WLDN - Willdan: Leading The Charge Towards A Sustainable Future

2023-10-14 06:50:30 ET

Summary

- Willdan’s revenue has grown at a CAGR of 19% during the last decade, with EBITDA exceeding this at 25%.

- The company operates in a consulting niche, specializing in utilities and energy. Willdan is currently enjoying a significant upswing in spending due to the clean energy revolution.

- Willdan is essentially positioned to win contracts associated with all large new energy infrastructure projects and any infrastructure upgrades associated with decarbonization. This market is substantial.

- Its quarterly results illustrate this, with strong growth and new customer wins. Management is highly bullish, expecting revenue growth of ~15% in the coming three years.

- Willdan has superior growth relative to its peers but is lacking margins. Although this is concerning, Willdan is trading at a sufficient discount to suggest an upside.

Investment thesis

Our current investment thesis is:

- Willdan is performing extremely well and is positioned to align its growth with the Sustainable energy transition. The company is has deep expertise and a clear focus on this segment, allowing it to differentiate itself from its generalist peers.

Company description

Willdan Group, Inc. ( WLDN ) is a leading provider of professional technical and consulting services. With a focus on delivering innovative solutions, Willdan serves public agencies, utilities, and private industry clients across the United States. Their expertise spans areas like energy efficiency, engineering, and environmental consulting.

Share price

Willdan’s share price has generated impressive gains over the last decade, significantly outperforming the wider market. These returns have been incredibly volatile, with the stock up over 1,000% at one point, before declining to its current level. This volatility aligns with its financial performance, with periods of strong growth and margin expansion, followed by equal declines.

Financial analysis

{kind=link}

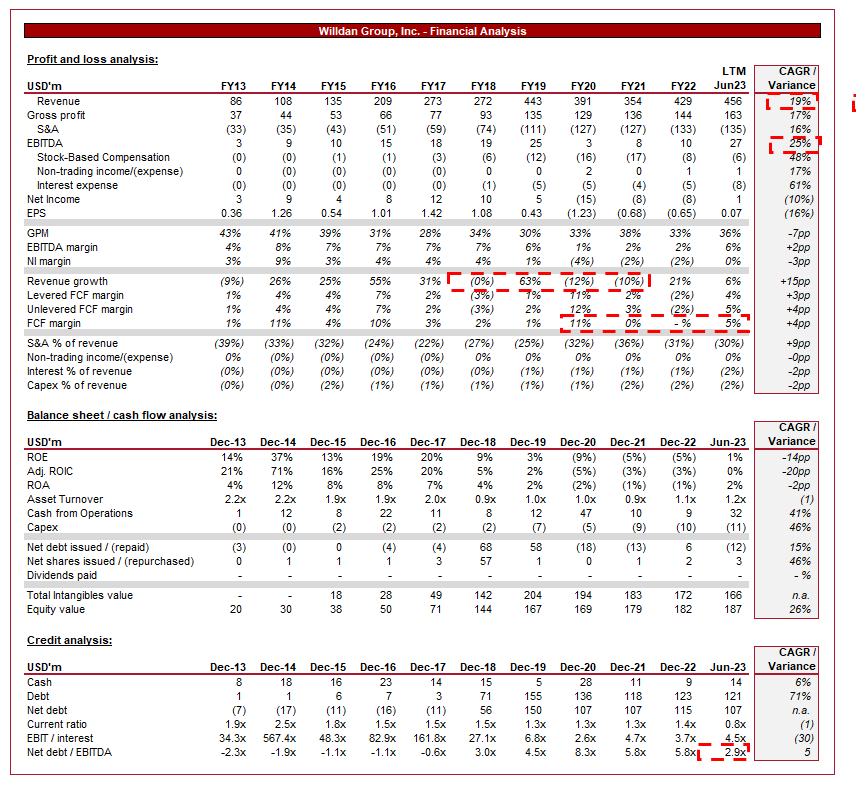

Presented above are Willdan's financial results.

Revenue & Commercial Factors

Willdan’s revenue has grown at an impressive CAGR of 19% during the last decade, with inconsistent gains year-on-year. Its growth trajectory has been materially impacted by various acquisitions and the inherent nature of contractual work. Large wins and roll-offs have and will materially impact the company. EBITDA has broadly exceeded this level, with a CAGR of 25%.

Business Model

Willdan offers a wide range of consulting services, including energy efficiency and sustainability solutions, engineering and planning, public finance and economic consulting, and disaster recovery services. This diversity allows it to target a broad client base, including utilities, and private enterprises.

Willdan has a significant presence in government contracts and consulting, particularly in the US. It assists government agencies at the federal, state, and local levels in addressing critical issues such as energy efficiency upgrades, disaster recovery planning, and infrastructure development. The company has developed a long track record (of over a number of decades in some cases) of high-quality support, utilizing this to develop its brands and pitch for additional work.

The company's consultants are highly specialized in their respective fields, with selective recruitment and a strong emphasis on training. These expertise are critical given the complex nature of the energy industry and the scrutiny associated with being allocated multi-year contracts.

