WSM - Williams-Sonoma: A Robust Retailer With A Shareholder-Friendly Strategy

2023-07-28 09:36:47 ET

Summary

- Williams-Sonoma has a strong online presence and strong revenues, making it resilient in the evolving retail landscape.

- The company's commitment to shareholders, including dividends and stock buybacks, makes it an attractive investment.

- While there are potential economic challenges, Williams-Sonoma's strong brand, operational agility, and shareholder-friendly strategies make it a strong buy.

Williams-Sonoma (WSM) has shown resilience and adaptability in the evolving retail landscape. With a robust online presence, growing revenues, and a strong commitment to shareholders, the company stands strong despite potential economic challenges. Given its solid brand, operational agility, and most importantly its shareholder-friendly strategies, I rate Williams-Sonoma as a strong buy at current levels and is a must add for a fire-and-forget portfolio.

About Williams-Sonoma

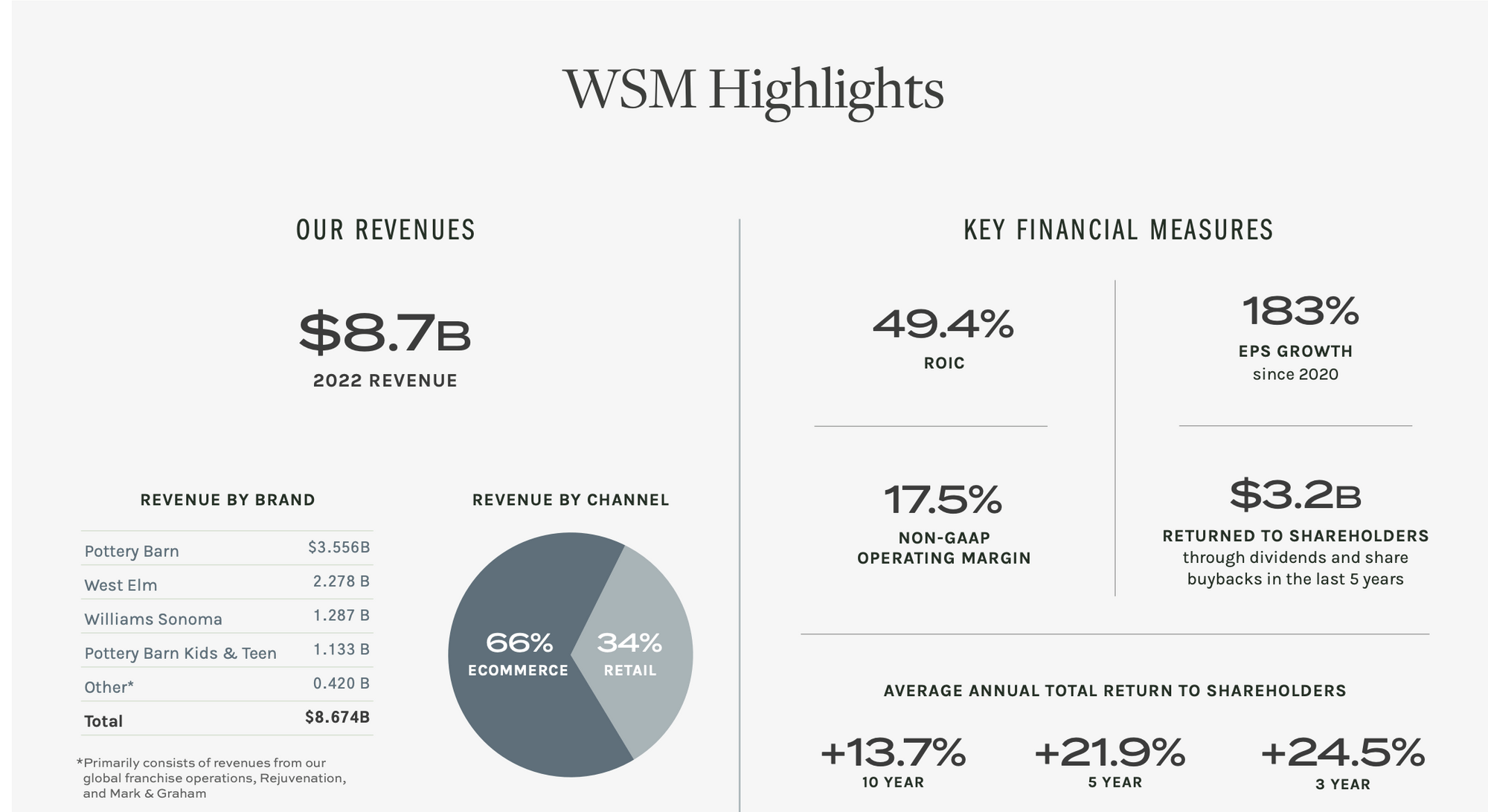

Williams-Sonoma, Inc. is a leading American retailer specializing in high-quality kitchenware and home furnishings. Established in 1956, the company operates through both e-commerce and retail segments, reaching a broad customer base. Its portfolio includes distinguished brands such as Pottery Barn, West Elm, and its namesake, Williams-Sonoma. Leveraging technology, Williams-Sonoma integrates its online and in-store operations to provide a seamless shopping experience. With its strong brand portfolio and commitment to innovation, the company holds a robust position within the home goods industry. While the company adorns the moniker Williams-Sonoma, over half of the revenue comes under the Pottery Barn Brand.

{kind=link}

Throughout its history, Williams-Sonoma has consistently demonstrated an ability to adapt and thrive amid changing consumer behaviors and technological shifts. This forward-thinking strategy is evident in the fact that nearly two-thirds of the company's revenue is now generated through online sales, reflecting its successful transition into the digital age. This substantial online presence has played a vital role in creating a seamless shopping experience for its customers, which, in turn, has fortified the company's brand appeal and market standing.

Driven by changes in consumer behavior due to the pandemic, more people were spending time at home and investing in home improvements. Williams-Sonoma's revenue surged from $5.5 billion in 2018 to an impressive $8.7 billion in 2022 and as they got bigger so did the strength of their brand. The presence of physical stores complements the company's e-commerce platform, giving customers the added benefit of experiencing the products firsthand — a unique advantage not typically offered by online-only retailers.

