WSM - Williams-Sonoma: A Deep Bargain You Won't Want To Miss

2023-06-27 17:10:06 ET

Summary

- Williams-Sonoma's strong lifestyle brands and omnichannel strategy make it an attractive investment opportunity despite recent top-line and margin pressures.

- The company's expansion into B2B and international markets, along with cost-saving initiatives, should support long-term growth.

- The current discounted valuation, share buybacks, and dividend yield offer potential for strong returns for value investors.

It's simply hard to start a new business from scratch. Ask any entrepreneur and they'll probably discourage you from doing it unless if you're a little bit crazy and have a burning desire to do something different.

That's because established businesses have branding that enable them to charge a premium for their goods and services, and which gives them a strong competitive advantage. In the words of Warren Buffett, your brand better deliver something special, else you're not going to get the business.

What may be even better is if that special brand is selling at a bargain price, allowing investors to buy into a moat-worthy business at a discount. Such I find the case to be with Williams-Sonoma (WSM), which is now trades at a PE of around just 9 and sits well below its 52-week-high. I last covered WSM here in December, highlighting its robust customer analytics platform. In this article provide an update on the business and valuation, so let's get started.

Why WSM?

Williams-Sonoma may be thought of as being a furniture company but I regard it as being more of a lifestyle brand for high-end and aspirational tastes. It's successfully adopted an omnichannel strategy and bills itself as being a digital-first, design-led sustainable home retailer.

This strategy makes sense, as modern consumers tend to scope out big ticket home items both online and in-store before making an important decision. WSM's key brands include 'household' names such as Pottery Barn, Williams-Sonoma, and West Elm.

WSM hasn't been immune to economic pressures as outsized spending from consumers flush with cash last year veered in the other direction with a pullback. This was reflected by comparable brand revenue declining by 6% YoY during the first quarter. However, looking longer term, comparable sales are still up by 3.5% on a 2-year basis and way up by 46.5% on a four year basis, compared to 2019.

