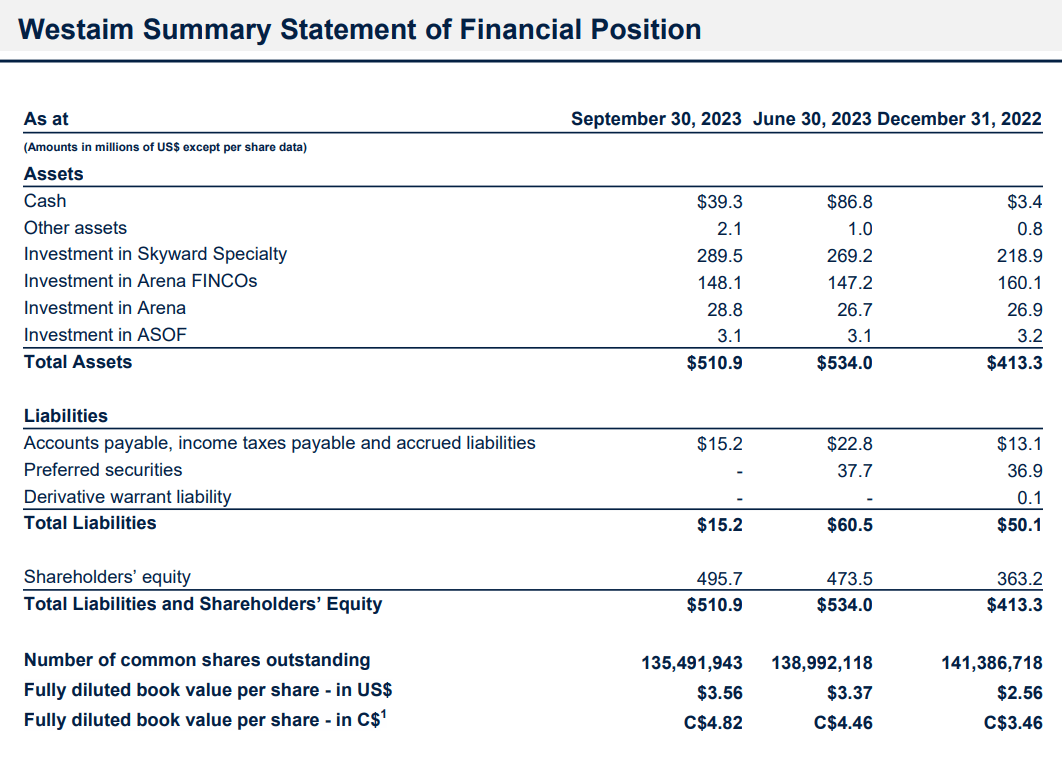

In Q3 2023, Westaim demonstrated significant improvement in its balance sheet. The book value per fully diluted share experienced a notable increase, rising by $1.00 (+39.1% YTD) to $3.56 at September 30, 2023.

{kind=link}

From what I can see, Westaim strategically utilized its strong cash position at the beginning of the quarter for various financial moves. The company deployed cash to redeem its preferred securities liability after the quarter-end, leading to a redemption and delisting of all 5,000,000 preferred securities for C$50 million on July 17, 2023. Additionally, Westaim sold 3,987,500 Skyward Specialty common shares in a Secondary Offering during Q2 2023, receiving net cash proceeds of $87.4 million. As of September 30, 2023, Westaim retained ownership of 10,579,639 Skyward Specialty common shares. Furthermore, in Q3 2023, Westaim acquired and canceled 3,740,478 common shares at a cost of $9.8 million, contributing to the overall enhancement of its financial position. So far in YTD 2023, the company acquired and canceled 6,135,078 common shares at a cost of $16.3 million through its normal course issuer bid ((NCIB)), showcasing a commitment to optimizing its capital structure.

{kind=link}

As far as I can see from the company's data, all 3 other divisions should continue to recover in the medium term.

