WSM - Williams-Sonoma: A Great Dividend Growth Stock On Sale

2023-11-17 11:20:07 ET

Summary

- In due time, the dividend growth investing strategy can help you achieve financial freedom.

- Williams-Sonoma's well-known brands helped it to hold up well in a difficult operating environment.

- A flawless balance sheet is another reason to like the company.

- Williams-Sonoma appears to be meaningfully discounted at its current share price.

- The stock could outperform the S&P 500 index through the next two years and perform about in line with it in the next 10 years.

As I've noted time and time again, the goal of investing is to substantially improve your finances over the long run. Depending on life circumstances like marital status, children, philanthropic endeavors and the like, everybody's "number" needed to attain financial independence is going to look different.

There are different investing strategies for different risk tolerance levels and investing objectives. However, the route that I have been taking and plan to continue doing so is through mostly buying and holding dividend growth stocks. This is because great businesses can steadily up their payouts to shareholders. Time plus capital deployment plus patience gives me the best shot at eventually reaching the finish line where my passive income exceeds my expenses.

One of the core holdings within my portfolio is Williams-Sonoma (WSM). As my 11th largest investment by market value, the company comprises 1.6% of my individual stock holding portfolio. For the first time since last month , let's take a look at the company's recent operating results and its valuation to understand why I'm maintaining my buy rating.

{kind=link}

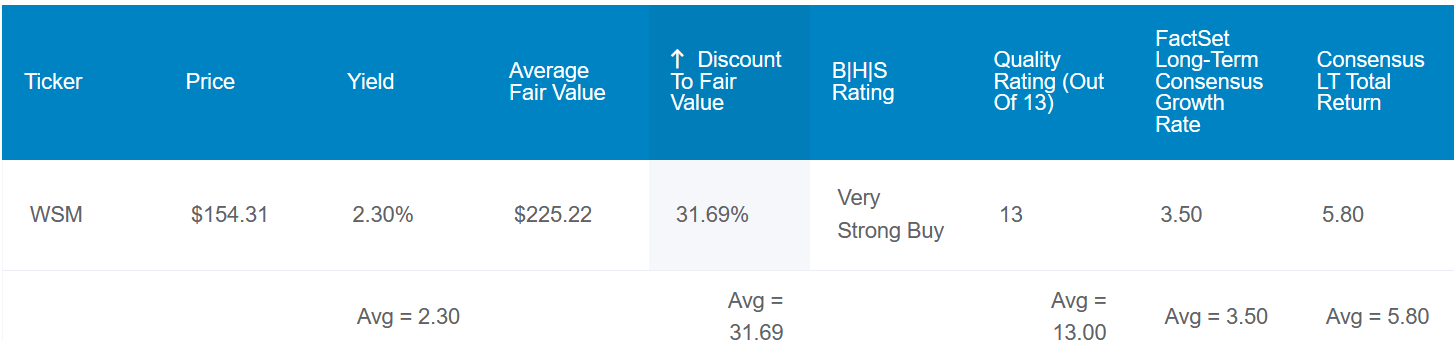

Williams-Sonoma's 2.2% dividend yield is better than the 1.5% yield of the S&P 500 index ( SP500 ). The company's 25% EPS payout ratio is far below the rating agencies' safe guideline of 60% for its industry.

Though Williams-Sonoma isn't rated by S&P, the company's strong balance sheet would earn it an effective A+ credit rating per Dividend Kings. That implies the company's risk of going bankrupt by 2053 is just 0.6%. For these reasons, Dividend Kings projects a mere 0.5% probability of Williams-Sonoma cutting its dividend in an average recession and only 1% in a severe recession.

{kind=link}

Williams-Sonoma is a fundamentally sound business that has gone on sale. Using historical fair value metrics like P/E ratio and dividend yield, Dividend Kings assigns a $225 fair value to shares of the stock. Against the $169 share price (as of November 16, 2023), the high-end retailer is 25% undervalued.

If the company grows 1% ahead of analyst expectations (Williams-Sonoma has a history of topping the analyst consensus) and reverts to fair value, here is what total returns could look like for the next 10 years:

- 2.2% yield + my 4.5% annual earnings growth estimate + 2.8% annual valuation multiple expansion = 9.5% annual total return potential or a cumulative 148% total return versus the 9% annual total return potential of the S&P 500 or a cumulative 137% total return

Williams-Sonoma Delivered A Robust Third Quarter Despite Challenges

Williams-Sonoma Q3 2023 Earnings Press Release

Williams-Sonoma's net revenue declined 15.5% year-over-year to $1.9 billion in the third quarter ended October 29, missing the analyst consensus by $90 million . Yet, the company's results for its third quarter were solid overall.