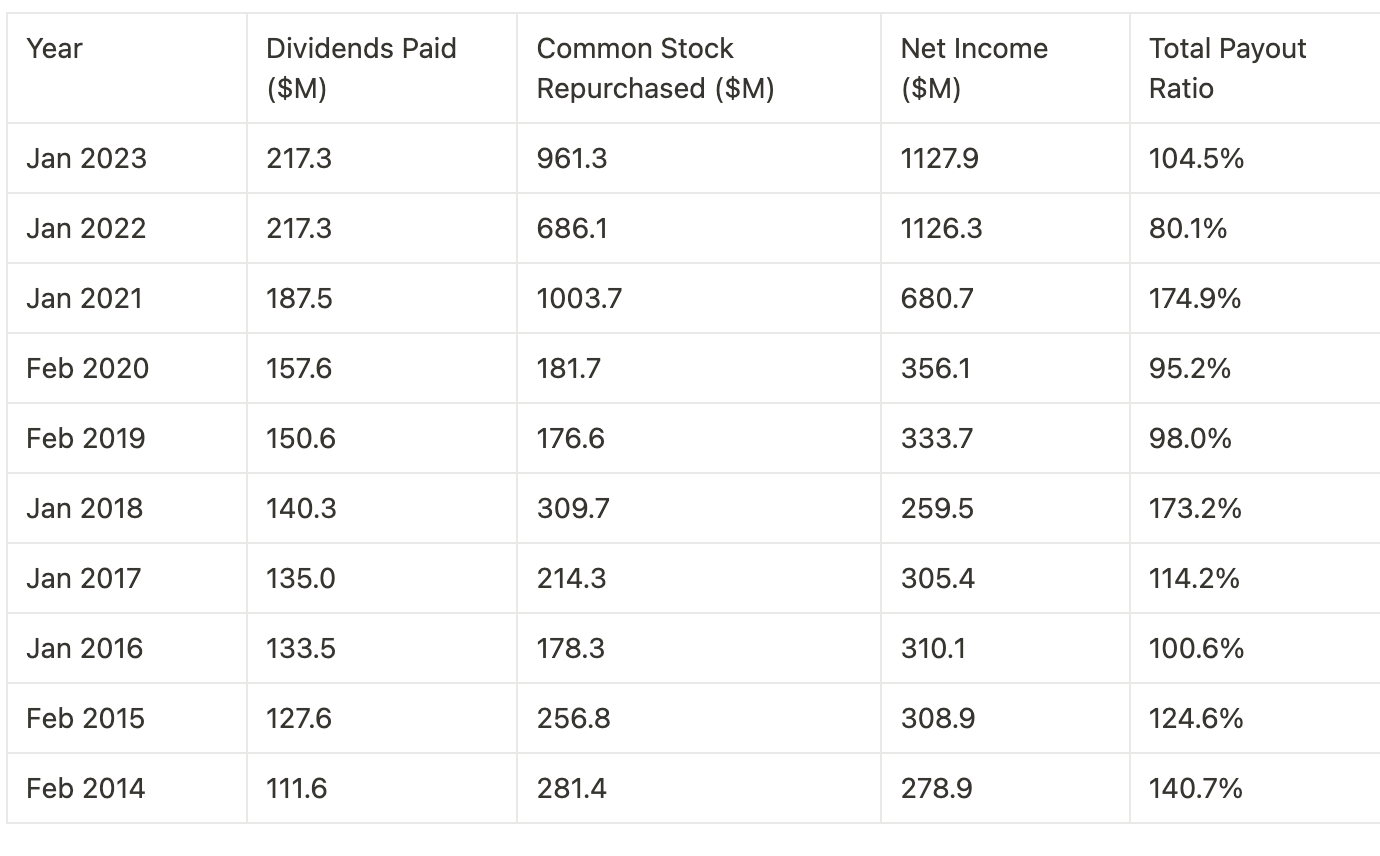

Williams-Sonoma has also displayed consistent growth on the shareholder front. The company's net income has nearly tripled from $333 million in 2019 to a remarkable $1,126 million in January 2022. Over the past decade, the company has exhibited a strong commitment to maximizing shareholder value, channeling nearly all of its net income back to investors through dividends or stock buybacks.

While future total payout ratios may not remain above 100% as they have in some previous years, the company's track record suggests that a significant portion of net income will continue to be distributed to shareholders. This approach underscores Williams-Sonoma's ongoing commitment to delivering value to its investors, even as it navigates the evolving and challenging retail landscape.

{kind=link}

Risks and Market Pricing

{kind=link}

While growth during Covid was a great tailwind, in the uncertain economic landscape of 2023, this positive growth trajectory appears to be losing steam. A crucial factor in this slowing trend is the impending resumption of student loan payments come September. The company's sales, particularly for its more premium product lines, are likely to take a hit. Higher-end products often require a degree of discretionary income, and with the additional financial burden of loan repayments, many consumers might resort to cutting back on such expenses.

The anticipated decrease in sales is expected to trickle down to the company's earnings. However, some market analysts argue that there could be an overreaction to the anticipated effects on sales and earnings. It is essential to keep in mind that markets can sometimes be swayed more by sentiment and speculation than by hard data.

