FTS - Why We're Not Buying Canadian Utilities Right Now

Summary

- Investors typically buy utilities for current income.

- The discussed Canadian utilities have generally experienced slower dividend growth recently.

- It had largely to do with slower earnings growth than dividend growth in the last 10 years.

- It's not the best time to buy Canadian utilities as they're generally slow growth and they're not trading at attractive valuations. At best, they're fairly valued.

- Of the four utilities, if we had to pick one to invest now, we'd go with Fortis.

Canadian Utilities ( OTCPK:CDUAF )( CU:CA ) is a global energy infrastructure company that has assets in North and South America and Australia. Its utility business consists of electricity and natural gas transmission and distribution operations. Its energy infrastructure operations include energy storage, energy generation, industrial water solutions, and clean fuels.

The TSX stock has earned the prestige of being the Canadian Dividend Aristocrat with the longest dividend growth streak of 50 years. This is quite an achievement indeed.

[The figures in this article are in Canadian dollars unless otherwise noted.]

At the recent quotation of C$40.49, the stock trades at about 17.5 times earnings and yields 4.39%. That's a decent yield, fitting for a stable utility with an investment grade S&P credit rating of BBB+. As a result, some investors might own the dividend stock for income generation.

However, the utility's long-term earnings-per-share ("EPS") growth rate is not stellar. Specifically, its 10-year adjusted EPS growth rate is 2.29%. It's no wonder that its dividend growth rate ("DGR") has slowed in recent years because the payout ratio can only expand so much.

Specifically, its various DGRs are as follows:

- One year: 1.0%

- Three year: 3.8%

- Five year: 6.2%

- Ten year: 8.1%

Canadian Utilities' payout ratio has expanded from 2011's 46% to last year's 81%.

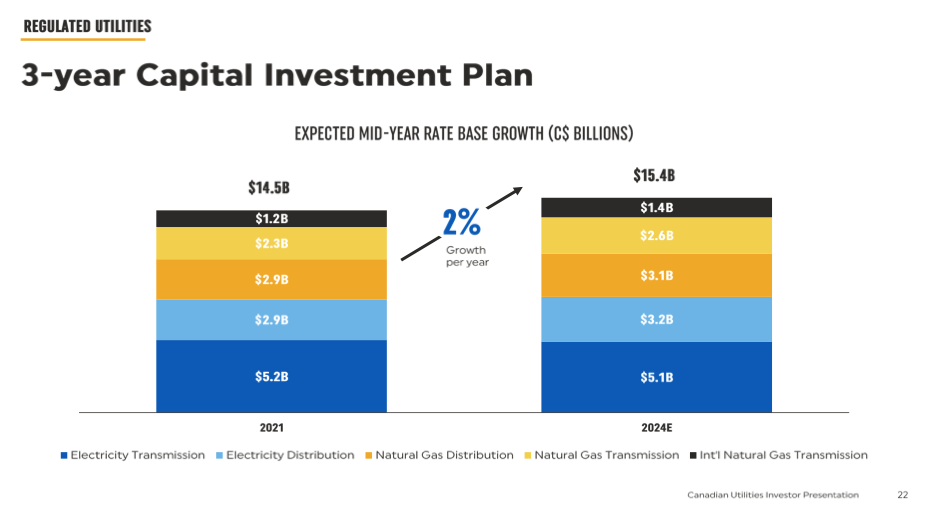

From 2021 to 2024, the utility estimates its rate base growth rate to be 2%, which aligns with its 10-year growth rate. But again, the growth rate underperforms those of its peers.

{kind=link}

Here are other Canada-based utilities that investors can consider:

Hydro One

Hydro One ( OTCPK:HRNNF )( H:CA ) is a relatively new publicly-traded utility, but its history stems back to 1906. It's a regulated electric utility in Ontario, the most populous province in Canada. The province owns close to half of a stake in the business, but the stock has no liquidity issue, as Hydro One stock's average trading volume is over 1.1 million and close to 80% higher than Canadian Utilities' volume.

