ACTV - Will The Surge In Interest Rates Cause A Recession And Bear Market?

2023-10-06 08:45:00 ET

Summary

- Investors await jobs report to determine Fed's next move on interest rates.

- Wage growth and revisions to previous monthly totals are key factors to watch.

- Household and corporate debt levels suggest the economy is less sensitive to rising interest rates.

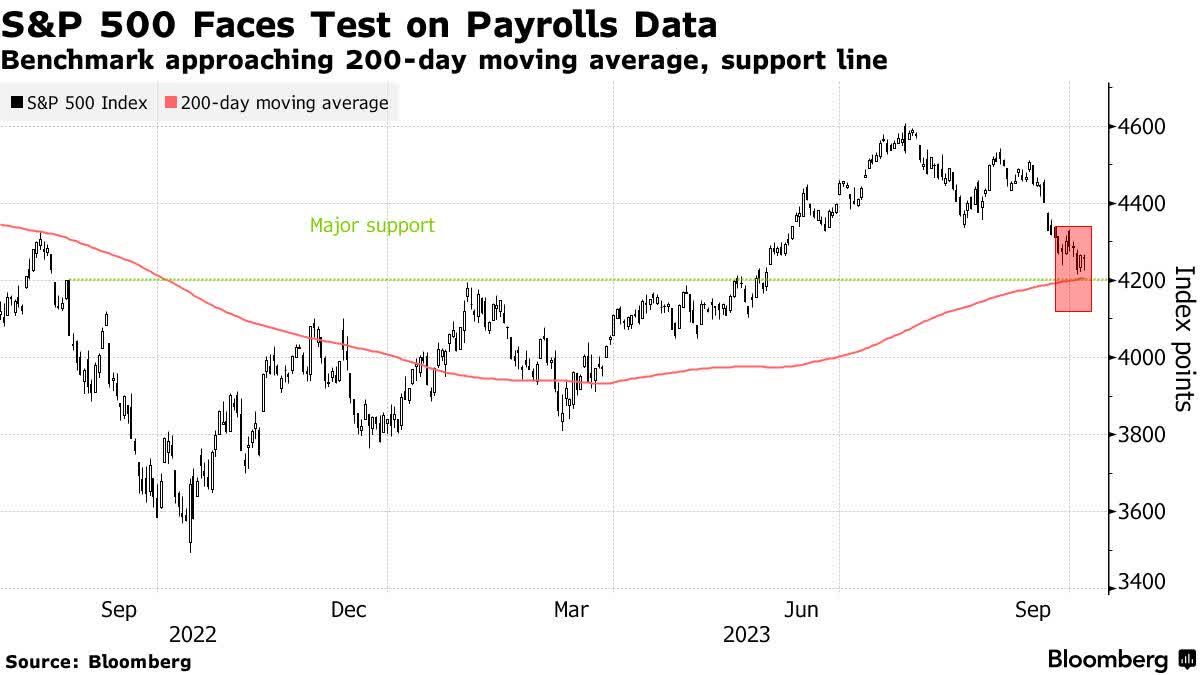

While long-term interest rates stabilized, the major market averages all edged lower, as investors brace for this morning's jobs report, which pundits say will help determine whether the Fed holds steady or raises rates again at its November meeting. Weekly unemployment claims remain stubbornly low with just 207,000 filing in the latest week, but the number investors should focus on tomorrow is wage growth. If wage growth continues to moderate, that should trump a jobs number that is stronger than expected. Additionally, the revisions to previous monthly totals have been leaning south for several months, which tells us that the labor market is cooling.

{kind=link}

I continue to think this debate about whether the Fed will raise rates again is absurd, but so long as Fed officials are afraid to acknowledge the progress we have made on the inflation front, they will lean hawkish. That will feed the bearish narrative of higher for longer rates. Supposedly, higher interest rates are the death knell of this expansion and bull market, but few recognize that our economy is not as sensitive to rising rates as it has been during previous business cycles.

{kind=link}

It is true that when interest rates go up rapidly, consumers tend to spend less on goods and services, businesses tend to spend less on equipment and expand, corporate profits are negatively impacted, and unemployment increases. This combination can result in an economic contraction, which is why so many expect one. Yet there are aspects of this business cycle that go underappreciated, which I think will help us avoid such a contraction.