Firstly, Arena. Since its launch in 2015, it has deployed >$5.2 billion into 370+ privately negotiated transactions, emphasizing a credit-oriented and asset-backed approach that deviates from traditional private credit. With 149 active positions, the underwritten IRR stands at 17.9%, while the current IRR, reflecting all investment activity, is at 8.4% as of Q3 FY2023. Moreover, Arena's end-to-end IT systems ensure robust governance, transparency, and a competitive edge, while maintaining an average transaction size of <$50 million, differentiating itself from larger competitors. As the post-crisis bull market evolves, Arena's unique world-view attracts private credit investors, positioning the company for continued success.

Secondly, Arena FINCOs. With 52% of the portfolio invested in equity, REO, and hard assets, the composition contributes to fair market value volatility, reflected in unrealized net gains (losses). As a representation of Westaim's proprietary capital, Arena FINCOs invests in Arena Investors' core multi-strategy, occasionally serving as the lead or seed investor in Arena product offerings. So this strategic role positions Arena FINCOs to contribute to the growth and development of the business. Despite a reduction in net assets in YTD 2023, which included a distribution of $6.9 million to Westaim, the financial maneuvering underscores the strategic distribution approach, with the YTD 2023 distribution totaling $10.3 million, indicating a dynamic and forward-looking financial stance.

Thirdly, Skyward Specialty . It's an expanding and forward-thinking specialty insurance firm, offering commercial property and casualty products and solutions on both non-admitted and admitted bases. Their strategic focus centers on establishing defensible positions in high-profit niche segments, ensuring consistent top quartile returns. The company's success is attributed to top-tier talent, driving disciplined underwriting, claims excellence, and efficient capital management. The company's financial strength is reflected in its total stockholders' equity, which saw a 27.0% increase to $535.4 million from Q4 2022. This growth was primarily fueled by net IPO proceeds of $62.4 million and YTD 2023 net income. Skyward Specialty's robust financial position is underscored by a debt-to-capitalization ratio of 19.4% as of September 30, 2023, emphasizing its stability and continued strength in the insurance market.

All in all, Westaim seems attractive to me from the point of view of its operational activities. But what about the valuation of the stock?

Westaim's Valuation

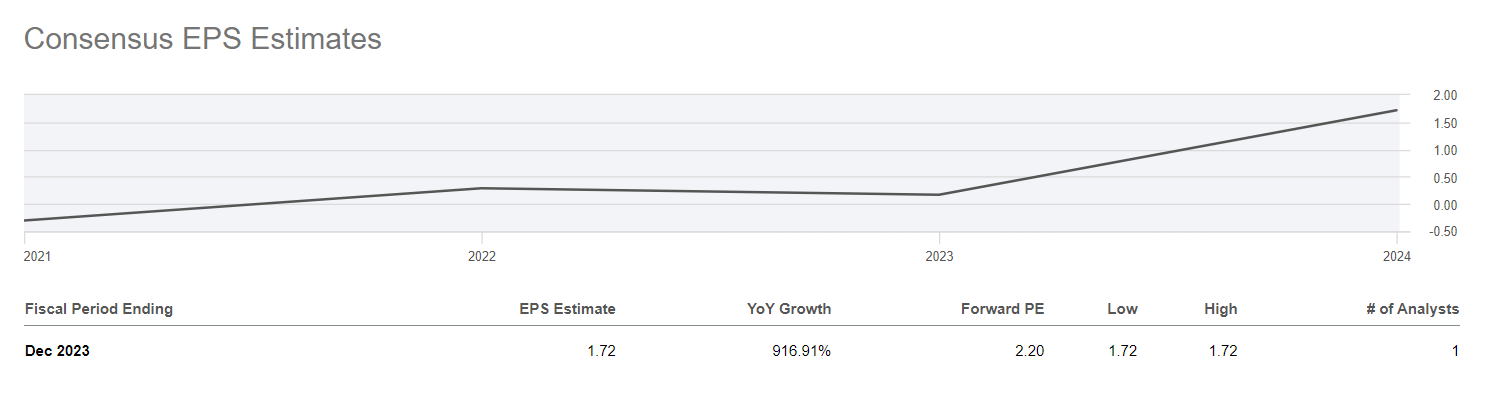

The problem with valuing companies like Westaim is the paucity of coverage by major banks and therefore the lack of clear and reliable consensus forecasts that investors usually rely on in their due diligence. So all we see when we look at Westaim's earnings estimates is just one analyst forecasting EPS growth of 916.91% YoY for FY2023 and no forecasts beyond that at all.