Willdan is currently capitalizing on the growing demand for energy efficiency and sustainability solutions. It is helping clients reduce energy consumption, lower carbon emissions, and achieve sustainability goals. This is a global trend that is supported by societal pressure and government regulation, contributing to a strong tailwind. We believe this transition will materially impact Willdan in two key verticals. Firstly, there is a growing market for renewable energy projects and infrastructure, including solar and wind, offering opportunities for Willdan to design and consult on sustainable energy solutions. Secondly, the public and private sector will be investing heavily in infrastructure upgrades given this is the only material way to reduce climate impact rapidly. This again presents avenues for Willdan to offer engineering and consulting services.

Willdan is currently leveraging technology to enhance its consulting services. It uses data analytics, modeling tools, and software solutions to optimize energy usage, assess infrastructure needs, and make data-driven recommendations. This has significantly enhanced the company’s cross-selling capabilities. The following is an excerpt from Management’s communications illustrating this.

We were recently selected by a major health care provider with over 1,200 facilities. The problem we are working on is how much of their capital budget is allocated to their decarbonization roles. To solve this problem, we are using our front-end consulting services, E3, along with our utility energy-efficiency programs and design/construction services. This decarbonization project is very similar to the LL 97 project for New York City. Where we created a $4 billion budget to help decarbonize over 4,000 buildings.

Finally, Management is active in strategically acquiring companies with complementary expertise, broadening its service portfolio and customer base. These acquisitions have accelerated growth and increased market share, covering any weaknesses or deficiencies in its existing model.

The company has a strong business model. It operates similarly to leading consulting firms, with a range of related services that are complementary (developed organically and through M&A), a focus on reputation building through successful projects, and an emphasis on high-quality recruitment. The key differentiation with Willdan is its focus on the energy segment. Historically, this would represent a partially cyclical but low-risk segment due to its emphasis on multi-year government contracts. Now, however, the company will benefit from an extended tailwind as various institutions seek to decarbonize their infrastructure while others are focused on new clean investments. Willdan will essentially benefit from its historical strengths, while its growth trajectory improves.

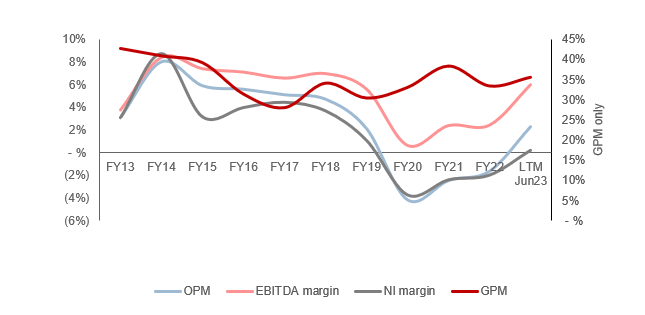

Margins

{kind=link}

Willdan’s margins have been incredibly volatile, aligning with the rest of the business. This is a reflection of the company’s cyclicality and contact-based nature, in conjunction with a relatively fixed cost base. With tailwinds ahead, we expect a normalization in its year-on-year performance, which could mean a smoothing of this profile.

Quarterly results

Willdan’s recent performance remains strong, with revenue growth of +23.5%, +22.8%, +11.7%, and +16.0% in its last four quarters. In conjunction with this, margins sequentially improved relative to prior years.

This may be a surprise to some given the wider macroeconomic environment, with the expectation that spending by clients would soften. This has not been the case. Management is seeing no “signs of a recession”. Labor shortages and Willdan’s capabilities have allowed it to expand its services across the US, with a number of new client wins and upselling opportunities.

Key takeaways from Management’s recent communications include:

- The company’s backlog is extremely good, with its various businesses currently heavily focused on the delivery of existing contracts. Many of these are currently working on their largest projects to date (such as a $120m contract with one of the US’ largest school districts).

- Management is seeing large private infrastructure funds pivoting portfolios to clean energy investments, a broader megatrend we have identified as critical. These investments are supported by Willdan’s capabilities, such as in city engineering, utility programs, grid distribution, and construction management.

- Additionally, the growing demand for electric vehicles, solar, batteries, wind power, and electrification is contributing to renewed opportunities for projects associated with distribution grid planning and forecasting. This covers both its consulting and software services.

- Looking ahead, Management is seeking to resume M&A by early 2024, as market conditions improve and debt markets become more favorable. With its existing trajectory, backlog, and scope for additional M&A, Management is expecting >15% growth in the coming 3 years.

Overarchingly, it appears clear that industry tailwinds and the broader trajectory of its clients have outweighed any economic concerns. Management is very confident of growth and is investing heavily to ensure its various businesses are positioned to maximize their reach.

Balance sheet & Cash Flows

Willdan’s balance sheet is relatively clean. The company has a ND/EBITDA ratio of 2.9x, which implies a comfortable debt position although it lacks scope for further debt without profitability growth. With Management expecting M&A to begin again in the near future, we could see capital raised through equity or more expensive debt, neither of which is ideal in our view.