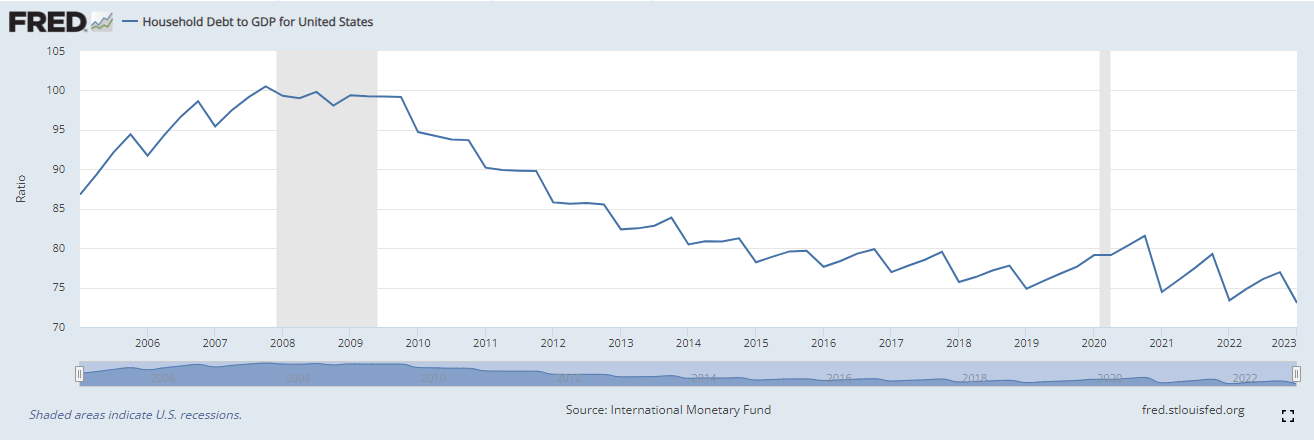

For all the concern about overleveraged consumer balance sheets, household debt as a percentage of U.S. gross domestic product has fallen from more than 100% during the Great Financial Crisis in 2008 to a two-decade low of 77%. This is a result of more responsible lending standards and more reasoned consumers. Yes, we are seeing an increase in delinquency rates for credit cards and auto loans, but these are falling closer in line with pre-pandemic levels. The stimulus-induced levels of 2021-2022 were not sustainable. The picture of overall household debt tells a much better story.

{kind=link}

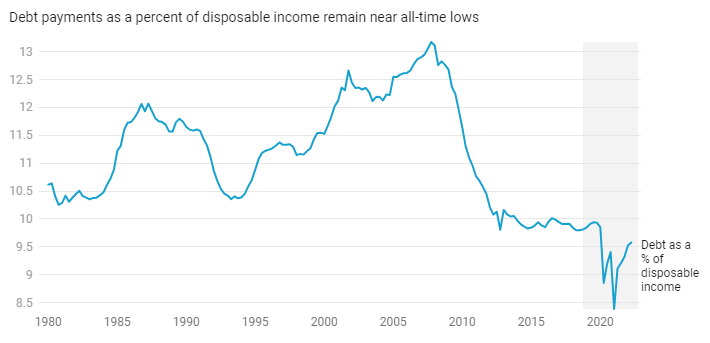

I keep hearing about how credit card debt has surpassed $1 trillion . That's a big number that is bound to scare anyone, but it has to be viewed in the context of the size of the overall economy, which consistently grows, and the cost to service the debt. There has been a dramatic decline in the amount of after-tax income required to service outstanding debt. The debt servicing ratio fell from a record high 13.2% to an all-time low during the pandemic, and it remains near a multi-decade low of 9.6%.

{kind=link}

The decline in outstanding stock of debt is the reason that the 520 basis points in rate increases by the Fed over the past 18 months only resulted in a 1.5% increase in the percentage of disposable income required to service that debt. This is helping to sustain consumer spending levels, and prolong the expansion, but it isn't just the consumer who is less sensitive to changes in monetary policy.

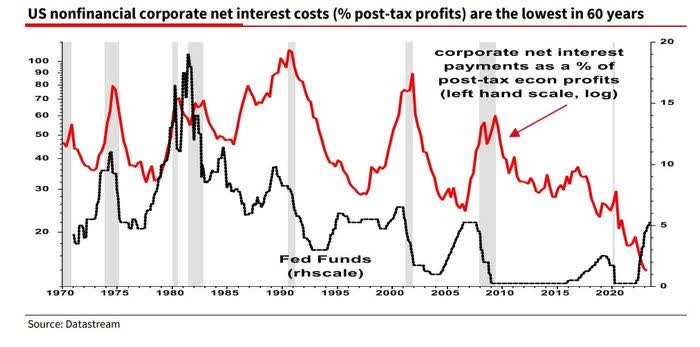

Corporate debt has seen similar changes. The stock of outstanding corporate debt as a share of GDP at 43% is not far from its 2008 peak of 45%, but as a percentage of corporate net worth it is at a 50-year low. Additionally, the debt outstanding is predominately fixed rate and longer term with average maturities ranging from four to 10 years, depending on asset class. The percentage of investment-grade debt maturing after 2028 has risen to 56%, while the percentage of high-yield debt is up to 42%. This means that corporate America is also less sensitive to rising interest rates. In fact, the Fed's rate-hike campaign has been a windfall for most sectors of the S&P 500, because net interest costs as a percentage of post-tax profits have collapsed.

During the ultra-low interest rate period from 2020-2022, corporations refinanced outstanding debt at fixed rates for longer terms in the same way that homeowners refinanced mortgages. When the yield curve inverted, due to the surge in short-term rates, corporations started earning huge sums on their cash balances in the same manner that retail investors are profiting from money market funds. This is boosting corporate profits and helping to fuel capital spending, as net interest costs have plunged to a 60-year low.

{kind=link}

I think the outlook for interest rates to be higher for longer is a farce, given the incoming high-frequency economic data. Regardless, consumers and corporations are far less sensitive to rising interest rates than they have been in the past. With the Fed's rate-hike cycle having likely concluded, and the disinflationary trend intact, a soft landing is looking more probable with each passing month. The correction in stocks over the past two months in combination with the sharp rise in long-term interest rates is creating a lot of doubt, but a recession and bear market are still not in the numbers.

For further details see:

Will The Surge In Interest Rates Cause A Recession And Bear Market?