{kind=link}

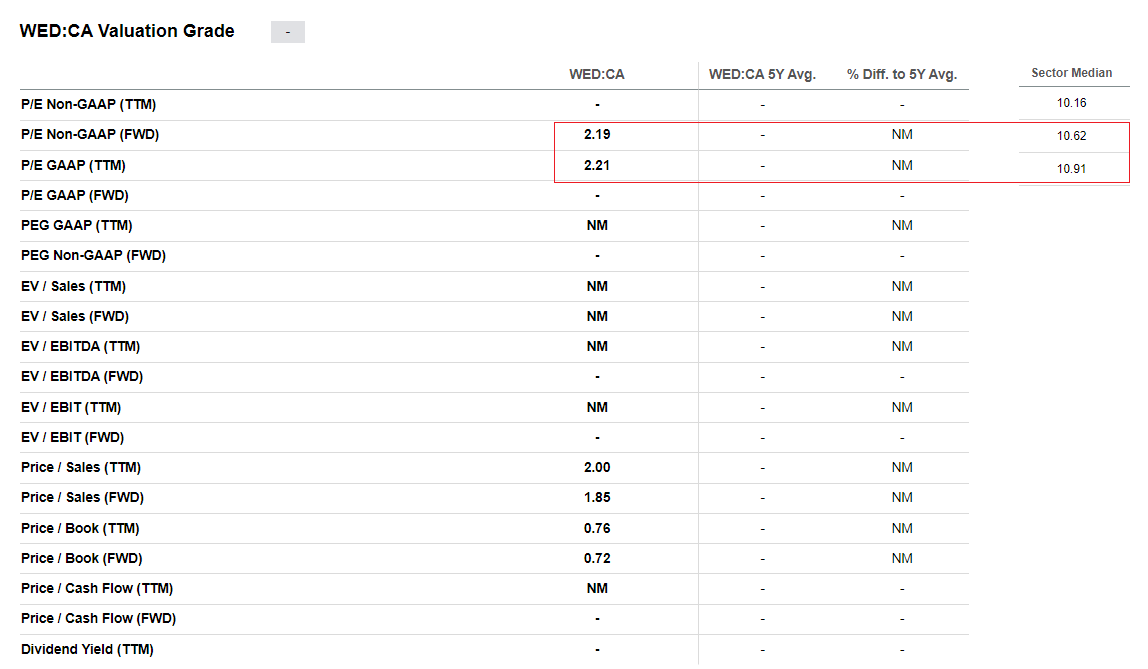

However, pay attention to the implied P/E ratio for FY2023 - it is only slightly above 2x. That means if you put aside the value of the company's assets and only consider net earnings, Westaim is trading at a price of just over 2x its annual net income, which looks insanely cheap compared to the sector as a whole .

{kind=link}

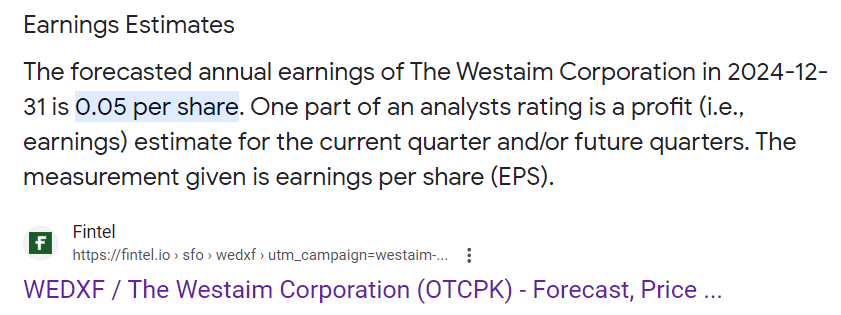

The Internet is full of unrealistic, in my opinion, EPS forecasts for 2024. Fintel , for example, gives an EPS of $0.05 for FY2024:

{kind=link}

I don't believe this forecast as the FY2023 EPS forecast of $0.24 seems completely off the mark with YTD EPS of $1.05.