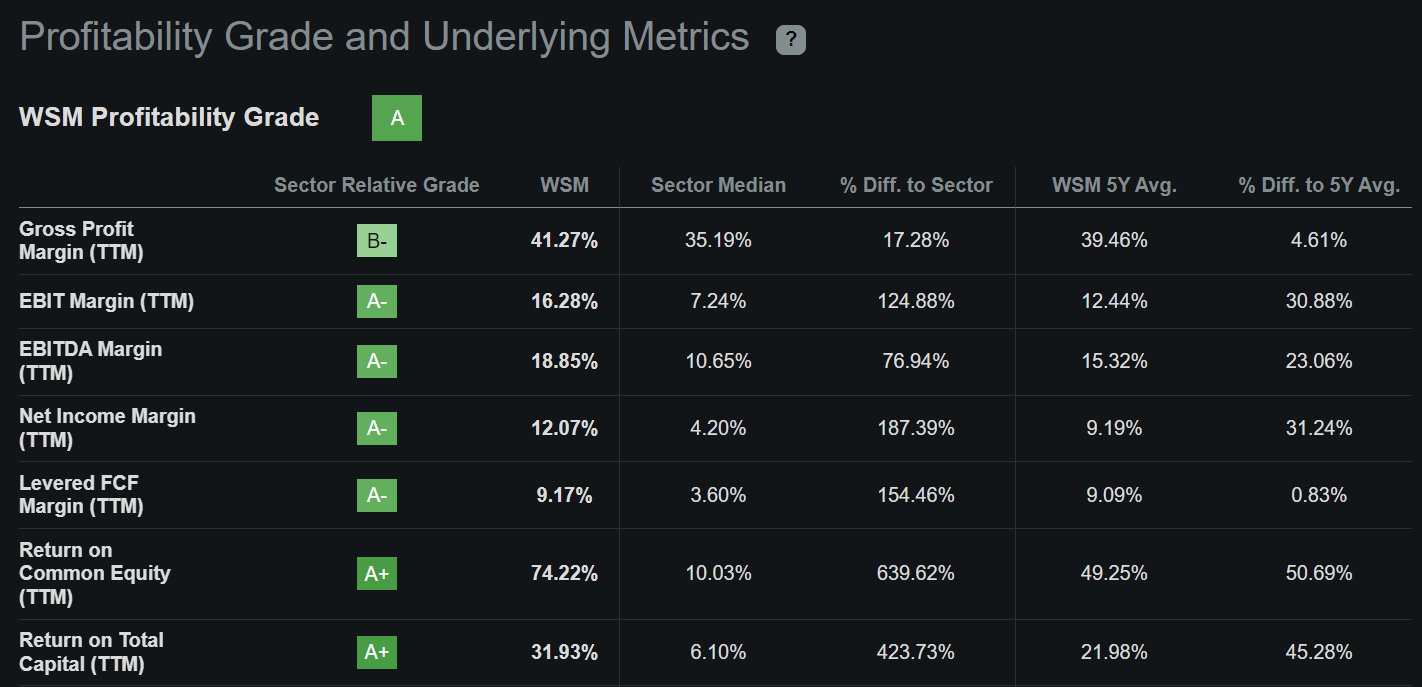

Cost inflation continues to be a headwind for WSM, as reflected by adjusted gross margin declining by 520 basis points YoY to 38.6%, and adjusted operating margin of 12.9% during Q1 is currently below management's long-term target of 15%. However, WSM maintains a strong profitability grade relative to its sector, with TTM EBITDA and Net Income margins that sit well above the sector median, as shown below.

{kind=link}

Looking ahead, I wouldn't expect for revenue to turn back to growth this year, considering that the health of WSM's business remains tied closely that of the housing market, which has been pressured by higher mortgage rates. However, there are signs that mortgage rates should more or less stabilize, considering that Fed is expected to raise rates just two more times for the remainder of the year.

Also, Comerica Bank ( CMA ) recently issued a report last week saying that the homebuilding market is set for a rebound, considering that falling material costs and logistics constraints are in the rear view mirror, and that the existing home resale market is currently muted due to present homeowners being locked in at lower interest rates. This bodes well for WSM, as new homeownership could help drive sales.

Moreover, I would expect for margin pressures to ease as WSM's cost savings initiatives should bear fruit later this year, and as the inventory glut continues to be worked down. The long-term growth thesis remains intact, as WSM's B2B business shows plenty of promise, with contract value grew in the mid-teens during the first quarter with more B2B wins. WSM is also seeing international growth opportunities in India and the Middle East, with new store openings anticipated in those regions, as noted during the recent conference call :

Our brand momentum continues to exceed expectations in the India market, and we are driving growth to retail expansion with the opening of our third West Elm store our second Pottery Barn store and our first Pottery Barn Kids store in Q3 2023. India is a strategic market as we expand globally, and we plan to open additional locations in 2024.

Additionally, we are seeing strength across all of our brands in the Middle East, led by strong design services. We'll be expanding in the region with the opening of an additional Pottery Barn and West Elm store in Saudi Arabia in Q2. Canada is also a highlight with digital representing our biggest growth opportunity for the market.

Importantly, WSM maintains a very strong balance sheet with $297 million of cash on hand and no outstanding debt. This enables quicker shareholder returns as WSM has no interest payments or debt refinancing to be concerned about. Management was able to use excess cash flow and take advantage of the current low valuation to repurchase 3.8% of its outstanding shares during Q1 alone for $300 million. As shown below, WSM has materially reduced its share count by 20% over the past 5 years alone.

{kind=link}

The reduced share count further protects the 2.9% dividend yield, which comes with a low 21% payout ratio and a 5-year dividend CAGR of 15.1%. While I wouldn't expect for the next dividend raise in 2024 to be as high as the recent past, due to management prioritizing share buybacks at the current valuation, growth could pick back up in 2025 for the reasons mentioned earlier.

Lastly, I see the share price of $125.52, as of writing, with forward PE of 9.1 (sitting below its normal PE of 15) as more than reflecting the near-term headwinds, thereby creating value for long-term investors who can afford to wait it out. With my expectation of annual EPS growth normalizing into the mid to high single digit over the next 12-24 months, I believe a forward PE of 11 to 13 is not out of the question, creating the potential for potentially strong double-digit total returns in the near to medium term.

Risks to the thesis include potential for a recession and higher than expected interest rates, which may dampen housing demand and the related spend on WSM's products. Also, higher than expected inflation in the near term may exert more margin pressure on the company.

{kind=link}

Investor Takeaway

Williams-Sonoma has strong lifestyle brands that connect with customers through an omnichannel strategy. While it has experienced top-line and margin pressures like most retailers today, I see the long-term growth thesis as being intact, as it expands into B2B and international markets.

I see the current valuation as more than baking in near-term headwinds, while accretive share buybacks at low prices and the dividend make for compelling shareholder returns. As such, value investors may be well-served to take a hard look at WSM at the current discounted valuation.

For further details see:

Williams-Sonoma: A Deep Bargain You Won't Want To Miss