To counteract this potential downturn in sales, Williams-Sonoma is adopting a strategic expansion in to business-to-business (B2B) sales. On the operational front, B2B sales might not be a dramatic departure from their existing customer sales model, given the potential similarities in product offerings. The primary difference would likely be larger order quantities and an increased level of designer involvement, given the nature of corporate clients and larger projects. The extent to which Williams-Sonoma, or indeed any single firm, can penetrate this market is still an open question.

What remains consistent in Williams-Sonoma's favor, however, are the high-profit margins on its products. These margins not only provide a robust financial buffer against competitors and slowing sales but also afford the company some flexibility. If necessary, they could strategically lower prices to stimulate demand without significantly jeopardizing profitability. This flexibility could be a game-changer in maintaining a competitive edge, demonstrating the company's resilience in the face of changing market dynamics.

Conclusions

{kind=link}

On a forward earnings basis, Williams-Sonoma is currently trading at a P/E 10.22 and a EV/EBITDA of 7.12 while 10-year treasuries trade at ~4% (P/E 25x).

Such a valuation might be justified for businesses encumbered with hefty debt or those lacking in capital efficiency or product market fit. However, it's challenging to apply this to a company like Williams-Sonoma, which is profitable, boasts operational agility, and carries no debt on its balance sheet.

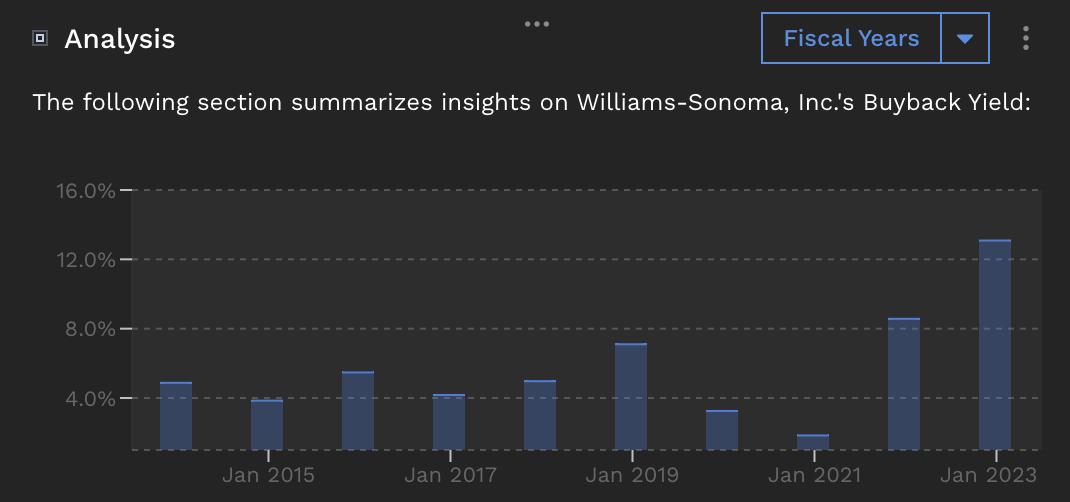

If Williams-Sonoma's shareholder returns, specifically its stock buyback program prior to the Covid-19 pandemic, the company's management consistently repurchased shares at an average buyback rate of about 5% per year. In addition, they maintained a steadily growing dividend, underscoring their commitment to returning value to investors. This level of investor-focused return seems to be undervalued by the current market.

{kind=link}

Admittedly, there is some uncertainty surrounding potential recession risks and the potential impact of student loan repayments resuming on sales. However, there should be no doubt about management's ability and dedication to generating shareholder value. With their robust branding, superior product offerings, and proven resilience, Williams-Sonoma is well-positioned to weather any temporary economic downturn that may arise.

Given the company's compelling fundamentals and the limited downside risks at its current price, I argue that Williams-Sonoma is a worthy long-term investment. To put it more strongly, I believe that this stock is a 'Strong Buy' at any price below $150 and a Buy up to ~$190. This is compounder that will reward the patient investor.

For further details see:

Williams-Sonoma: A Robust Retailer With A Shareholder-Friendly Strategy