There is good scope to raise funds through FCF but the volatile nature of its operations means this is highly uncertain. As an example, the company has generated ~$0m between FY21 and FY22. With greater backlog and new business wins, this should improve.

Outlook

Outlook (Capital IQ)

Presented above is Wall Street's consensus view on the coming 2 years.

Analysts are forecasting strong growth in the coming years, with a CAGR of 10% into FY24F. In conjunction with this, margins are expected to slightly improve from the FY22 levels.

These assumptions appear reasonable in our view, as Management communications imply an improvement in the company’s trajectory with tailwinds improving. Its recent contracts alone should ensure HSD/LDD growth, although analysts are likely being conservative with new customer wins. As a reminder, Management is of the belief that when M&A is factored in, growth will reach ~15%.

Industry analysis

{kind=link}

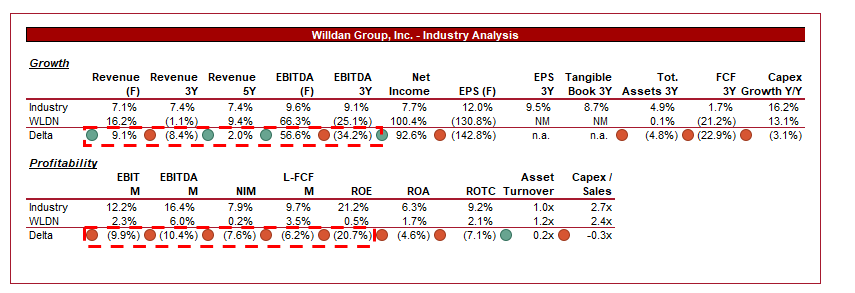

Presented above is a comparison of Willdan's growth and profitability to the average of its industry, as defined by Seeking Alpha (30 companies).

Willdan’s revenue growth has been strong relative to its peers, exceeding the industry on a 3Y basis, with the expectation of this to continue in the forward period. The company’s strong growth is a reflection of the broader energy transition, contributing to increased demand for services beyond the normalized level. Willdan’s margins are its key weakness, with a material deficit to the industry. This is a gap the company is unlikely to close based on historical results.

Given the maturity of the industry, our preference is for margins over growth, which means Willdan should be trading at a discount to its peers.

Valuation

{kind=link}

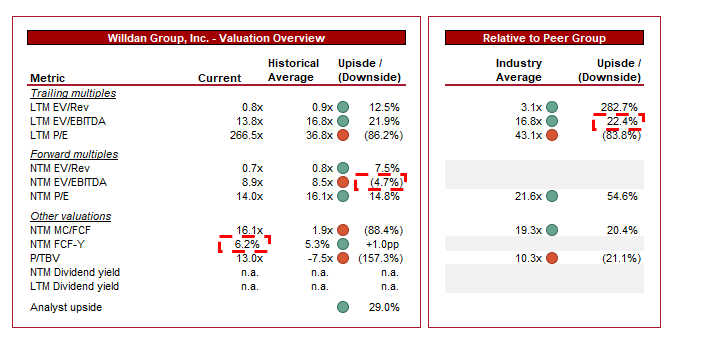

Willdan is currently trading at 14x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average, although not on a NTM EBITDA basis.

Our view is that Willdan should be trading at a small premium to its historical average. Our rationale is that its margins are currently slightly above average, while its growth trajectory is enhanced by the current energy transition that will likely unwind over >10 years. Based on this, Willdan is attractively priced, with a 10-20% upside in our view. Confirming this for us is its NTM FCF yield, which is above average at 6.2%.

Further, Willdan is trading at a 22% LTM EBITDA and 55% NTM P/E discount. This substantially covers the margin weakness in our view, only because the growth runway is sufficiently long to allow for accretive returns.

Both analysts and Seeking Alpha concur with this view, with a Strong Buy rating.

Seeking Alpha

Key risks with our thesis

The risks to our current thesis are:

- Economic conditions affecting clients' budgets - Although this has not occurred thus far, this will continue to be a key risk until expansionary policy returns.

- Regulatory changes impacting key markets - Given the business works heavily with Government agencies, as well as the broader highly regulatory nature of the industry, this is a key risk should actions be taken that harm the company.

Final thoughts

Overall, we believe Willdan represents an attractive investment for those seeking exposure to the energy transition. The business is a leader in this segment, with deep expertise that is underpinned by technological capabilities. This is a relatively wide moat given its historical track record and focus on this segment (which is significantly more niche compared to mainstream, public industries). When considered in conjunction with M&A, we see good runway to achieve Management’s objective of ~15% growth.

Although there is economic uncertainty, the company continues to perform exceptionally well and outperform its peers. We do think its debt could restrict its scope for M&A but the cash flow from its existing contracts will mean, at worst, M&A is delayed.

With an outperformance relative to its peers alongside a discounted valuation, we see upside at its current share price.

For further details see:

Willdan: Leading The Charge Towards A Sustainable Future