CA - Why I Would Sell Blackstone's BREIT To Buy REITs Instead

Summary

- Blackstone claims that its REIT is superior to others.

- I think that it is inferior and yet it is a lot more expensive.

- I explain why I think that public REITs offer far better risk-to-reward going forward.

Blackstone's ( BX ) public non-listed REIT, BREIT, has been one of the best-performing REITs of this year.

It has managed to deliver a 9% total return with low volatility even as the public REIT market ( VNQ ) dropped by nearly 30% on average:

The manager, Blackstone, is of course very proud of this outperformance. They explain on a conference call earlier this year that:

"For the first six months of the year, our real estate strategies appreciated 9% to 10% versus a 20% decline in the REIT index , equaling an outperformance of roughly 3,000 basis points. I don't know many asset classes that perform -- outperform indexes by 3,000 basis points." [added emphasis]

That's great!

But what about today? Is now still a better time to invest in BREIT, or should you rather consider public REITs?

Blackstone would of course argue that BREIT is the better investment opportunity because BREIT is uniquely attractive for a number of reasons:

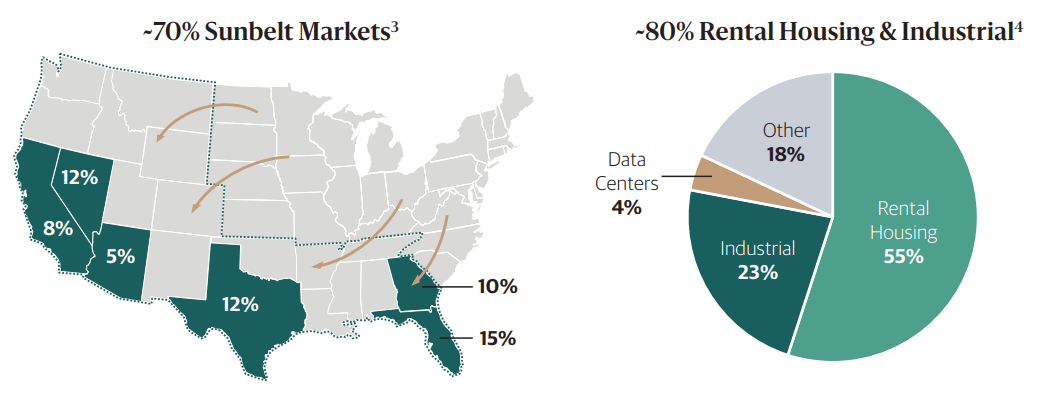

- It is heavily invested in rapidly growing sunbelt markets.

- It owns mainly rental housing and industrial properties.

- Its rents are growing rapidly.

- It has a strong balance sheet with mostly fixed-rate debt.

{kind=link}

Blackstone

I strongly disagree.

Blackstone of course wants you to think that BREIT is the better opportunity because it earns fees for managing it.

But I think that public REITs are today far more opportunistic than BREIT. If I owned BREIT, I would try to get out of it to invest in public REITs instead.

Here are 5 reasons why:

Reason #1: Public REITs are much cheaper today

This is the most important reason. Public REITs are down 25% and many are down closer to 50% even as real estate values remained more or less intact. Cap rates have expanded a bit, but so has the property NOI in most cases.

As such, many REITs are now priced at large discounts relative to the underlying value of the real estate they own. In many cases, the discount is 20, 30, 40, or even 50% in extreme cases. This means you can buy real estate at 50 cents on the dollar through the public market. Just to give you a few examples of REITs that own similar properties as BREIT:

- Camden Property ( CPT ), a sunbelt-focused apartment REIT, is currently priced at a 25% discount to NAV.

- BSR REIT ( BSRTF ), a Texas-focused apartment REIT, is currently priced at a 40% discount to NAV.

- EastGroup Properties ( EGP ), a sunbelt-focused industrial REIT, is currently priced at a 25% discount to NAV.

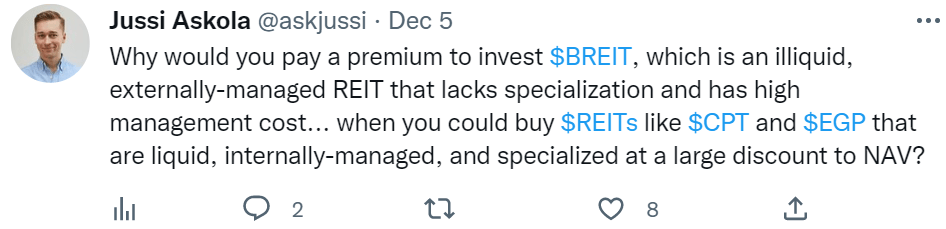

Why would you pay a much higher valuation to invest in BREIT instead?