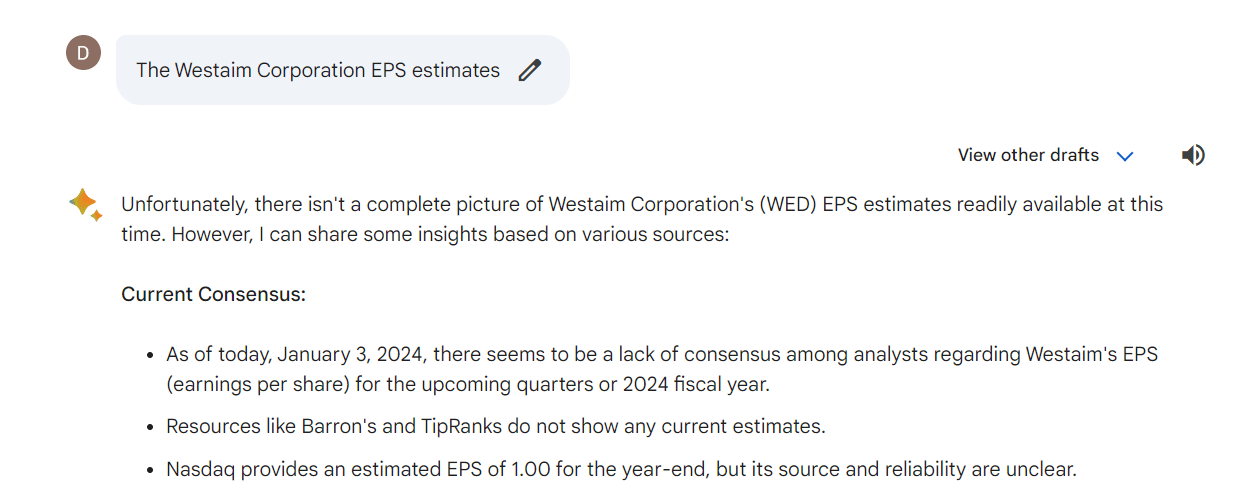

Google's Bard's response to the request for projected EPS data refutes my conclusion that Westaim is a real hidden gem that is not being covered. However, Bard was able to find an EPS figure of $1.0 for FY2024, though its source is unknown.

{kind=link}

But even if we assume that Westaim only earns half of what Bard states, this still results in an implied P/E ratio of ~7.56x, which is below the median of the sector.

The Verdict

Before investing in Westaim Corp. stock, one should take into account several key risks. First, being a private equity firm, detailed financial information is not readily available to the public, and the stock's lack of trading on major exchanges limits liquidity. Second, the company's investment focus on early and mid-stage ventures introduces a higher risk and potential for volatility compared to established businesses. Third, Liquidity challenges arise due to the stock's restricted tradability, hindering quick buying or selling of shares. Additionally, Westaim may employ leverage in its investment strategies, amplifying both gains and losses, leading to increased volatility. Operating in a complex regulatory environment, changes in regulations pose potential risks to the company's operations and the value of its investments.

But despite these risks, Westaim still seems very attractive to me as a medium-term investment. The stock looks insanely cheap, which is explained by a lack of information in the market - uncertainty always rewards companies with a valuation discount. However, I think investors will have more and more information available as the company reports through 2024 and will move the stock in the direction that this information tells them to. Based on the company's fundamental profile, I expect the upward trend to continue.

Thanks for reading!

For further details see:

Why I'm Still Bullish On The Westaim Corporation Stock