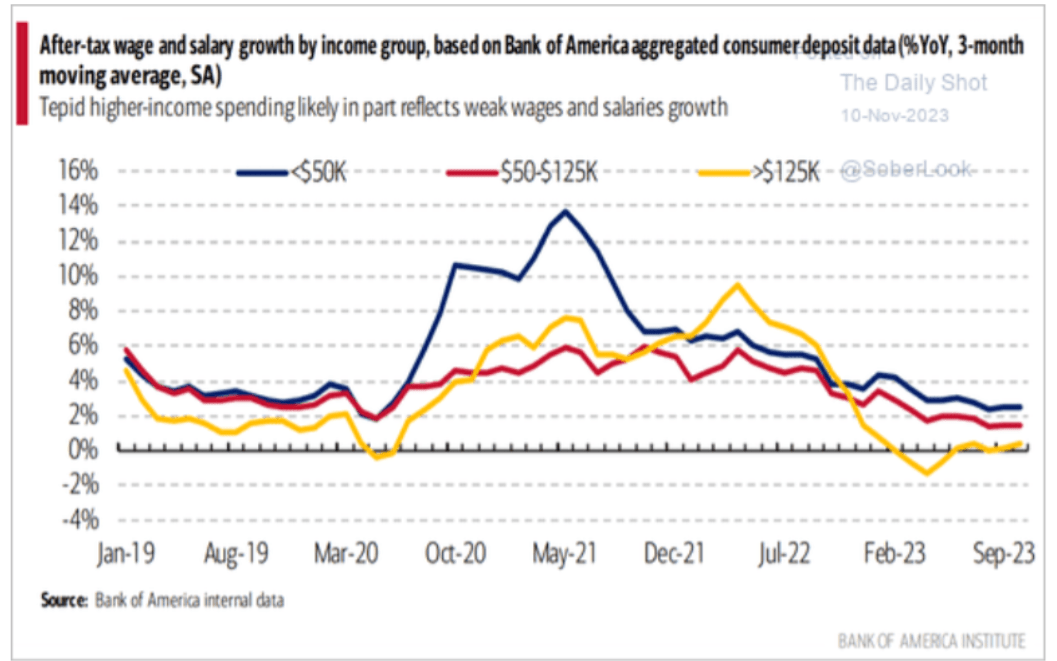

Williams-Sonoma's comparable brand revenue dropped by 14.6% over the year-ago period during the third quarter. Across the board, comparable brand revenue contracted. This was driven mostly by double-digit decreases in Pottery Barn and West Elm, as well as single-digit dips in Williams-Sonoma and Pottery Barn Kids and Teen. Why would I not be worried about this seemingly poor topline performance?

{kind=link}

Well, it's not a secret that Williams-Sonoma's target audience is those in the upper-income bracket. As illustrated above, after-tax wage and salary growth of high-income earners has been trailing lower-earning counterparts for a while now. With these figures in mind, Williams-Sonoma's president and CEO Laura Alber's remark of hesitancy toward high-ticket discretionary furniture spend makes sense. Unsurprisingly, this has been detrimental to Williams-Sonoma.

There's still good news, though. While the company's 2-year comp is -6.5%, the 4-year comp is substantially higher at +34.8%. This goes to show that Williams-Sonoma's revenue base can keep growing throughout a full economic cycle.

Another positive is that the company's supply chain efficiencies and insistence on full-price selling propelled non-GAAP operating margin to a third-quarter record of 17%. Combined with a moderate reduction in its outstanding diluted share count, this is how non-GAAP diluted EPS fell just 1.6% over the year-ago period to $3.66. That was $0.32 ahead of the analyst consensus.

Operating fundamentals aside, Williams-Sonoma's balance sheet is also exceptionally strong. As of October 29, the company had no long-term debt and $698.8 million in cash and cash equivalents (all details sourced from Williams-Sonoma's Q3 2023 Earnings Press Release ).

The Company Is Minting Major Free Cash Flow

If Williams-Sonoma's decent operating results in a tough environment and its sizable cash position weren't enough to convince you, its free cash flow generation might do the trick.

The company's 10-Q filing for the third quarter won't be out for a while longer. But through the first two quarters of this fiscal year, Williams-Sonoma put up $715 million in operating cash flow. Compared to the $92.9 million in property and equipment purchases, this is a free cash flow of $622.1 million.

