METV - Why The SVB Collapse Is Positive For Industrial Technology

2023-03-20 15:15:00 ET

Summary

- SVB collapse, consequences, and implications for technology.

- Role of productivity improvement in addressing inflation.

- What we learned from industrial tech earnings - identifying focus areas within our macro framework.

The collapse of the Silicon Valley Bank ( SIVB ) ("SVB") rattled the markets, but the consequence are yet to be felt. In this report, we dive deeper into why we believe this is a systematic problem and why it creates a positive set-up for industrial technology.

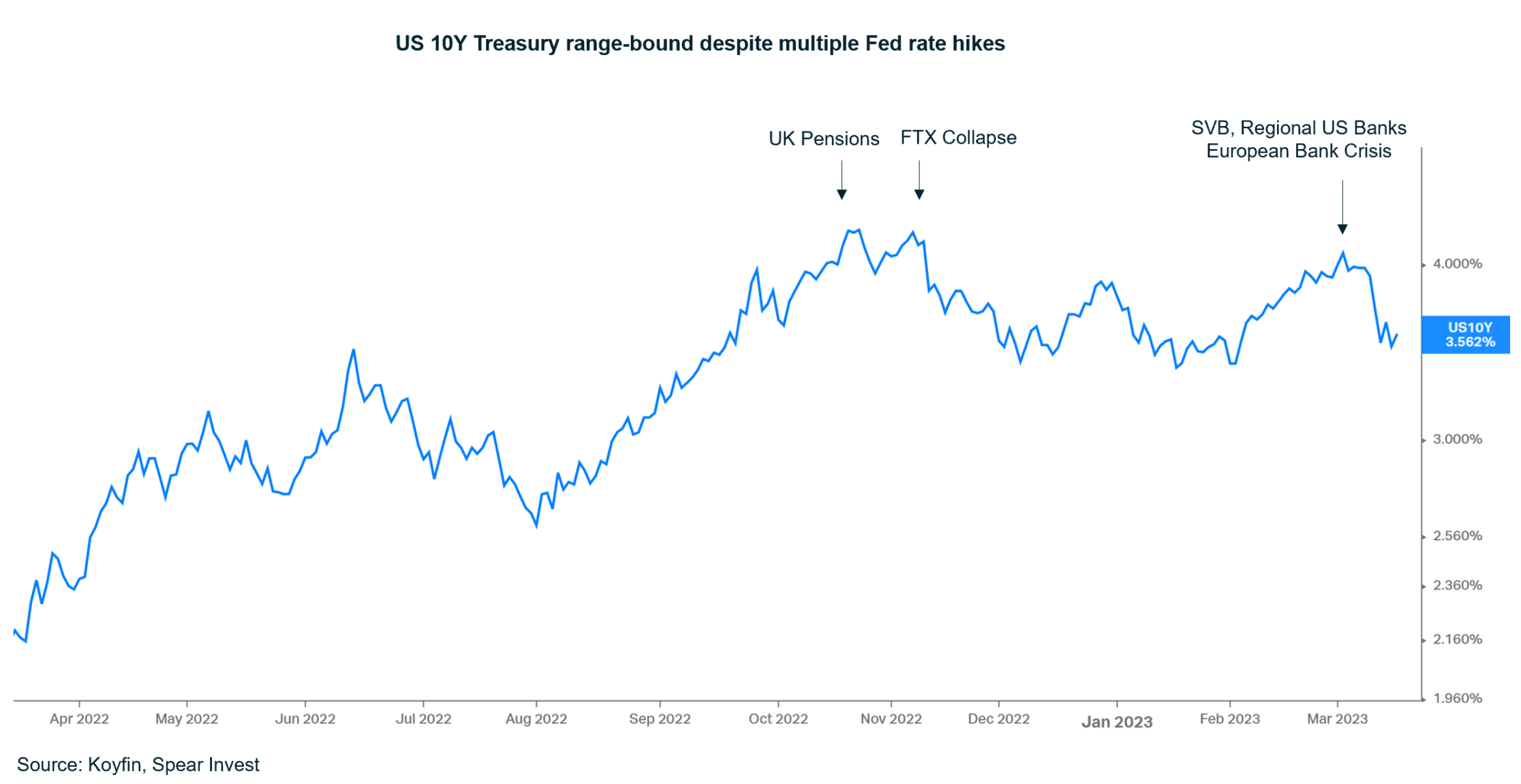

Our base-case framework for the next 5 years is very slow economic growth, high inflation, and interest rates (10Y) at ~3.5%. We believe that productivity improvement will be the only way to address inflation on a structural basis. Industrial technology can outperform in this type of an environment.

Why SVB is a systematic problem

We believe that SVB was not a one-off, but a systematic problem that is just starting to trickle across the banking system globally. While the SVB collapse was caused by a unique set of circumstances (i.e., concentrated depositor base reliant on the VC ecosystem), we believe that the depositor concentration was the catalyst and not the underlying problem. Rapid increases in the risk-free rate has created large unrealized losses on the balance sheets of many institutions (including, but not limited to, banks).