In any case, Hydro One's five-year adjusted EPS growth rate is 5.88% versus Canadian Utilities' -0.4%. Hydro One's 5-year DGR is 4.6%.

The utility's latest estimate is a rate-base growth of approximately 6%. Having a higher-growth profile and an S&P credit rating of A-, accordingly, Hydro One stock trades at about 21.7 times earnings and offers a lower yield of 3.1%. The stock appears to be, at best, fairly valued.

Emera

Emera ( OTCPK:EMRAF )( EMA:CA ) earns revenues from six utilities. It generates about 63% of its adjusted earnings from the U.S. About 95% of the utility's adjusted earnings is regulated.

It has a 15-year dividend growth streak, which is considered to be fairly long on the TSX. Its 10-year adjusted EPS growth rate is 4.7%, which along with a payout ratio expansion from 74% to 92% drove a DGR of 7.0% in this period.

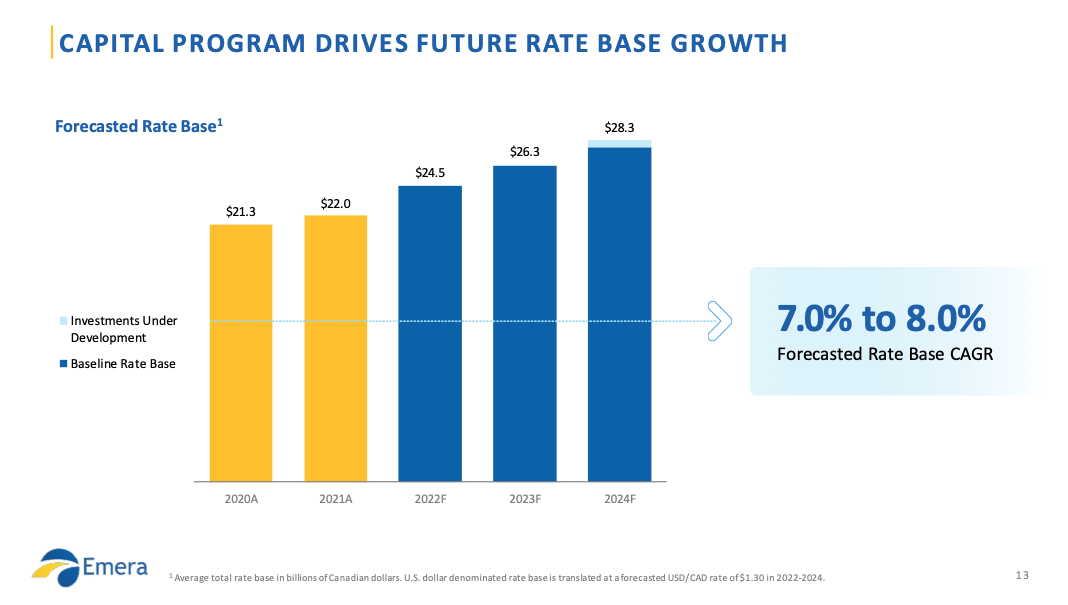

As a result, the utility's more recent DGR has rightly slowed. Its five-year DGR is 5.2%. Management has targeted a rate base growth rate of 7-8% from 2020 to 2024. And it plans to continue with a DGR of 4-5% through 2024 to help drive down the payout ratio to healthier levels.

{kind=link}

Notably, about 70% of its current capital plan is focused in Florida. The "Sunshine State" is the fourth-largest economy in the U.S. and experiences faster economic growth versus the country average.

At C$61.08 per share at writing, Emera stock trades at about 20.8 times earnings and offers a yield of 4.3%. The S&P credit rating BBB stock also seems to be fairly valued.

Fortis

Fortis ( FTS )( FTS:CA ) consists of 10 regulated utility businesses. Like Emera, it generates a meaningful portion of its earnings from the United States. Fortis generates about 65% of its operating earnings in the U.S. and the Caribbean.