Against the $116.6 million in dividends paid during that time, this equates to a modest 18.7% free cash flow payout ratio. That also explains how Williams-Sonoma repurchased $310 million of shares in the first half, which can keep dividend growth exceeding bottom line growth moving forward (info according to page 8 of 31 of Williams-Sonoma's 10-Q filing ).

Risks To Consider

Williams-Sonoma is deservedly considered an ultra SWAN by Dividend Kings. However, it still has risks that investors must be able to tolerate before becoming a shareholder.

As I noted in my previous article, the state of the economy remains a risk to Williams-Sonoma. Analysts expect that the company will return to growth in its new fiscal year beginning in less than three months. But if a more severe recession hits the U.S. economy, these estimates could be revised downward as consumer spending further weakens. This could weigh on its stock performance in the near term.

As a consumer-facing company, Williams-Sonoma's reputation as a brand is paramount to its success. If anything were done to jeopardize its highly trusted brand portfolio, the company's fundamentals could be materially damaged.

Summary: Buy Williams-Sonoma And Sleep Well At Night

{kind=link}

{kind=link}

Williams-Sonoma's operating fundamentals and balance sheet make it an objectively high-quality business. To be clear, that doesn't mean the stock isn't volatile, with a 1.5 beta over the last five years.

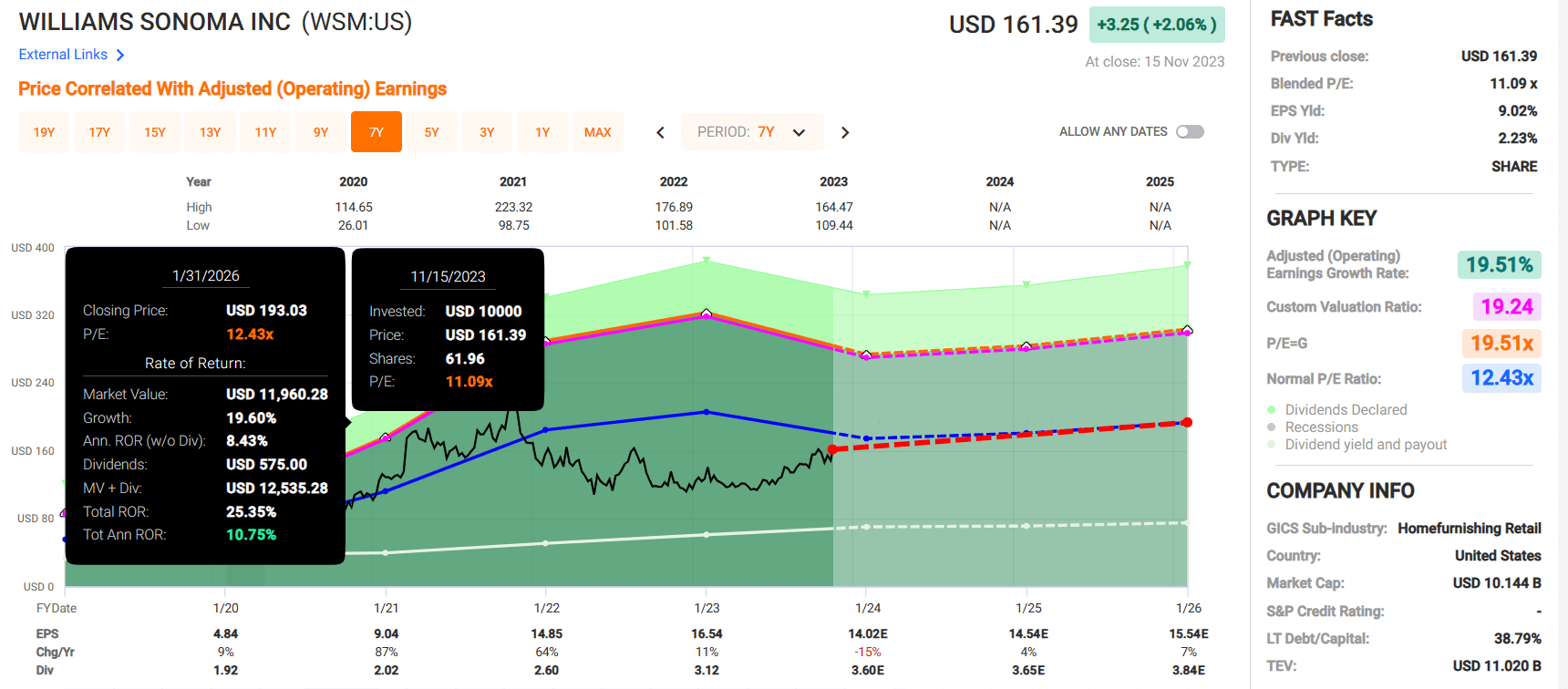

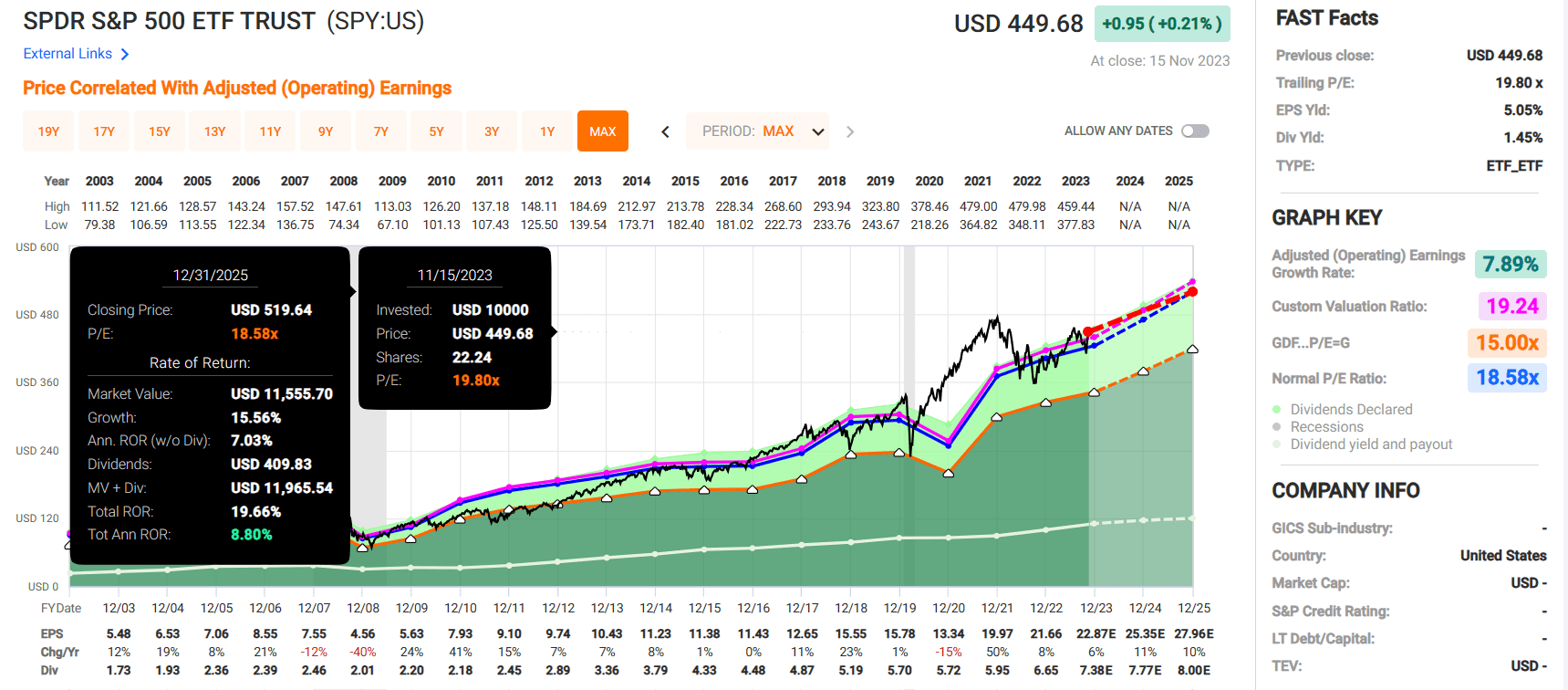

For those who can tolerate this volatility, Williams-Sonoma arguably has an attractive risk-reward profile. In assuming a reversion to the historical P/E ratio of 12.4 over the last seven years and growth as expected, shareholders stand to gain nearly 11% annually in the next two years. That's better than the 9% annual returns that the SPDR S&P 500 ETF Trust (SPY) is currently projected to deliver over that time. Thus, this is why I rate shares of Williams-Sonoma a buy.

For further details see:

Williams-Sonoma: A Great Dividend Growth Stock On Sale