While the public equity market was very quick to price in the rapid interest rate increases, with many high-growth stocks down 70% from their peaks by 2Q22, only months after the Fed begun tightening, other asset classes were not marked down as quickly even though they are facing the same dynamic. The challenges are not only limited to banks/MBS, but include:

- Risky FCF negative private investments marked at a premium to their publicly traded comps

- Potential bankruptcies from companies that have maturities coming due in the next 2 years, needing to replace free money with debt at prevailing market rates (if that is even an option)

- Auto loans issued at ~1% interest rate on car values above MSRP

- Corporate loans to risky companies (FCF negative) with lower interest rates than the risk-free rate

- Convertible debt that yields ~0% interest with way out-of-the-money options

- Governments outside of the US that are reliant on borrowing (e.g., Japan)

The consequences have started to emerge over the past week: regional banks under pressure, which will likely lead to more consolidation in the US, European banks under severe pressure already resulting in bank rescues ( UBS stepping in to take over Credit Suisse ( CS ), almost entirely wiping out equity holders with heavy government guarantees). Likely more to come.

In short, every time the 10Y reaches 4%, something breaks. In October/November, we had the UK Pension crisis and the FTX ( FTT-USD ) collapse. While the market wrote off those two events as isolated, the banking crisis is very different. We believe that this crisis creates a ceiling for the 10Y, and even if the Fed continues to raise interest rates, it will be hard to push those to the real economy.

Ceiling on interest rate is a significant positive for for technology stocks, as they have already taken a significant hit and are pricing in a risk-free rate >4% (10Y). Moreover, we believe an environment of persistently higher inflation will be positive for industrial/B2B companies, as productivity improvement will be key in structurally bringing down inflation.

{kind=link}

Tighter credit = slower growth. We expect liquidity to dry up, and less liquidity generally means slower growth. This creates a tough set-up for companies that do not generate cash flow. We believe that small/mid-sized businesses and start-ups could be hardest hit. Conversely, companies that do generate cash flow and can self-fund their growth (both organic and M&A) could get a valuation premium.

It is important to note that this crisis is the reverse of what a typical crisis looks like. A typical crisis is usually caused by overcapacity, which is then followed by credit defaults (borrowers unable to meet their obligations) and finally the government comes to the rescue. In this case, there is no overcapacity, the borrowers are in a decent shape and locked in attractive deals, but it is the lenders that are getting the short end of the stick.

B2B technology and inflation

Our research suggests that while inflation has cooled off since 2022 levels, it will be very difficult to bring it down to the 2% goal. Fed rate hikes have been effective in slowing the economy down, but we are reaching a point where the marginal benefit is not outweighing the costs.

An example is shelter inflation. While the housing market has significantly cooled off and rents have declined, we are starting to note capacity constraints. The general expectation is that shelter inflation will follow rents, but we may actually see a version of the reverse. With limited capacity and higher mortgage rates, rents may actually start increasing.

Our channel checks indicate that inflation is much more sticky than most investors believe. There are structural drivers that are at the core, e.g., re-shoring/de-globalization, ESG, capacity constraints.

As we emerge out of this downturn, we expect that wage inflation will re-surface as a challenge. We believe that productivity improvement will be the only way to address inflation structurally.

We are at the cusp of significant artificial intelligence ((AI)) developments that will have game-changing impact on productivity. Today, the largest application of AI at scale that falls within the productivity theme is AI used in code development. Microsoft's ( MSFT ) GitHub already has 1 million developers that have used GitHub Copilot (its AI assistant) to date. According to Microsoft, users are 55% more productive, and 40% of code they are checking is AI-generated and unmodified.

Several companies have since announced new AI integrations: AI for CRM systems (Salesforce ( CRM ) and HubSpot ( HUBS ) writing assistants), AI as a shopping assistant (Shopify ( SHOP )), etc. It is important to note that embedding AI in an application will be a requirement rather than a differentiator, similar to having a website or a mobile version of it. While we are in the early days, we believe that the productivity gains will be visible systemwide even in a medium-term (3-5 year) time frame.

Opportunities in industrial technology - 4Q22 earnings takeaways

The majority of our technology coverage universe reported earnings over the past month, and the overall results were underwhelming. The theme across all reports was similar to last quarter: elongated sales cycles, customers only purchasing what they need, splitting up large deals in small pieces, etc.

On the positive side, semiconductor fundamentals have clearly bottomed, with Nvidia ( NVDA ) expecting qoq growth in all segments. This is very significant, as semis usually lead the rest of enterprise software out of a downturn.

We noted few clear trends coming into 2023 from this earnings season:

- Cost cutting is just starting to show up in results (Salesforce, Meta ( META ), HubSpot);

- Early-cycle semiconductor fundamentals are bottoming (Nvidia, AMD );

- Platforms are performing better than point solutions (Palo Alto Networks ( PANW ), CrowdStrike ( CRWD ));

- "Must-haves" such as cybersecurity performed better than "nice-to-haves" such as DevOps, collaboration tools.

We expect that these themes will continue for the rest of the year. We will dive deeper into each trend in our next report.

{kind=link}

Original Source: Author

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Why The SVB Collapse Is Positive For Industrial Technology