{kind=link}

Twitter Jussi Askola

{kind=link}

Twitter Jussi Askola

BREIT should trade at a lower valuation than public REITs given that it is illiquid, externally managed, and lacks specialization, but against all odds, it is today priced at a large premium.

Reason #2: Public REITs are more cost-efficient and better aligned with shareholders

BREIT is an externally-managed REIT. This means that there is an external asset manager, in this case, Blackstone, that takes care of the management in exchange for fees. It gets paid a 1.25% of the NAV each year as well as 12.5% of the annual total return subject to a 5% hurdle. There are also selling commissions upfront that can amount up to 3.5% and stockholder servicing fees that can add up to 0.85% each year.

That's a lot of fees!

Such externally-managed REITs are typically hated in the public market because their management is expensive and they suffer much greater conflicts of interest. They always want to grow because it maximizes the fees that they own. It leads to "growth at all costs", which hurts returns, and this is why such externally-managed REITs are disliked by investors. Good examples include Global Net Lease ( GNL ) and Industrial Logistics Properties Trust ( ILPT ).

But most public REITs are internally-managed. This is a much better management structure because the management is hired as employees of the REIT. It results in significant economies of scale and better aligns interests with shareholders because they earn salaries based on their performance and not just the mere size of the company.

The average annual cost of a public internally-managed REIT is around 0.6%, and some REITs like Realty Income ( O ) have it as low as 0.4%.

{kind=link}

Realty Income

Reason #3: Public REITs offer better diversification potential

Blackstone will often claim that BREIT is superior to public REITs because it supposedly provides better diversification benefits.

They claim that, unlike public REITs, BREIT is uncorrelated with the public stock market because it is a non-listed real estate investment vehicle.

But I don't agree.

Just because something isn't quoted does not mean that it isn't correlated or volatile. Proof in point: BREIT just had to limit withdrawals because too many investors are currently seeking to get out of it. If you can't get your money back, does the "paper valuation" then have any meaning?

Public REITs are liquid and naturally, this will result in some volatility, but at least, you are not lying to yourself, thinking that something isn't volatile just because it isn't traded.

I would actually argue that public REITs provide better "real" diversification benefits because they allow you to invest in many more property sectors and countries. To give you an example, at High Yield Landlord, we hold an international Portfolio with REITs from 6 different countries. Our largest position, Vonovia (VONOY) (VNNVF), is the biggest landlord in Germany. It is today priced at just 35 cents on the dollar due to the war in Ukraine and we think that it is very opportunistic.

If we were just investing in BREIT, we would miss these opportunities to gain geographic diversification.

Reason #4: Public REITs are liquid

BREIT has a redemption plan, but as we highlighted in a recent article, this redemption plan can be quite restrictive and Blackstone recently limited withdrawals because too many investors sought to get at out at once.

This limits your ability to get in and out of the real estate market, increasing risks, and potentially also limiting your ability to act on new investment opportunities. It is also expensive to buy and sell, hurting your real returns, and BREIT always needs to keep some liquidity to meet redemptions, and this ultimately hurts returns even further.

With public REITs, you have much more flexibility. You can buy or sell with minimal fees with just a few clicks of mouse. Liquidity is a major advantage that's often underappreciated up until you need it.

Reason #5: Public REITs offer higher yields and more upside

Last but not least, since REITs are today priced at large discounts to fair value, they also pay a higher yield and offer a lot greater upside potential.

BREIT offers a 4.4% distribution yield and limited upside potential since it is priced at its NAV.

Public REITs, on the other hand, trade at a >6% dividend yield in many cases with lower payout ratios, and also offer significant upside potential since they are priced at large discounts to their net asset value.

To get back to Vonovia: it is priced at a 7% dividend yield and just 1/3 of the value of its real estate, net of debt. Even if you expected its property values to drop a bit, its share price could still double before reaching its net asset value. Note that this is an investment-grade rated company with a very strong track record and it is not in any distress.

I think that the risk-to-reward of these discounted public REITs are far better.

Bottom Line

Blackstone of course wants you to invest in BREIT because they earn fees for managing it. To be fair, BREIT is a pretty vehicle and it has a strong track record.

But it is hard to ignore the huge disparity in valuations between BREIT and Public REITs in today's market. Even Blackstone's COO indirectly told us in the Q2 conference call that public REITs are a lot more opportunistic today:

"The best opportunities today are clearly in the public markets on the screen and that's where we're spending a lot of time."

Therefore, I continue to accumulate real estate through the public market. It is a lot cheaper and offers better upside potential going forward.

For further details see:

Why I Would Sell Blackstone's BREIT To Buy REITs Instead