It has impressively increased its dividend for 48 consecutive years. Its 10-year adjusted EPS growth rate is 4.4%, which along with a payout ratio expansion from 69% to 79% drove a DGR of 5.9% in this period.

{kind=link}

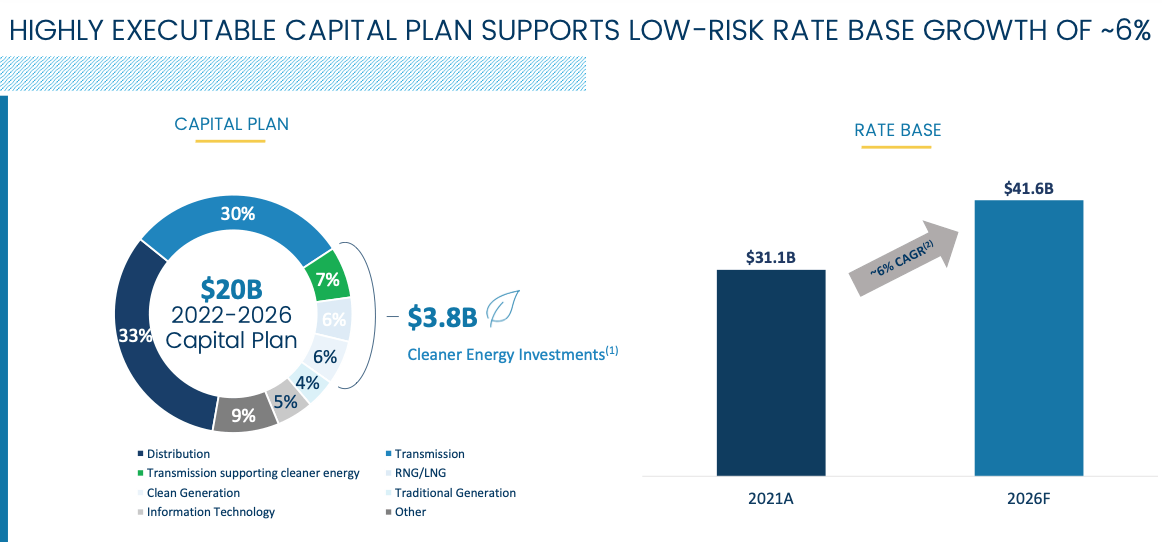

From 2021 to 2026, Fortis targets a low-risk rate base growth of approximately 6%. As well, it aims for a DGR of roughly 6% through 2025. The stock yields almost 3.7% at C$58.57 per share, which is roughly 21.7 times earnings.

Conclusion

Other than Hydro One stock that doesn't have a long enough publicly-trading history, Canadian Utilities and Emera's dividend growth rates have been on a decline. Fortis stock has had the most stable dividend growth rate which maintained roughly at the 6% level over the last one, three, five, and 10 years. (In the past one, three, and five years, Hydro One's dividend growth rate has been consistently at about 5%.)

These utilities are typically stable businesses that investors buy for current income. Additionally, investors can get stable total returns in the long run as long as they don't overpay for the shares and the utilities are able to grow at satisfactory growth rates.

Ideally, of course, you'd buy your favorite utility stock on the cheap. Right now, they're at best fairly valued, which is why Canadian utilities aren't at the top of our buy list currently.

If we had to pick one utility to invest in among this group, we'd go with Fortis for its diversity and consistency.

The results speak for themselves - it's probably a good idea to avoid Canadian Utilities as it has underperformed its peers in the last five and 10 years. Here's a 10-year total return chart based on an initial $10,000 investment.

Here's a 5-year chart that includes Hydro One.

References

- Florida Economic Estimating Conference

- The Conference Board Economic Forecast for the US Economy

For further details see:

Why We're Not Buying Canadian Utilities Right Now